(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHAT’S UP WITH TECH?),

(MSFT), (TSLA), (AAPL), (QQQ), (NVDA), (MU), (AMD), (BRKB), (ARRK), (ROM), (VIX), (FCX), (TLT), (BRKB), (TSLA), (JPM), (SPY), (QQQ), (SPX)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-08 11:04:072021-03-08 11:21:08March 8, 2021

That great wellspring of personal wealth, technology stocks, has suddenly run dry.

The leading stock market sector for the past decade took some major hits last week. More stable stocks like Microsoft (MSFT) only shed 8%. Some of the highest beta stocks, like Tesla (TSLA), took a heart-palpitating 39% haircut in a mere two months.

Have tech stocks had it for good? Has the greatest investment miracle of all times ground to a halt? Is it time to panic and sell everything?

Fortunately, I have seen this happen many times before.

Technology is a sector that is prone to extremes. Most of the time it is a hero, but occasionally it is a goat. When too many short-term traders sit in one end of the canoe, we all end up in the drink.

This is one of those times.

Technology stocks undeniably need a periodic shaking out. You need to get rid of the day traders, the hot money, the excessively leveraged, and find out who has been swimming without a swimsuit. The sector rotates between being ridiculously cheap to wildly overvalued. We are currently suffering the latter.

During the past 12 years, Apple’s (AAPL) price earnings multiple has traded from 9X to 36X. It was a value play for the longest time, all the way up to 2016. Nobody believed in it. It is currently at a 33X multiple. While the stock has gone nowhere since August, its earnings have increased by more than 10%, and better is yet to come.

After trading tech stocks for more than 50 years, I can tell you one thing with certainty.

They always come back.

And this time, they are in position to come back sooner, faster, and bigger than ever before. Remember the Great Dotcom Bust of 2000-2003? It lasted two years and nine months and saw NASDAQ (QQQ) crater by 82%, from 5,000 to 1,000. This time, it’s only dropped by 13%, by 1,850 from 14,250 to 12,400.

I don’t see the selloff lasting much longer or lower, no more than another 5%-10% until September. For these are not your father’s technology stocks.

There are only three numbers you need to know. Technology now accounts for a mere 2% of the US workforce, but a massive 27% of stock market capitalization and 37% of total us company earnings. A sector with such an impressive earnings output won’t fall for very long, or very far.

The pandemic accelerated technological innovation tenfold. Companies now have mountains of cash with which to bring forward their futures.

This is no more true than for biotech stocks. The technologies used to create Covid-19 vaccines can be applied to cure all human diseases. And they now have mountains of cash to implement this.

So, I’ll be taking my time with tech stocks. But they are setting up the best long side entry point since the March 20, 2020 pandemic low.

The biggest call remaining for 2021 is when to take profits and sell domestic recovery value stocks and rotate back into tech. But if you are running the barbell strategy I have been harping about since the presidential election, the work is already being done for you. Nonfarm Payroll comes in at a blockbuster 379,000 in February, far better than expected. It a preview of explosive numbers to comes as the US economy crawls out of the pandemic. That’s with a huge drag from terrible winter weather. The headline Unemployment rate is 6.2%. The U-6 “discouraged worker” rate is still a sky-high 11%, those who have been jobless more than six months. Leisure & Hospitality were up an incredible 355,000 and Retail was up 41,000. Government lost 86,000 jobs. We are still 12 million jobs short of the year-ago trend. See what employers are willing to do when they see $20 trillion about to hit the economy?

Will US GDP Growth hit 10% this year? That is the sky-high number that is being mooted by the Atlanta Fed for the first three months of 2021. The vaccine is working! They do tend to be high in the home of Gone with the Wind. This Yankee would be happy at 7.5% growth. Manufacturing just hit a three-year high as companies try to front-run imminent explosive growth. The only weak spot is employment, which is still at recessionary highs.

Herd Immunity is here or says the latest numbers from Johns Hopkins University. New cases have plunged from 250,000 to 46,000 in a month, the fastest disease rollback in human history. We may be seeing new science at work here, where mass vaccinations combine with mass infections to obliterate the pandemic practically overnight. If true, the Dow has another 8,000 points in it….this year. Buy everything on dips. The economic data is about to get superheated.

Warren Buffet’s Berkshire Hathaway blows it away, buying back a staggering $25 billion worth of his own stock in 2020, including $9 billion in the most recent quarter. It’s what I’m always looking for, buying quality at a discount. Warren pulled in $5 billion in profits during the last quarter of 2020, up 13.6% over a year earlier. Net earnings were up 23%. If Buffet, a long time Mad Hedge reader, is buying his stock, you should too. Buy (BRKB) on dips. It's also a great LEAP candidate as the best domestic recovery play out there. Rising rates have yet to hurt Real Estate, as the structural shortage of housing is so severe. Historically speaking, interest rates are still very low, even though the ten-year yield has soared by 82% in two months. Cash is still pouring into REITs coming off the bottom. Home prices always see their fastest moves up at the beginning of a new rate cycle as everyone rushes to beat unaffordable mortgages. The Chip Shortage worsens, with Tesla shutting down its Fremont factory for two days. The Texas deep freeze made matters much worse, where many US fabs are located, like Samsung, NXP Semiconductors, and Infineon Technologies. Buy (NVDA), (MU), and (AMD) on dips.

Jay Powell lays an egg at a Wall Street Journal conference. He said it would take some time to return to a normal economy. The speed of the interest rate rise was “notable.” We are unlikely to return to maximum employment in a year. We couldn’t have heard of more dovish speech. But all that traders heard was that inflation was set to return, but will be “temporary.” That was worth a 600-point dive in the stock market and a 5-basis point pop in bond yields. My 10% correction is finally here! Here today, gone tomorrow. Cathie Wood was far and away the best fund manager of 2020. She, value investor Ron Baron, and I, were alone in the darkness four years ago saying that Tesla (TSLA) could rise 100-fold. Cathie’s flagship fund The Ark Innovation ETF (ARKK) rose a staggering 433% off the March 2020 bottom. Alas, it has since given up a gut-punching 30% since the February high, exactly when ten-year US Treasury bonds started to crash. Watch (ARKK) carefully. This is the one you want to own when rates stabilize. It’s like another (ROM). When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

It’s amazing how well selling tops and buying bottoms can help your performance. My Mad Hedge Global Trading Dispatch reached a super-hot 11.61% during the first five days in March on the heels of a spectacular 13.28% profit in February. The Dow Average is up a miniscule 4.00% so far in 2021.

It was a week of frenetic trading, with the Volatility Index (VIX) all over the map. I took profits in Freeport McMoRan (FCX) and my short in US Treasury bonds (TLT) and buying Berkshire Hathaway (BRKB), Tesla (TSLA), JP Morgan (JPM). I opened new shorts in the S&P 500 (SPY) and the NASDAQ (QQQ).

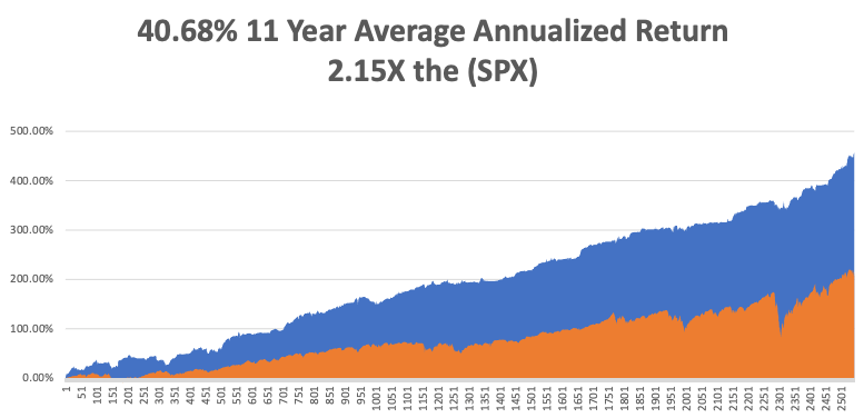

This is my fifth double digit month in a row. My 2021 year-to-date performance soared to 35.10%. That brings my 11-year total return to 457.65%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.68%.

My trailing one-year return exploded to 110.25%, the highest in the 13-year history of the Mad Hedge Fund Trader.

We need to keep an eye on the number of US Coronavirus cases at 29 million and deaths topping 525,000, which you can find here.

The coming week will be a boring one on the data front.

On Monday, March 8, at 11:00 AM EST, Consumer Inflation Expectations for February are out.

On Tuesday, March 9, at 7:00 AM, The NFIB Business Optimism Index for February is published. On Wednesday, March 10 at 8:30 AM, the US Inflation Rate for February is printed. On Thursday, March 11 at 8:30 AM, Weekly Jobless Claims are out. On Friday, March 12 at 8:30 AM, the Producer Price Index for February is disclosed.

At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, it was with great sadness that I learned of the passing of my old friend, Sheikh Zaki Yamani, the great Saudi Oil Minister. Yamani was a true genius, a self-taught attorney, and one of the most brilliant men of his generation.

It was Yamani who triggered the first oil crisis in 1973, raising the price from $3 to $12 a barrel in a matter of weeks. Until then, cheap Saudi oil had been powering the global economy for decades.

During the crisis, I relentlessly pestered the Saudi embassy in London for an interview for The Economist magazine. Then, out of the blue, I received a call and was told to report to a nearby Royal Air Force base….and to bring my passport.

There on the tarmac was a brand-new Boeing 747 with “Kingdom of Saudi Arabia” emblazoned on the side in bold green lettering. Yamani was the sole passenger, and I was the other. He then gave me an interview that lasted the entire seven-hour flight to Riyadh. We covered every conceivable economic, business, and political subject. It led to me capturing one of the blockbuster scoops of the decade for The Economist.

When Yamani debarked from the plane, I asked him “why me.” He said he saw a lot of me in himself and wanted to give me a good push along my career. The plane then turned around and flew me back to London. I was the only passenger on the plane.

When the pilot heard I’d recently been flying Pilatus Porters for Air America, he even let me fly it for a few minutes while he slept on the cockpit floor.

Yamani later became the head of OPEC. At one point, he was kidnapped by Carlos the Jackal and held for ransom, which the king readily paid.

And if you wonder where I acquired my deep knowledge of the oil and energy markets, this is where it started. Today, the Saudis are among the biggest investors in alternative energy in California.

We stayed in touch ever since.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-on-a-camel.png454470Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-08 11:02:032021-03-08 13:21:48The Market Outlook for the Week Ahead, or What’s Up with Tech?

Below please find subscribers’ Q&A for the March 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are SPACs here to stay?

A: Yes, but I think that in the next bear market, 80% of these SPACs (Special Purpose Acquisition Companies) will disappear, will deliver large losses, and will continue charging you enormous fees until then. It’s either that or they won’t invest their money at all and give it back, net of the fees. So, I’m avoiding the SPAC craze unless it's associated with a very specific investment play that I know well. The problem with SPACs is that they all come out expensive—there are no bargain basement SPACs on launch day. Me, being the eternal cheapskate that I am, always want to get a great bargain on everything. The time to buy these is actually in the next bear market, if they still exist, because then investors will be throwing their positions away at 10 or 20% discounts. That’s always what happens with specialized ETF, closed-end funds, and so on. They are roach motel investments; you can check-in, but you can never check out.

Q: What do you think of Elizabeth Warren's asset tax idea?

A: It’s idiotic. It would take years to figure out how much Jeff Bezos is worth. And even then, you probably couldn't come within ten billion dollars of a true number. We already pay asset taxes, our local county real estate taxes, and those are bad enough, delivering valuations that are miles from true market prices. There are many other ways to fix the tax system and get billionaires paying their fair share. There are only three things you really have to do: get rid of carried interest so hedge funds can’t operate tax-free, get rid of real estate loss carry forwards which allow the real estate industry to basically operate tax-free, and get rid of the oil depletion allowance, which has enabled the oil industry to operate tax-free for nearly 90 years. So those would be three easy ones to increase the fairness of the tax system without any immense restructuring of our accounting system.

Q: When will share buybacks start?

A: They’ve already started and have been happening all year. There are two ways the companies do this: they either have an outside accounting firm, buying religiously every day or at the end of every month or something like that, so they can’t be accused of insider trading; or they are in there buying on every dip. Certainly, all the big cash-heavy companies like Berkshire Hathaway (BRKB) or Apple (AAPL) were buying their shares like crazy last March and April because they were trading such enormous discounts. So that is another trillion dollars sitting under the market, waiting to come in on any dip, which is yet another reason that we are not going to see any major sell-offs this year—just the 5%-10% variety that I have been predicting.

Q: Is it time to buy Salesforce (CRM)?

A: Yes, Marc Benioff’s goal is to double sales in two years, and the stock is relatively cheap right now because they’ve had a couple of weak quarters and are still digesting some big acquisitions.

Q: Is CRISPR Therapeutics (CRSP) good buy?

A: Yes, I would be buying right here; it’s a good LEAP candidate because the stock could easily double from here. We’ve only scratched the surface on CRISPR technology being adopted and the potential growth in this company is enormous—I'm surprised they haven’t been taken over already.

Q: Will you start a letter for investing advisors on how to deal with the prolific numbers of Bitcoin?

A: There are already too many Bitcoin newsletters; there are literally hundreds of them and thousands of experts on Bitcoin now because there’s nothing to know and nothing to analyze. It’s all a belief system; there are no earnings, there are no dividends, and there is no interest. So, you purely have to invest in the belief that somebody else is going to take you out at a higher price. I think there is a big overhang of selling in that when they raise the number of Bitcoin, we’ll get another one of those 90% crashes that Bitcoin is prone to. So, go elsewhere for your Bitcoin advice; your choices are essentially unlimited now, and they are much cheaper than me. In fact, people are literally giving away Bitcoin advice for free, which means you’re getting what you’re paying for. I buy Bitcoin when they have a customer support telephone number.

Q: Zoom (ZM) has come down a lot after a big earnings report—do you like it?

A: Long term, yes. Short term, no. You want to avoid all the stay-at-home stocks because no one is staying at home anymore. However, there is a long-term story in Zoom once they find their bottom because even after we come out of the pandemic, we’re all still using Zoom. I have like five or ten Zoom meetings a day, and my kids go to school on Zoom all day long. They’re also bringing out new products like telephone servers. They’re also raising their prices—I happen to be one of Zoom’s largest customers. I’m paying $1,100/month now, and that’s rising at 10% a year.

Q: What would be the best LEAP for Salesforce (CRM)?

A: The rule of thumb is that you want to go 30% out of the money on your first strike. So, find a current stock price; your first strike is up 30%, and then your second strike is up 35%. And all you need to double your money on that is a bounce back to the highs for this year, which is not unrealistic. That’s the lay-up there with Salesforce. That’s the basic formula; Advanced Micro Devices (AMD), Walt Disney (DIS), Berkshire Hathaway (BRKB), Palantir (PLTR), and Nvidia (NVDA) are all good candidates for LEAPS.

Q: How often do you update the long-term stock portfolio?

A: Twice a year, and we just updated in January, which is posted on the website in your membership area. If you can't find it, just email customer support at support@madhedgefundtrader.com and they’ll tell you where to find it. And we only do this twice a year because there just aren't enough changes in the economy in six months to justify a more frequent update.

Q: When do you think real estate will come back?

A: It never left. We’ve had the hottest real estate market in history, with 20% annual gains in many cities in 2020. And that will continue, but not at the 20% rate, probably at a more sustainable 5% or 6% rate. Guess what the best inflation play in the world is? Real estate. If you’re worried about inflation, you want to run out and buy a house or two. The only thing that will really kill that market is a rise in 30-year fixed-rate mortgages to 5%, and that is years off. Or a rise in the ten-year treasury to 5% or 6%—that is several years off also. So, I think we’ve got a couple of good years of gains ahead of us. I at least want the market to stay hot until my kids get out of high school, and then I can sell my house and go live on some exotic tropical island with great broadband.

Q: When you’re doing LEAPS, do you just do the calls only or do you do these as spreads?

A: You can do both. Just do the math and see what works for you on a risk/reward basis. You can do a 30% out of the money call 2 years out and get anywhere from a 1,000% to a 10,000% return—people did get 10,000% returns buying deep out of the money LEAPS in Tesla (TSLA) a year ago (that’s where all the vintage bourbon is coming from). Or you can do it more conservatively and only make 500% in two years on Tesla spread. For example; do something like a Tesla January 2023 $900-$950 call spread. If Tesla shares rise to $950, that position is an easy quadruple. But do the numbers, figure out the cost today, what the expiration value is in two years, and there you go.

Q: Do you think overnight rates could go negative as some people predict?

A: Not for a long time. They will go negative at the next recession because we’re starting off such a low base—or when we get the next pandemic, which could be as early as next year. We could get another one at any time from a completely different virus, and it would generate the same stock market results that we got last time—down 40% in a month. We’re not out of the pandemic business, we’re just having a temporary break waiting for the next one to come along out of China or some other country, or even right here in the USA. So that may be a permanent aspect of investing in the future. It could be the price we pay having a global population that's at 7 billion heading to 9 billion.

Q: Expiration on LEAPS?

A: I always go out two years. The second year is almost free, that’s why. So why not go for the second year? It gives you twice as much time to be right, always useful.

Q: My two-year United States Treasury Bond Fund (TLT) $125 put LEAPS have turned very positive. Is this a good trade?

A: That is a good trade, which you should put on during the next (TLT) rally. If you think we’re going to $105 in 2 years, do something like a $127-$130 two-year put LEAP, and there's a nice four bagger right there.

Q: Your Amazon (AMZN) price target was recently listed at $3,500, below last year's high, but I’ve also seen a $5,000 forecast in two years. Are you sticking with that?

A: Yes, I think when you get a major recovery in the economy, Amazon will be one of the only pandemic plays that keeps on going. It’s just taking a rest here with the rest of big tech. The breakup value of Amazon is easily $5,000 a share or more. Plus, they’re still going gangbusters growing into new industries that they’ve barely touched so far, like pharmaceuticals, healthcare, and so on. So yes, I would definitely be a buyer of LEAPS, and you could do something like the January 2023 $3700-$4000 LEAP two years out and make a killing on that.

Q: Anything you can do in gold (GLD)?

A: Not really. Although gold and silver (SLV) have been a huge disappointment this year, I think this could be the beginning of a capitulation selloff in gold which will bring us a final bottom, but it may take another month or two to get there.

Q: How can I sell short the dollar?

A: You sell short the (UUP), or there are several 1X and 2X short ETFs in the currencies that you can do, like the ProShares Ultra Short Euro ETF (EUO). That is the way to do it.

Q: What is the best timing for buying LEAPS?

A: Buy at market bottoms. A year ago, I was sending out lists of 10 LEAPS at a time saying please buy all of these. You need both a short-term selloff in the stock, and then an upside target much higher than the current price so your LEAP expires at its maximum profit point. And if you’re in the right names, pretty much all the names that we talk about here, you will have 30%, if not 300% or 3,000% gains in them in the next two years.

Q: Do you think Tesla’s Starlink global satellite system will disrupt the cell tower industry?

A: Yes, that is the goal of Starlink—to wipe out all ground communication for WIFI and for cell phones. It may take them several years to do it, but if they do pull it off, then it just becomes a matter of pricing. The last Starlink pricing I looked at cost about $500 to set up, open the account, and get your dish installed. And the only flaw I see in the Starlink system is that the satellite dishes are tracking dishes, which means they lock onto satellites and then follow them as they pass overhead. Then when that signal leaves, it locks onto a new satellite; at any given time they’re locked onto four different satellites. That means moving parts, and you want to be careful of any industry that has moving parts—they wear out. That’s the great thing about software and online businesses; no moving parts, so they don’t wear out. And that’s also why Tesla has been a success; they eliminated the number of moving parts in cars by 80%. I’m waiting for Starlink to get working so I can use it, because I need Internet access 24 hours a day, even if all the local hubs are out because of a power outage. I’m now using something called Viasat (VSAT), which guarantees 100 megabyte/second service for $55 a month. It's not enough for me because I use a gigabyte service landline, but when that’s not available then I can go to satellite as a backup.

Q: Is there too much Fed liquidity in the market already? Why is the $1.9 trillion rescue package still positive for the market?

A: Firstly, there is too much liquidity in the market; that is screamingly obvious. If you look at liquidity over the decades, we are just staggeringly high right now. M2 is growing at 26% against the normal rate of 5%-6%. What the stimulus package does is get money to the people who did not participate in the bull market from last year. Those are low-income people, cities, and municipalities that are broke and can’t pay teachers, firemen, and policemen. It also goes to individual states which were not invested in the stock market. It turns out that states that were invested in the stock market like California have money coming out of their ears right now. And it gets money to low wage workers with kids who are certainly struggling right now. So, it is rather efficiently designed to get the money to people who need it the most. There is still half the country that doesn't own any stocks or even have savings of any kind. One or two people might get it who don’t deserve it but try doing anything in a 330 million population country and have it be 100% efficient.

Q: Is inflation coming?

A: Only incrementally in tiny pieces, so not enough to affect the stock market probably for several years. I still believe technology is advancing so fast that it wipes out any effort to raise prices or increase wages, and that may be what the perennially high 730,000 weekly jobless claims is all about. Those jobs that might have been there a year ago have been replaced by machines, have been outsourced overseas, or the demand for the product no longer exists. So, as long as you have a 10% unemployment rate and a weekly jobless claim at 730, inflation is the last thing you need to worry about.

Q: Is there any way to cash in on Reddit’s Wall Street Bets action?

A: No, and I would bet the majority of people who are trading off of these emojis and Reddit posts are losing money. You only hear about these things after it’s too late to do anything about them. I don't think you’ll get any more $4 to $450 moves like you did with GameStop (GME) because in that one case only, there was a short interest of 160%, which should have been illegal. All the other high short interest stocks have already been hit, with short interests all the way down to 30%, so I think that ship has sailed. It has no real investing merit whatsoever.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-05 10:02:582021-03-05 11:46:15March 3 Biweekly Strategy Webinar Q&A

Its flagship magazine was wiped out by free internet porn last year after a storied 66-year run. During the 1970s, an invitation to a new club opening was the hottest ticket in town.

Of course, I bought the magazine only to read the articles.

Melania Trump as a centerfold? The business possibilities boggle the mind. Of course, it’s going public through a SPAC. Nobody else would touch this with a ten-foot pole. The ticker symbol will be (PLBY).

What this IPO does tell me is how overheated the markets are getting. In 1996, former Fed governor, saxophone player, and Ayn Rand acolyte, the gnomish Alan Greenspan warned the stock market of “irrational exuberance.” Since then, the Dow Average has risen by 5.2 times in 23 years, revisiting the 6,000 low once in 2009.

In fact, let me explain to you why stocks are so cheap.

At the 2000 Dotcom Bubble top, ten-year US Treasury yields stood at 6%. Stocks would have to rise five times more from today’s paltry 1.20% to reach the same relative valuation.

Dow 163,000 anyone?

Similarly, the big FANG stocks would have to triple in value to get us to the 100X price earnings multiple that prevailed in 2000. That gets us at least to Dow 94,500.

And this is what people don’t get about liquidity-driven bull markets. They go on far, far longer than anyone imagines possible. You had to be in Tokyo in 1989 to understand this.

If you’re really and truly worried about stocks, take a look at the chart below and how they reacted to the last catastrophic selloff that took place during 2007-2009.

After an initial, frenetic move, they rose by, you guessed it, 5.2 times.

The Global Chip Shortage is spreading beyond cars to phones and electronics. High prices beckon across the board. Could this be the black swan that heads off the recovery? It’s all a screaming BUY for (NVDA), (AMD), and (MU). I can’t believe these haven’t moved yet.

Biden created a Bull Market in Oil (USO) when he banned new leases on federal lands. The move took 3 million barrels a day off the market, taking a bite out of the 10 million barrels a day oversupply. And economic recovery should soak up the remaining 7 million barrels, 2021 forecasts for Texas tea are now reaching as high as $80.

Space X is taking pre-orders for Starlink, Elon Musk’s Global satellite WIFI network. Another industry disrupted. For a $99 deposit, you can access 500 megabytes a second, faster than available for most of the US. The goal is to launch 11,943 satellites by 2024. If it works, AT&T (T), Comcast (CMCSA), and Verizon (V) could be in big trouble. When you own your own rocket company, it’s easy to undercut the competition.

Weekly Jobless Claims are still weak, at 793,000, far higher than expected, but less than last week. Total jobless claims have it an unbelievable 20.44 million, just short of the 1930’s Great Depression high. Perhaps 20% of the country is living on government handouts.

The Pandemic Property Boom continues, posting the hottest numbers since 2005. The National Association of Realtors says the price of a single-family home rose by a staggering 14.9% in Q4. The Northeast was the leader at a 21% gain. The market keeps going from strength to strength.

Will the Dow double in a year? We only have 4,500 points to go for a 100% gain from the last March 20 low. We have already seen the sharpest gain in history, beginning when Biden took the lead in the primaries. Will passage of the $1.9 trillion rescue package take us over the finish line? And are we setting up for a “Buy the rumor, sell the news? We’ll know in a month. I bet you’ve just made more money in stocks than you’ve ever imagined possible. Take short-term profits in everything.

Bonds hit new lows, taking the ten-year US Treasury yield up to 1.20%. The Feds hit the markets for a massive $120 million in debt this week and buyers are obviously glutted. Keep selling those rallies in the (TLT). Maybe you should start selling dips, too. Use bond selloffs for your stock market timing. They’re about to become “certificates of confiscation” again.

No hint of rising rates soon, hints Fed governor Jay Powell. Recovery is the only goal, damn the inflation torpedoes. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 16.48% so far in February after a blockbuster 10.21% in January. The Dow Average is up a trifling 2.80% so far in 2021.

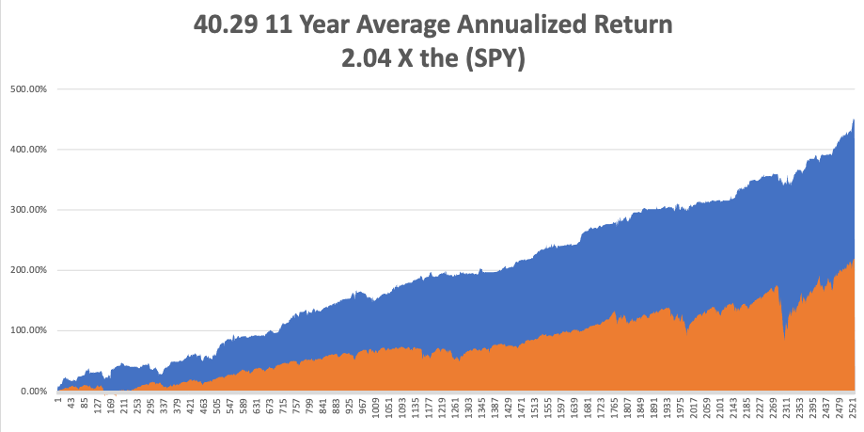

This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 26.69%. There are only four trading days left until the February 19 option expiration, when I automatically go into 80% cash. That’s convenient!

That brings my 11-year total return to 449.24%, some 2.04 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.29%.

My trailing one-year return exploded to 90.96%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 108.63% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 27.7 million and deaths approaching 500,000, which you can find here.We are now running at a heartbreaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 15, markets are closed for Presidents Day.

On Tuesday, February 16 at 8:30 AM EST, the NY Empire State Manufacturing Index is out. CVS (CVS) and Zoetis report. On Wednesday, February 17 at 8:30 AM, US Retail Sales for January are published. At 2;00 PM, we learn the Fed Open Market Committee minutes from the last meeting. Shopify and Twilio report.

On Thursday, February 18 at 9:30 AM, Weekly Jobless Claims are printed. Barrick Gold (GOLD) and Roku (ROKU) report. On Friday, February 19 at 10:00 AM, Existing Home Sales for January are released. We learn the Baker-Hughes Rig Count. As we have a three-day weekend following, option volatility should collapse. John Deere (DE) reports.

As for me, let me tell you what the last weeks of the great Japanese bull market were like at the end of 1989.

The big thing then was to eat sushi salted with flecks of pure gold. Any foreigner who could speak Japanese was worth hundreds of thousands of dollars a year.

The brokers would hire anyone. Kids went from running sandwich shops to trading desks at Morgan Stanley. Others upgraded from bicycles to Porsche Carrera’s and used to race on Tokyo’s abandoned freeway system in the middle of the night.

And you know what? Someone offered me a piece of gold-flecked sushi just the other day!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Stock Gains Since Greenspan’s “Irrational Exuberance” Comment

https://www.madhedgefundtrader.com/wp-content/uploads/2016/12/john-tokyo.jpg425318Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-16 12:02:352021-02-16 12:05:40The Market Outlook for the Week Ahead, or A Return to Irrational Exuberance

A better headline for this piece might have been “Ten stocks to Buy at the Bottom”, except that you have to redefine the word “bottom.”

The rules of the greatest liquidity-driven market of all time demand a different explanation of The NEW bottom, and that is something that hasn’t gone up lately.

And that would be big tech, which appears ready to blast out to the upside from a six-month long sideways “time” correction.

It would be a perfectly rational thing to see in these highly irrational markets. After all, these names just announced blockbuster earnings presaging greater things to come. And these companies actually HAVE earnings, compared to recent market frontrunners, which have none at all.

Coming in here and betting the ranch is now a no-lose trade. If I’m right, the pandemic ends in three months, stocks will soar. If I’m wrong and the global epidemic explodes from here, you’ll be dead anyway and won’t care that the stock market crashed further.

Needless to say, I have a heavy tech orientation with this list, far and away the source of the bulk of earnings growth for the US economy for the foreseeable future. If anything, the coronavirus will accelerate the move away from shopping malls and towards online commerce as consumers seek to shy away from direct contact with the virus.

What would I be avoiding here? Directly corona-related stocks like those in airlines, hotels, casinos, and cruise lines. Avoid human contact at all cost! There is no way of knowing when or where these stocks will bottom. Only the virus knows for sure.

Microsoft (MSFT) – still has a near-monopoly on operating systems for personal computers and a huge cash balance. Their inroads with the Azure cloud services have been impressive.

Apple (AAPL) – Even with the Coronavirus, Apple still has a cash balance of $225 billion. Its 5G iPhone launches in the fall, unleashing enormous pent-up demand. Apple’s rapid move away from a dependence on hardware to services continues.

Alphabet (GOOGL) – Has a massive 92% market share in search and remains the dominant advertising company on the planet.

QUALCOMM (QCOM) – Has a near-monopoly in chips needed for 5G phones. It also won a lawsuit against Apple over proprietary chip design. In the very near future, you won’t be able to do ANYTHING without 5G. It’s also not a bad idea to own a chip stock during the worst global chip shortage in history.

Amazon (AMZN) – The world’s preeminent retailer is growing by leaps and bounds. Dragged down by its association with the world’s worst industry, (AMZN) is a bargain relative to other FANGs.

Visa (V) – The world’s largest credit company is a call on the growth of the internet. We still need credit cards to buy things. And guess what? Coronavirus will accelerate the move of commerce out of malls where you can get sick to online where you can’t.

American Express (AXP) – Ditto above, except it charges higher fees and has snob appeal (read higher margins). Its stock has lagged Visa and MasterCard in recent years.

NVIDIA (NVDA) – The leading graphics card maker that is essential for artificial intelligence, gaming, and bitcoin mining. Another great chip play that has flatlined for half a year.

Advanced Micro Devices (AMD) – Stands to benefit enormously from the chip shortage created by the coming 5G and the explosion of the cloud.

Target (TGT) – The one retailer that has figured it out, both in their stores and online. It can’t be ALL tech.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Looks Like a “BUY” Signal to Me

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/buy-signal.png484864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-12 10:02:012021-02-12 10:09:26Ten Stocks to Buy Before You Die

To gain a glimpse into the current psyche of tech investing, we need to take a raw snapshot of the state of Softbank’s Vision Fund.

The Vision Fund is the brainchild of the Japanese telecom company’s founder Softbank Masayoshi Son and is the world’s largest technology-centric venture capital fund with over $100 billion in capital.

The torrent of bullish price action of late has meant that SoftBank recorded a record quarterly profit in its Vision Fund as a gangbusters’ stock market lifted the value of its portfolio companies.

However, the significant gains accrued in equity were also substantially offset by painful derivatives losses as Son attempted to parlay his winnings into leverage directional bets in the short-term.

The Vision Fund’s $8 billion profit in the December quarter is a stark change from the prior March when the pandemic was in full gear and the Fund booked major losses amid embarrassing flops like office space sharing company WeWork.

As 2020 came to a close, tech growth firms like Uber (UBER) stock exploded higher and DoorDash (DASH) gave the Vision Fund a nice payday going public at the end of the year in stellar fashion.

On the options trading front, things didn’t go so rosy.

SoftBank posted a 285.3 billion yen or $2.7 billion derivatives loss in the period.

I understand “hedging your bets” but for Son to create this massive loss undeniably has to infuriate deep-pocketed investors from Arab nations that have stuck with him through tumultuous events.

The staggering option losses was why the asset management arm registered a loss of 113.5 billion yen or $1.08 billion, up from losses of 85.2 billion yen in the previous three-month period.

Experiencing wonderful gains only to have the narrative wiped out because of high stakes option bets is perhaps a sign of the times as phenomena like the Gamestop (GME) have moved to the forefront indicating that players have access to too much liquidity at this point in the market cycle.

Some 15 companies have gone public from the Vision Fund so far, and Son does have a long list of busts and winners.

However, one might assume that he won’t hit on every company as he revealed that his Vision Fund 1 and Vision Fund 2 have invested in a total of 131 companies. In the case of DoorDash, SoftBank invested about $680 million for a stake now worth about $9 billion while its $7.7 billion investment in Uber is worth $11.3 billion.

There are still shining stars on the balance sheet.

Another six more portfolio companies are planning IPOs this year and bringing this volume model to the public markets is logical considering even zombie companies are getting funded out the wazoo at this point.

Tech is also still holding its perch as the darling of the market and Son is simply delivering to market what investors want which is growth tech and more of it.

Other issues on Softbank’s list are to sell off its interests in Alibaba, T-Mobile US Inc., and SoftBank Corp., the Japan telecommunications unit. SoftBank also announced a deal to sell its chip designer Arm to Nvidia (NVDA) for $40 billion.

On top of the risky growth companies, Softbank has also parked its capital in a who’s who of tech firms such as a $7.39 billion investment in Amazon.com (AMZN), $3.28 billion in Facebook (FB). and $1.38 billion in Alphabet or Google (GOOGL). The operation is managed by its asset management subsidiary SB Northstar, where Son personally holds a 33% stake.

Son labeled his options debacle as a “test-drive stage” hoping to play down the fact that he should have made a lot more with the massive ramp-up in tech demand in 2020.

It’s not all smooth for Son with the chaos at Alibaba (BABA), Son’s most exotic investment success to date and SoftBank’s largest asset, tanked 20% last quarter amid a Chinese government clampdown on Alibaba Founder Jack Ma.

This has to worry Son’s future tech investing prospects in China (P.R.C.).

SoftBank’s own sale of Arm to Nvidia (NVDA) is still making the rounds through the EU approval process. The United Kingdom and European Union are both preparing to launch probes into the deal.

All in all, a mixed bag for the Vision Fund where profits should have been higher and most of the damage was self-inflicted.

At some point, throwing massive amounts of capital to juice up tech growth firms will backfire, but the generous access to liquidity that Son has makes this strategy work while even affording him some massive failures.

In short, the Vision Fund should be many times more profitable and it’s a reminder that these leveraged bets aren’t going away which should mean enough liquidity out there to take the markets higher.

We should also be aware that the eventual “market mistake” could give us 10% tech corrections, which are no brainer buying opportunities if the same liquidity volume persists.

Then consider that many tech companies have done well in the recent earnings season and combine that with the eventual reestablishment of buybacks and the neutral observer must think that tech has more room to run in 2021.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-08 11:02:292021-02-14 15:02:00Venture Capitalists Share Clues to the Tech Market

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.