Global Market Comments

June 2, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADING INTO STALL SPEED),

(GLD), (SPY), (MSTR), (AAPL), (QQQ), (TSLA), (SLV), (SIL), (WPM)

Global Market Comments

June 2, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADING INTO STALL SPEED),

(GLD), (SPY), (MSTR), (AAPL), (QQQ), (TSLA), (SLV), (SIL), (WPM)

Global Market Comments

May 30, 2025

Fiat Lux

Featured Trade:

(The Mad Hedge June Traders & Investors Summit is ON!)

(MAY 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(MSTR), (DAX), (SPY), (UPS), (UNP), (FDX), (SLV), (GLD)

Global Market Comments

May 2, 2025

Fiat Lux

Featured Trade:

(APRIL 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXI), (AGQ), (NVDA), (SH), (UNG), (USO),

(TSLA), (SPX), (CCJ), (USO), (GLD), (SLV)

Below, please find subscribers’ Q&A for the April 30 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Why is the Australian dollar not moving against the US dollar as much as the other currencies?

A: Australia is too closely tied to the Chinese economy (FXI), which is now weak. When the Chinese economy slows, Australia slows. Australia is basically a call option on the Chinese economy. So they're not getting the ballistic moves that we've seen in, say, the Euro and the British pound, which are up about 20%. Live by the sword, die by the sword. If you rely on China as your largest customer for your export commodities, you have to take the good and the bad.

Q: I see we had a terrible GDP print on the economy this morning, down 0.3%. When are we officially in a recession?

A: Well, the classical definition of a recession is two back-to-back quarters of negative GDP growth. We now have one in the bank. One to go. And this quarter is almost certain to be much worse than the last quarter, because the tariffs basically brought all international trade to a complete halt. On top of that, you have all of the damage to the economy done by the DOGE cuts in government spending. Approximately 80% of the US states, mostly in the Midwest and South, are very highly dependent on Washington spending for a healthy economy, and they are going to really get hit hard. So the question now is not “do we get a recession?”, but “how long and how deep will it be?” Two quarters, three quarters, four quarters? We have no idea. Even if trade deals do get negotiated, those usually take years to complete and even longer to implement. It just leaves a giant question mark over the economy in the meantime.

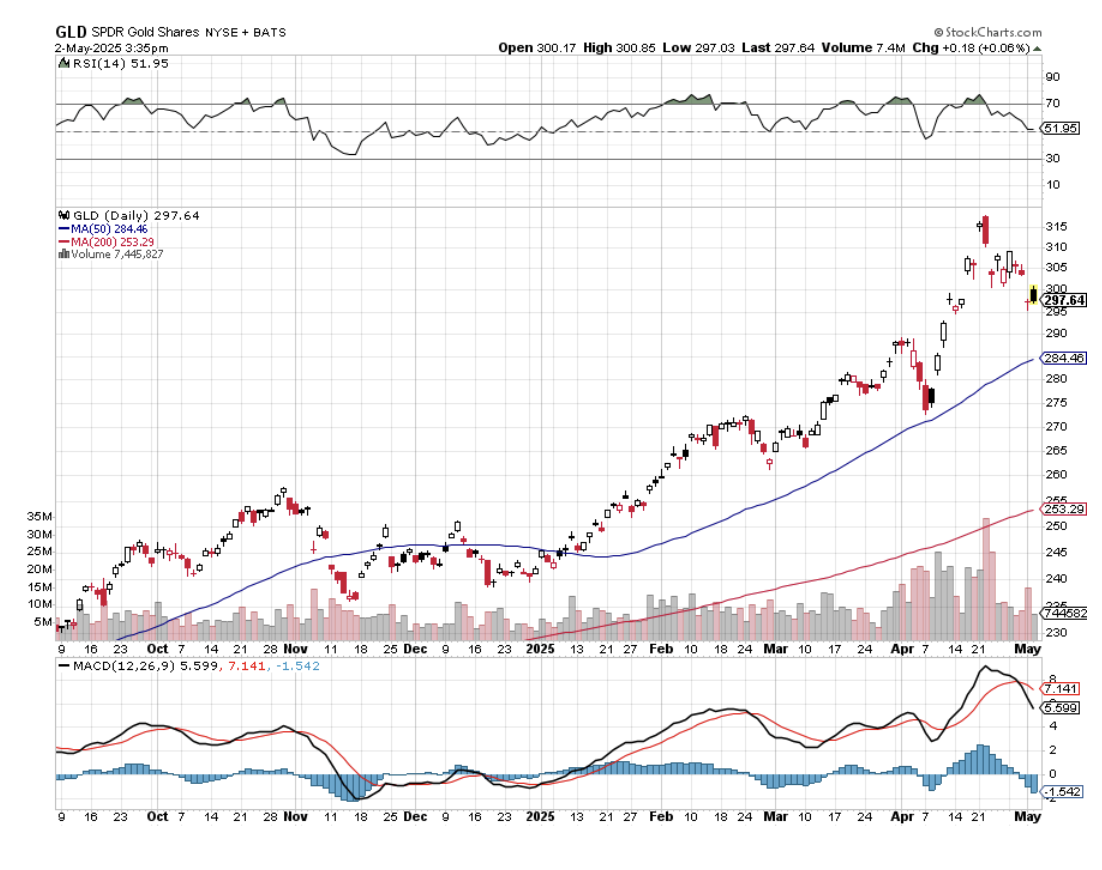

Q: Is SPDR Gold Trust (GLD) the best way to play gold, or is physical better?

A: I always go for the (GLD) because you get 24-hour settlement and free custody. With physical gold, you have to take delivery, shipping is expensive, and insurance is more expensive. Plus, then you have to put it in a vault. Private vaults have a bad habit of going bankrupt and disappearing with your gold. You keep it in the house, and then if the house burns down, all your gold is gone there. Plus, it can get stolen. There's also a very wide dealing spread between bid and offer on physical gold coins or bars; usually it's at least 10%, often more. So I often prefer the ease of trading with the GLD, which owns futures on physical gold, which is held in London, England. So that is my call on that.

Q: Is ProShares Ultra Silver (AGQ) the leveraged silver play?

A: It absolutely is, but beware: (AGQ) is only good for short, sharp rises because the contango and the storage operating costs of any 2x are very, very high—like 10% a year. So, good if you're doing a day trade, not good for a one-year hold. Then you're just better off buying silver (SLV).

Q: What is more important with the Fed's mandate—unemployment or fear of inflation?

A: That's an easy one. Historically, the number one priority at the Fed has been inflation. That is their job to maintain the full faith and credit of the U.S. Dollar, and inflation erodes the value, or at least the purchasing power of the US dollar, so that has always historically been the priority. Until we see inflation figures fall, I think the chance of them cutting interest rates is zero, and we may not see actual falls until the end of the year, because the next influence on prices is up because of the trade war. The trade war is raising prices everywhere, all at the same time. So that will at least add 1 or 2% to inflation first before it starts to fall. You can imagine how if we get a 6% inflation rate, there's no way in the world the Fed can cut rates, at least for a year, until we get a new Fed governor. So that has always historically been the priority.

Q: Do you think the 10-year yield is going down to 5%?

A: You know, we're really in a no-man's-land here. Recession fears will drive rates down as they did yesterday. I haven't even had a chance to see where the bond market is this morning because. So, rates are rising on a recessionary GDP, which is the worst possible outcome. Rates should be falling on a recessionary GDP print. Of course, Washington’s efforts to undermine the U.S. dollar aren't helping. Threatening to withhold taxes on interest payments to foreign owners is what caused the 10% down move in bonds in one week—the worst move in the bond market in 25 years. So, the mere fact that they're even thinking about doing something like that scares foreign investors, not only from the bond market, but all US investments period. And certainly, we've seen some absolutely massive stock selling from them.

Q: Why won't the market go down to 4,000 in the S&P 500?

A: Absolutely, it could; that is definitely within range. That would put us down 30% from the February highs, it just depends on how long the recession lasts. If you just get a two-quarter shallow recession, we could bounce off 4800 for the (SPX) until we come out. If the recession continues for several quarters, and it's looking like it will, then 4,000 is definitely within range. So, it's all about the economy. And remember, stocks are expensive. They don't get cheap until we get a PE multiple of 16, and even then, that alone, just a multiple shrinkage would take us down to 4,000.

Q: Would it be a good idea to buy the S&P 500 (SPY) as it falls?

A: I'm getting emails from readers asking if it's time to buy Nvidia (NVDA) or time to buy Tesla (TSLA). What I've noticed is that investors are constantly fighting the last battle. They're always looking for what worked last time, and that does not succeed as an investment strategy. As long as I'm selling rallies, I'm not even thinking about what to buy on the bottom. The world could look completely different on the other side. The MAG-7 may not be the leadership in the future, especially with the Trump administration trying to dismantle four out of seven companies through antitrust, and the rest are tied up in the trade wars. So, tech is still expensive relative to the main market, and we're going to need to look for new leaders. My picks are going to be mining shares, gold, and banking. Those are the ones I'm looking to buy on dips, but right now, cash is king unless you want to play on the short side. Being paid 4.3% to stay away sounds pretty good to me, especially when your neighbors have 30% losses. You know, I've heard of people having all of their retirement funds in just two stocks: Nvidia and Tesla, and they're getting wiped out. So, you don't want to become one of them.

Q: After a tremendous run in Gold, is Silver a better risk-reward right now?

A: I would say yes, it is. Silver has been lagging gold all year because central banks, the most consistent buyers for the past decade, buy gold—they don't buy silver. But what we may be in store for here now is a prolonged sideways move in gold while the technicals catch up with it. And in the meantime, the money goes elsewhere into silver and Bitcoin. That's my bet.

Q: Is Apple (APPL) a no-touch now?

A: I’d say yes. The trade war is changing by the day, and Apple probably does more international trade than any other company in the world. Also, Apple gets hit with recessions like everybody else. There was a big front run to buy Apple products ahead of tariffs—my company bought all its computer and telephone needs for the whole year ahead of the tariffs. We're not buying anything else this year. And I would imagine millions more are planning to do the same, so you could get some really big hits in Apple earnings going forward.

Q: Should I sell my August Proshares Short S&P 500 (SH) LEAPS?

A: No, I would keep them. If the (SPX) IS trading between 5,000 to 5,800, your $4-$42 SH LEAPS should expire at max profit in August, so I'm hanging on to mine. Next time we take a run at 5,000, you should be able to get out of your SH LEAPS at 80% to 90% of the max profit.

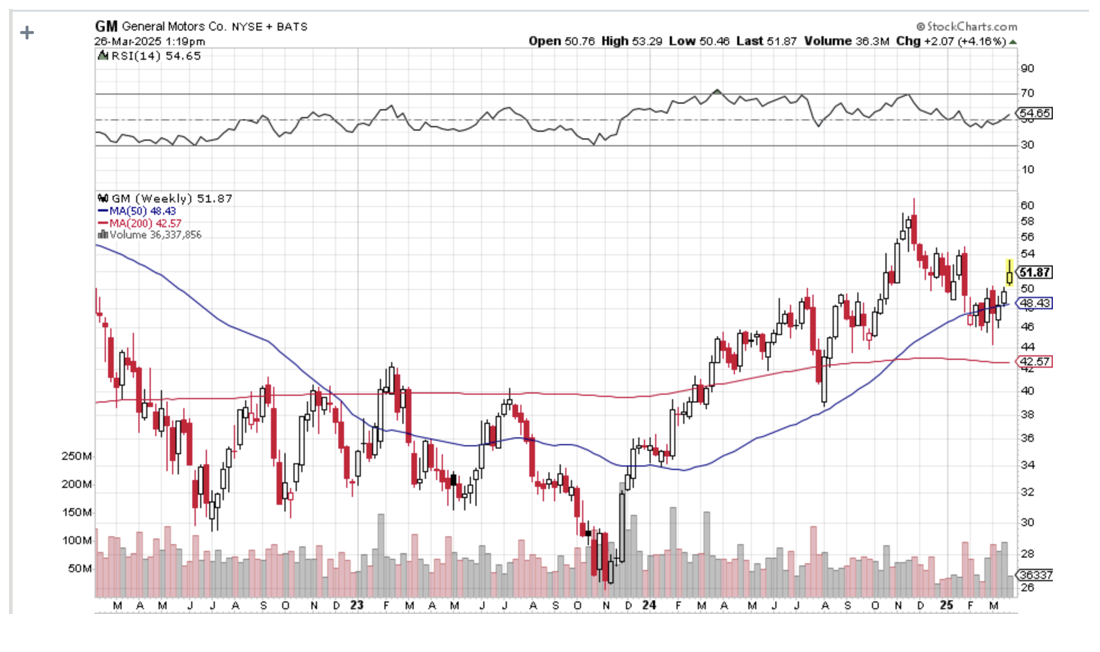

Q: What car company stock will do the best in a high-tariff global economy?

A: Tesla (TSLA), because 100% of their cars are made in the US with 90% US parts (the screens come from Panasonic in Japan). Their foreign components are only about 10%, so they can eat that. For General Motors (GM), it's more like 30% of all components are made abroad, and they can't eat that; their profit margins are too low. (GM) expects to lose $5 billion because of tariffs. By the way, the profit margins on Tesla have fallen dramatically from 30% down to 10% in two years, so it's not like they're in great shape either. Also, Tesla hasn’t had a CEO for ten months, which is why the board is looking for a replacement.

Q: Is it a good time to buy the dip in oil (USO)?

A: Absolutely not. Oil is the most sensitive sector to recessions, because if you can't sell oil, you have to store it, very expensively. It costs 30 to 40% a year to store oil—that's the contango; and once all the storage is full, then you have to cap wells, which then damages the long-term production of the wells. I think at some point you will expect an announcement from Washington to refill the Strategic Petroleum Reserve, which was basically sold by Biden at $100 a barrel. You can now get it back for $60. That may not be a bad idea if you're going to have a strategic petroleum reserve. What's better is just to quit using oil completely, which we were on trend to do.

Q: Will interest rates drop by year-end?

A: They may drop by year-end once unemployment runs up to 5% or 6% —which is likely to happen in a recession—and inflation starts to decline, even if it declines from a higher level. Even if they don't cut by year end, they'll still cut in a year when the president can appoint a new Fed governor. What the Trump really needs to do is appoint Janet Yellen as the Fed governor. She kept interest rates near zero for practically all of her term. We need another Yellen monetary policy.

Q: The job market here seems to be slowing quite fast. Is there any way this will rebound and stave off recession?

A: No, there is not. Companies are going to be looking to cut costs as fast as they can to offset the shrinkage in sales, but also to help cope with tariffs. So no, the job market is actually surprisingly strong now. That means future data releases are probably going to get a lot worse. In April, we saw job gains in Health care, adding 51,000 jobs. Other sectors posting gains included transportation and warehousing (29,000), financial activities (14,000), and social assistance. I highly doubt any of these sectors will show gains next month.

Q: What about nuclear energy plays?

A: I like them, partly because people are buying stocks like Cameco Corp (CCJ) as a flight to safety commodity play, like they're buying gold, silver, and copper. But also, this administration is supposed to be deregulation-friendly, and the only thing holding back nuclear (at least new modular reactors) is regulation. That and the fact that no one wants to live next door to a nuclear power plant, for some strange reason.

Q: What do I think about natural gas (UNG)?

A: Don't touch. Don't buy the dip. All energy plays look terrible right here, going into recession.

Q: What are your thoughts on manufacturing returning to the U.S? And how will that affect the stock market?

A: I think there's zero chance that any manufacturing returns to the U.S. Companies would rather just shut down than operate money-losing businesses. You know, if your labor cost goes from $5 to $75 an hour, there's no chance anyone can make money doing that, and no shareholders are going to want to touch that stock. That is the basic flaw in having a government where no one is actually running a manufacturing business anywhere in the government. They don't know how things are actually made. They're all real estate or financial people.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 17, 2025

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT REPLAYS ARE UP)

(APRIL 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (SH), (SDS), (TLT), (MSTR), (GLD),

(GOLD), (SLV), (AGQ), (NEM)

Below, please find subscribers’ Q&A for the April 16 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Is it time to get out of the (SH), which is the short S&P 500 LEAPS?

A: I would say no. We're still very deep in the money for the LEAPS I put out two months ago. I doubt we're going to new highs by August when that LEAPS expires, so I would hang on to it, especially if you have other longs on the stock market. But if you're nervous, you probably have at least a 50% profit in that anyway, so take the money and run.

Q: Could the S&P 500 trade down to 4,500?

A: Absolutely, yes. China is kind of in a good position. They can wait. They can wait a very long time until they get what they want. We can't. Trump needs China to fold immediately, or the trade with China will cause a never-ending recession in the US. Remember, we have elections here—in China, they don't. That puts them in a very strong negotiating position. That's why you're seeing basically all economic data roll over and point to a recession. Even if some settlement is negotiated, there still will be some tariffs left. They just won't be at 145%. You know, it’s not a great investment environment to bet your retirement savings on, and certainly not an environment to engage in very rapid short-term trading unless you have 50 years of experience like I do. That's why I'm up this month, and the rest of the world is getting absolutely crushed.

Q: Are you going to send more LEAPS?

A: LEAPS are something we do at market bottoms, not tops, because we have such enormous leverage in the LEAPS trade—they’re usually 10 - 1 to 100 - 1 leverage. At some point, there'll be a lot of fantastic LEAPS in technology stocks, but I don't think we've hit bottom yet. In fact, at best, they've mounted weak bounces over the last few days. So, the charts still look terrible—not a good time for LEAPS.

Q: When do you see the bottom?

A: I have no idea, nobody has any idea. It's like economic policy is changing hour by the hour. Best thing to do is nothing in that situation—and that's what most of the economy is doing. That's why the economy is shutting down. Nobody knows what the final picture will look like—the uncertainty is the greatest since the uncertainty of the pandemic, or 9/11 before that.

Q: Should I hide in a money market fund?

A: No, with the money market fund, you run credit risk with the issuer of that fund. With 90-day US Treasury bills, there's no risk, so you have a government guarantee to get all your money back on the maturity date. If your custodian goes bankrupt, you can always get the T-bills back. It may take you three years in custodian bankruptcy proceedings to get your money market fund back. That’s what we saw with MF Global in 2011.

Q: What is the end game of the China-US trade dispute? How does it affect the stock market?

A: Well, we can't see an end game. Basically, you have two counterparties who are stubborn as heck, and we could be stuck in no man's land for a very long time. You'd have to think eventually a settlement of some type comes. Is that worth a recession for the U.S? For most people, I doubt it. And what if China just wants to wait out Trump and wait for the tariffs to go away in four years? That is a possible outcome. Stock markets always discount the worst-case scenario first before they discount anything else. I think that's what we saw last week, when we broke 5,000 in the S&P 500.

Q: Are you optimistic about bank stocks now?

A: No. They will lead the downturn along with technology stocks. But when this all ends, they will also lead the upturn, and that's why you're seeing bank stocks have such hard bounces off their bottom. It's another one of two sectors that people will be first to rush into—banks and technology stocks. And while tech is expensive, banks are cheap.

Q: How can interest rates fall when government policies, interest rate policies, are causing them to spike?

A: Well, it's very simple: when foreign investors lose faith in the U.S. Government, they have, they pull their money out. They don't need to be here. It's a situation of, “Well, if you don't need us, we don't need you.” And foreigners own about 25% of all of the $36 trillion in national debt out there, or about $9 trillion. And in stocks they own here and the number goes up to $12 trillion. It doesn't take much selling to cause a panic in the bond market. That is what we have been seeing. Whether that continues, I have no idea—it depends on the next tweet coming out of Washington.

Q: What about Bank of America (BAC)?

A: Yeah, it will also bounce the hardest off the bottom—great buy, and these things are all cheap relative to technology stocks. You know, banks still have PE multiples in the low teens. Tech stocks are all the way down to the low 20s from the 30s and 40s, so they're roughly trading at double the multiples of bank stocks. That's one reason people are rushing back into these.

Q: What's the basis of your prediction on a falling US dollar?

A: Again, it's foreign selling. I don't think I've ever seen a falling dollar and rising interest rates in 60 years of watching. It goes against all economic fundamentals in the currency markets. But when there's a panic, there's a panic. People want out of everything at any price, and that's what's happening now. As long as foreigners are dumping our assets, the dollar will keep going down—dumping our assets means dollar selling after 80 years of dollar buying.

Q: Is gold the only safe haven?

A: Yes. We'll get into this in the gold section, but even gold went down for three days, and then wiser heads prevailed and it actually triggered a panic melt-up in gold assets. The miners were up 25% in days. That is another great weak-dollar play.

Q: How do you protect the US from a dollar fall?

A: Change our economic policies; end the trade war.

Q: Is it a good time to buy a house?

A: No, it is not, unless you can wait out the current downturn. High interest rate mortgage rates shot up from 6.5% to 7.1% in a week, and that basically kills off the housing market for the foreseeable future. And of course, when people are worried about their futures, their savings, and their assets, the last thing they do is go out and buy a house.

Q: Is there enough negative sentiment around now for us to go back into the bond market?

A: No. There is no precedent for the type of market action that's going on now. Will the U.S. government suddenly become reasonable? I doubt it. You can expect tweet bombs to happen at any time. So, people are just hoarding cash and avoiding risk at all costs. It used to be that bonds were the safe place to go. No longer. Not with 10% moves down in a week like we saw last week. Sorry—T-Bills are the only actual safe play out there, and their yield is the same as Treasury bonds without the risk.

Q: Will crypto keep going down?

A: If we continue with a risk-off market, I think you can expect crypto to keep falling. Crypto fell 30% from its top—at least Bitcoin did. It's basically matching the downside with tech stocks one for one, so no protection in crypto, no diversification. The protection aspect that was promised by crypto promoters lever shows. No flight to safety is happening there whatsoever. And that's why I'm looking to add to my short in MicroStrategy Inc. (MSTR)—they're a leveraged long Bitcoin play.

Q: Is the U.S. economy set for a hard landing?

A: I think absolutely, yes, the hard landing is in progress. That's what all of the economic data says. It's hard to find any positive news coming out of the economy—people are running for their lives, essentially.

Q: Do you expect inflation to return and take stocks lower?

A: Absolutely, yes. The highest tariffs in history start hitting retail prices in the next month or two, and the price increases should be dramatic, especially on anything from China. So yeah, we should see that come out in the data in the next few months.

Q: Do you expect silver to follow gold?

A: Yes, I do, but it hasn't been performing as well because there is a recession drag on silver, which you don't have for gold. Silver (SLV), (AGQ) are used in a lot of electronics and solar panels.

Q: When do you get back into gold (GLD)?

A: Whenever we get a dip. So far, any dips have been very brief and short-term. It's kind of reminiscent of the 1970s when gold moved from $32 an ounce to $900. That’s when you found me in a line in Johannesburg, South Africa, waiting to sell all my Krugerrands.

Q: Which countries will benefit from manufacturing moving out of China?

A: The answer is really no countries. As soon as manufacturing moves from China to another one like Vietnam, the US then puts punitive tariffs on that second country. So, there's no place to hide. It's really a war against the world. That's the message that the administration is putting out: if you don't want to build a factory here, we don't want to do business with you. We don't want your products. And most companies will do nothing. They'll wait this out, wait for a future president to eliminate all tariffs. Until then, international trade grinds to a halt. No trade makes sense at 145% tariff. Just to give you some idea on how much that is, if you buy a top end MacBook Pro for $8,000, and you pay the full 145% tariff, that is an $11,600 tariff if you have to pay it, which brings the total cost of a MacBook Pro to nearly $19,600. How many are you going to buy at that price?

Q: Do you think the Fed will cut interest rates?

A: No, we haven't seen the inflation data yet. They are backward-looking, and only after we see a sharp rise in prices will they raise rates. Chances of them cutting now are zero with all the risks in inflation to the upside right now and unemployment still under control. So, no interest rate cuts this year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 4, 2025

Fiat Lux

Featured Trade:

(APRIL 4 BIWEEKLY STRATEGY WEBINAR Q&A),

(DAL), (LCID), (RIVN), (MSTR), (PLTR),

(AAPL), (GLD), (TSLA), (SLV), (SPY)

Below please find subscribers’ Q&A for the April 2 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Why are there days when both bonds and interest rates are going up?

A: Well, there is a tug-of-war going on in the bond market. When recession fears are the dominant theme of the day, interest rates go down and bond prices go up. Remember, it's an inverse relationship. When the deficit and inflation are the big fears and you get those on the inflation announcement days—we get three or four of those a month—then interest rate goes up and bonds go down. That will be a big driver of stock prices because they are very sensitive to interest rates always.

Q: Do you think Tesla (TSLA) has hit bottom?

A: I don't think so. I think the declining sales continue. I think the Tesla brand has been severely damaged as long as Elon Musk stays in politics. Also, no one buys cars in recessions—sorry, but that is the last thing that people or companies want to buy is a brand-new car.

Q: What will happen to the smaller EV makers?

A: They will all go bankrupt. You know, unless they have a very rich uncle like Lucin Group (LCID) does—Saudi Arabia can keep pumping money in there forever. Amazon owns a big piece of Rivian Motors (RIVN) I don't think any of the small EV makers will make it because they now have Tesla to compete against.

Q: Do you have any way to short restaurant stocks as an industry?

A: I don't know of a single industry ETF for restaurants only. Restaurants are not an industry I have spent a lot of time studying because the margins are so low. I prefer a 70% margin to a 3% margin ones. There are a lot of things like consumer discretionary, so you just have to go shopping in the ETF world. There are more than 3,000 listed ETFs these days in every conceivable subsector of the economy, more than there are listed stocks, so there might be something out there somewhere. Yes, you are correct in wanting to short restaurants going into a recession as well as airlines, rental car companies, and hotels, but these things are already down a lot—you know, 40% or so. So, be careful shorting after these things have already had enormous declines in a very short time.

Q: Will the recession cause Democrats to win midterm elections?

A: If I were a betting man—and of course I'm not, I only go after sure things, —I would say yes. But, you know, 18 months might as well be 18 years in the political world. So, who knows what will happen? Suffice it to say that yesterday's election results were overwhelmingly positive for the Democrats and represent a very strong “no vote” for Trump policies and Musk policies. Even in Florida where they won, the victory margin shrank from 35% six months ago to 12%. That is an enormous swing in the electorate away from Republicans, and that's why the Republicans are very nervous about any election. That's why the Texas governor is blocking a by-election there. He’s afraid he’ll lose.

Q: Is Tesla (TSLA) toast for good?

A: If Elon Musk went back to Silicon Valley and just managed Tesla and kept his mouth shut on non-Tesla issues, I bet the stock would double from these levels over the medium term. So yes, it just depends on how much Elon Musk wants his $200 billion back. That's how much he's lost on the stock depreciation since December.

Q: Is it time to short Delta Air Lines (DAL)?

A: You kind of missed the boat. No point in closing the barn door after the horses have bolted. This was a great short in February, and the same with hotels and rail companies. So be careful of your biggest recession indicators; they have all already collapsed and are more likely to bounce along the bottom.

Q: What are the probabilities that the tariff war could backfire, and we end up with massive job losses and a shortage of goods?

A: Actually, that is the most likely outcome. In my humble opinion, we know big layoffs are coming already. Prices are going to go up, so people will buy less. And prices will go up a lot because of the tariffs, so it's the perfect, perfect economy destruction strategy. And of course, that all feeds directly into the stock market.

Q: Do you think a 10% decline is enough to reflect all of that?

A: Absolutely not. More like down 20% or down 30% to discount the destruction of the economy—some say by half. So, that's an easy question to answer.

Q: Do you think Palantir (PLTR) will recover from this dip?

A: Only when government spending resumes. That could happen sooner once we get some clarity on where the government is actually going to spend its money. Palantir claims they can save masses of money for the government by getting it just to use their software, and a lot of companies are making that claim, like Arthur Anderson, who also had all their contracts axed. So, we don't know. “We don't know” is the most commonly heard expression in the country today. We just don't know what's going to happen.

Q: And is Palantir (PLTR) cheap after a 40% sell-off?

A: No. It's still incredibly expensive and that is the concern.

Q: Is crypto a good short-term bet in this type of high volatility?

A: No, it's not. It's a horrible bet. A 10% decline in the S&P 500 delivered a 30% decline in crypto. If we drop another 10%, you can expect crypto to drop another 30%. You know, it's like a 3x long NASDAQ ETF. That's how it's behaving. So, I watch it very carefully as a risk indicator. If we get a substantial rally, I'm looking to short the big players in crypto, which would be MicroStrategy (MSTR) and ProShares Bitcoin Strategy ETF (BITO). Looking for a good short there or at least to write calls. The call premiums are extremely high on all these crypto plays—sometimes they're 84%.

Q: How much more inflation can the economy handle before we are in a deep recession?

A: Well, I think we're in recession now. Almost every inflation indicator is pointing to lots of upside and, of course, the tariffs haven't even started yet. They start today, and it'll take at least a month or two to see what the actual impact of the tariffs will be on local prices.

Q: Why do you think the tariffs will be damaging to the economy?

A: Virtually every economist in the world has agreed that the trade wars of the 1930s were a major cause of the Great Depression, but not the sole cause. The only economists that have changed their minds now are the ones that have just gotten Trump appointments. I mean, that's it, clear and simple. You raise the price, you get less demand—basic supply and demand economics. I'm not inventing anything new here. It’s basic economics 101.

Q: Here's a good question that has puzzled people for a century: If Copper is up, why is Freeport McMoRan (FCX) down?

A: Freeport is a stock first and a commodity producer second. When stocks crash, people flee to commodities, and that is what is happening. Chinese are buying up copper ingots as a gold alternative, and people are dumping Freeport because it's in an index. Some 80% of all the selling is index selling. So if you're in that index, your stock goes down regardless of your individual fundamentals. Whether it's a good company or not, whether your earnings are expanding or not, I'm seeing this happen in lots of other great companies.

Q: Is gold (GLD) subject to 25% import duties? What will that do to the pricing of gold?

A: Physical gold got an exemption, so it is not. However, gold stocks in COMEX warehouses in New York hit record highs as the managers rushed to bring in gold to beat the tariffs to meet the ETF demand in the United States. So there’s a lot of turmoil in that market, as there are in all markets now—people trying to beat the tariffs. By the way, I bought all the computer equipment my company needs for the rest of this year in order to beat the tariff increases because all my Apple (AAPL) stuff comes from China and they're looking at 60% tariffs.

Q: If the silver (SLV) does go to a new all-time high, does that mean the S&P 500 is going to an all-time high?

A: No, if anything (SPY) goes to a multi-year low. We may be losing a generation of stock investors here. That puts silver within easy range at $50.

Q: Will biotech stocks shift because of the policy changes?

A: They're losing their government research funding, the authorization process for new drug approvals has had sand thrown at it. Time delays have been greatly extended on new approvals and suffice to say, the leadership does not have the confidence of the industry, and biotech stocks are doing horribly. You know, when you appoint someone to head a department whose main job is to dismantle that department, that's generally really horrible for the industry, especially when the industry is dependent so much on government grants for research. We are losing a generation of new scientists. That puts off any cures for cancer, Alzheimer’s, or diabetes into the far future.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 27, 2025

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

One of the most fascinating things I learned when I first joined the equity trading desk at Morgan Stanley during the early 1980s was how to parallel trade.

A customer order would come in to buy a million shares of General Motors (GM), and what did the in-house proprietary trading book do immediately?

It loaded the boat with the shares of Ford Motors (F).

When I asked about this tactic, I was taken away to a quiet corner of the office and read the riot act.

“This is how you legally front-run a customer,” I was told.

Buy (GM) in front of a customer order, and you will find yourself in Sing Sing shortly.

Ford (F), Toyota (TM), Nissan (NSANY), Daimler Benz (DDAIF), BMW (BMWYY), and Volkswagen (VWAPY), were all fair game.

The logic here was very simple.

Perhaps the client completed an exhaustive piece of research concluding that (GM) earnings were about to rise.

Or maybe a client's old boy network picked up some valuable insider information.

(GM) doesn’t do business in isolation. It has thousands of parts suppliers for a start. While whatever is good for (GM) is good for America, it is GREAT for the auto industry.

So through buying (F) on the back of a (GM) might not only match the (GM) share performance, it might even exceed it.

This is known as a Primary Parallel Trade.

This understanding led me on a lifelong quest to understand Cross Asset Class Correlations, which continues to this day.

Whenever you buy one thing, you buy another related thing as well, which might do considerably better.

I eventually made friends with a senior trader at Salomon Brothers while they were attempting to recruit me to run their Japanese desk.

I asked if this kind of legal front-running happened on their desk.

“Absolutely,” he responded. But he then took Cross Asset Class Correlations to a whole new level for me.

Not only did Salomon’s buy (F) in that situation, they also bought palladium (PALL).

I was puzzled. Why palladium?

Because palladium is the principal metal used in catalytic converters, it removes toxic emissions from car exhaust and has been required for every U.S.-manufactured car since 1975.

Lots of car sales, which the (GM) buying implied, ALSO meant lots of palladium buying.

And here’s the sweetener.

Palladium trading is relatively illiquid.

So, if you catch a surge in the price of this white metal, you would earn a multiple of what you would make on your boring old parallel (F) trade.

This is known in the trade as a Secondary Parallel Trade.

A few months later, Morgan Stanley sent me to an investment conference to represent the firm.

I was having lunch with a trader at Goldman Sachs (GS) who would later become a famous hedge fund manager, and asked him about the (GM)-(F)-(PALL) trade.

He said I would be an IDIOT not to take advantage of such correlations. Then he one-upped me.

You can do a Tertiary Parallel Trade here by buying mining equipment companies such as Caterpillar (CAT), Cummins (CMI), and Komatsu (KMTUY).

Since this guy was one of the smartest traders I ever ran into, I asked him if there was such a thing as a Quaternary Parallel Trade.

He answered “Abso******lutely,” as was his way.

But the first thing he always did when searching for Quaternary Parallel Trades would be to buy the country ETF for the world’s largest supplier of the commodity in question.

In the case of palladium, that would be South Africa (EZA).

Since then, I have discovered hundreds of what I call Parallel Trading Chains and have been actively making money off of them. So have you, you just haven’t realized it yet.

I could go on and on.

If you ever become puzzled or confused about a trade alert I am sending out (Why on earth is he doing THAT?), there is often a parallel trade in play.

Do this for decades as I have and you learn that some parallel trades break down and die. The cross relationships no longer function.

The best example I can think of is the photography/silver connection. When the photography business was booming, silver prices rose smartly.

Digital photography wiped out this trade, and silver-based film development is still only used by a handful of professionals and hobbyists.

Oh, and Eastman Kodak (KODK) went bankrupt in 2012.

However, it seems that whenever one Parallel Trading Chain disappears, many more replace it.

You could build chains a mile long simply based on how well Apple (AAPL) or NVIDIA (NVDA) is doing.

And guess what? There is a new parallel trade in silver developing. Whenever someone builds a solar panel anywhere in the world, they use a small amount of silver for the wiring. Build several tens of millions of solar panels and that can add up to quite a lot of silver.

What goes around comes around.

Suffice it to say that parallel trading is an incredibly useful trading strategy.

Ignore it at your peril.