Global Market Comments

April 18, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GET READY TO SELL IN MAY)

($INDU), (SPY), (TLT), (WFC), (JPM), (TSLA), (TWTR)

Global Market Comments

April 18, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GET READY TO SELL IN MAY)

($INDU), (SPY), (TLT), (WFC), (JPM), (TSLA), (TWTR)

So when you are supposed to “Sell in May and go away”, what are you supposed to be doing on April 18?

Not much.

War, inflation, disease, runaway energy prices, and soaring interest rates are usually not a good backdrop for trading stocks. When the wind is blowing against me with gale-force winds instead of behind me, I tend to quit. I only like playing games that are rigged in my favor, or in yours.

Retreating to fight another day sounds like a good strategy to me because it’s much easier to dig out of a small hole than a large one. And it’s impossible to recover if you lost all your money chasing marginal low-quality trades. That 100-day cruise around the world that Cunard is offering right now looks pretty good. If the central bank says it is set on slowing the economy, believe it. The free Fed put is a distant memory.

But whatever Armageddon we are facing out there, it will be a modest one. We now have an unemployment rate of 3.6%, but there are still 11 million open jobs. That means there are more jobs in the US right now than workers, a first in history.

There are in fact several big positives the markets are ignoring right now because it is fashionable to do so. You know these supply chain problems? They’re slowly going away. You see this in falling freight rates for US truckers.

The Cass Freight Index measure of domestic shipping demand edged up a bare 0.6% in March from the month before, an unseasonable slowing of growth at the end of the quarter. From where I sit, the number of Chinese container ships at anchor in San Francisco Bay is on a definite decline.

Going into real recessions, consumers usually baton down the hatches, don their hard hats, and reign in spending. And while they tell pollsters they are worried about the economy, they act like they believe in the opposite, spending with reckless abandon. Wells Fargo (WFC) has seen spending on credit cards soaring by 33% in Q1, while it has jumped by an impressive 29% at JP Morgan (JPM).

There is also a great positive out there which is being completely ignored by the market. The pandemic is gone. Daily cases have dropped from one million to only 20,000 in two months, a record drop in the history of epidemiology. Masks are now only required at mass events like rock concerts and the San Francisco Ballet.

So I will endeavor to entertain you with my stories long enough to keep you from getting bored until trading stocks becomes the slam dunk no-brainer affair it once was. That would be in anything from 2-5 months.

Elon Musk makes $53 billion takeover bid for Twitter in a move that gobsmacked Wall Street. He made the offer in a 281-character tweet to the board of directors. His goal will be to end all censorship, which means bringing back the crazies and the violent. If they don’t accept his premium offer, then he will sell the 9.9% of shares that he already owns and the board will get sued to death by shareholders.

Inflation jumps to 8.5% YOY, a 40-year high, with half of the increase coming from gasoline prices. Stocks and bonds were up on a “buy the rumor, sell the news” move. Unless oil prices completely collapse, next month will be worse.

Producer Price Index rockets by 11.2%, an 11-year high. This is on the heels of yesterday’s red hot Core Inflation report. It makes a half-point rate hike on April 29 a sure thing.

Retail Sales jumped 0.5% in March, and up 6.9% YOY, while import prices hit an 11-year high.

Bonds hit new three-year lows, with yields soaring to 2.81% overnight. The market is transitioning from a Fed that is raising rates from a quarter point at each meeting to a half point. We may be reaching the end of this leg down, off $9.00 in weeks. Only sell the big rallies. (TLT) LEAPS holders are sitting pretty.

Mortgage Refis down 67% YOY, thanks to a 30-year fixed rate mortgage that has topped 5.0%. It looks like the loan sharks won’t be grabbing as much in fees. This market won’t recover for several years. If you didn’t refi last year at century low rates, you’re screwed.

NVIDIA downgraded from outperform to neutral and the price target was chopped from $360 to $225 by Baird & Co. It’s a bold move as (NVDA) has long been a Mad Hedge favorite and 70-bagger over the last five years. Baird cites cancellations driven by a combination of excess GPUs, or graphics processing unit in Western Europe and Asia, as well as a slowdown in consumer demand, especially in China. Slowing consumer demand for GPUs was evident in the continuing reduction in graphics card pricing. I believe any slowdowns are temporary and you should keep buying (NVDA) on dips.

Used Car Sales take a hit, as affordability becomes a major issue. Carmax just reported a 6.5% plunge in Q4. I can sell my Tesla Model X for more than I paid three years ago because it takes a year to get a new one.

Weekly Jobless Claims hit 185,000, up 18,000 from the previous week. The stock market may be worried about a coming recession but the jobs market sure isn’t.

Morgan Stanley blows away earnings. Equity trading came in a hot $3.2 billion and bond trading $2.9 billion. The shares popped 7% on the news. Buy (MS) on dips.

Mercedes breaks 600 miles range on a single charge with its EQXX prototype, driving from Stuttgart to the French Riviera. But the cost per watt is still double Tesla’s. Mercedes plans to go all-electric by the end of the decade.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

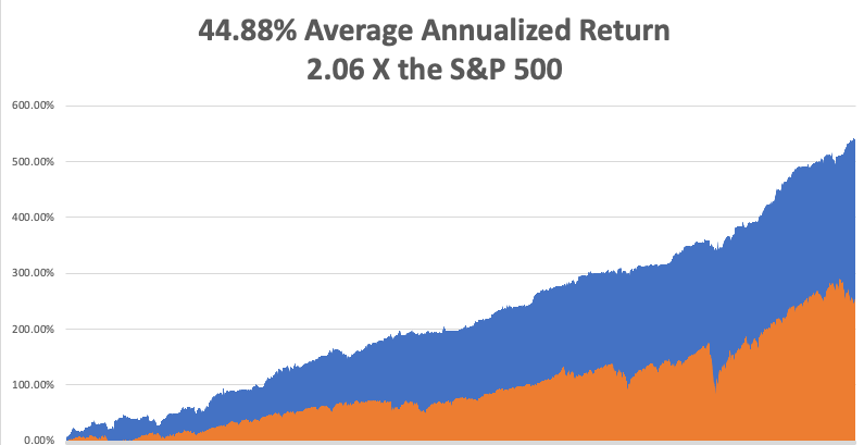

My March month-to-date performance retreated to a modest 0.38%. My 2022 year-to-date performance ended at a chest-beating 27.23%. The Dow Average is down -5.1% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 68.55%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 100% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 539.79%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.6 million, up only 300,000 in a week and deaths topping 988,000 and have only increased by 3,000 in the past week. You can find the data here. Growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 18 at 7:00 AM EST, the NAHB Housing Market Index is out. Bank of America (BAC) reports.

On Tuesday, April 19 at 8:30 AM, Housing Starts for March are published. Netflix (NFLX) reports.

On Wednesday, April 20 at 8:30 AM, the Existing Home Sales for March are printed. Tesla (TSLA) reports.

On Thursday, April 22 at 7:30 AM, the Weekly Jobless Claims are printed. Union Pacific (UNP) reports.

On Friday, April 23 at 8:30 AM, the S&P Global Composite Flash PMI is disclosed. American Express (AXP) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are out.

As for me, the call from Washington DC was unmistakable, and I knew what was coming next. “How would you like to serve your country?” I’ve heard it all before.

I answered, “Of course, I would.”

I was told that for first the first time ever, foreign pilots had access to Russian military aircraft, provided they had enough money. You see, everything in the just collapsed Soviet Union was for sale. All they needed was someone to masquerade as a wealthy hedge fund manager looking for adventure.

No problem there.

And can you fly a MiG29?

No problem there either.

A month later, I was wearing the uniform of a major in the Russian Air Force, my hair cut military short, sitting in the backseat of a black Volga limo, sweating bullets.

“Don’t speak,” said my driver.

The guard shifted his Kalashnikov and ordered us to stop, looked at my fake ID card and waved us on. We were in Russia’s Zhukovky Airbase 100 miles north of Moscow, home of the country’s best interceptor fighter, the storied Fulcrum, or MiG-29.

I ended up spending a week at the top-secret base. That included daily turns in the centrifuge to make sure I was up to the G-forces demand by supersonic flight. Afternoons saw me in ejection training. There in my trainer, I had to shout “eject, eject, eject,” pull the right-hand lever under my seat, and then get blasted ten feet in the air, only to settle back down to earth.

As a known big spender, I was a pretty popular guy on the base, and I was invited to a party every night. Let me tell you that vodka is a really big deal in Russia, and I was not allowed to leave until I had finished my own bottle, straight.

In 1993, Russia was realigning itself with the west, and everyone was putting their best face going forward. I had been warned about this ahead of time and judiciously downed a shot glass of cooking oil every evening to ward off the worst effects of alcohol poisoning. It worked.

Preflight involved getting laced into my green super tight gravity suit, a three-hour project. Two women tied the necessary 300 knots, joking and laughing all the while. They wished me a good flight.

Next, I met my co-pilot, Captain A. Pavlov, Russia’s top test pilot. He quizzed me about my flight experience. I listed off the names: Laos, Cambodia, Thailand, Israel, Croatia, Serbia, Bosnia, Kuwait, Iraq, and Saudi Arabia. It was clear he still needed convincing.

Then I was strapped into the cockpit.

Oops!

All the instruments were in the Cyrillic alphabet….and were metric! They hadn’t told me about this, but I would deal with it.

We took off and went straight up, gaining 50,000 feet in two minutes. Yes, fellow pilots, that is a climb rate of an astounding 25,000 feet a minute. They call them interceptors for a reason. It was a humid day, and when we hit 50,000 feet, the air suddenly turned to snowflakes swirling around the cockpit.

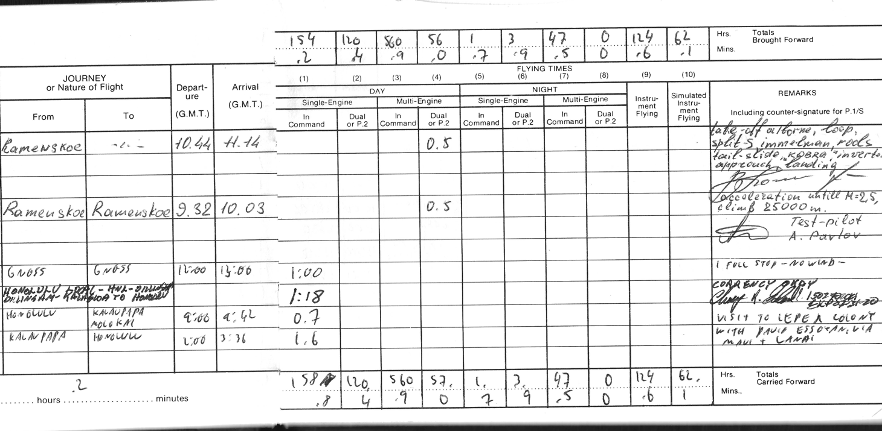

Then we went through a series of violent spins, loops, and other evasive maneuvers (see my logbook entry below). Some of them seemed aeronautically impossible. I watched the Mach Meter carefully, it frequently danced up to the “10” level. Anything over ten is invariably fatal, as it ruptures your internal organs.

Then Pavlov said, “I guess you are a real pilot, and he handed the stick over to me. I put the fighter into a steep dive, gaining the maximum handbook speed of March 2.5, or 2.5 times the speed of sound, or 767.2 miles per hour in seconds. Let me tell you, there is nothing like diving a fighter from 90,000 feet to the earth at 767.2 miles per hour.

Then we found a wide river and buzzed that at 500 feet just under the speed of sound. Fly over any structure over the speed of sound and the resulting shock wave shatters concrete.

I noticed the fuel gages were running near empty and realized that the Russians had only given me enough fuel to fly for an hour. That’s so I wouldn’t hijack the plane and fly it to Finland. Still, Pavlov trusted me enough to let me land the plane, no small thing in a $30 million aircraft. I made a perfect three-point landing and taxied back to base.

I couldn’t help but notice that there was a MiG-25 Foxbat parked in the adjoining hanger and asked if it was available. They said “yes”, but only if I had $10,000 in cash on hand, thinking this was an impossibility. I said, “no problem” and whipped out my American Express gold card.

Their eyes practically popped out of their heads, as this amounted to a lifetime of earnings for the average Russian. They took a picture of the card, called in the number, and in five minutes I was good to go.

They asked when I wanted to fly, and as I was still in my gravity suite I said, “How about right now?” The fuel truck duly back up and in 20 minutes I was ready for takeoff, Pavlov once again my co-pilot. This time, he let me do the takeoff AND the landing.

The first thing I noticed was the missile trigger at the end of the stick. Then I asked the question that had been puzzling aeronautics analysts for years. “If the ceiling of the MiG-25 was 90,000 feet and the U-2 was at 100,000 feet, how did the Russians make up the last 10,000 feet?

“It’s simple,” said Pavlov. Put on full power, stall out at 90,000 feet, then fire your rockets at the apex of the parabola to make up the distance. There was only one problem with this. If your stall forced you to eject, the survival rate was only 50%. That's because when the plane in free fall hit the atmosphere at 50,000 feet, it was like hitting a wall of concrete. I told him to go ahead, and he repeated the maneuver for my benefit.

It was worth the risk to get up to 90,000 feet. There you can clearly see the curvature of the earth, the sky above is black, you can see stars in the middle of the day, and your forward vision is about 400 miles. We were the highest men in the world at that moment. Again, I made a perfect three-point landing, thanks to flying all those Mustangs and Spitfires over the decades.

After my big flights, I was taken to a museum on the base and shown the wreckage of the U-2 spy plane flown by Francis Gary Powers shot down over Russia in 1960. After suffering a direct hit from a missile, there wasn’t much left of the U-2. However, I did notice a nameplate that said, “Lockheed Aircraft Company, Los Angeles, California.”

I asked, “Is it alright if I take this home? My mother worked at this factory during WWII building bombers.” My hosts looked horrified. “No, no, no, no. This is one of Russia’s greatest national treasures,” and they hustled me out of the building as fast as they could.

It's a good thing that I struck while the iron was hot as foreigners are no longer allowed to fly any Russian jets. And suddenly I have become very popular in Washington DC once again.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Russian Test Pilot A. Pavlov

Entries in my Logbook (Notice visit to leper colony on line 9)

U-2 Spyplane

Global Market Comments

April 8, 2022

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 29, 2022 LONDON STRATEGY LUNCHEON)

(APRIL 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (TLT), (TBT), (AAPL), (IBB), (GOOGL), (ADBE), (NVDA), (FXE), ($BTCUSD)

Below please find subscribers’ Q&A for the April 6 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: The iShares Biotechnology ETF (IBB) is down quite a bit—do I wait a bit longer to put on a debit call spread LEAPS for the end of this year and possibly the end of 2024?

A: This is really one of the two most interesting parts of the market right now. The biotech stocks have been absolutely destroyed over the past year—down 70, 80, 90% in some cases; and at that level, the worst-case scenario is in the price. Maybe we bounce along the bottom for another year. In the best case, these things all double or triple or even go up 10 times. We’re very close to putting on a 2024 call spread in the best biotech names, and if you get the Mad Hedge Biotech Letter (Click here for the link), you already know what they are because the downside risk on these things is getting close to nil, and the upside is 10 times. I like that kind of math—when the upside versus the downside is 10 to 1 in your favor. When I see specific LEAPS opportunities, I’ll send them out to you, but the answer is: not yet. We’re getting very close on biotech, however.

Q: I sold about a third of my ProShares UltraShort 20+ Year Treasury (TBT) position at $22.00 for a nice 40% gain, thank you very much. Should I hold the rest for a while? And is there a significant upside for 2022?

A: I’ve been telling everyone: hold those shorts. I know those of you who put on the December $150-$155 vertical bear put spread or the December $145-$150 vertical bear put spread already have substantial profits, but the time value on these options is still large, so there is still quite a lot of these profits to be made hanging on to all of your put spreads in the ProShares UltraShort 20+ Year Treasury Bond ETF (TLT). And is there a substantial downside from here? I think yes! If the Fed goes to a half-point rate hike schedule for the next 4 meetings, the (TLT) is absolutely going down to a $105 or $110 level or so. So, keep those shorts and add to shorts on rallies. We came close. I said sell on a $6 point rally and we got a $5 point rally. I didn't pull the trigger, and of course, now we’re here at new lows.

Q: Are we close to buying LEAPS in tech?

A: Yes, I think that once this current meltdown finishes, I want to go back in there. But I want to go long-dated.

Q: What does rapid unwind of the Fed balance sheet mean for the markets?

A: It’s terrible! The Fed has a balance sheet close to $9 trillion dollars. Before the financial crisis of ‘07, it was $800 million dollars, and in fact, in the last 4 years, it has gone up from $20 trillion to $30 trillion. So these are just bubblicious levels for the Fed to own. And what is QT or quantitative tightening? They sell those bonds. And of course, everyone knows they’re going to sell, so they’re dropping bids for bonds like crazy right now—that's why you’re getting the meltdown in the (TLT). This is bad for the stock market; there’s no world in which the stock market goes up with sharply rising interest rates. The best case is that you give up 20% and then make some of it back, and then give up 20% and then make some of it back. So yeah, expect to hear a lot about QT. We only ended QE or quantitative easing about 3 weeks ago, and it looks like we may go straight into QT as soon as May. And boy, the bond market is sure reflecting that today.

Q: How long will wage inflation last? Can I count on 10% pay increases forever?

A: No, it will last until the next recession. I have a feeling that the unemployment rate will hit all-time lows next month—probably 3.2% or 3.3%. And we’re essentially at a full employment economy right now. What happens next? Recession probably in one or two years. Then those wage hikes disappear completely, and people start getting laid off, and goodbye to inflation of all kinds since 60% or 70% of the inflation calculation is wage cost.

Q: What is a good age to retire?

A: Never. I can’t tell you how many friends I’ve had who retire and die within a year. I had one friend retire and he died the next day. What you could do is keep your old job and cut your hours by half, or you could retire from your old job to go on to a new job that you love, like opening a restaurant or a job built around your lifetime hobby, whatever that is. As long as you stay engaged, you keep Alzheimer’s at bay and you’re an active contributing person to society. As soon as you stop doing that and just start doing something like golf, your days are numbered.

Q: What factors will create a recession in 2022?

A: Well I don't think that's going to happen; that would be like multiple 1% rate rises by the Fed, and the Fed completely panicking like we said, and causing a premature recession. But I do think that by 2024 rates will be so high that we will get a recession, probably a short one, maybe 6 months. A lot also depends on the war and if Europe can replace their Russian gas/oil fast enough or they go into an oil shock and recession there.

Q: Will the Fed destroy the economy in order to save it?

A: Yes, they will, if we get inflation up into the teens, which we saw in the 1980s, they absolutely will raise rates. And then I think the 10-year made it to 12% in the early 80s when Volcker was around, and the overnight rate got to 18%. And I know that because I bought a coop in New York City with a mortgage rate of 18%. I took out one of the first floating rate mortgages and by the time I sold the house, the mortgage rate had dropped down to 11% and the value of the home had doubled.

Q: Google (GOOG), Adobe (ADBE), and Apple (AAPL) spreads are treading water.

A: That is a sign that these are the stocks that will lead the next recovery. So, only 20% down, top to bottom, in Apple while all other stocks were getting hammered for 40% or more means Apple is going to lead any recovery in the market. Watch these big tech stocks carefully—they are the new leaders, they just don’t know it yet.

Q: What will inflation do to the housing market? Should I sell or hold my investment properties?

A: Keep them. Housing is one of the biggest beneficiaries of inflation. Not only do the house prices go up, so does everything that goes into the house, like the copper, steel, lumber, kitchen appliances, etc. You really have the best play on inflation, and I don’t think interest rates will kill the housing market. I think all that will happen is people will move from 30-year fixed to 5-year adjustables, as they have done in previous high interest rate cycles.

Q: Where is the buy territory on the Mad Hedge Market Timing Index?

A: Below 20. It’s almost impossible to lose money when you buy at a market timing index of 20. You may get a day or two visit down into the teens, but if you hang on, that’ll become a big moneymaker for you. That’s been working for me for 50 years—it should work for you too.

Q: Do the chips and transports breaking down worry you about the general market?

A: No, I think they’re discounting a recession that isn’t going to happen. Remember half of all the recessions discounted in the market don’t actually happen, and I think that these are one of those non-recessionary selloffs. But it may take them a couple of months to figure out that this bull market still has a couple of years of life to it and that it’s too early to sell. By the way, once people realize that they discounted the recession too early, what are they going to pour back into the fastest? The semiconductor stocks. That's why I’ve got a laser focus on NVIDIA (NVDA).

Q: If there is no recession coming, are the retailers getting too oversold?

A: Yes, but in the world that’s out there, where you really only want to own two or three of the best sectors and avoid the other 97, retailers are the ones you want to avoid—unless there's some specific single company story that you know about.

Q: Housing prices can’t fall when there's such enormous demand coming from millennials, right?

A: That’s true. In fact, the number of houses that need to be built to meet this demand is anywhere from one to five million, so this is a shortfall that will take at least a decade to address, and house prices don’t fall in that situation. They may appreciate at a slower rate, but they will appreciate, nonetheless.

Q: Is there any level where you would consider a call spread in the TLT?

A: Well, I had the April $127-$130 vertical bull call spread and I had my head handed to me. So somewhere, but clearly not yet—again, it depends a lot on what the Fed does and how fast.

Q: What’s the outlook for the Euro (FXE), (NVDA)?

A: Lower. Until the Ukraine War ends, they get an economic recovery, and they wean themselves off of Russian energy and move over to American energy. And that's at least a year down the road, so I’m not rushing into any European investment—stocks, bonds, or currencies.

Q: Are rising interest rates good for banks?

A: Yes, but right now those benefits are being offset by recession fears which will probably go away in a couple of months. So that kind of makes banks a strong buy right here.

Q: When the Shanghai lockdown ends, will it create another surge in commodity prices?

A: Absolutely, yes. China is the world's largest consumer of commodities, and the restoration of any of their purchasing power will certainly be great for all commodity prices—food, energy, metals, you name it.

Q: Is Tesla (TSLA) a LEAPS candidate?

A: Yes but wait for it to take a run at the $700 low that we saw last month. We probably won’t get there, but $800 this time around is probably a great LEAPS candidate for Tesla going forward. I expect them to meet all of their goals for production this year.

Q: Won’t Bitcoin ($BTCUSD) keep falling if equity markets are lower?

A: Yes, but we don’t have that much lower to go in equity markets—maybe 10%. So just as we’re looking to buy equities and the smaller technology stocks on dips, we're also looking to buy Bitcoin on dips. If we can get back into the $30,000 handle, that might be a ripe buy territory for all the cryptocurrency plays.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 4, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE ROUND TRIP MARKET)

(SPY), (TLT), (VIX)

If you had followed my advice and taken a cruise around the world in December, you would be getting home about now. A review of your portfolio would review that most of your positions were either unchanged or down slightly.

And if you had chunky positions in bond shorts, as I pleaded, begged, and cajoled you into taking on, you would be sitting pretty. In fact, you could well afford to take yet another cruise around the world.

That could be the best advice I can give right now, for the next quarter, the market will remain trapped in a wide but volatile range. That’s fine if you are backed up with mainframe computers, a programming staff of a dozen strong, and dedicated lightning-fast fiber optic cables, all the resources of a high-frequency trader shooting for pennies per trade.

If instead, you’re trading on your iPhone in between meetings at work, on every other hole at the golf course, or whenever you have free time, as many of you do, you may well want to sit Q2 out. There are not any great trades out there at the moment, the market is still expensive and the challenges ahead are legion.

For a start, stocks are in the process of discounting one of those annoying recessions that aren’t going to happen, as it does about half the time. I know this is important for many of you who run their own businesses remorselessly tied to the economic cycle.

Yes, I know that there is a rising tide of recession calls from the analyst community. But the models that reliably worked in the past are missing two crucial factors.

They never had to account for Medusa’s head of supply chain problems we now face, where perhaps 5% of US GDP is tied up on the West coast docks stacked in containers ten high. Untie this Gordian knot and you get another surprise spurt for the economy.

The other is the coming reconstruction of Ukraine, one of the greatest public works projects of all time, on a scale with the WWII Marshall Plan. Every major engineering company in the world will have to get involved, including Fluor (FLR), Bechtel (private), and those in Europe, Japan, and China. I reckon it could add 1% of global growth per year for the next several years.

How are the impoverished Ukrainians going to pay for all this work? With the $1 trillion in overseas Russian assets already seized, Ukraine easily gets control through proceedings at the World Court.

All Putin really accomplished with his war was to bring forward the end of oil by 20 years, at least for Russia, and to shrink the Russian standard of living by 90% practically overnight. It has been duly kicked out of the global economy. A million Russians have already lost their jobs and the shelves in Moscow are empty.

By the way, you may have noticed that Apple was up every day for 11 days for the first time since 2003. All the war really meant is that you got to buy Apple for a few minutes at $150 instead of $160. This is not what coming recessions are made of. The Volatility Index (VIX) at $19 is screaming as much.

It all confirms my 2022 scenario of a rambunctious H1 followed an H2 zeroing in on new all-time highs. You heard it here first!

Now for last week’s highlights:

Unemployment Plunges to 3.6%, a new cycle low, with the hot 431,000 March nonfarm Payroll. It’s yet another reason for the Fed to raise interest rates and increases the prospects of a 50-basis point rise this month. Leisure and Hospitality gained an eye-popping 118,000, Professional & Business Services 102,000, and Manufacturing 38,000. The U-6 “discouraged worker rate” fell to an incredible 6.9%. The back months saw big upward revisions. Overall, it was a blowout report.

ADP up 455,000 in March, showing the jobs market is still on fire. Services are seeing huge gains. Leisure & Hospitality continues its post covid bounce back. It makes the coming Nonfarm Payroll report on Friday look pretty industry.

JOLTS Comes in Red Hot, showing that there were 11.3 million job openings in February, 5 million more than the number of unemployed. The great labor shortage continues and may be permanent, dashing all recession fears.

Will the Fed Screw Up? That is the biggest risk to the markets according to 46% of all investors. Rising inflation comes in at 33%. If the Fed panics and excessively raises interest rates in a tardy response to higher prices the 46% will be right.

The Five- and 30-Year Bonds Invert, meaning it is cheaper to borrow for 30 years than it is for five. Such a move usually presages a recession. Other than that, Mrs. Lincoln, how was the play?

Oil Plunges 8% on China Lockdown Fears, to $104.50 a barrel, as a new Covid wave hits Shanghai. China is the world's largest importer of oil by a large margin.

Tesla to Split Shares and Pay Dividend, according to SEC filings, sending the shares soaring by $90. (TSLA) has more than doubled since the last split in August 2020. Buy (TSLA) on dips.

S&P Case Shiller Up 19.2% in January, yet another new all-time high. Phoenix (33%), Tampa (31%), and Miami (28%) were the big winners and January is when mortgage interest rates started to rise sharply. This has led to an increase in all cash offers and buyers no longer qualify for loans. Home prices should keep rising for the rest of the decade, although at a slower rate.

Biden to Boost Battery Metal Production, by invoking the Defense Production Act, to hasten the end of our reliance on oil. Permitting and environmental regulation will get eased for the miners of lithium, cobalt, and nickel. The government has figured out that there are nowhere near the materials needed to meet the lofty sales forecasts of EV makers, like Tesla.

The Energy Sector Has Hit a Gusher in Profits, with earnings up an eye-popping 228% YOY. But if you are not in already, you missed it. Topping out risk is beginning, especially if the Ukraine War ends, cratering oil prices.

Biden to release 1 Million Barrels a Day for the SPR, the most in the 47-year history of the facilities, putting a serious dent in the current energy shortage. That’s against daily US consumption of 20 million barrels. The Strategic Petroleum Reserve currently has 714 barrels. It should be emptied and shut down as it is nothing more than a government subsidy for three two red states, Texas and Louisiana. Russia says it will only take rubles for oil and gas sales from Friday.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With near-record volatility, my March month-to-date performance retreated to a still blistering 12.26%. My 2022 year-to-date performance ended at a chest beating 26.85%. The Dow Average is down -4.00% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding more long positions in technology.

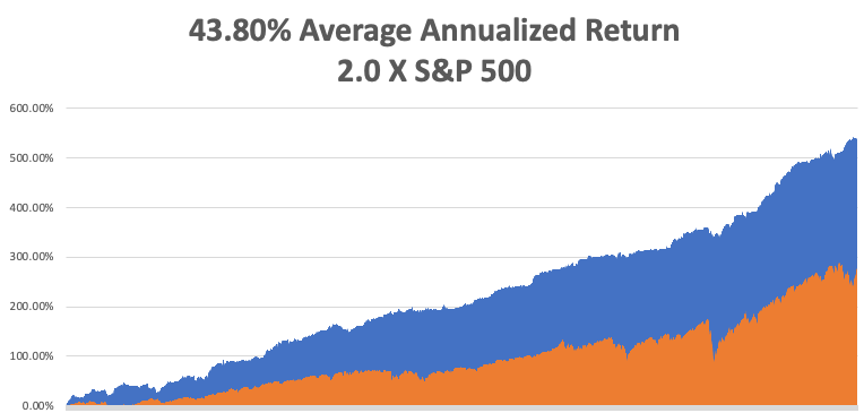

That brings my 13-year total return to 539.41%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 43.80%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.2 million and rising quickly and deaths topping 983,000 and have only increased by 1,000 in the past week. You can find the data here. The growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 4 at 7:00 AM EST, US Factory Orders for February are published.

On Tuesday, April 5 at 9:00 AM, the ISM Non-Manufacturing Index for February is printed.

On Wednesday, April 6 at 11:00 AM, The minutes from the last Fed meeting are released and will almost certainly lean hawkish.

On Thursday, April 7 at 7:30 AM, the Weekly Jobless Claims are printed.

On Friday, April 8 at 8:30 AM, Wholesale Inventories for February are announced. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I backpacked around Europe in 1968, I relied heavily on Arthur Frommer’s legendary paperback guide, Europe on $5 a Day, which then boasted a cult-like following among impoverished, but adventurous Americans. The charter airline business was then-booming, and suddenly Europe came within reach for ordinary Americans like me.

Over the following years, he directed me down cobblestoned alleyways, dubious foreign neighborhoods, and sometimes converted WWII air raid shelters, to find those incredible travel deals. When he passed through town some 50 years later, I jumped at the chance to chat with the ever cheerful worshipped travel guru.

Frommer believes there are three sea change trends going on in the travel industry today. Business is moving away from the big three travel websites, Travelocity, Orbitz, and Priceline, who have more preferential lucrative but self-enriching side deals with airlines than can be counted, towards pure aggregator sites that almost always offer cheaper fares, like Kayak.com, Sidestep.com, and Fairchase.com.

There is a move away from traditional 48-person escorted bus tours towards small group adventures, like those offered by Gap Adventures, Intrepid Tours, and Adventure Center, that take parties of 12 or less on culturally eye-opening public transportation.

There has also been a huge surge in programs offered by universities that turn travelers into students for a week to study the liberal arts at Oxford, Cambridge, and UC Berkeley. His favorite was the Great Books programs offered by St. John’s University in Santa Fe, New Mexico.

Frommer says that the Internet has given a huge boost to international travel, but warns against user-generated content, 70% of which is bogus, posted by hotels and restaurants touting themselves.

The 81-year-old Frommer turned an army posting in Berlin in 1952 into a travel empire that publishes 340 books a year or one out of every four travel books on the market. I met him on a swing through the San Francisco Bay Area (his ticket from New York was only $150), and he graciously signed my tattered, dog-eared original 1968 copy of his opus, which I still have.

Which country has changed the most in his 60 years of travel writing? France, where the citizenry has become noticeably more civil since losing WWII. Bali is the only place where you can still actually travel for $5/day, although you can see Honduras for $10/day. Always looking for a deal, Arthur’s next trip is to Chile, the only country in the world he has never visited.

Arthur’s Next Big Play is Bali

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 28, 2022

Fiat Lux

(SPECIAL WARTIME ISSUE)

Featured Trade:

(TESTIMONIAL),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE UNBELIEVABLE MARKET),

(SPY), (TLT), (TBT), (TSLA), (NVDA)

Listening to the market commentary this week, the word “unbelievable” kept popping up.

It was “unbelievable” that the market crashed by 15% when Russia invaded Ukraine. It was equally “unbelievable” that it then melted up 7% over five trading days.

So has the market gone from discounting the outbreak of WWIII and complete Armageddon to a total victory by Ukraine, the resurgence of NATO, and the end of Russia….in a week?

Well, maybe they have done just that.

The only thing we can count on for sure is that volatility will continue for the indefinite future. The only certainty we have is that change will continue, and it is accelerating at a phenomenal rate.

Of course, it’s all amazing to me. I am a creature of the American 1950s who is now living 70 years in the future. Yes, even the Jetson-type flying cars have happened.

Let me update you on the war, since I know you’re all dying to know.

The Ukraine is winning. What once appeared to be a small, defenseless nation had in fact been preparing for a prolonged guerilla war for seven years, ever since Crimea was invaded.

Javelin and stinger missiles were stockpiled at every key intersection in the country. And the California National Guard has been training the army on how to use them for the last seven years. It was all a gigantic ambush in the making.

The Russian Army, which has seen no real combat experience for 30 years, believed their own propaganda and literally expected to be showered with roses on day one. As a result, they ran out of gasoline, food, and ammunition, and now precision weapons. Some 10% of the army has been killed and maybe 20% of their Air Force shot down. The war is essentially over, so Putin is desperately seeking a way to call it a victory and get out.

Putin himself is toast. At this point, he is the richest man in the world who can’t spend a single ruble of his money. What wealth he had overseas has been seized and will be used to finance the reconstruction of Ukraine. Putin can never leave Russia again without being arrested as a war criminal. But if he stays, he runs the constant risk of assassination. The guy has made a lot of enemies.

What about Putin’s nukes you may ask? Of the headline 7,000 such weapons mentioned in the SALT treaties, only 200 actually work. The rest are corroding empty shells. The math is very simple. Russia’s $1 trillion GDP can’t support any more of these wildly expensive weapons. By the way, China has the same number.

The logic of MAD (Mutually Assured Destruction) still applies, making nuclear weapons useless. If Putin fires off one nuke, his entire country vaporizes in 30 minutes. His generals know this. If ordered to use nukes, they would either ignore the order or depose him immediately.

As someone who has spent the last half-century contemplating the future of the universe, the consequences of this are absolutely mind-boggling.

Economic warfare has finally come into its own as a weapon more destructive than nuclear weapons. In a year, per capita income in Russia will have plunged from last year’s $10,000 to the Soviet-era $1,000. In weeks, Putin has written off 30 years of economic growth. A second Russian Revolution is a sure thing, but what form it will take should be interesting.

How did such a clever man as Putin end up in such a predicament? He surrounded himself with advisors who told him only what he wanted to hear. Such is the way of dictators who have been in power too long. A recent US president had the same problem, with similar results.

The US is the huge winner in all this. Biden announced on Friday that America will replace the missing Russian oil and gas, some 10% of the total world supply. This has already started a renaissance of the US energy industry, which only two years ago was on its heels and destinated to become the next buggy whip industry.

As I have been pointing out to the Joint Chiefs since all this started, strong support for Ukraine not only eliminates Russia as a threat, it puts the shackles on China with its own expansionist desires. You haven’t heard much about Taiwan lately. For America, it’s a twofer.

To say all of this is wildly positive for American stock markets is an understatement. It certainly keeps my $240,000 forecast for the Dow by 2030 on the table. How long it will take investors to figure all this out is anyone’s guess. But I think we are setting up for one hell of a second half.

You see all this in the behavior of a single stock. After NVIDIA (NVDA), the best stock in the world, plunged 40% on fears of deglobalization, it rocketed by 47% in the past week, suggesting that deglobalization is coming back stronger than ever. It reiterates my argument that you use this correction to pick up the Cadillacs at a discount, not Volkswagens.

Bonds Crashed, on comments from Fed governor Jay Powell that if he has to raise interest rates by 50 basis points next month, he will. It’s nothing new but it certainly set the cat among the pigeons with bond longs. The (TLT) broke $130, triggering a round of stop losses before it bounced back. The double short (TBT) popped to $21.33. The good news is that this is more than covered by the seven other bond trades we have closed in 2022 that made money. Those who have bond put LEAPS, which is almost all of you, are making a fortune. It looks like my yearend target of a $2.50% ten-year yield may be hit imminently. Keep selling rallies in the (TLT).

Will the Fed Raise Interest Rates by a Full 1% in April? Our central banks could make such a move at their April 28 confab as they are so far behind the curve, especially if inflation data continues hot. Such a move, or the fear of us, might give us a second shot at a double bottom in stocks at the (SPY) $410 level. Such a move would make your sizeable bond shorts look pretty good.

Recession is Unavoidable Without Russian Oil, says the Dallas Fed. There isn’t enough time to bring alternatives on to the market. The scenario is similar to the invasion of Kuwait in 1991 when we lost 1.5 million barrels a day overnight. This time, it’s 9 million b/d. It all augers for higher oil prices and slower economic growth….unless you drive a Tesla!

Weekly Jobless Claims Lowest Since 1969 at 187,000, down an eye-popping 28,000 on the week. No problems with the economy here. The drop in claims is consistent with a labor market in which employers are desperately trying to hang onto workers and attract new ones.

Berkshire Hathaway Buys Alleghany Insurance for $11.6 billion, taking (BRKB) to yet another new all-time high. Warren Buffet definitely loves the insurance industry, which he uses as a cash cow to fund all his other investments. Alleghany Insurance is in effect a mini-Berkshire, starting out in railroads and evolving into a general investment holding company. Keep buying (BRKB) on dips, a long time Mad Hedge favorite

Tesla Delivers First German Made Model Y, which will enable the company to reach its 1.5 million vehicle target for 2022, up 50%. With an energy crisis in Europe, Tesla will sell these as fast as they can make them. There is currently a one-year wait to get a Model X in the US, and I can sell mine for more than I paid for it three years ago.

Jeffries Raises Tesla Target from $1,250 to $1,400. It cites a dramatically changed geopolitical environment which sent oil prices through the roof, greatly benefiting all makers of electric vehicles, of which Tesla is far and away the largest. The company is firing on all cylinders, which it actually doesn’t make. Maybe in five years, they will get to my own $10,000 target for Tesla. Buy (TSLA) on dips.

Alibaba Announces Monster Share $25 billion Buy Back, taking the shares up 11%. Could this spell the end of the Chinese stock market crash, with many companies down 80%-90%?

New Home Sales Dive, down 2% to 772,000 in February. Inventories are still very light at 6 months compared to a scant 2-month supply for existing homes. Interest rates are starting to bite, and prices are still soaring, taking the median national price to a new high of $406,600, up 10.6% YOY.

The US to Replace Russian Gas for Germany, some two-thirds by year-end and completely by 2027. It is already on track to supply a record 22 billion cubic feet last year and 50 billion cubic feet by 2030. But the US is at maximum capacity and only major investments will increase supply. More specialized LNG carriers will need to be built and Golar LNG (GLNG) and Flex LTD (FLEX) are the plays there. Buy Chenier Energy (LNG), Tellurian Inc. (TELL), and Sempra (SRE) on dips.

Pending Homes Sales Sink, down 4.1% in February, the fourth straight month of declines. The share of disposable income taken by monthly mortgage payments rose by an incredible 8.3% last month, shutting out buyers. It explains why homebuilder stocks like Lennar (LEN) and KB (KBH) are getting slaughtered.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

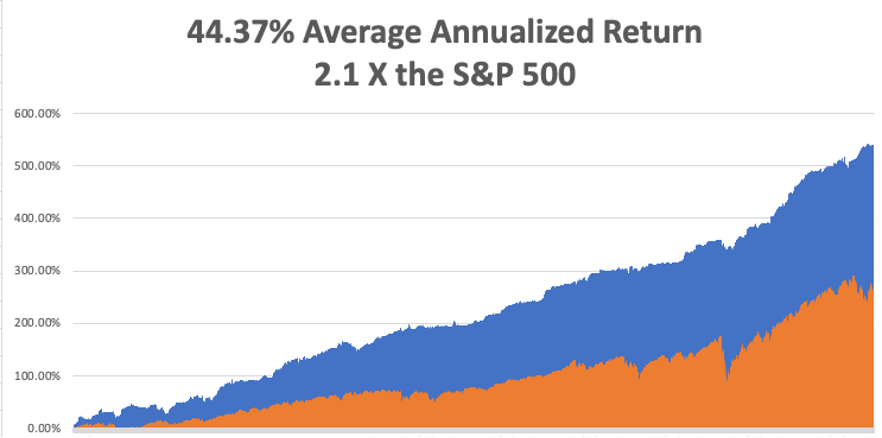

With near-record volatility, my March month-to-date performance retreated to a still blistering 12.60%. My 2022 year-to-date performance ended at a chest-beating 27.19%. The Dow Average is down -4.00% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding more long positions in technology.

That brings my 13-year total return to 539.75%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80 million and rising quickly and deaths topping 976,000 and have only increased by 7,000 in the past week. You can find the data here. Growth of the pandemic has virtually stopped, with new cases down 96% in a month.

On Monday, March 28 at 7:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, March 29 at 9:00 AM, The S&P Case Shiller National Home Price Index is published.

On Wednesday, March 30 at 8:15 AM, the ADP Private Employment Data is out.

On Thursday, March 31 at 7:30 AM, the Weekly Jobless Claims are printed.

On Friday, April 1 at 8:30 AM, the March Nonfarm Payroll Report is announced. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, I received calls from six readers last week saying I remind them of Ernest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens, I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete works.

I visited his homes in Key West and Ketchum, Idaho. His Cuban residence is high on my list now that Castro is gone.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Ernest shot a German colonel in the face at point blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was still being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are now glued to the tables.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 21, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or FROM QE TO QT),

(SPY), (TLT), (TBT), (TSLA)

A client asked me today if, after the 5th worst start to a year since 1927, I thought the stock market had bottomed.

My response? One interest rate rise down, 12 to go, or 3.00% if we stick to the quarter-point pace.

And while the first seven rate rises have already been discounted by the futures market, the additional six we will get in 2023 haven’t.

We have just seen the best week for stocks in nearly two years, but don’t get your hopes up. We are in the process of weaning the markets off of 12 years of free money and we aren’t going to get away with a measly 15% correction.

And when I say markets, I don’t just mean stocks, but for bonds, commodities, foreign exchange, precious metals, energy, and real estate as well. No asset has actually had a real price for more than a decade.

So, how does all this end? You can count on several tradable rallies for the rest of the year, like the one we have just had. Big tech earnings are still racing ahead like a bat out of hell. By yearend, tech should be stupid cheap, cheap enough to take the indexes to new highs, even if they are marginal ones at best.

Eventually, the Fed will take rates high enough to assure a recession. That happens when yield curves are completely flat, i.e, when the two, ten, and 30-year yields are the same, which is about two years off.

That could happen sooner if inflation fails to abate and the Fed has to resort to successive half-point hikes to cool a superheated economy. Currently, Jay Powell doesn’t believe that will be necessary because he expects the inflation rate to drop to 4% by the end of 2022 as wage demands fade, supply chain problems sort themselves out, and the Ukraine war stalemates.

News flash: Fed governors have been known to be wrong.

Here’s an interesting tidbit. I renewed my pilot’s medical this week in case I get a midnight call from Washington DC. Don’t worry, I passed with flying colors, thanks to all my nighttime backpacking.

But you know what the flight surgeon told me? Every medical he had done in the last two weeks was for someone headed to Ukraine.

This could be a really interesting war.

The Fed Raises Interest Rates by a quarter point. The futures markets are already discounting seven rate hikes this year, but not the six in 2023. The Fed is so far behind the curve they may have to resort to half-point rises later this year if inflation doesn’t fade. According to that timetable, the yield curve will be completely flat by then, triggering the next recession.

China Crashes, on fears they may get dragged into the Ukraine war by Russia. Delisting threats from the SEC, a slowing economy, flight from growth tech stocks, and a new Covid outbreak aren’t helping either. Some $2.1 trillion in market cap has been lost since these stocks looked so great a year ago. Not a great place to be when a new iron curtain is descending. Right now, the US is the only safe place to be.

Bonds Collapse on happy talks about Russia/Ukraine talks, making my shorts look even better. Ten-year US Treasury yields hit a three-year high at 2.08% yield. It’s a resumption of a steep downtrend in bond prices that started in November. I used the war-induced rally to ramp up positions. But I don’t think we break $130 in the (TLT) for at least another month. Keep selling big rallies in the (TLT).

The Producer Price Index is Up a Hot 10% YOY, and 0.8% in February, largely driven by soaring energy prices. Food prices are up as Ukraine’s wheat, one-third of the world supply, disappears from the marketplace. It makes the Fed rate hike a sure thing.

Russia has $350 Billion of US stock for Sale at Market. That is the amount Russian oligarchs are thought to own in US hedge funds which the Justice Department is in the process of seizing. It’s part of $1 trillion in foreign assets overall, which include the Chelsea soccer team, several tens of billion worth of US real estate, and a $200 billion stake in Uber.

China has to Choose, whether to have Russia or the US as an ally. Will it be the sanctioned $1 trillion economy in free fall, or a booming $25 trillion economy? Certain the costs of going against the US have been made clear. I’ve been arguing vociferously to the Joint Chiefs from the beginning that standing up to Putin gets you a two for: it forces China to back off from aggressive moves towards Taiwan as well. Russia can stand sanction. Chinese would starve, as the bulk of its wealth over the last 30 years came from trade with the US.

Existing Home Sales Plunge by 7.2% to 6.02 million units in February. Soaring mortgage rates and rock bottom inventories are taking their toll. Many homes are gone only a week after listing.

Nickel Futures are Limit Down in London, off by 12%, indicating that the super spike in commodities prices triggered by the Ukraine war may be over. The price fell by $36,915 per metric tonne, well off the $100,000 high from weeks ago when Chinese speculators covered shorts generating massive losses.

Weekly Jobless Claims Come in at 214,000, a two-month low. The economy is recovering slowly and is on the verge of full employment.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With near record volatility, my March month to date performance catapulted to a blistering 15.23%. My 2022 year-to-date performance ended at a chest beating 29.82%. The Dow Average is down -4.3% so far in 2022. It is the great outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

My five March positions expired at their maximum potential profit with the options expiration on Friday. That leaves me 90% in cash and 10% in a single long bond position which is close to breaking even. Only the next capitulation selloff day I’ll be adding more long positions in technology.

That brings my 13-year total return to 542.38%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.88%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80 million and rising quickly and deaths topping 971,000, which you can find here. Growth of the pandemic has virtually stopped, with new cases down 96% in a month.

On Monday, March 21 at 7:30 AM EST, the Chicago Fed National Activity Index is out.

On Tuesday, March 22 at 12:30 PM, API Crude Oil Stocks are released.

On Wednesday, March 23 at 10:00 AM, New Home Sales for February are printed.

On Thursday, March 23 at 7:30 AM, Durable Goods Orders for February are published. Weekly Jobless Claims are out at 8:30.

On Friday, March 25 at 9:00 AM, Pending Home Sales for February are disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great grandmother lived during the waning days of WWII. Little did I know that Palermo had the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot of the Alitalia jet say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 tourists. Two days later the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York City.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I has continued my flight, the rag would have settled over my fuel intake valve, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed his Lockheed P-38 Lightning in 1944.

In the end, The crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note