Mad Hedge Technology Letter

December 30, 2024

Fiat Lux

Featured Trade:

(THE UNBEATABLE PARTNERSHIP)

(EMR), (GRMN), (AMBA), (NVDA), (DXCM), (CSCO), (INTC), (QCOM)

Mad Hedge Technology Letter

December 30, 2024

Fiat Lux

Featured Trade:

(THE UNBEATABLE PARTNERSHIP)

(EMR), (GRMN), (AMBA), (NVDA), (DXCM), (CSCO), (INTC), (QCOM)

Let me introduce to you one of the hottest trends in tech.

It has been on the tip of everyone's tongue for years, and that might be an understatement, but the interaction of the Internet of Things (IoT) and artificial intelligence (AI) offers companies a wide range of advantages.

In order to get the most out of IoT systems and to be able to interpret data, the symbiosis with AI is almost a must.

If the Internet of Things is merged with data analysis based on artificial intelligence, this is referred to as AIoT.

Moving forward, expect this to be the hot new phrase in an industry backdrop where investors love these hot catchphrases and monikers.

What is this used for?

Lower operating costs, shorter response times through automated processes, and helpful insights for business development are just a few of the notable advantages of the Internet of Things.

AI also offers a variety of business benefits: it reduces errors, automates tasks, and supports relevant business decisions. Machine learning as a sub-area of AI also ensures that models – such as neural networks – are adapted to data. Based on the models, predictions and decisions can be made. For example, if sensors deliver new data, they can be integrated into the existing modules.

The Statista Research Institute assumes that there will be 200 billion networked devices by 2026.

This is exactly where AI comes into play, which generates predictions based on the sensor values received.

However, many companies are still unable to properly benefit from the potential of connecting IoT and AI, or AIoT for short.

They are often skeptical about outsourcing their data - especially in terms of security and communication.

In part because the increased number of networked devices, which requires the connection of IoT and AI, increases the security requirements for infrastructure and communication structure enormously.

It is not surprising that companies are unsettled: Industrial infrastructures have grown historically due to constantly increasing requirements and present companies with completely new challenges, which manifest themselves, for example, in an increasing number of networked devices. With the combination of IoT and AI, many companies are venturing into relatively new territory.

By connecting IoT and AI, a continuous cycle of data collection and analysis is developing.

But, companies can no longer deny the advantages of AIoT because this technical combination makes networked devices and objects even more useful.

Based on the insights generated by the models, those responsible can make decisions more easily and reliably predict future events. In this way, a continuous cycle of data collection and analysis develops. With predictive maintenance, for example, production companies can forecast device failures and thus prevent them.

The combination of the two technologies also makes sense from the safety point of view: continuous monitoring and pattern recognition help to identify failure probabilities and possible malfunctions at an early stage – potential gateways can thus be better identified and closed in good time.

The result: companies optimize their processes, avoid costly machine failures, and at the same time reduce maintenance costs and thus increase their operational efficiency.

In this way, IoT and AI represent a profitable fusion: While AI increases the benefit of existing IoT solutions, AI needs IoT data in order to be able to draw any conclusions at all.

AIoT is, therefore, a real gain for companies of all sizes. They thus optimize processes, are less prone to errors, improve their products, and thus ensure their competitiveness in the long term.

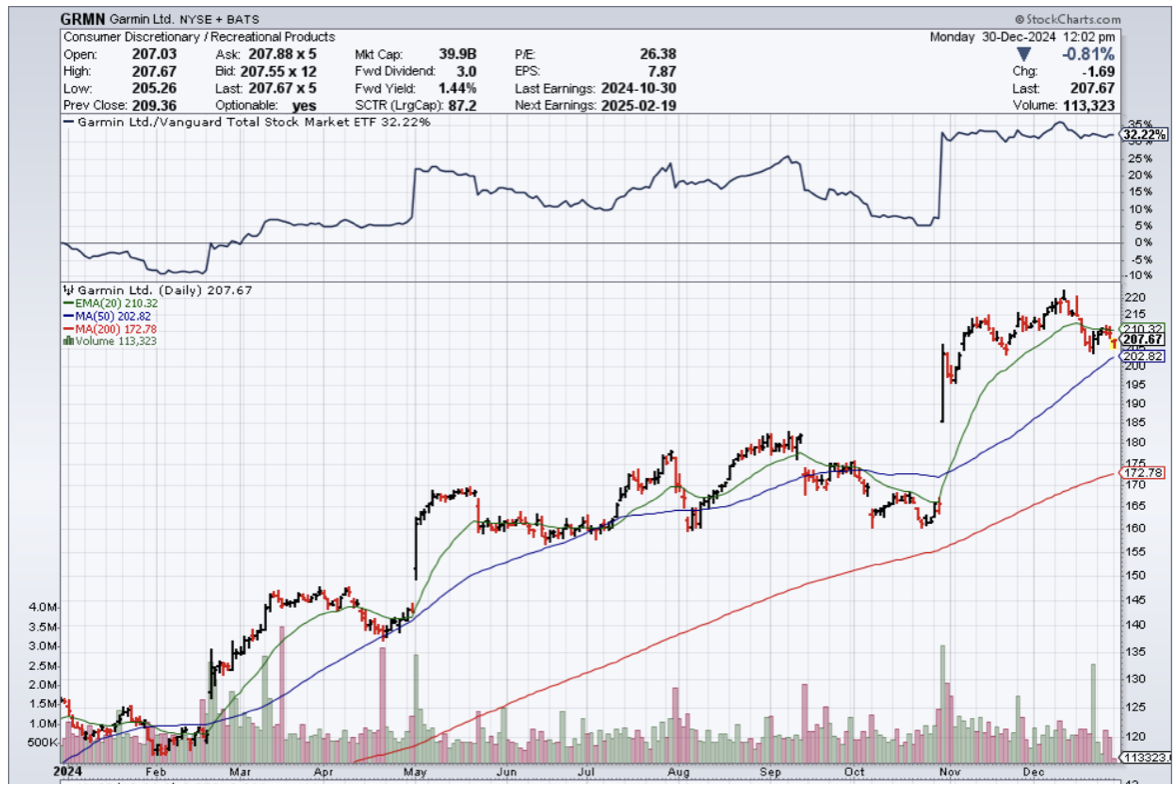

Some hardware, software, and semiconductor stocks that will offer exposure into AIoT are Emerson Electric Co. (EMR), Garmin (GRMN), Ambarella (AMBA), Nvidia (NVDA), DexCom (DXCM), Cisco (CSCO), Intel (INTC), and Qualcomm (QCOM).

Mad Hedge Technology Letter

July 26, 2024

Fiat Lux

Featured Trade:

(THE UNBEATABLE PARTNERSHIP)

(EMR), (GRMN), (AMBA), (NVDA), (DXCM), (CSCO), (INTC), (QCOM)

Let me introduce to you one of the hottest trends in tech.

It has been on the tip of everyone's tongue for years, and that might be an understatement, but the interaction of the Internet of Things (IoT) and Artificial Intelligence (AI) offers companies a wide range of advantages.

In order to get the most out of IoT systems and to be able to interpret data, the symbiosis with AI is almost a must.

If the Internet of Things is merged with data analysis based on artificial intelligence, this is referred to as AIoT.

Moving forward, expect this to be the hot new phrase in an industry backdrop where investors love these hot catchphrases and monikers.

What is this used for?

Lower operating costs, shorter response times through automated processes, and helpful insights for business development are just a few of the notable advantages of the Internet of Things.

AI also offers a variety of business benefits: it reduces errors, automates tasks, and supports relevant business decisions. Machine learning as a sub-area of AI also ensures that models – such as neural networks – are adapted to data. Based on the models, predictions and decisions can be made. For example, if sensors deliver new data, they can be integrated into the existing modules.

The Statista Research Institute assumes that there will be 75 billion networked devices by 2025.

This is exactly where AI comes into play, which generates predictions based on the sensor values received.

However, many companies are still unable to properly benefit from the potential of connecting IoT and AI, or AIoT for short.

They are often skeptical about outsourcing their data - especially in terms of security and communication.

In part because the increased number of networked devices, which requires the connection of IoT and AI, increases the security requirements for infrastructure and communication structure enormously.

It is not surprising that companies are unsettled: Industrial infrastructures have grown historically due to constantly increasing requirements and present companies with completely new challenges, which manifest themselves, for example, in an increasing number of networked devices. With the combination of IoT and AI, many companies are venturing into relatively new territory.

By connecting IoT and AI, a continuous cycle of data collection and analysis is developing.

But companies can no longer deny the advantages of AIoT because this technical combination makes networked devices and objects even more useful.

Based on the insights generated by the models, those responsible can make decisions more easily and reliably predict future events. In this way, a continuous cycle of data collection and analysis develops. With predictive maintenance, for example, production companies can forecast device failures and thus prevent them.

The combination of the two technologies also makes sense from the safety point of view: continuous monitoring and pattern recognition help to identify failure probabilities and possible malfunctions at an early stage – potential gateways can thus be better identified and closed in good time.

The result: companies optimize their processes, avoid costly machine failures, and at the same time reduce maintenance costs and thus increase their operational efficiency.

In this way, IoT and AI represent a profitable fusion: While AI increases the benefit of existing IoT solutions, AI needs IoT data in order to be able to draw any conclusions at all.

AIoT is therefore a real gain for companies of all sizes. They thus optimize processes, are less prone to errors, improve their products and thus ensure their competitiveness in the long term.

Some hardware, software, and semiconductor stocks that will offer exposure into AIoT are Emerson Electric Co. (EMR), Garmin (GRMN), Ambarella (AMBA), Nvidia (NVDA), DexCom (DXCM), Cisco (CSCO), Intel (INTC), and Qualcomm (QCOM).

Mad Hedge Technology Letter

September 13, 2023

Fiat Lux

(A GREAT CHIP STOCK TO BUY AND HOLD)

(QCOM), (APPL), (SOC), (SAMSUNG), (TSM)

If there is a company I would tell my grandkids to work for then it would be semiconductor company Qualcomm (QCOM).

Why?

Even Apple (APPL) can’t replace them so easily and that counts for a lot in this day and age.

We learned just as much as Qualcomm said that it will supply Apple with 5G modems for smartphones through 2026.

Qualcomm expected to lose the Apple smartphone business, because they expected Apple to use an internally developed 5G modem starting in 2024.

They couldn’t develop the product fast enough so it is back snapping up modems with QCOM.

QCOM is the best of breed for smartphone chips and they can be found in every flagship Android device.

I am specifically referring to QCOM’s Snapdragon products which are a suite of system on a chip (SoC) semiconductor products for mobile devices.

The Snapdragon's central processing unit (CPU) uses the ARM architecture.

This line of chips is incredibly competitive and one of the foundational reasons to hold the stock.

Samsung’s SoC competitor named the Exynos is still a far cry from the Snapdragon no matter how hard they try and it seems like each iteration of the Exynos flagship SoC is always a generation behind the Snapdragon.

Apple do use their own SoC with the newest one named the Apple A17 Bionic, but QCOM will still monopolize the Android market with their own Snapdragon that is actually slightly better than the A17 Bionic chip.

The Snapdragon 8 Gen 3 beats the CPU clock speed of the A17 Bionic.

This doesn’t always translate to better real-world performance, but it’s still an impressive feat.

People believe the new Taiwan Semiconductor Manufacturing Company (TSM) 3 nanometer (nm) processing can lose to the advanced 4nm node on the 8 Gen 3.

However, Apple will probably maintain a CPU lead, thanks to better software tuning and more transistors in the same area thanks to a smaller 3-nanometer node.

Basically, Snapdragon is a little faster but Apple has higher performance because of its superior software.

There is no denying that Apple has fantastic software.

On the revenue side, this is great news for the staying power of Snapdragon products and continued sales to Apple will boost Qualcomm’s handsets business, which reported $5.26 billion in sales in the past quarter and could soften the blow of potentially losing a critical customer.

About 21% of Qualcomm’s fiscal 2022 revenue of $44.2 billion came from Apple.

APPL purchased Intel’s smartphone modem division in 2019 to build its own modem. However, evidence suggests that it will be challenging for Apple to move away from Qualcomm’s chips because of their complexity.

Qualcomm also makes money from Apple through cellular licensing fees, which were about $1.9 billion in 2022.

Qualcomm continues to collect royalties from Apple under a six-year agreement. That agreement was struck at the end of a legal battle between Apple and Qualcomm over royalties that was settled in 2019.

Qualcomm says that it expects to only supply 20% of the modems needed for Apple’s 2026 smartphone launch, signaling that it likely still expects the Apple business to eventually decline.

Apple’s new iPhone called iPhone 15 uses QCOM modems as do many other high-end smartphones.

It’s hard to believe that QCOM’s market capitalization is only $125 billion. The eye test alone makes me think this is a half a trillion-dollar company.

Revenue is accelerating and they offer a 2.9% dividend yield.

I can’t talk more about the high quality of products made by QCOM.

This company will have staying power and even if Apple decides to move on, there are a slew of companies ready to gobble up QCOM chips.

Readers shouldn’t trade this stock, but they should buy and hold for the long haul.

Mad Hedge Technology Letter

February 27, 2023

Fiat Lux

Featured Trade:

(THE UNBEATABLE PARTNERSHIP)

(EMR), (GRMN), (AMBA), (NVDA), (DXCM), (CSCO), (INTC), (QCOM)

Let me introduce to you one of the hottest trends in tech.

They have been on the tip of everyone's lips for years, and that might be an understatement, but the interaction of the internet of things (IoT) and artificial intelligence (AI) offers companies a wide range of advantages.

In order to get the most out of IoT systems and to be able to interpret data, the symbiosis with AI is almost a must.

If the Internet of Things is merged with data analysis based on artificial intelligence, this is referred to as AIoT.

Moving forward, expect this to be the hot new phrase in an industry backdrop where investors love these hot catchphrases and monikers.

What is this used for?

Lower operating costs, shorter response times through automated processes, and helpful insights for business development are just a few of the notable advantages of the Internet of Things.

AI also offers a variety of business benefits: it reduces errors, automates tasks, and supports relevant business decisions. Machine learning as a sub-area of AI also ensures that models – such as neural networks – are adapted to data. Based on the models, predictions and decisions can be made. For example, if sensors deliver new data, they can be integrated into the existing modules.

The Statista research institute assumes that there will be 75 billion networked devices by 2025.

This is exactly where AI comes into play, which generates predictions based on the sensor values received.

However, many companies are still unable to properly benefit from the potential of connecting IoT and AI, or AIoT for short.

They are often skeptical about outsourcing their data - especially in terms of security and communication.

In part because the increased number of networked devices, which requires the connection of IoT and AI, increases the security requirements for infrastructure and communication structure enormously.

It is not surprising that companies are unsettled: Industrial infrastructures have grown historically due to constantly increasing requirements and present companies with completely new challenges, which manifest themselves, for example, in an increasing number of networked devices. With the combination of IoT and AI, many companies are venturing into relatively new territory.

By connecting IoT and AI, a continuous cycle of data collection and analysis is developing.

But companies can no longer deny the advantages of AIoT because this technical combination makes networked devices and objects even more useful.

Based on the insights generated by the models, those responsible can make decisions more easily and reliably predict future events. In this way, a continuous cycle of data collection and analysis develops. With predictive maintenance, for example, production companies can forecast device failures and thus prevent them.

The combination of the two technologies also makes sense from the safety point of view: continuous monitoring and pattern recognition help to identify failure probabilities and possible malfunctions at an early stage – potential gateways can thus be better identified and closed in good time.

The result: companies optimize their processes, avoid costly machine failures, and at the same time reduce maintenance costs and thus increase their operational efficiency.

In this way, IoT and AI represent a profitable fusion: While AI increases the benefit of existing IoT solutions, AI needs IoT data in order to be able to draw any conclusions at all.

AIoT is therefore a real gain for companies of all sizes. They thus optimize processes, are less prone to errors, improve their products and thus ensure their competitiveness in the long term.

Some hardware, software, and semiconductor stocks that will offer exposure into AIoT are Emerson Electric Co. (EMR), Garmin (GRMN), Ambarella (AMBA), Nvidia (NVDA), DexCom (DXCM), Cisco (CSCO), Intel (INTC), and Qualcomm (QCOM).

Mad Hedge Technology Letter

July 8, 2022

Fiat Lux

Featured Trade:

(THE END OF SAMSUNG)

(SAMSUNG), (QCOM), (MU), (AAPL)

Samsung, Korea’s stalwart chaebol, is toast.

Remember the past two years when lockdowns were in vogue?

Digital products were the hottest item in the world as everybody was stuck in their homes.

Growth brought forward is never a bad thing for a company, especially tech companies.

However, it sets the stage for hard comps to topple and a reversion back to the mean which can look messy.

The world needed chips and phones back then, the world is now traveling, getting on planes, and taking cruise ships to the Caribbean.

This is why video game growth is quite subdued this year.

Samsung internally has also been taking a machete to its forward-looking estimates multiple times in order to front-run collapsing demand.

The boom bust nature of chips and devices is an inherent beast in the industry that is hard to tame.

Samsung was able to hit watered-down targets in the second quarter, but that was mainly due to a 7% currency tailwind of the Korean won sliding fast just like many Asian currencies.

Take a look at the Japanese yen, it’s gone off a cliff all the way to 136 per $1.

I remember when I took a vacation to Tokyo in 2011, Japan felt awfully expensive at 77 yen to $1.

The currency tailwinds are a transitory elixir yet under the hood, these economies are weakening fast.

The aging population and cost of living crisis are also crushing sales.

Internal data reveals deeper damage than initially thought.

Operating profit missed by a wider margin than revenue beat and prices for its premium products isn’t fetching the prices they once did.

For example, Samsung markets its Exynos 2200 chips as on-par rivals to the Snapdragon 8 Gen 1 and Apple’s (AAPL) A15 Bionic chip found in smartphones.

However, the Exynos fails to compete with its supposed flagship chip comps, performing at levels lagging almost a generation behind in speed and functionality.

It’s clear that devices made with Exynos chips simply won’t be able to sell for as much as flagship Android phones with Snapdragon 8 Gen 1 or Apple iPhones with A15 Bionic chips.

I fully expect the operation profit to go from 6% to 3% for Samsung.

US rival Micron (MU) has already rung the alarm. While the world’s third-largest maker of DRAM posted revenue and operating profit for the quarter in line with estimates, its forecast for the coming three months was 20% lower than expectations.

It now sees the PC and smartphone markets much weaker than previously thought.

Tech has experienced a massive downgrade in terms of sentiment and sales while massive pressure on the supply side costs.

Cloud computing and streaming services which all need chips have been the poster boys of underperformance.

Growth stocks have also gotten killed.

I do believe this is more a signal of deeper individual malaise at Samsung and an indication they are getting trounced by Chinese firms who just do it better for cheaper.

Margins won’t ever come back up for Samsung as they lack the nimbleness of the Chinese and brute power of the American tech.

They are essentially stuck between a rock and a hard place where products will become less competitive, face rapidly shrinking margins, and participate in a Korean economy that lacks vibrancy.

Once chip stocks bottom, avoid Samsung, and get into Qualcomm (QCOM) and Micron (MU).