The AI server market is booming and so are the AI chip markets.

I’ll talk about 2 prestigious companies right in the mix of things.

For long-term portfolios, it’s essential to not miss out on these supercharge growth companies.

I just don’t think that average investors will be able to make up the performance if they miss the boat of these 2 companies. The law of large numbers will just put you too far behind.

All the hot new money is going into AI which adds to the momentum of the share price trajectories.

Even the old money, after not being convinced by Bitcoin, is starting to come around to AI partly because most of the companies involved in AI are publicly listed companies on the New York Stock Exchange.

It makes it a lot easier when the source of exponential growth isn’t on some alternative exchange in some alternate currency in some backwater jurisdiction.

With a few clicks and moving a few dollars here and there, investors can be part of the AI future whether it be in AI chips or AI servers like the companies I am about to talk about.

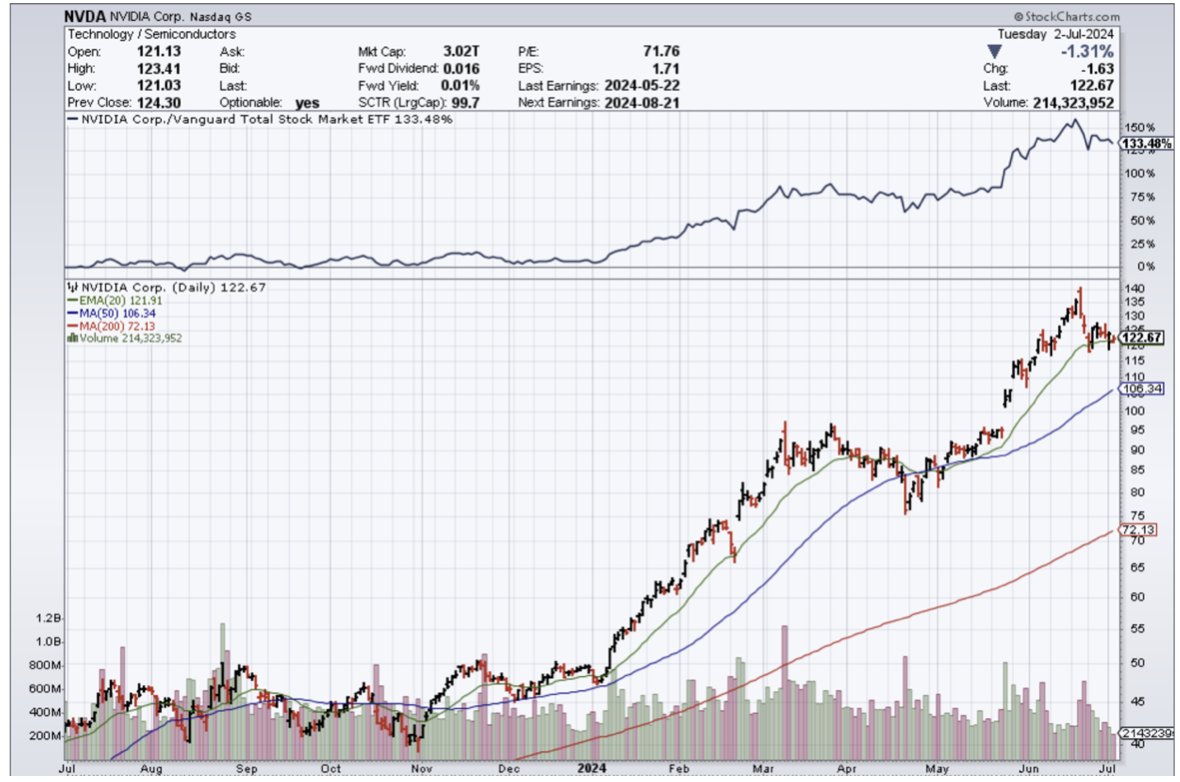

What up with Nvidia?

Nvidia (NVDA) dominates an impressive 94% of the AI chip market. It’s basically a monopoly or close to it.

Revenue is rising a stunning 262% year over year.

Even more interesting, emerging growth avenues in the nascent AI market indicate that Nvidia could end up doing even better than that.

For instance, governments are also betting the ranch on AI and this stable source of revenue will highly likely grow substantially for the foreseeable future.

Nvidia's customer base is diversifying beyond the major cloud infrastructure providers that have been deploying its chips in large numbers to train and deploy AI models.

Spending on AI chips is expected to grow more than 10-fold over the next decade, generating $341 billion in revenue in 2033 compared to $23 billion last year.

Nvidia should remain the Tom Brady of AI stocks as the race to develop AI applications by companies and governments alike has created a secular growth opportunity.

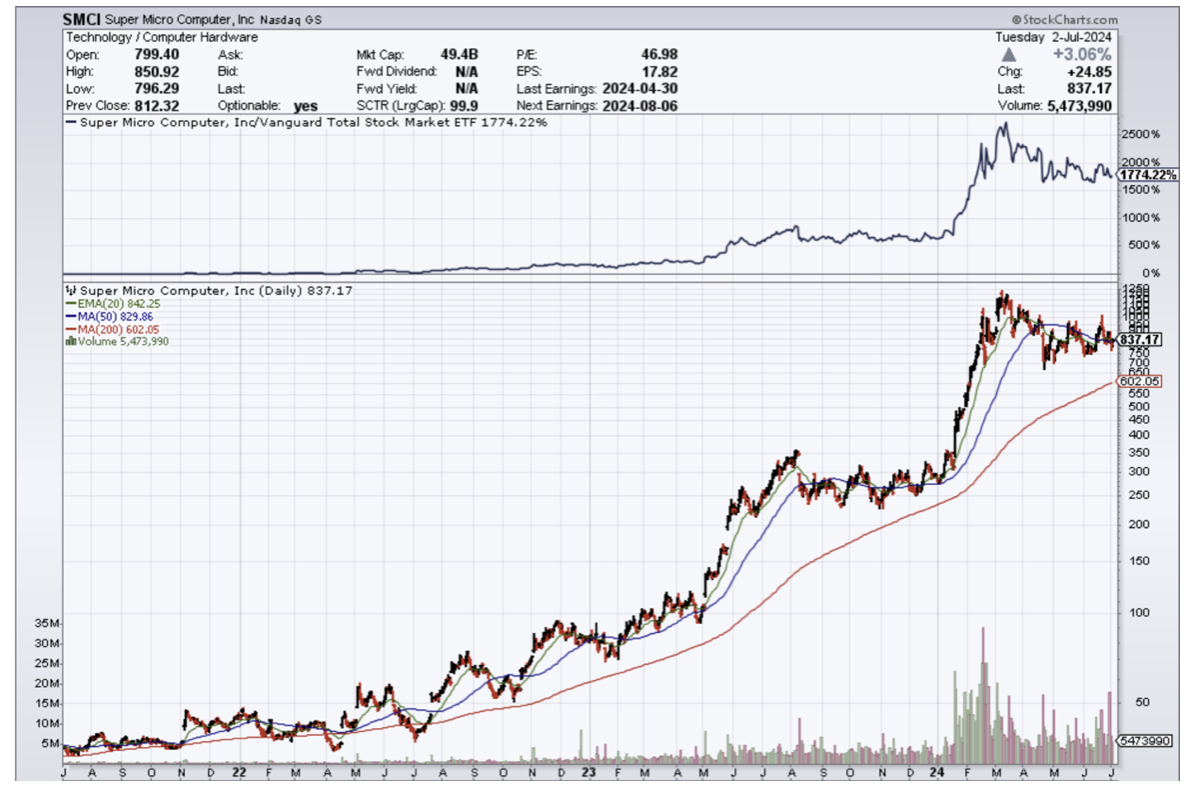

What about Super Micro Computer?

Supermicro's future prospects are attached to some extent with that of Nvidia’s.

Data center operators require server rack solutions of the type that Supermicro sells to mount the processors sold by Nvidia and other chipmakers.

Revenue jumped 200% year over year and Supermicro isn't all that far behind Nvidia when it comes to how AI has supercharged its fortunes.

I expect its top line to nearly double over the next couple of years.

Demand for AI servers is expected to expand at a compound annual rate of 25% through 2029.

Supermicro is growing at a faster pace than the AI server market right now. As it turns out, its growth is faster than that of more established companies such as Dell.

How to invest?

Supermicro is cheaper than Nvidia and Nvidia’s run-up to a more than $3 trillion market valuation has got to scare some people with sticker shock.

People with a time advantage of more than a few years should invest in Super Micro, whereas investors looking for that quick sugar high should buy the dips in Nvidia.

In short, anyone under the age of 40 and many years in front of them should invest long-term in Super Micro at a market cap of $50 billion. With Nvidia, I could easily see its market cap climbing to $4 trillion soon, but a wicked pullback would mean its market cap going from $4 to $3 trillion.

Either way, these are two tech firms with great prospects in the current and future.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-07-03 14:02:272024-07-03 14:12:13Should I Invest In AI Chips Or AI Servers?

SoftBank Group raised about $1.86 billion via dollar and euro bond sales in one of the biggest foreign-currency deals by a Japanese company this year.

This is big news.

Softbank is one of the most prominent venture capitalist funds in the world and they plan on deploying the capital solely into generative artificial intelligence.

Many of these heavyweights from Asia, and the Middle East, and other billionaires around the finance world are chomping at the bit to get a piece of American AI firms.

This trend is in the early innings and won’t slow down.

It’s interesting that Softbank raised the currency in dollars and euros which is another bet on the Japanese yen strengthening and the Fed cutting rates.

The Yen has been one of the worst-performing currencies in the past few years and there is a chance this move could blow up in Softbank’s face.

The dollar is strong and has been increasingly strong lately as the Fed stays higher for longer.

However, if the dollar does get stronger, it will mean that Softbank will need to pay higher costs. Even that said, they will still dive head-first into AI.

My belief is that their CEO Masayoshi Son, who I know very well, will bet the ranch on AI considering he sold out of his Nvidia shares in 2022 and calls it the “fish that got away.”

He rues leaving hundreds of billions of dollars in profits on the table and I don’t believe he is willing to allow that to happen again.

So he will approach these new investments as an “all or nothing” all guns blazing type of strategy.

In its first non-yen debt offering since 2021, billionaire Masayoshi Son’s company priced two dollar tranches totaling $900 million and two euro tranches raising €900 million ($964 million).

It’s not only Softbank, it’s also other Japanese companies looking for ample liquidity.

SoftBank joins a bond bonanza by issuers from Asia and elsewhere including even bigger deals from fellow Japanese borrowers such as Takeda Pharmaceutical and Rakuten.

The Japanese firm this year directly invested $200 million into Tempus AI, a startup that analyzes medical data for doctors and patients to come up with better treatments. More recently, it backed Perplexity AI at a $3 billion valuation, betting on a firm that aims to use AI to compete with Alphabet’s Google search.

Longer term, SoftBank is working on a plan to deploy some $100 billion into AI-related chips in a project dubbed Izanagi, Bloomberg News reported in February.

My belief here is that Softbank and other Japanese companies are on the verge of deploying over $1 trillion of new money into generative artificial companies in America.

There is a reason why leading AI companies like Nvidia (NVDA) have surged to the skies and a lot of it is foreign money coming chasing the new hot trend.

I don’t believe this trend will stop will money from all corners of the globe from flooding the US markets chasing the few quality AI companies.

The ultimate takeaway is that the best companies connected the generative artificial intelligence are at the beginning of a huge run in share price that will extend years into the future.

Don’t fight the trend – especially the biggest ones in the world.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-07-01 14:02:502024-07-01 14:33:23Softbank Bets The Ranch On AI

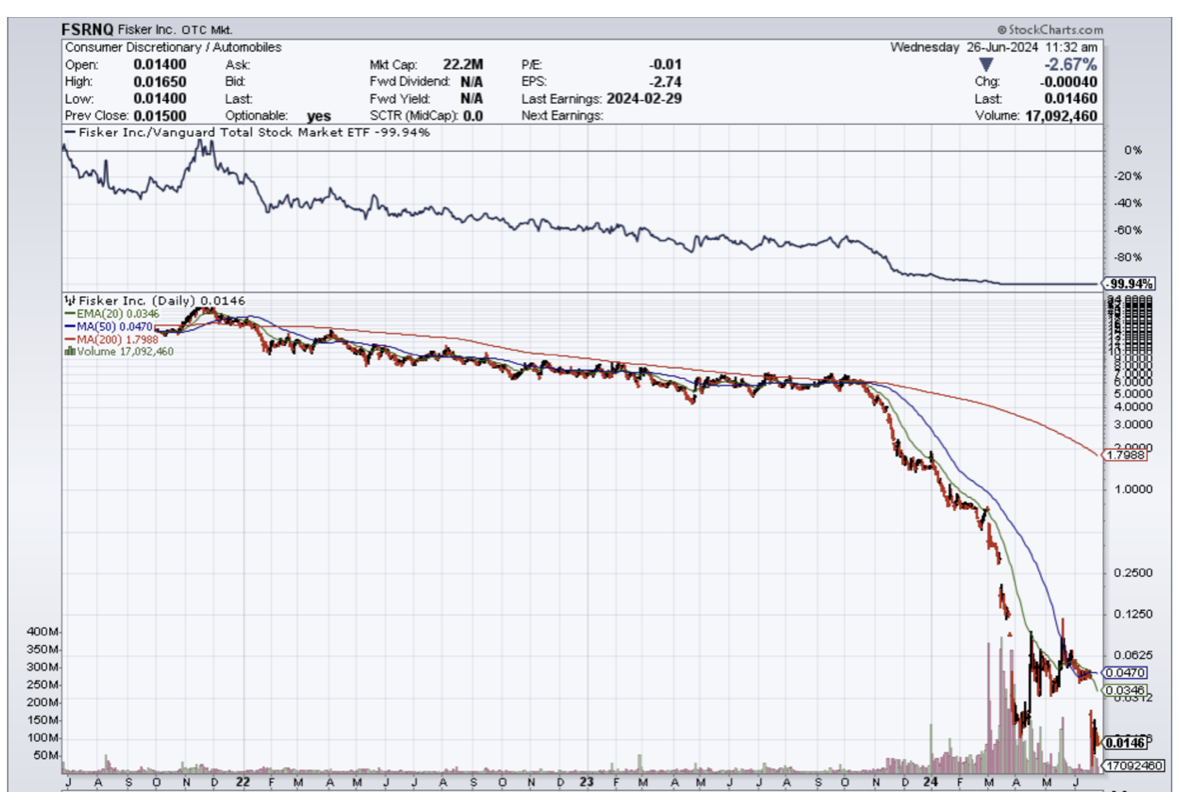

Fisker (FSRNQ) is bankrupt and I can tell you that I am not surprised.

The sushi has hit the fan.

The non-Nvidia (NVDA) tech firms minus big tech are really having a tough time staying liquid and dare I might say profitable.

Many already knew Fisker was in trouble.

They also have a terrible car which doesn’t help its case.

If Tesla (TSLA) is having a hard time selling EVs then imagine what it is like for Fisker to sell an utter clunker.

FSRNQ’s car has been coined as the worst EV on the market by many prominent bloggers.

Fisker management told us they might run out of cash before 2024 is over.

Definitely not shareholders like to hear in an industry that is looking more like a race to zero than an industry able to price itself at a premium.

I believe many car executives are ruing the fact of the multi-decade knowledge transfer to the Chinese about building quality cars.

How do we take tabs of the situation at Fisker?

It only sells one car called the Fisker Ocean electric SUV. Last year, around 10,000 of the SUVs were made but only about half had been delivered to customers.

In a recent interview with Automotive News, the company’s founder and CEO Henrik Fisker admitted that the Ocean had quality problems. He blamed the issues on software from different suppliers that worked poorly together and said they were being addressed through updates.

Worldwide sales of plug-in vehicles could rise 21% this year, which represents a smaller rise than the 35% increase in 2023.

The company listed between $500 million and $1 billion of assets, and between $100 million and $500 million of liabilities, in its petition filed in Delaware. The filing protects Fisker from creditors while it works out a plan to repay them.

While Fisker Ocean sport utility vehicle production started on schedule in November 2022, the first SUVs lacked basic features including cruise control. The California-based company told customers it would deploy capabilities it had promised them the following year, via over-the-air software updates.

Fisker produced 10,193 Oceans last year but delivered only 4,929 vehicles to customers.

Fisker follows a handful of other EV startups into bankruptcy, including Charge Enterprises, the installer of EV charging stations that filed for Chapter 11 protection in March. Other EV makers that have filed for bankruptcy include Lordstown Motors, Proterra and Electric Last Mile Solutions.

Anecdotally, EVs didn’t calculate properly how difficult it is to convince the 2nd wave of buyers.

For example, everyone in my family that will buy an EV has already bought one.

One Gen Z relative of mine swears he will never buy an EV because it doesn’t amount to more than a “toy car” with a battery that needs to be plugged in. He prefers a Ferrari or a Maserati where he can hear the engine roar. There is a high chance he will never be persuaded to buy an EV or if he does get persuaded, it will take 10-20 years for him to come around.

That is what EV makers face in bringing forward the next buyer.

Therefore, look at the bottom of the barrel EV production, they are all facing Chapter 11 and this is just the beginning.

Fisker’s share price peaked at around $30 per share in 2021 and now shares trade at $.02 per share. I would not buy the stock even at these levels.

Tesla’s halving of its share price also most likely means it is fairly priced for right now as we wait for a catalyst to send us either up or down.

The walls are closing in on the EV industry in the short-term and I advise readers to head to higher ground, let’s say the chip industry for a better crack at tech stocks.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-26 14:02:042024-06-26 14:17:17Fisker Blows Up

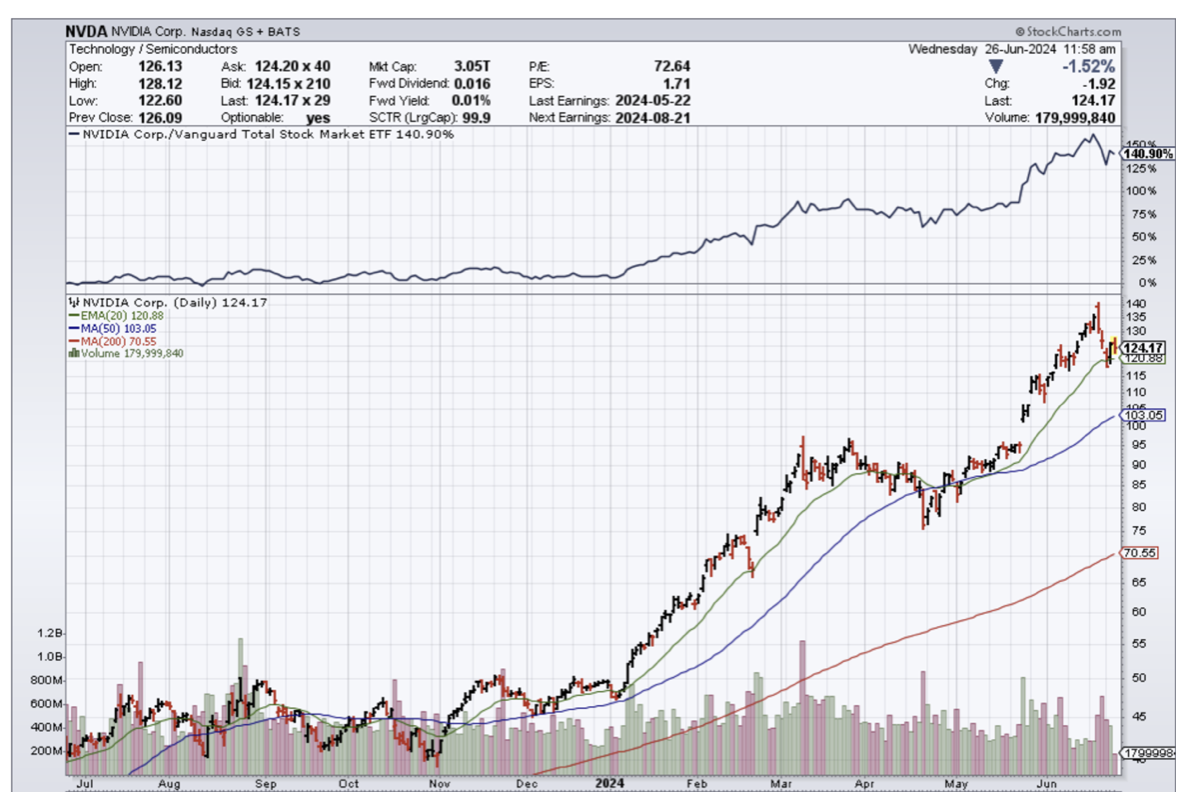

We have a three-horse race underway in the stock market right now between Apple (AAPL), Microsoft (MSFT), and NVIDIA (NVDA). One day, one is the largest company in the world, another day a different company noses ahead.

And here’s the really good news: this race has no end. Sure, (NVDA) has far and away the most momentum and it should hit my long-term target of $1,400 this year, giving it a market capitalization of $3.44 trillion. (MSFT) and (AAPL) will have to stretch to make another 20% gain by year-end.

Who will really end this three-year race? You will, as the benefits of AI, hyper-accelerating technology, and deflation rains down upon you and your retirement portfolio.

Here is the reality of the situation. The Magnificent Seven has really shrunk to the Magnificent One: NVIDIA. (NVDA) alone has accounted for 32% of S&P 500 gains this year. There are now 400 ETFs where (NVDA) is the biggest holding, largely through share price appreciation. These dislocations in the market are grand. This will end in tears….but not yet.

Dow 240,000 here we come!

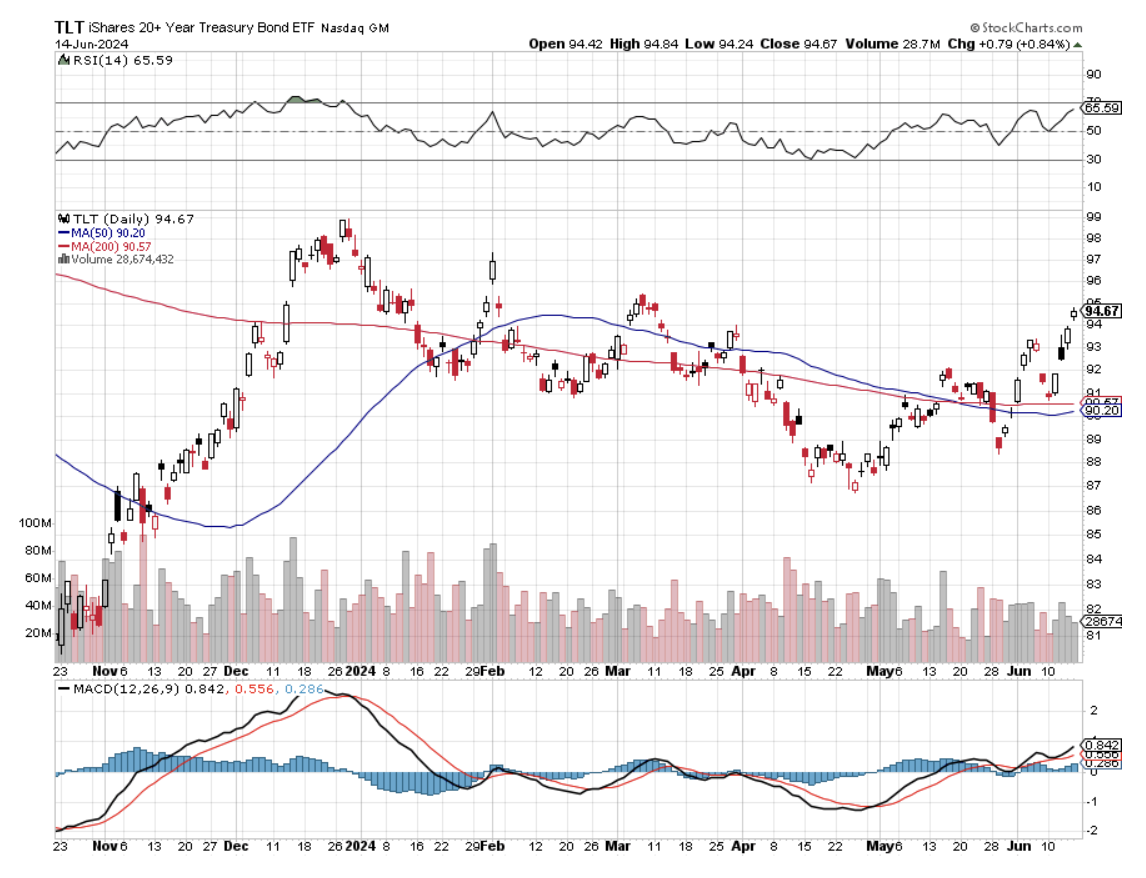

After six months of grief, pain, and suffering last week, my (TLT) LEAPS finally went into the money last week.

Remember the (TLT)?

On January 18, I bought the United States Treasury Bond Fund (TLT) January 17, 2025, $95-98 at-the-money vertical Bull Call spread LEAPS at $1.25 or best. On Friday, they nudged up to $1.35. But I kept averaging down with the $93-$96’s and the $90-$93’s which are now at a max profit.

We lost six months on this trade thanks to a hyper-conservative which is eternally fighting the last battle. A 9.2% peak certainly put the fear of God in them and they persist in thinking a return to higher inflation rates is just around the corner.

Markets, however, have a different view. They are now discounting a 25-basis point cut in September followed by another in December. That will easily take the (TLT) up to $100. This is why we go long-dated on LEAPS. There is plenty of room for error….lots of room, even room for the Fed’s error. If you wait long enough, everything goes up.

With THIS Fed fighting it seems to pay off. That is what happened when Jay Powell waited a full year until raising rates for a super-heated economy. He now risks tipping the US into recession by lowering rates too slowly, when virtually all data points are softening. I guess that’s what happens when you have a Political Science major as Fed governor.

And here is what the Fed is missing. AI is destroying jobs at a staggering rate, not just minimum wage ones but low-end programming ones as well. That’s what the 300,000 job losses over the last two years in Silicon Valley have been all about.

It’s unbelievable the rate at which AI is replacing real people in jobs. If you want a good example of that, I had to call Verizon (VZ) yesterday to buy an international plan, and I never even talked to a human once. They listed three international plans in a calm, even, convincing male voice, and I picked one.

Or go to McDonalds (MCD) where $500 machines are replacing $40,000 a year workers. This is going on everywhere at the same time at the fastest speed I have ever seen any new technology adopted. So buy stocks, that’s all I can say.

It is not just the (TLT) that is having a great month. The entire interest rate-sensitive sector has been on fire as well. My favorite cell phone tower REIT, Crown Castle International with its generous 6.28% dividend yield, has jumped 15%. Distressed lender Annaly Capital Management (NLY) with its spectacular 13.08% dividend, has appreciated by 11%.

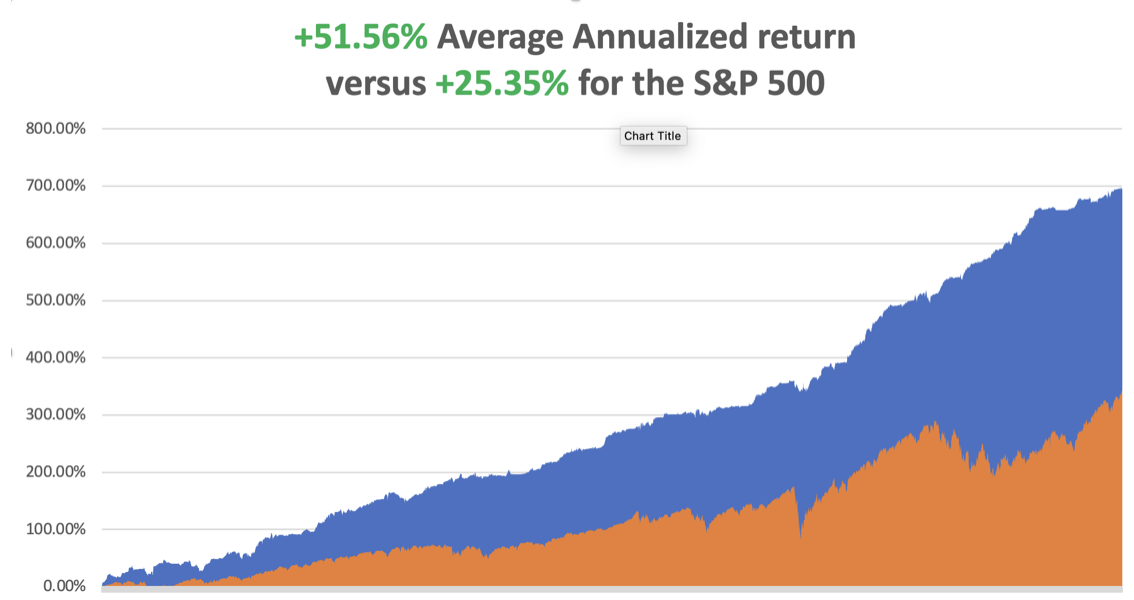

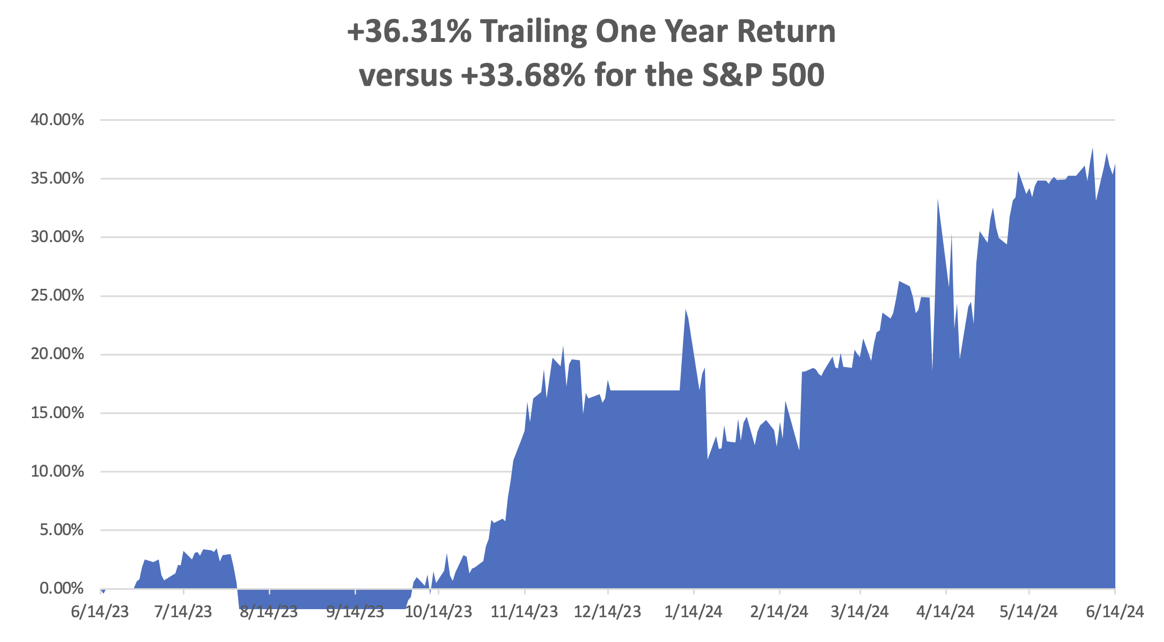

So far in June, we are up +1.04%. My 2024 year-to-date performance is at +19.39%.The S&P 500 (SPY) is up +13.83%so far in 2024. My trailing one-year return reached +36.31%. That brings my 16-year total return to +696.02%.My average annualized return has recovered to +51.56%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I stopped out of my near-money gold position (GLD) at close to breakeven because we were getting too close to the nearest strike price.

Some 63 of my 70 round trips were profitable in 2023. Some 29 of 38 trades have been profitable so far in 2024, and several of those losses were really break-even.

Fed Leaves Rates Unchanged at 5.25%-5.5% but reduces the cuts by March from three to one, citing an inflation rate that remains elevated. The projections were very hawkish, and the markets sold off on the news.

CPI Comes in Cool, unchanged MOM and 3.4% YOY. The May Nonfarm Payroll Report out Friday was an anomaly. It’s game on once again.

Europe Imposes Stiff Tariff on Chinese EVs, up to 38.1%. Daimler Benz, BMW, and Fiat have to be protected or they will go out of business.

The Gold Rush Will Continue through 2024, as much of Asia is still accumulating the yellow metal. Asia lacks the stock market we here in the US enjoy. A global monetary easing is at hand.

Broadcom (AVGO) Announces a 10:1 Split, and the shares explode to the upside. Earnings were also great. I actually predicted this in my newsletter last week and again at my Wednesday morning biweekly strategy webinar. The split takes place on July 15. Split fever continues. Buy (AVGO) on dips.

Apple (AAPL) Soars to New All-Time High, over $200 a share for the first time. However, it is now only the third largest company in the world, losing first place to (NVDA) and (MSFT). Analysts piled up the benefits of pitching AI to one billion preexisting customers. Just don’t tell Elon Musk.

Dollar Hits One Month High, on soaring interest rates spinning out from the super-hot May Nonfarm Payroll Report. This may be your last chance to sell at the highs. Never own a currency with falling interest rates. Just look at the Japanese yen.

Stock Buybacks Hit $242 Billion in Q1, but a new 1% tax may slow down the activity. The tax was passed as part of the Inflation Reduction Act in 2022 and is retroactive to January 1, 2023. (AAPL), (DIS), (CVX), (META), (GS), (WFC), and (NVDA) were the big buyers.

Home Equity Hits All-Time High at $17 Trillion according to CoreLogic. About 60% of homeowners have a mortgage. Their equity equals the home’s value minus outstanding debt. Total home equity for U.S. homeowners with and without a mortgage is $34 trillion. That is a lot of cash that could potentially end up in the stock market.

Home Prices to Keep Rising says Redfin CEO. While experts are forecasting more homes will be available, they said the boost in supply is not enough to solve affordability issues for buyers. Interest rates are expected to come down, but not by enough to counteract high prices.

Elon Musk Wins his $56 Billion Pay Package after a shareholder vote where retail investors came to his rescue. Institutional investors like CalPERS were overwhelmingly against it. It didn’t help that Elon moved Tesla to Texas. State pension funds always show a heavy bias in favor of local companies. Luck for California teachers includes (NVDA), (AAPL), (GOOGL), and (SMCI). (TSLA) rose 4% on the news.

The Gold Rush Will Continue through 2024, as much of Asia is still accumulating the yellow metal. Asia lacks the stock market we here in the US enjoy. A global monetary easing is at hand.

US Homes Sales Fall, down 1.7% month-over-month in May on a seasonally adjusted basis and dropped 2.9% from a year earlier. Median home sale price rose to a record high of $439,716, up 1.6% month-over-month and 5.1% year-over-year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 17, the New York Empire State Manufacturing Index is released.

On Tuesday, June 18 at 7:00 AM EST, Retail Sales are published.

On Wednesday, June 19, the first-ever Juneteenth holiday where the stock market is closed. Juneteenth celebrates the date when the slaves in Texas were freed in 1866, the last to do so.

On Thursday, June 20 at 8:30 AM, the Weekly Jobless Claims are announced. We also get Building Permits.

On Friday, June 21 at 8:30 AM, the Existing Home Sales are announced.

At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, as I am about to embark on Cunard’s Queen Elisabeth from Vancouver Canada on the Mad Hedge Seminar at Sea, I thought I’d recall some memories from when I first visited there 54 years ago.

Upon graduation from high school in 1970, I received a plethora of scholarships, one of which was for the then astronomical sum of $300 in cash from the Arc Foundation, whoever they were.

By age 18, I had hitchhiked in every country in Europe and North Africa, more than 50. The frozen wasteland of the North and the Land of Jack London and the northern lights beckoned.

After all, it was only 4,000 miles away. How hard could it be? Besides, oil had just been discovered on the North Slope and there were stories of abundant high-paying jobs.

I started hitching to the Northwest, using my grandfather’s 1892 30-40 Krag & Jorgenson rifle to prop up my pack and keeping a Smith & Wesson .38 revolver in my coat pocket. Hitchhikers with firearms were common in those days and they always got rides. Drivers wanted the extra protection.

No trouble crossing the Canadian border either. I was just another hunter.

The Alcan Highway started in Dawson Creek, British Columbia, and was built by an all-black construction crew during the summer of 1942 to prevent the Japanese from invading Alaska. It had not yet been paved and was considered the great driving challenge in North America.

One 20-mile section of road was made out of coal, the only building material then available, and drivers turned black after transiting on a dusty day. I’ll never forget the scenery, vast mountains rising out of endless green forests, the color of the vegetation changing at every altitude.

The rain started almost immediately. The legendary size of the mosquitoes turned out to be true. Sometimes, it took a day to catch a ride. But the scenery was magnificent and pristine.

At one point a Grizzley bear approached me. I let loose a shot over his head at 100 yards and he just turned around and lumbered away. It was too beautiful to kill.

I passed through historic Dawson City in the Yukon, the terminus of the 1898 Gold Rush.There, abandoned steamboats lie rotting away on the banks, being reclaimed by nature. The movie theater was closed but years later was found to have hundreds of rare turn-of-the-century nitrate movie prints frozen in the basement, a true gold mine. Steven Spielberg paid for their restoration.

Eventually, I got a ride with a family returning to Anchorage hauling a big RV. I started out in the back of the truck in the rain, but when I came down with pneumonia, they were kind enough to let me move inside. Their kids sang “Raindrops keep falling on my head” the entire way, driving me nuts. In Anchorage they allowed me to camp out in their garage.

Once in Alaska, there were no jobs. The permits required to start the big pipeline project wouldn’t be granted for four more years. There were 10,000 unemployed.

The big event that year was the opening of the first McDonald’s in Alaska. To promote the event, the company said they would drop dollar bills from a helicopter. Thousands of homesick showed up and a riot broke out, causing the stand to burn down. It was rumored their burgers were made of much cheaper moose meat anyway.

I made it all the way to Fairbanks to catch my first sighting of the wispy green contrails of the northern lights, impressive indeed. Then began the long trip back.

I lucked out by catching an Alaska Airlines promotional truck headed for Seattle. That got me free ferry rides through the inside passage. The driver wanted the extra protection as well. The gaudy, polished cruise destinations of today were back then pretty rough ports inhabited by tough, deeply tanned commercial fishermen and loggers who were heavy drinkers and always short of money. Alcohol features large in the history of Alaska.

From Seattle, it was just a quick 24-hour hop down to LA. I still treasure this trip. The Alaska of 1970 no longer exists, as it is now overrun with summer tourists. It now has 27 McDonald’s stands.

And with runaway global warming the climate is starting to resemble that of California than the polar experience it once was. Permafrost frozen for thousands of years is melting, causing the buildings among them to sink back into the earth.

It was all part of life’s rich tapestry.

The Alcan Highway Midpoint

The Alaska-Yukon Border in 1970

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/alcan-yukon-border.png462476april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-17 09:02:192024-06-17 10:45:37The Market Outlook for the Week Ahead, or The Three-Horse Race

Below please find subscribers’ Q&A for the June 12 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: How will Nvidia (NVDA) trade post-split?

A: Well, it’ll probably keep going up, because I think the year-end target—the old $1400, which is now $140—is still good. And I have a whole bunch of LEAPS, which are post-split $40, $50, $60 in-the-money, and I’m just keeping those. It’s a good cash management tool to have. So, even $500 points in the money, you’re still looking at about 20% returns by the end of the year on a January LEAPS. If you can buy the January 2025 $70-$71 LEAPS for 83 cents that’s a 20.48% profit at expiration in six months. So if you want a safe, very high return, that is the best way to do it in the financial markets, is to go way in the money. LEAPS will still pay you a lot of money amazingly. This trade will disappear someday but it’s there now and I’m taking it. Screw 90-day T-bills—I’m going into $500 in-the-money LEAPs on Nvidia, which pays four times as much.

Q: Is Broadcom Inc (AVGO) the next Nvidia?

A: There is no next Nvidia—the next Nvidia is Nvidia. Buy Nvidia on a 20% decline, which I think we may get sometime this summer. That’s a dip you want to buy for a year-end run to $140. Also, Broadcom isn’t exactly undiscovered at this point. It has doubled since October, while Nvidia is up 4 times. So if the bargain in the market for you is double in six months, I’m not sure you should be in the market. That said, I put out a report on split candidates last week and (AVGO) is very high on the list.

Q: What’s the best way to trade split candidates?

A: I actually just wrote a newsletter about this last week. There are in fact 36 high-priced, good money-earning split candidates, and I listed them all. You can buy really any of those if you’re looking for a high-priced stock that is growing. And management has a huge incentive to do splits because it makes the stock go up faster, and they’re all paid in stock options. So that is another reason you go into these. The best way to trade splits is buying the candidates because the biggest move is on the announcement of the split—you usually get 10%, 15%, or even 20% returns on the announcement.

Q: How do you envision AI in 10 years?

A: Well, it’s unimaginable. I can tell you from experiencing a lot of these big technology changes—it’s always tremendously underestimated by the markets, and you can safely bet on that. It’ll go up a lot more than you realize. That’s what happened when we jumped from six track tapes to cassettes, Betamax to VHS, teletypes to faxes, and faxes to emails. I thought Steve Jobs was crazy when he introduced the iPhone. Nobody makes money in handsets. But he proved me wrong.That makes my $240,000 DOW by 2030 projection completely reasonable.

Q: What will inflation do for the rest of the year, and how will it affect stocks?

A: Inflation will go flat to down for the rest of the year. And that is being driven by artificial intelligence—the greatest deflationary product ever created in the history of the economy. It’s unbelievable the rate at which AI is replacing real people in jobs. If you want a good example of that, I had to call Verizon yesterday to buy an international plan, and I never even talked to a human. They listed out three international plans in a calm, even male voice, and I picked one. Or go to McDonald's where $500 machines are replacing $40,000 a year workers. This is going on everywhere at the same time at the fastest speed I have ever seen any new technology adopted. So buy stocks, that’s all I can say.

Q: What’s your opinion on Arm Holdings (ARM)?

A: I love it. There are very few serious companies in the chip area, and this is one of them.

Q: Do you expect gold mining stocks to continue upward?

A: Yes, but the better play here is the metal. Gold and silver aren't being held back by inflation while the miners are. Plus, the main buyers in the market now are the Chinese, and they don’t buy gold miners—they buy gold, silver, copper, platinum, and uranium outright.

Q: What about Tesla (TSLA) long-term? Kathy Woods's target is $2000 long-term.

A: I think Kathy Woods is right. But we have to get through the nuclear winter in the EV space first, where suddenly the market got saturated. I think Tesla is the only one who could come out of this alive by cutting costs and advancing technology, as they have always done. When I bought my first Tesla Model S1 in 2010, the battery cost $32,000. Now it’s $6,000, and you get a lot more range. Did (GM) offer an equivalent cost improvement with internal combustion engines? So, yes, never bet against Elon Musk—that’s a good 25-year lesson on my part, and should be for you too.

Q: Can you elaborate on the lithium trades?

A: I listed three names in my letter last week, (SQM), (FMC), (ALB),and the only thing you know for sure is that they’re cheap now. They could stay cheap for another six or 12 months. But when you get a turnaround in the global EV market and the manufacturers start screaming for more lithium, and all of the lithium stocks will double, or triple and they’ll do it fairly quickly. You can’t beat a market bottom for getting involved. Just look at my above (NVDA) trade. Not only would they be good stocks buy, but it would be a good LEAPS buy down here because then you could get 4 or 5 times your money on a small move.

Q: Can you suggest Amazon (AMZN) LEAPS?

A: January 2025 $195-200 just out of the money, should give you a return of about 120% over the next 6 months. That gets you the annual yearend run-up. And that’s my conservative position. My aggressive ones are all in Nvidia.

Q: Do you think zero-day options have permanently forced the Volatility Index ($VIX) to the $12 handle?

A: Yes, I do; it’s killed that market. Something like 40% of all the optiontraders on the CBOE were trading the ($VIX) from the short side. Shorting the ($VIX) now would be madness. That has to bring tough times for that whole industry. Trading call spreads at a $12 volatility, you’re better off buying the LEAPS because the LEAPS give you much bigger returns with much less risk. And a $12 ($VIX) means you’re getting your LEAPS at half the historic price. I’m just waiting for a new market low to start pumping out the LEAPS recommendations. All the more reason to sign up for the Mad Hedge Concierge Service to get an early read into the LEAPS recommendations. For more information on that, contact support at support@madhedgefundtrader.com

Q: What will happen to Apple (AAPL) after the 11% surge?

A: It goes to $250 by the end of the year. Now that it has the kiss of AI on it, people will pour into it.

Q: Why is value lagging?

A: Because AI is entirely a growth story, and you look at all the domestic value stocks, they’re going absolutely nowhere. Value has been in the dog house for years and I’m in no hurry to get in there.

Q: What is the best dividend stock I can invest in right now?

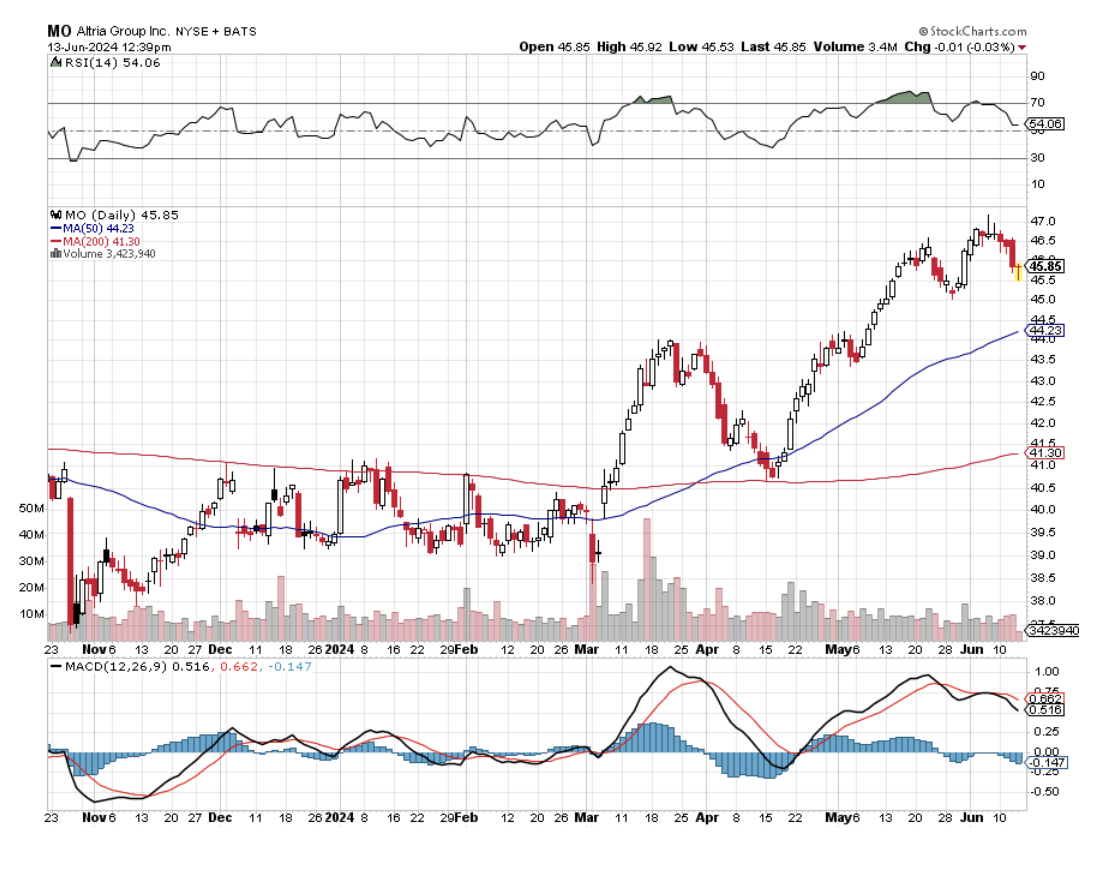

A: That’s an easy one.Altria (MO) has a 9% dividend—you can’t beat that. But you have to hold your nose when you buy this stock because they are in the cigarette business. However, their big growth now is in Asia ex-Japan where the government has a monopoly on tobacco, particularly China. Note that this is not an undiscovered idea; lots of people like a 9% dividend stock and (MO) has already gone up 20% this year, but I think there is still some money to be made here.

Q: How can we subscribe to get early LEAPS recommendations?

A: That would be the Concierge Service. Contact Filomena at customer support, and they will get you taken care of right away.

Q: What about the small nuclear plays?

A: I actually happen to know quite a lot about nuclear plant design, having worked for the Atomic Energy Commission in my youth, and the new designs address every major issue that held back nuclear power with the old 1950s designs. For example, building them underground and eliminated the need for these giant billion-dollar four-foot-thick reinforced concrete containment structures that dot the horizon. Not using pure Uranium alloys that can’t go supercritical is another great idea. So I like them. Are they good stock plays? Not right now. It takes a long time to introduce a new energy technology. Bill Gates is financing a new plant built by Terrapower in Wyoming, and it looks like a fantastic plant, but only Bill Gates could invest at this stage and expect to make money on it. He has very long-term money and you don’t. I would wait until you get a working model plant in the United States before going into these things, but potentially you’re looking at a 10 to 100 times return on your money if it works.

Q: Should I invest in Airbnb (ABNB) because of increased international travel?

A: Yes, we like Airbnb. Especially since they will get a push with the Paris Olympics next month. Not only does that get people to Paris, but it gets people to all of Europe because they usually add on additional trips to a visit to the Olympics.

Q: What would you do in Netflix (NFLX), and what strikes would you use?

A: I would do a LEAPS. Wait for a correction, at least 10%, preferably 20%, and then I would go at the money one year out and that would get you about 100% return. So, that’s the way to do that. This is not LEAPS territory right here —all-time highs are not LEAPS territory. You want to put on LEAPS when everyone else is throwing up on their shoes; the last time they did that was October 26.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.