Mad Hedge Biotech & Healthcare Letter

July 23, 2020

Fiat Lux

Featured Trade:

(WHY IT'S OFF TO THE RACES FOR BRISTOL MYERS),

(BMY), (PFE), (GILD), (REGN)

Mad Hedge Biotech & Healthcare Letter

July 23, 2020

Fiat Lux

Featured Trade:

(WHY IT'S OFF TO THE RACES FOR BRISTOL MYERS),

(BMY), (PFE), (GILD), (REGN)

For investors, compounding has long been considered the eighth wonder of the world.

Compounding refers to growing your initial capital over time, boosted by well-timed additions to increase your pool of funds. Warren Buffet calls it “snowballing.”

For compounding to work out, though, it’s important to have a long-term investment plan.

Naturally, the first step to successfully invest is choosing the most suitable stock for your portfolio. Ideally, these businesses should have growth runways set up to thrive in the long run and coupled with clear-cut competitive advantages.

These companies should be able to pay out decent dividends as well since these can later be reinvested to accelerate returns.

Among the companies in the biotechnology and healthcare sector today, Bristol-Myers Squibb (BMY) fits the bill.

The company’s strengths lie in its oncology and hematology departments, with sales for its pipeline of drug candidates estimated to beat expectations.

With the new drugs in late-stage trials, BMY raised its annual sales forecast to reach somewhere between $15 billion and $20 billion. This number is expected to be sustained over the next 10 years.

Many of BMY’s promising programs came from its Celgene acquisition in November 2019.

While the whopping $74 billion deal faced pushback at first, the merger is expected to yield $2.5 billion in savings for BMY. This offers the company more elbow room to invest in its R&D sector.

BMY is working on combining its cancer drugs Opdivo and Yervoy with Celgene’s top moneymakers Revlimid and Pomalys, effectively transforming the New York-based company into the largest seller of cancer treatments in the world.

Outside its immuno-oncology lineup, BMY is also performing quite well in the cardiovascular field.

Its blockbuster drug Eliquis, which is a collaborative effort with Pfizer (PFE), remains one of the highest-selling treatments among atrial fibrillation patients.

In 2019 alone, Eliquis raked in $7.71 billion in sales. As for its performance this year, this heart disease drug is estimated to add another $1 billion, pushing its 2020 annual sales to $8.79 billion.

So far, 8 of BMY’s drugs available in the market generate over $1 billion in yearly sales. The company also has 9 new products undergoing Phase 3 trials, with more than 20 drugs slated for review in the next 10 years.

For 2020, BMY is projected to earn $41.8 billion in revenue and roughly $6.20 per share compared to $4.69 last year.

BMY is also anticipated to generate over $14 billion in free cash this year. Thanks to its Celgene acquisition, the company’s revenue will experience a one-time jump of about 60%.

For 2021, BMY is expected to report a 7.5% revenue growth to reach $45 billion or $7.33 per share. This is just a conservative estimate though.

BMY is an attractive stock right now.

It’s currently trading at roughly $60. The company has about $136 billion in market capitalization and pays an annual dividend of $1.80 for a yield of 3%.

In the past 5 years, except for a single quarter in 2017, BMY reported positive quarterly earnings growth.

The shares trade for 8.6 times its expected earnings in the next 12 months, which is just ridiculous for a premium stock.

In terms of its long-term earnings per share, the company is expected to report a 9.3% growth rate.

Finding value among the biotechnology and healthcare sector has become increasingly tricky.

Since the pandemic broke, industry stalwarts like Gilead Sciences (GILD) and Regeneron Pharmaceuticals (REGN) have been receiving constant media attention for their COVID-19 vaccines and treatments. This pushed their valuations to skyrocket.

However, there remain a number of reasonably affordable biotechnology growth stocks.

While these are not making headlines in the fight against COVID-19, these companies offer attractively high long-term earnings-per-share growth rates – and BMY is one of them.

Global Market Comments

July 22, 2020

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (BABA), (EEM), (FXA), (FCX), (GLD)

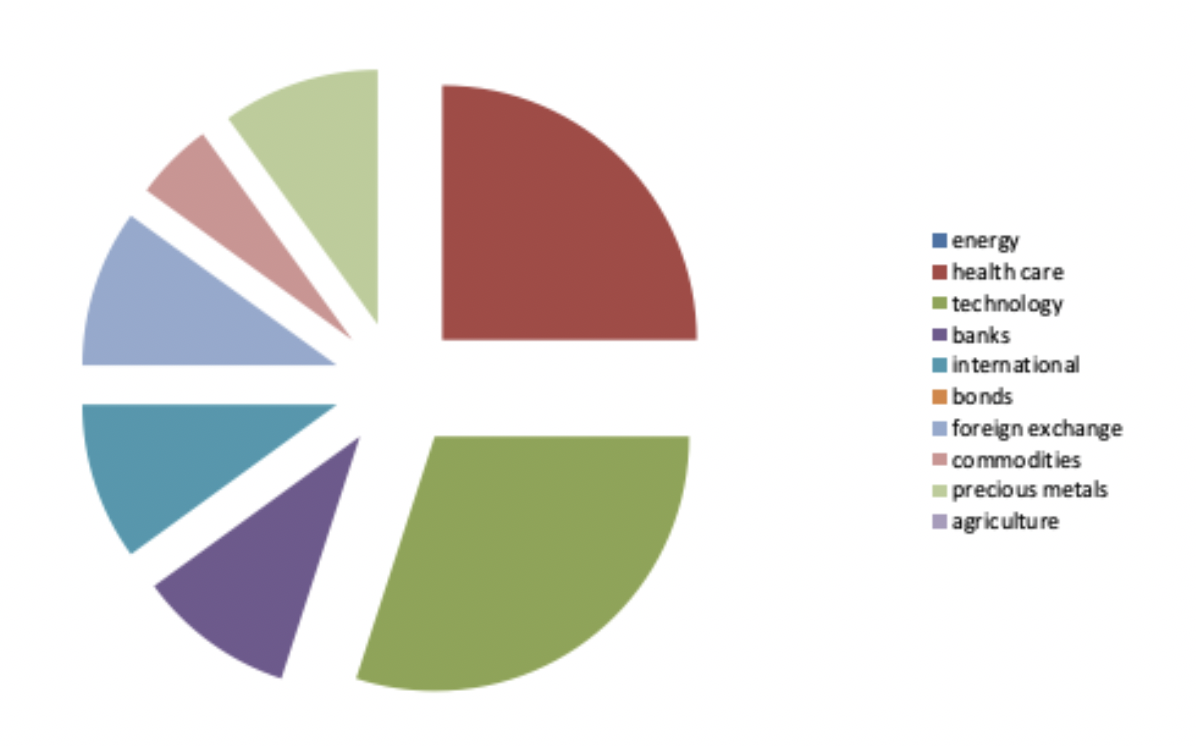

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on October 17, 2019. In fact, not only did we nail the best sectors to go heavily overweight, we completely dodged the bullets in the worst-performing ones, especially in energy.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 70 ½.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red.

To download the entire portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com , log in, go to “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

My 5% holding in Biogen (BIIB) was taken over by Bristol Myers (BMY) at a hefty premium at an all-time high, so I’ll take the win. I am replacing it with Covid-19 vaccine frontrunner Bristol Myers (BMY) itself.

I am also taking out healthcare provider Cigna (CI), whose profits have been hammered by the pandemic. A future Biden administration might also move to a national healthcare system that will cap profits. I am replacing it with another Covid-19 vaccine leader Pfizer (PFE).

My 30% weighting in technology remains the same. Even though these stocks are 30% more expensive than they were three years ago, I believe they will lead the charge into the 2020s. It’s where the big growth is. These have doubled or more over the past nine months.

I am sticking with a 10% weighting in banking. Thanks to trillions in stimulus loans, they are now the most government-subsidized sector of the economy. I also believe that massive bond issuance by the US Treasury will deliver a sharply steepening yield curve, another pro bank development.

With my 10% international exposure, I am taking out a 5% weight in slow-growth Japan and replacing it with Chinese Internet giant Alibaba (BABA). The US will most likely dial back its vociferous anti-Chinese stance next year and (BABA) will soar.

I am executing another switch in my foreign currency exposure, taking out a long in the Japanese yen (FXY) and a short in the Euro (EUO) and substituting in a double long in the Australian dollar (FXA).

Australia will be a leveraged beneficiary of a recovery in the global economy, both through a recovery on commodity prices and gold which has already started, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

I’m quite happy with my 10% holding in gold (GLD), which should move to new all-time highs imminently….and then go ballistic.

As for energy, I will keep my weighting at zero, no matter how cheap it has gotten. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free.

My ten-year assumption for the US and the global economy remains the same.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

July 21, 2020

Fiat Lux

Featured Trade:

(WHY PFIZER AND BIONTECH ARE NOW VACCINE FRONTRUNNERS)

(PFE), (MRNA), (BNTX), (NVAX), (MY), (RHHBY), (SNY)

Pfizer (PFE) and BioNTech (BNTX) have stealthily positioned themselves as the new leaders in the COVID-19 vaccine race.

They recently received an FDA fast-track label for BNT162, pushing the timeline for their vaccine candidate to start late-stage trials for 30,000 patients this July as well — a timeline similar to Moderna’s plans.

Like Moderna’s vaccine candidate, Pfizer and BioNTech also use mRNA technology.

Basically, this system takes advantage of our own biological building block to trigger our body to create proteins. These can then help us protect ourselves from pathogens such as the coronavirus.

The announcement of the FDA fast-track pushed Pfizer stock to immediately jump by 5%, an impressive leap for a company with almost $200 billion in market capitalization. Meanwhile, BioNTech stock rose by 15%.

While the vaccine is anticipated to be launched by December 2020, Pfizer executives appear to be more bullish on the timeline.

In fact, the company expects a release date for the late-stage trial data to be available by September with a potential FDA approval by October.

If Pfizer’s vaccine candidate does manage to pass muster, then the two companies are expected to manufacture almost 100 million doses by the end of the year, with the number reaching 1.2 billion by December 2021.

Other than BNT162, Pfizer and BioNTech also received FDA fast track designations for two of the most advanced candidates in their pipeline, BNT162b1 and BNT162b2.

Having all these vaccine candidates under FDA fast track reviews is a welcome reprieve in this ongoing pandemic.

To say that we need an effective vaccine now more than ever is an understatement. This health crisis has been pushing not only the US but also the entire world on the brink of a financial shutdown.

So far, we have recorded over 13 million cases globally—3.5 million of those come from the US alone. With the increasing number of cases, more and more hospitals are crying out for help because they’re getting overburdened.

Apart from its coronavirus program, Pfizer offers a plethora of opportunities for investors.

In 2019, the company raked in $51.8 billion in revenue.

For this year, Pfizer has been zeroing in on improving its pipeline with eight potential blockbuster products anticipated to generate an additional $1 billion or more in annual sales.

Outside its own pipeline, Pfizer is also expected to reap the rewards from its spinoff Upjohn and the merger of this particular unit with Mylan (MYL).

The new company, called Viatris, will inherit some previous blockbusters from Pfizer.

This move is aimed to pave the way for Pfizer to focus on its rising stars like blood clot treatment Eliquis and heart failure medication Vyndaqel. Overall, these changes are projected to provide a bigger impact on Pfizer’s growth.

Meanwhile, BioNTech is also an interesting company to check out.

As with any typical biotechnology stock with no product out in the market yet, BioNTech remains speculative despite its $17.83 billion market capitalization.

However, its involvement with Pfizer in the development of a COVID-19 vaccine will definitely light a fire under this German company.

With that in mind, BioNTech shouldn’t be considered a one-trick pony.

Prior to its work with Pfizer, the company has been focused on creating individualized cancer treatments. So far, it has 10 cancer drug candidates in the 11 clinical trials underway.

Aside from Pfizer, BioNTech has also been working on other biotechnology and healthcare bigwigs like Sanofi (SNY) and Roche (RHHBY).

The race to complete the Phase 3 of the late-stage clinical trials for the COVID-19 vaccine has been tight.

Initially, it was only Moderna that held the top spot—and the stock definitely flourished because of it. Since the pandemic broke out, this biotechnology company’s stock skyrocketed to a jaw-dropping 202% year to date.

At the time, the close second was another small biotechnology with a market capitalization of $6.44 billion, Novavax (NVAX). The company’s stock also soared by a whopping 252.1% thanks to its COVID-19 efforts.

Now, Pfizer and BioNTech are well on their way to dethroning Moderna—if they haven’t done so already.

With a market capitalization of $198.42 billion compared to Moderna’s $31.9 billion, Pfizer has the upper hand in terms of resources, more extensive access to manufacturing partners, and of course, distribution.

![]()

Global Market Comments

July 14, 2020

Fiat Lux

Featured Trade:

(UPDATE ON THE COVID-19 VACCINE FRONTRUNNER)

(AZN), (MRNA), (RHHBY), (LLY), (PFE), (JNJ)

With the flu season just around the corner and herd immunity nowhere in sight, the pressure to develop a COVID-19 vaccine becomes even more urgent. From where things stand right now though, it looks like we could have a vaccine either already available on the market or ready to hit the market around this time in 2021.

We know we’ll need hundreds of millions of vaccine doses, and the majority of the vaccine programs today are getting built on industrial-scale vaccine platforms. This is positive news.

On an even more positive update, a handful of biotechnology and health care companies are now on late-stage testing for the COVID-19 vaccine.

Leading the charge so far is AstraZeneca (AZN), which received $1.2 billion in financial assistance courtesy of the US government’s Operation Warp Speed program.

AstraZeneca is working on an experimental vaccine, called AZD1222, with the University of Oxford and China National Pharmaceutical Group (Sinopharm).

So far, this is the only COVID-19 vaccine candidate in late-stage Phase 3 trials.

The trials are scheduled to be conducted in different countries, with some already in progress in South Africa, Brazil, and of course, the UK.

The stage will enroll over 10,000 people in the UK alone. The goal is to determine AZD1222’s efficacy in a sizeable group aged 18 and older.

What we know about AstraZeneca’s vaccine candidate is that it’s created from a weakened version of adenovirus, which comes from one of the virus types that causes the common cold. It also includes genetic material from COVID-19, which was added to help the patient’s body recognize the pathogen and trigger a defense mechanism to fight off the infection.

Researchers say that the best-case scenario is for the Phase 3 efficacy results of the AstraZeneca vaccine to be available by this fall.

However, AstraZeneca remains an attractive stock even sans its Covid-19 program thanks to its remarkable drug pipeline. With the foresight to stockpile drugs during this pandemic, the company’s earnings are projected to continuously grow.

In the past five to six years, AstraZeneca has been aggressive in investing in its pipeline to combat patent losses. Now, the company joins Roche (RHHBY) and Eli Lilly (LLY) in the list of companies with the most innovative candidates that are poised to launch commercial products capable of driving growth in the next decade.

A notable growth driver for AstraZeneca is its cancer franchise, particularly its key drug Tagrisso, which is set to tap into a massive market.

Before AstraZeneca was dubbed the leader in the COVID-19 vaccine race, there was Moderna (MRNA). Actually, this small biotechnology company is also expected to begin its late-stage Phase 3 trial in July.

Like AstraZeneca, Moderna is also one of the companies included in the Operation Warp Speed project and received $483 million from the government.

Unlike AstraZeneca, Moderna appears to be experiencing delays due to conflicts between the company’s experts and the US government scientists.

While Moderna shares jumped by over 200% since the pandemic started, these reported tensions represent a risk for its investors. It is particularly alarming because the company is a clinical-stage biotechnology company with no marketed products.

Although Moderna’s timeline remains to be the most aggressive, it could easily drown in the competition.

Keep in mind that other companies competing for the top spot in the COVID-19 race are all established and armed with extensive experience in launching new drugs to market. The list includes Pfizer (PFE), which has a market capitalization of $185.86 billion, and Johnson & Johnson (JNJ) with $375.40 billion.

Needless to say, the inexperience of companies like Moderna could prove to be a handicap in this highly competitive race.

![]()

Mad Hedge Biotech & Healthcare Letter

July 2, 2020

Fiat Lux

Featured Trade:

(FIVE BIOTECH STOCKS TO BUY AT THE MARKET TOP)

(REGN), (GILD), (PFE), (ABBV)

No, this is not a typo, a misprint, nor an alcohol-induced departure from reality. I only buy stocks at market tops when I believe that newer, higher market tops are imminent. That is certainly the case with the entire biotech sector.

That’s why I moved this morning into a very aggressive triple weighting to the sector.

As the world grapples with the COVID-19 pandemic, Regeneron (REGN) has been hailed as one of the “miracle stocks” in the biotechnology sector.

Although late to the party, Regeneron quickly became a frontrunner in the race to find a COVID-19 treatment in June when the company entered clinical trials with its COVID-19 treatment candidate. The New York biotechnology company has already started manufacturing, with the company expecting trial results to be released later this summer.

Regeneron followed the lead of other biotechnology companies repurposing seasoned medicines to treat this deadly disease, such as Gilead Sciences (GILD) and Pfizer (PFE).

Prior to developing it to target SARS-CoV-2, Regeneron’s antibody cocktail had been used to treat Ebola.

In response to Regeneron’s promising progress on the COVID-19 treatment, the market showed its appreciation by pushing the company’s shares up over 60% year-to-date.

Needless to say, Regeneron has been heavily outperforming the broad biotechnology indexes and even the broader market.

However, Regeneron’s success these days isn’t only attributed to its COVID-19 efforts. In fact, Regeneron’s annual revenue has been consistently increasing for more than a decade now.

Prior to starting its coronavirus program, the company has already lined up several candidates that can serve as catalysts for growth.

One of the catalysts for Regeneron’s growth is skin cancer injection Libtayo.

At present, Libtayo dominates the advanced cutaneous squamous cell carcinoma market as seen in the 179% jump in its sales to hit $75 million in the first quarter of 2020.

Riding on the momentum of Libtayo’s current sales, Regeneron is also looking to expand its coverage to include non-small cell lung cancer and basal cell carcinoma.

This means that Libtayo still has a long way to go before it reaches its peak.

To give this drug’s potential some context, keep in mind that roughly 9,500 individuals in the United States alone get a skin cancer diagnosis every day. Meanwhile, over 3 million Americans are diagnosed with either basal cell carcinoma or squamous cell carcinoma each year.

As for non-small cell lung cancer, this disease accounts for 84% of over 228,000 cases of lung cancer in the US annually.

Combined, the market size of Libtayo could reach roughly 3.2 million patients.

Libtayo is priced at $9,100 to cover a three-week treatment course. Patients are advised to regularly take the infusion every three weeks. This puts the annual cost of Libtayo treatment somewhere around $158,000.

With this annual treatment cost and the projected total market size in mind, it’s safe to say that Libtayo can yield profits of well over 12 figures. This is the best-case scenario, though.

If we go for the least likely scenario, where Regeneron only reaches 10,000 patients for all the diseases mentioned, then the company can still generate an annual revenue exceeding $1.5 billion.

As for the other products in Regeneron’s pipeline, the company’s recent earnings report showed that sales in the first quarter were only marginally impacted by the pandemic.

For instance, Eylea’s annual growth rate was only at 6%. Nonetheless, this wet macular degeneration and metastatic colorectal cancer medication’s first quarter sales still reached a decent $1.9 billion.

Moreover, there’s a growing market that can substantially boost Eylea’s performance in the coming years.

Studies show that the global market for wet age-related macular degeneration is projected to rise at an annual rate of 7.1%. By 2024, this market could reach $10.4 billion.

Aside from Eylea, Regeneron’s eczema biologic Dupixent sales have been soaring as well. This drug went up by an impressive 124% year-over year, generating $855 million in revenue.

Dubbed as Regeneron’s “pipeline in a product,” the company is looking to transform Dupixent into a mega-blockbuster drug like AbbVie’s (ABBV) Humira.

So far, Dupixent is being studied to determine if it can also be marketed to asthma patients and recently gained approval to be cover atopic dermatitis as well.

Overall, Regeneron merits a closer look, especially among biotechnology investors searching for a dependable stock with a lot more room to grow.

Not only does the company have over $7.2 billion in cash and have minimal debt, it also has a remarkable profit growth.

In the first quarter of 2020 alone, Regeneron’s bottom line jumped by a whopping 48% year over year to reach $771 million or $6.60 per share.

Looking at its annualized rate, Regeneron stock is actually trading for roughly 22 times earnings -- a reasonable price to pay for a well-rounded blue chip company that offers such impressive growth and a strong track record.