Global Market Comments

February 2, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOLD, SILVER, AND BITCOIN CRASH!)

(GLD), (SLV), (B), (NEM), (GDX), (T), (VZ), (XLP), (GME), (PLTR), (XOM), (IWM), (AAPL), (AMZN), (MSFT)

Global Market Comments

February 2, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOLD, SILVER, AND BITCOIN CRASH!)

(GLD), (SLV), (B), (NEM), (GDX), (T), (VZ), (XLP), (GME), (PLTR), (XOM), (IWM), (AAPL), (AMZN), (MSFT)

Global Market Comments

October 25, 2024

Fiat Lux

Featured Trade:

(OCTOBER 23 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (JNK), (CCJ), (VST), (BRK/B), (AGQ), (FCX), (TM), (BLK), (NVDA), (TSLA), (T), (SLV), (GLD), (MO), (PM)

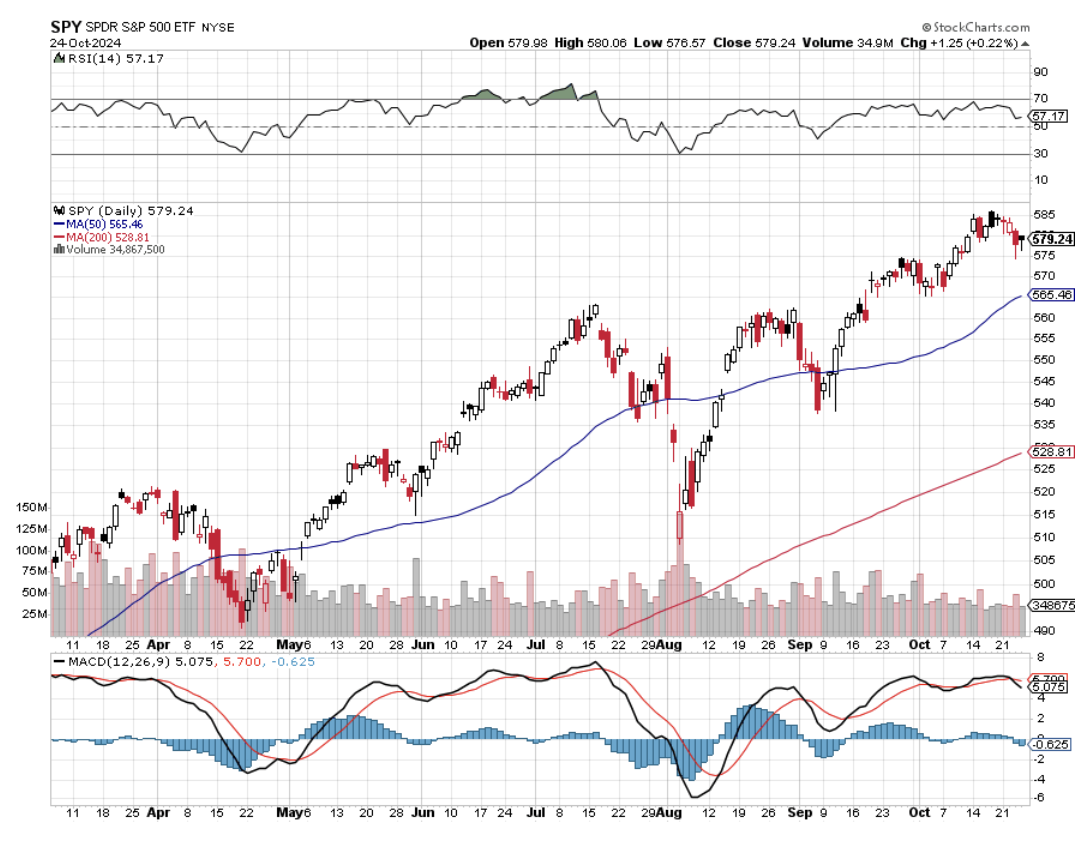

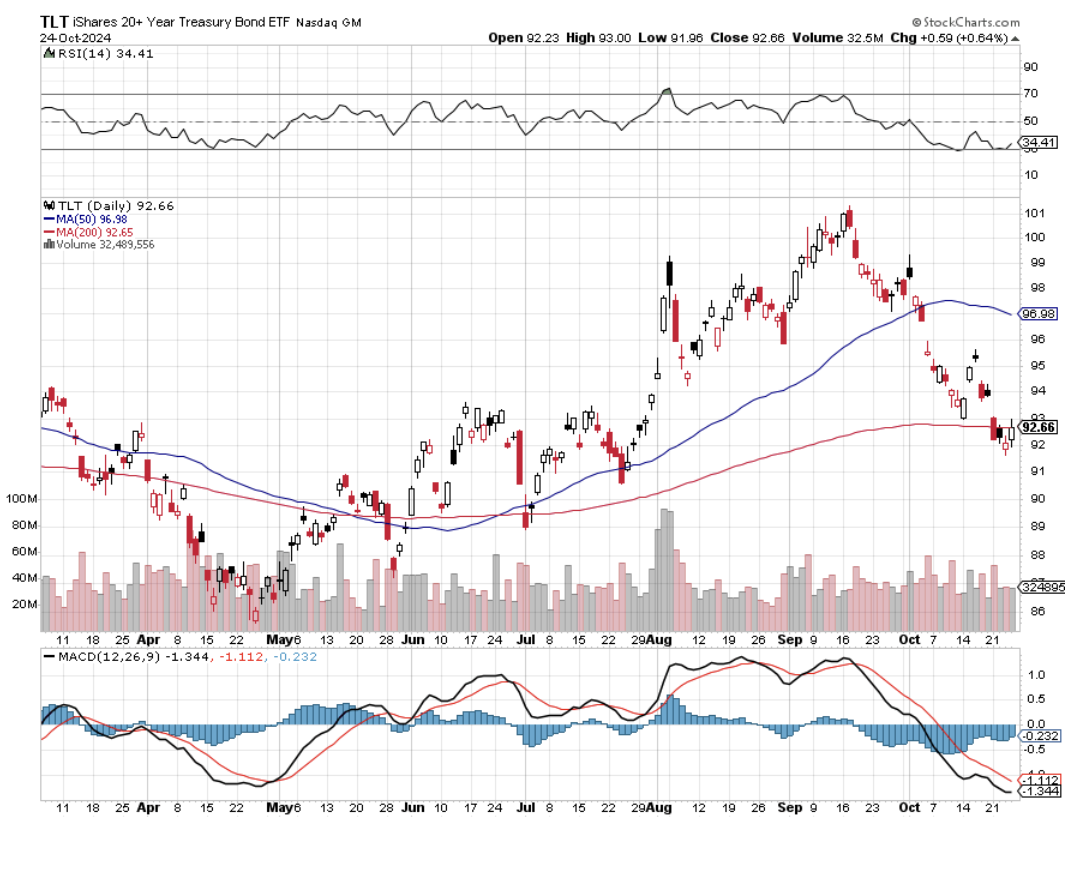

Below, please find subscribers’ Q&A for the October 23 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

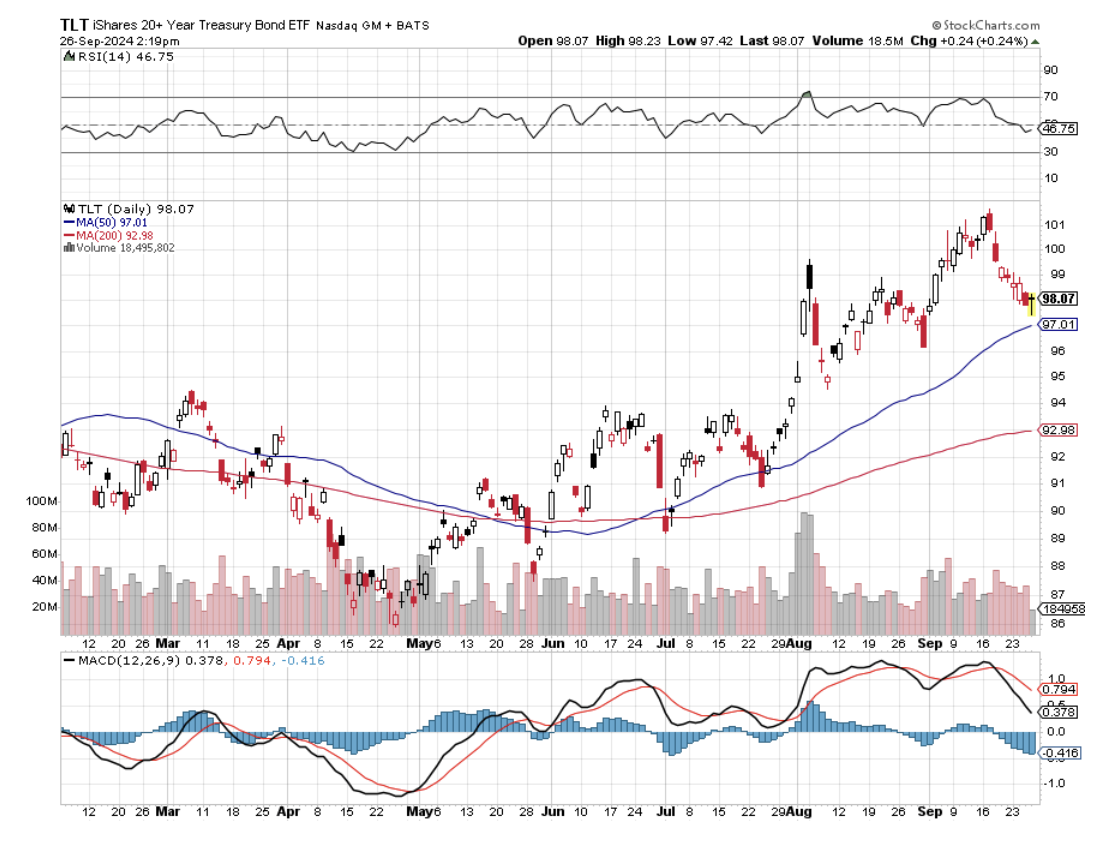

Q: What the heck is happening with the iShares 20+ Year Treasury Bond ETF (TLT)? It keeps dropping even though interest rates are dropping. It seems to be an anomaly.

A: It is. What’s happening is that bonds are discounting a Trump win, and Trump has promised economic policies that will increase the national debt by anywhere from $10 to $15 trillion. Bonds don’t like that—you borrow more money through bonds, and the price goes up. Interest rates could go as high as 10% if we run deficits that high (at least the bond market may go that low.) On the other hand, stocks are discounting a Harris win. Stocks went up 60% over the last four years. I did roughly double that. And a Harris win would mean basically four more years of the same. So stocks have been trading at new all-time highs almost every day until this week when the election got so close that the cautious money is running to the sidelines. So what happens if there's a Harris win? Bonds make back the entire 10 points they lost since the Fed cut interest rates. And what happens if Trump wins? Bonds lose another 10 points on top of the 10 points they've already lost. Someone with a proven history of default doesn't exactly inspire confidence in the bond market. So that is what's going on in the bond market.

Q: Will the US dollar continue its run into year-end?

A: No, I have a feeling it’s going to completely reverse in two weeks and, give up all of its gains, and resume a decade-long trend to new lows. So, I think everything reverses after election day. Stocks, bonds, commodities, precious metals—the only thing that doesn't is energy, and that keeps going down because of global oversupply that even a Middle Eastern war can’t support.

Q: Are you expecting a major correction in 2025?

A: I am, actually. We basically postponed all corrections into 2025 and pulled forward all performance in 2024. So, I think we could get at least a 10% correction sometime next year, and that is normal. Usually, we get a couple of them. This year, we only got the one in July/August. So, back to normal next year, which means smaller returns from the stock market. In fact, smaller returns from everything except maybe gold and silver. This is why they're going up so much now.

Q: Are you discounting a huge increase in the deficit under Biden-Harris?

A: No, the huge increase in the deficit is behind us because we had all the pandemic programs to pay for, and if anything, technology inflation should go down because of accelerating technology. We're already seeing that in many industries now, so I don't think there'll be any policy changes under Harris, except for little tweaks here and there. All the big policies will remain the same.

Q: What is a dip?

A: A dip is different for every stock and every asset class. It depends on the recent volatility of the underlying instrument. You know, a dip in something like McDonald's (MCD) or Berkshire Hathaway (BRK/B) might be 5%, and a dip in Nvidia (NVDA) might be 15 or 20%. So, it really depends on the volatility of the underlying stock, and no two volatilities are alike.

Q: What are your top picks on nuclear?

A: Well, we've been in Cameco (CCJ), the Canadian uranium company, since the beginning of the year, and it has doubled. Vistra Corp (VST) is another one, and there are many more names after that.

Q: What are your thoughts on Toyota (TM)?

A: I love Toyota for the long term. The fact that they were late into EVs is now a positive since the EV business is losing money like crazy. They're the ones who really pioneered the hybrid business, and I’ve toured many of their factories in Japan over the years. Great company, but right now, they're being held back by the slow growth of the Japanese economy.

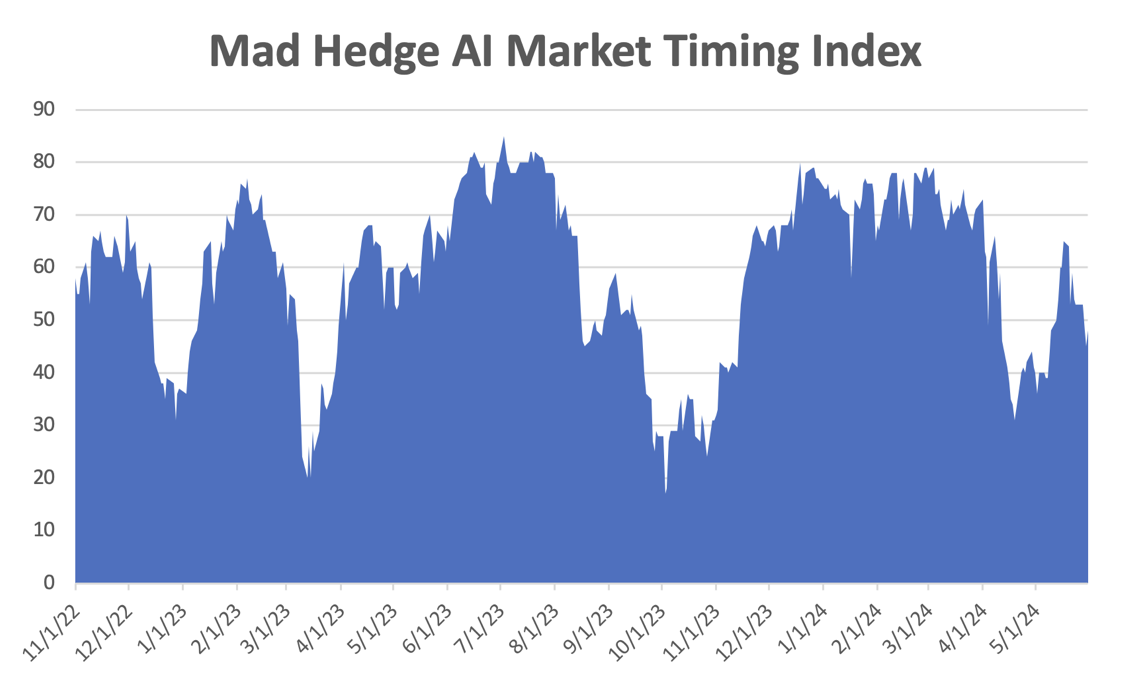

Q: Market timing index says get out. We're heading into the seasonally bullish time of the year. Should we be in or out over the next two months?

A: I would be in as long as you can handle some volatility around the stock market. When the market timing index is at 70, that means any new trades that you initiate have a 30% chance of making money. Now, they can sit at highs sometimes for months, and it actually did that earlier this year. Markets can get overbought and stay overbought for months, and that is a really difficult time to trade. If you're a long-term investor, you just ignore all of this and just stay in all the time.

Q: Silver has broken out; what's next?

A: Silver had had a massive run since the beginning of September—some 30%. We're up to about $31/oz. The obvious target for silver is the last all-time high, which I think we did 40 years ago, and that was at $50/oz. So there's another easy 60% of upside in silver. That's why I put out a LEAPS on the 2x long silver play (AGQ), and people are already making tons of money on that one. I think Silver will be your big performer going forward.

Q: Too late to invest in Chinese stocks?

A: No, it's selling off again. IT Could retest the lows, especially if the government sits on its hands for too long with more stimulus packages.

Q: Is big tech still a good bargain buy?

A: I would take “bargain” out of that. The rule on tech investing is you're always buying expensive stuff because the future always has a spectacular outlook. So, tech investing is all about buying something expensive that gets more expensive. This is exactly what tech stocks have been doing for the last 50 years, so it's not exactly a new concept. I know tons of people who never touched Nvidia (NVDA) or Tesla (TSLA) because it was too expensive. (NVDA) was too expensive when it was $2, and now it's even more expensive at $140 or, in Tesla's case, $260.

Q: Will Tesla (TSLA) go up or down tonight?

A: I have no idea. Anybody else who says they have an idea is lying. You go to timeframes that short, and you are subjecting yourself to random chance; even the weather could affect your position by tomorrow.

Q: How uncomfortable is the stem cell extraction?

A: Extremely uncomfortable. If they say it won't hurt a bit, don't believe them for a second. They take this giant needle hammer it into your backbone to get your spinal fluid (and I count the hammer blows.) Last time, I think I got up to 50 before I couldn't take the pain anymore, and they extracted the spinal fluid to get the stem cells. So, for those who don't tolerate pain very well, this is absolutely not for you.

Q: Why is Intel (INTC) stock doing so badly this year?

A: Low-end products, no new products, poor manager. Whenever a salesman takes over a technology company, you want to run a mile. That's what happened at Intel because they have no idea how the technology works.

Q: Should I sell my Philip Morris (PM) stock? It's just had a huge run-up.

A: No. For dividend holders, this is the dream come true. They pay a 4.1% dividend. This was a pure dividend play ever since the tobacco settlement was done 40 years ago. Then they bought a Swedish company that has these things called tobacco pouches, and that has been a runaway bestseller. So, all of a sudden, the earnings at Philip Morris are exploding. The dividend is safe. I think Philip could go a lot higher, so buy PM on dips. And I will dig into this story and try to get some more information out of it. I love high growth high dividend plays.

Q: What's the best play for silver?

A: I'm doing the ProShares Ultra Silver (AGQ), which is a 2x long silver and has gone from $30 to $50 since the beginning of September. If you want to sleep at night (of course, I don't need to), then you just buy the iShares Silver Trust (SLV), which is a 1x long silver play and that owns physical silver. I think it's held in a bank vault in London.

Q: Time to sell Copper (FCX)?

A: Short term, yes, as China weakens. Long-term, hang on because we are coming into a global copper shortage, and that'll take the price of copper up to $100 or (FCX) up to $100. So yes, love (FCX) for the long term. Short term, it has a China drag.

Q: Will inflation come back in 2025?

A: No, it won't. Technology is accelerating so fast, and AI is accelerating so fast it's going to cut costs at a tremendous rate. And that's why you're seeing these big tech companies laying off people hundreds at a time; it's because the low-end jobs have already been replaced by AI. There is a lot more of that to come. I'm not worried about inflation at all.

Q: Do you disagree with Tudor Jones on inflation?

A: Yes, I disagree with him heartily. Tudor Jones is talking his own book, which means he doesn't want to get a tax increase with a Harris administration. So he's doing everything he can to talk up Trump, and that isn't helping me with my investment strategy whatsoever. By the way, Tudor Jones is often wrong, you know; he made most of his money 30 years ago. And before that, it was when he was working for George Soros. So, yes, I agree with the man from Memphis. He’s in the asset protection business. You’re in the wealth creation business, a completely different kettle of fish.

Q: Do you hold the ProShares Ultra Silver (AGQ) overnight?

A: I've been holding my (AG for four months, and the cost of carry-on that is actually quite low because silver doesn't pay any dividend or interest. There really isn't much of a contango in the precious metals anyway—it's not like oil or natural gas. It’s a 3X plays that you really shouldn’t hold overnight.

Q: Where is biotech headed?

A: Up for the long term, sideways for the short term. That's because, after the election, risk on will go crazy. We could have a melt-up in stocks, and when that happens, people don't want to buy “flight to safety” sectors like Biotechs and healthcare; they want to buy more Nvidia. Basically, that's what happens. More Nvidia (NVDA), more Meta (META), and more Apple (APPL). They want to buy all the Mag7 winners. Well, let's call them the Mag7 survivors, which are still going up after a ballistic year.

Q: Any suggestions on where to park cash for five to six years?

A: 90-day T-Bills are yielding 4.75%. That would be a safe place to put it. And you might even peel off a little bit of that—maybe 10% — and put that into a junk fund, which is yielding 6%. You're still getting a lot of money for cash—but not for much longer. The golden age of the 90-day T-bill is about to end.

Q: BlackRock (BLK) keeps growing, trillions after trillions. Why is the stock so great at building value?

A: Because you get a hockey stick effect on the earnings. As the stock market goes up, which it always does over time, their fees go up. Plus, their own marketing brings in new money. So, you have multiple sources of income rising at a rapid pace. I'm kicking myself for not buying the stock earlier this year.

Q: How does any antitrust action by the government affect stock prices?

A: Short-term, it caps them. Long term, it doubles them because when you break up these big companies, the individual pieces are always worth a lot more than the whole. We saw that with AT&T (T), where you're able to sell the individual seven pieces for really high premiums. So, that's why I'm never worried about antitrust.

Q: Do dividend stocks provide little upward appreciation since they're paying investors already?

A: To some extent, that's true because low-growth companies like formerly Philip Morris (PM) and Altria (MO) had to pay high dividends to get people to buy their stock because the industries were not growing. AT&T is another classic example of that—high dividend, no growth. But that does set you up for when a no-growth company can become a high-growth company, and then the stocks double practically overnight. And that's what's happening with Philip Morris.

Q: Are you buying physical gold (GLD) and silver (SLV)?

A: I bought some in the 1970s when it was $34/oz for gold, and the US went off the gold standard, and I still have them. It's sitting in a safe deposit box in a bank I will not mention. The trouble with physical gold is high transaction costs—it costs you about 10% or more to buy and sell. It can be easily stolen—people who keep them hidden at home or have safes at home regularly get robbed. And what if the house burns down? You really can't insure gold holdings accept with very high premiums. So, I've always been happy buying the gold ETFs. The tracking error is very small unless you get into the two Xs and three Xs. Gold coins are good for giving kids as graduation presents—stuff like that. I still have my gold coins for my graduation a million years ago (and that was a really great investment! $34 up to, you know, $2,700.)

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2015 in Italy

Global Market Comments

September 27, 2024

Fiat Lux

Featured Trade:

(THE MAD HEDGE SEPTEMBER 17-19 SUMMIT REPLAYS ARE UP),

(SEPTEMBER 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (NVDA), (GLD), (SLV), (AGQ), (URA), (X), (PGE), (FDX), (V), (CEG), (NEE), (CCJ), (FSLR), (TLT), (WMT), (FCX), (UBER), (LYFT), (FXB), (T)

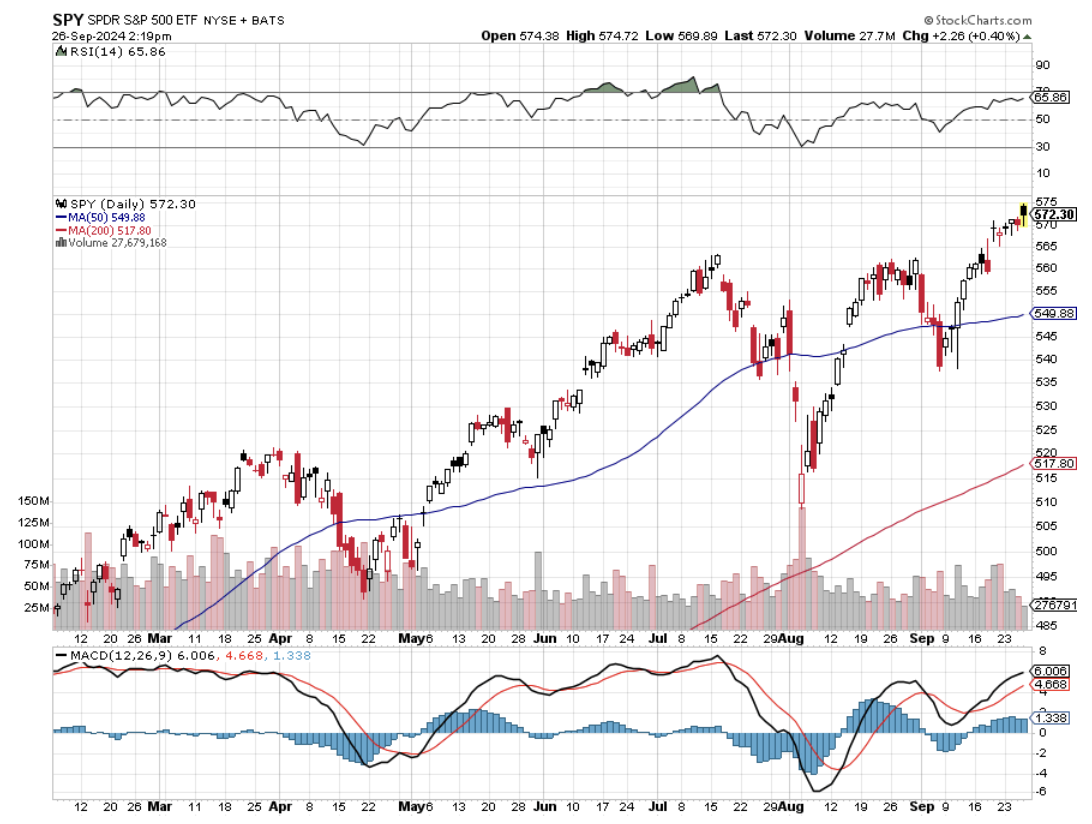

Below please find subscribers’ Q&A for the September 25 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe Nevada.

Q: The iShares 20+ Year Treasury Bond ETF (TLT) is not advancing like I had hoped. I’m not sure why the interest rate cuts have not impacted the 20-year maturity—is it too far out?

A: It’s not an issue of maturity; the fact is that the market has been discounting falling interest rates for six months, all the way back to March. It’s a classic “buy the rumor, sell the news” scenario. (TLT) rose $20 off the low this year, and once the rate cut actually happened, all the news was in. That is why I actually went short the TLT a couple of days ago, and that trade immediately started making money. Here’s the real problem: Fed futures are discounting 250 basis points in rate cuts by June of next year. If you don’t think we’re going to get 250 basis points in rate cuts, which is two 50 basis point rate cuts and five 25 basis point rate cuts, then the market is overbought for the short term and we’re selling short. That’s exactly what I did.

Q: Is it too late to buy Tesla (TSLA) and Nvidia (NVDA)?

A: No, it’s not, I think Tesla could hit $300 this year, and Nvidia could revisit $140. However, the more you wait, the more pain you have to take along the way. Nvidia did drop 40% off its high at one point this year, and Tesla dropped 80% off its high. The price of coming in late is pain, so be ready to take that pain or, even worse, to stop out.

Q: What is your take on Japan’s attempt to take over US Steel (X)?

A: Well, it’s entirely political. They definitely picked the wrong year to take a run at US steel because it’s headquartered in Pittsburgh, Pennsylvania, and neither political party can win their election without winning Pennsylvania. Nippon Steel is now 3x larger than US Steel (I covered the company for ten years when I lived in Japan.) It’s the steel factor Jimmy Doolittle bombed in the Pearl Harbor movie. US Steel is using 140-year-old technology—Open Hearth Technology—which hasn’t been updated since the Great Depression. Nippon Steel, meanwhile, is promising to scrap all of that and bring the Steel Industry into the 21st Century. All great ideas for Nippon Steel and their shareholders, but not so great for Unions; all of these takeovers always result in massive layoffs of Union workers. So, that is the issue. That’s where a large part of the added value comes from.

Q: What are the chances that interest rates drop to zero?

A: Zero. I don’t think we’ll ever see 0% interest rates again because people now understand the massive damage that causes to the economy and to savers. So, on the next interest rate cycle, we’ll go down maybe to 2% if we get a recession, but probably not much more than that.

Q: Is it a good time to buy FedEx Corp (FDX)?

A: Yes, it probably is. If there was one rule of trading this year, you buy everything on top of these monster selloffs that are caused by weak guidance. We did it on Palo Alto Networks (PANW) earlier this year—people made a fortune on that. FedEx just did the same thing, so yes, I’m looking very carefully at FedEx calls, call spreads, and LEAPS two years out.

Q: I recently saw a recommendation to buy California Utility Company PG&E (PGE) because of recent revenue gains. Should I take a look?

A: Absolutely, you should. PG&E has gone bankrupt twice in the last 25 years, and the current new management seems to know what they’re doing. They borrowed $20 billion to underground all the long-distance power lines in the state so they won’t be liable for any of these gigantic wildfires that caused the last bankruptcy. Also, you kind of want to own utilities when interest rates are falling because utilities are among the biggest borrowers in the country.

Q: Is Global X Uranium ETF (URA) a good proxy for Cameco Corp (CCJ)?

A: Yes, another one is Consolidation Energy Corp. (CEG), but they’ve all had absolutely astronomical moves ever since the announcement came out that Microsoft was reopening the Three Mile Island nuclear power plant. So, wait for a dip, but the thing is just going up every day right now.

Q: Is it time to buy iShares 20+ Year Treasury Bond ETF (TLT) LEAPS?

A: No, LEAPS territory was last year or the beginning of this year when we were in the $80s (and we issued a ton of (TLT) LEAPS last year.) LEAPS are what you do at market bottoms, not at new all-time highs or two-year highs. Remember, if LEAPS don’t work, they can go to zero, and you want to avoid the zero outcome as much as possible.

Q: Should I look at Visa Inc (V)?

A: Yes, this is another one of those poor guidance situations leading to 20% selloffs. In Visa’s case, they’re being sued by the US government for antitrust because they own 47% of the credit card market. So, I would maybe wait a little bit more, let the market fully digest that, and then Visa’s probably a really strong buy because they’re still growing at 15% a year and minting money like crazy.

Q: Do you see gold going to $3,000 next year?

A: Absolutely, yes, unless it goes to $3,000 this year, which raises a better question: what happens when gold hits $3,000? It goes to 4$,500, because Chinese savers have no other place to put their money except gold. The real estate has crashed and isn’t coming back, they don’t trust their own banks or currency—there really is nowhere else for them to put their own money. They don’t even buy gold miners, they just buy the gold metal and coins. So I think we could see much higher highs than gold, and I’m sticking to my longs.

Q: Will silver continue to lag?

A: No. In fact, in the last couple of weeks, silver has done a big catch-up that is happening because recession fears are going away. Even the soft-landing fears are starting to vaporize—we may have no landing at all. The economy may just keep going, and silver is far more sensitive to the economy than gold is; and that is all silver positive. When we get to the metals, you’ll see how much silver has actually caught up. Silver is probably the better buy here because it tends to outperform gold by two to one.

Q: Do you think the Japanese will cross 100 yen to the dollar in the near future?

A: No, but I think it may cross 100 to the dollar in two years. You’re looking at a permanently weak US dollar from now on. As long as we’re cutting interest rates faster than anyone else, our currency will be the weakest. Japan’s rates are at zero, so they’re not going to cut interest rates at all, which is why we've had this enormous move in the Japanese yen.

Q: Can you give me some good renewable energy stocks and reasons why they are good buys?

A: Well, my favorite renewables are the Canadian Uranium stock Cameco Corporation (CCJ), First Solar (FSLR), which has been the leading industrial-scale solar producer for a long time, and NextEra Energy (NEE), which is very heavily dependent on producing electric power from renewables and also have a 3% dividend.

Q: Why is the euro going up even though their economy is in such terrible shape?

A: Europe has much lower interest rates than the US, and therefore, much less ability to cut interest rates than the US; it is the interest rate cuts that are driving currencies down, and we are the world’s greatest interest rates cutter right now. So, that is why you’re getting outperformance of the euro (FXE).

Q: Financials have moved up over the last two weeks; what’s your take on year-end and beyond? Should I buy Goldman Sachs (GS), JP Morgan (JPM) and Morgan Stanley (MS)?

A: Yes on all three. They’re all big beneficiaries of falling interest rates, improving economies, declining default rates, and rising stock markets. So, you have a triple play on all three of those. I’d be buying the dips on all financials.

Q: When will the sell volatility come back?

A: When you get the Volatility Index ($VIX) over $30. That seems to be the sweet spot for selling volatility. We are now at $15.

Q: If the US sharply increases tariffs, what will be the impact on the economy?

A: It would basically amount to a 20% price increase on everything you buy—from clothes to electronic parts to everything else—and the stock market would crash. Probably 90% of the non-food items Walmart (WMT) sells is from China. That’s why they call it the Chinese embassy. Tariffs are a tremendous restraint of trade and never, ever work, except for targeted items like cars or solar panels. For instance, I am in favor of a 100% tariff on Chinese cars to keep them from demolishing our own car industry as they are currently doing in Europe.

Q: Do we expect commodities like copper (FCX) and foodstuffs to go up as rates are cut?

A: I do. They’re big beneficiaries of falling rates, but more importantly, they’re even bigger beneficiaries of a stimulated Chinese economy, and that’s why we see these monster moves over the last two days.

Q: If you had to invest in one rideshare company, would it be Lyft (LYFT) or Uber (UBER)?

A: Uber—they have far superior management, they’ll be the first into robo-taxis, and they are constantly evolving their model, with Lyft always struggling to catch up.

Q: How will antitrust regulation affect the Magnificent Seven?

A: The bottom line is it will double the value of the Magnificent Seven. If these companies are broken up, the individual parts are worth far more than the whole companies, and we saw this when we broke up AT&T (T) 50 years ago, and the resulting seven companies within a year had a combined market value that vastly exceeded the original AT&T. I actually participated in that deal when I was at Morgan Stanley (since I am 6’4” I was asked to carry the ballots from one floor to another). Expect the same to happen with the Magnificent Seven. They will be worth double or triple more.

Q: If China has a falling population, how will a stimulus program help?

A: Well, it will fill in for the 600 million consumers who were never born as a result of the one-child policy. Not many others are talking about this besides me, but the fact is that the current economic weakness comes entirely from the one-child policy, and there is no way out of that, so they are going to have to keep stimulating again and again, much like the US did through the pandemic.

Q: If you can buy gold and silver on the UK market in sterling, does that make more sense for a UK resident?

A: Yes, it does, since your home currency is in sterling. You will actually get a double play or a “hockey stick effect” because not only is gold going up against the US dollar, but sterling (FXB) is going up against the US dollar, so you’ll get a multiplied effect relative to the pound. We used to play this all day long in Europe in the 1970s and 1980s, back when you had individual currencies to trade and the euro hadn’t been invented yet.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Fishing in the High Sierras

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

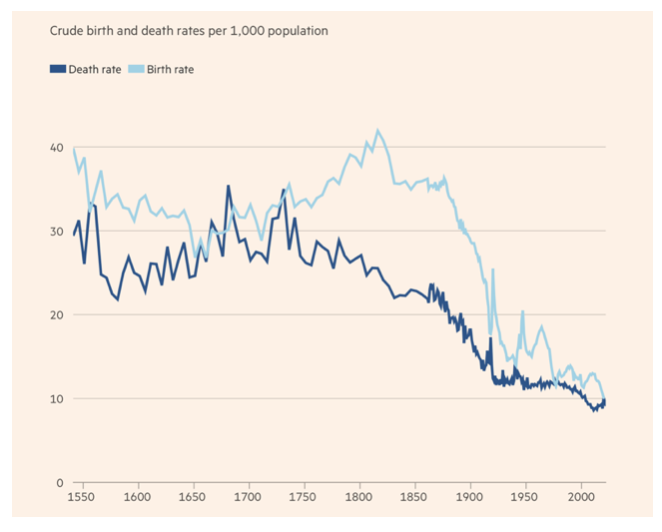

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

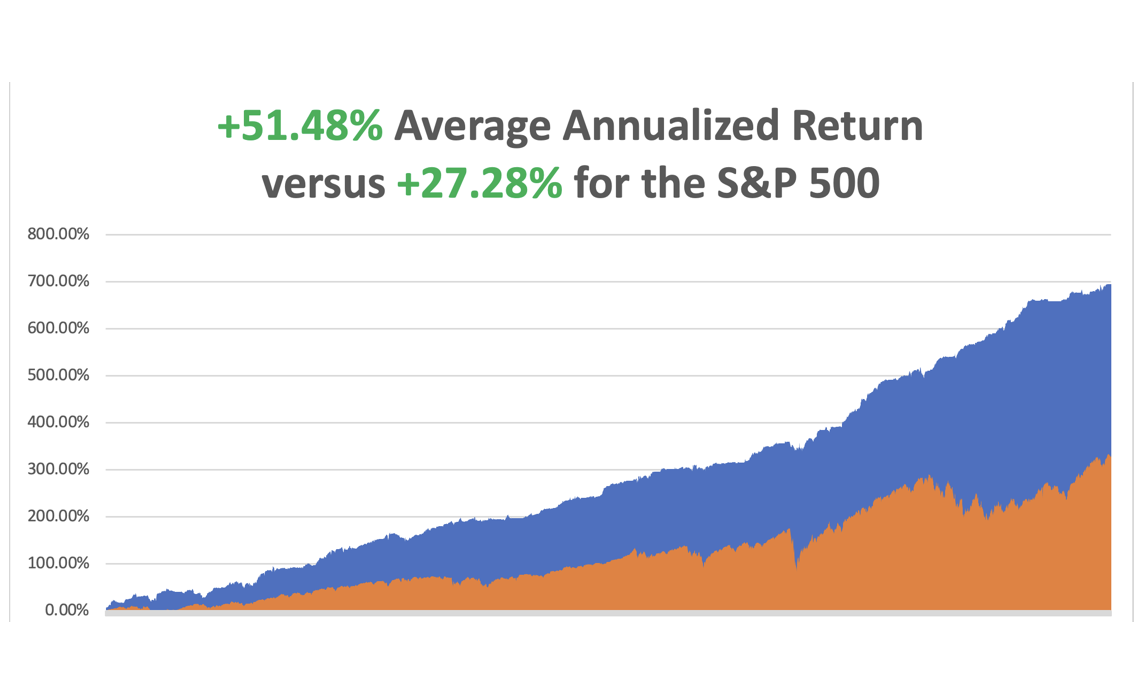

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%. The S&P 500 (SPY) is up +10.48% so far in 2024. My trailing one-year return reached +35.74%.

That brings my 16-year total return to +694.78%. My average annualized return has recovered to +51.48%.

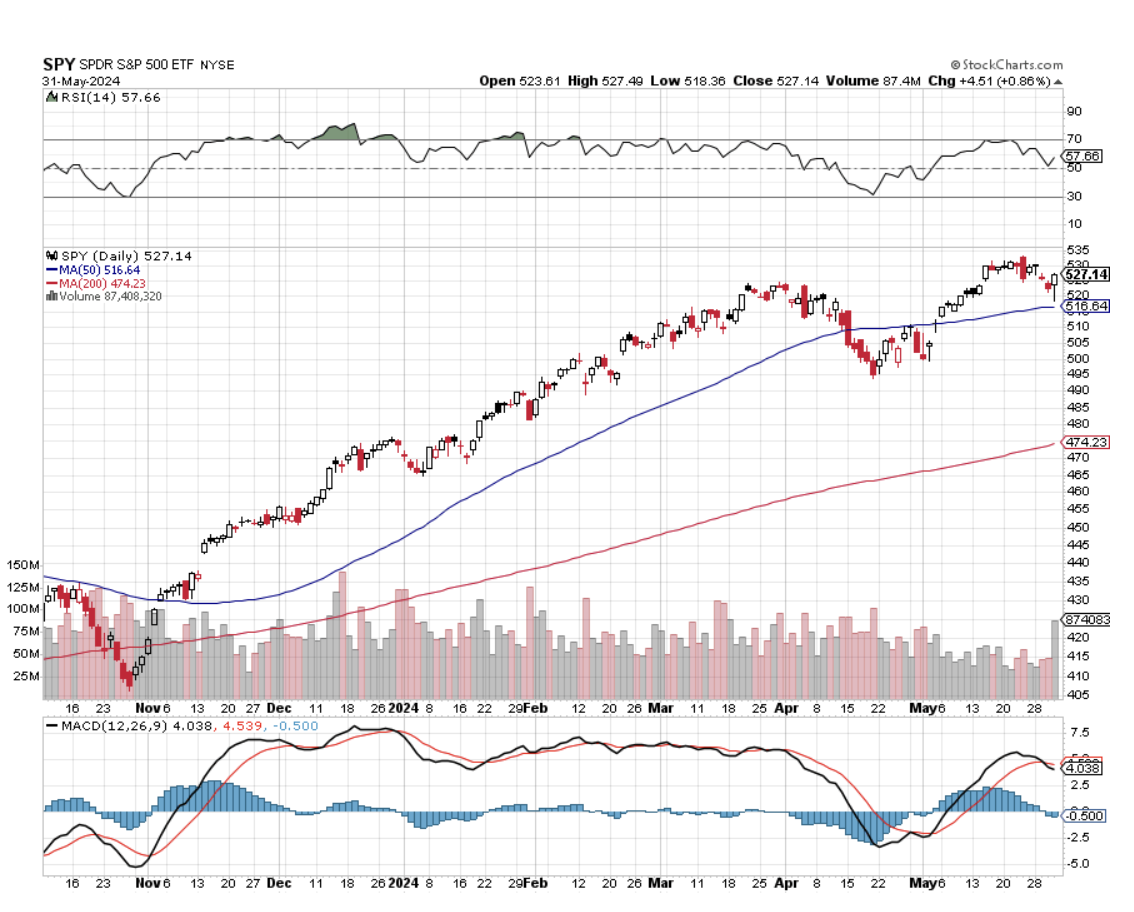

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day.

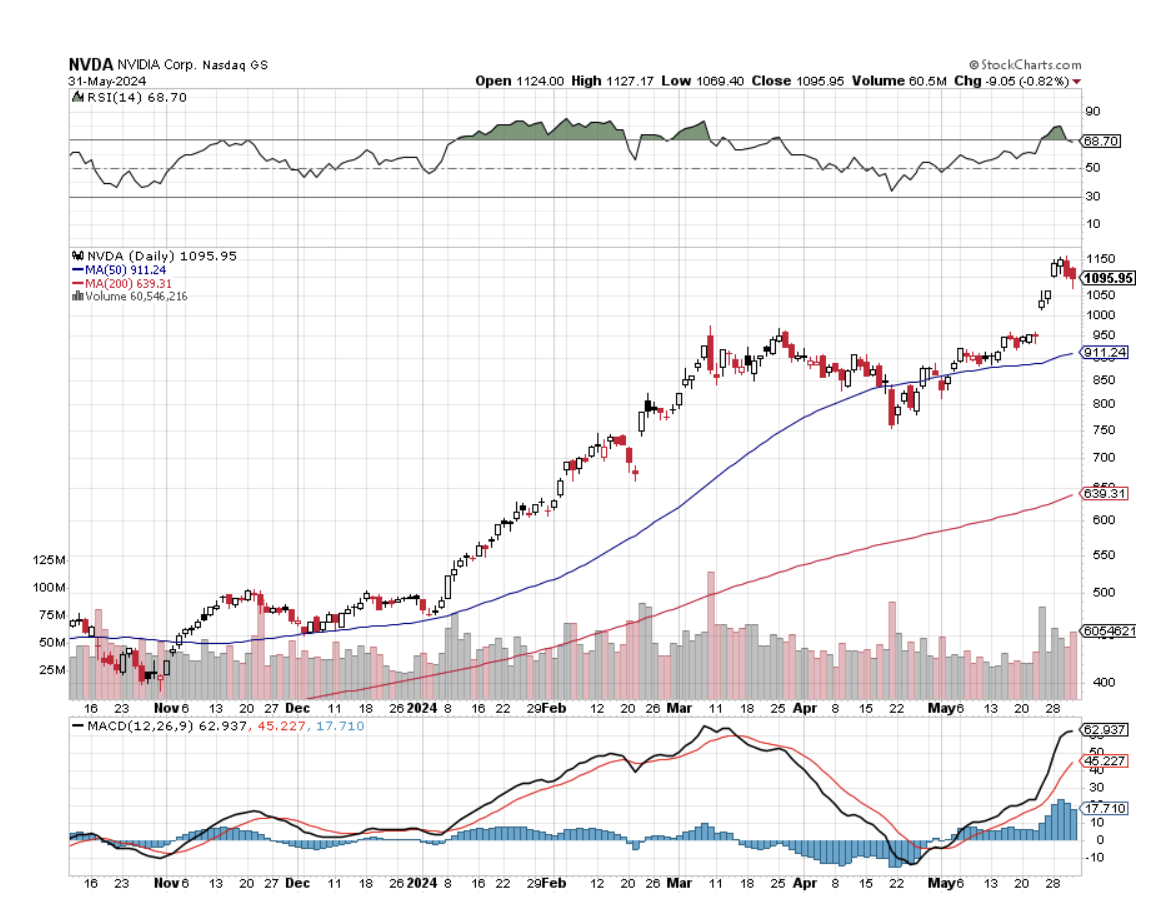

NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

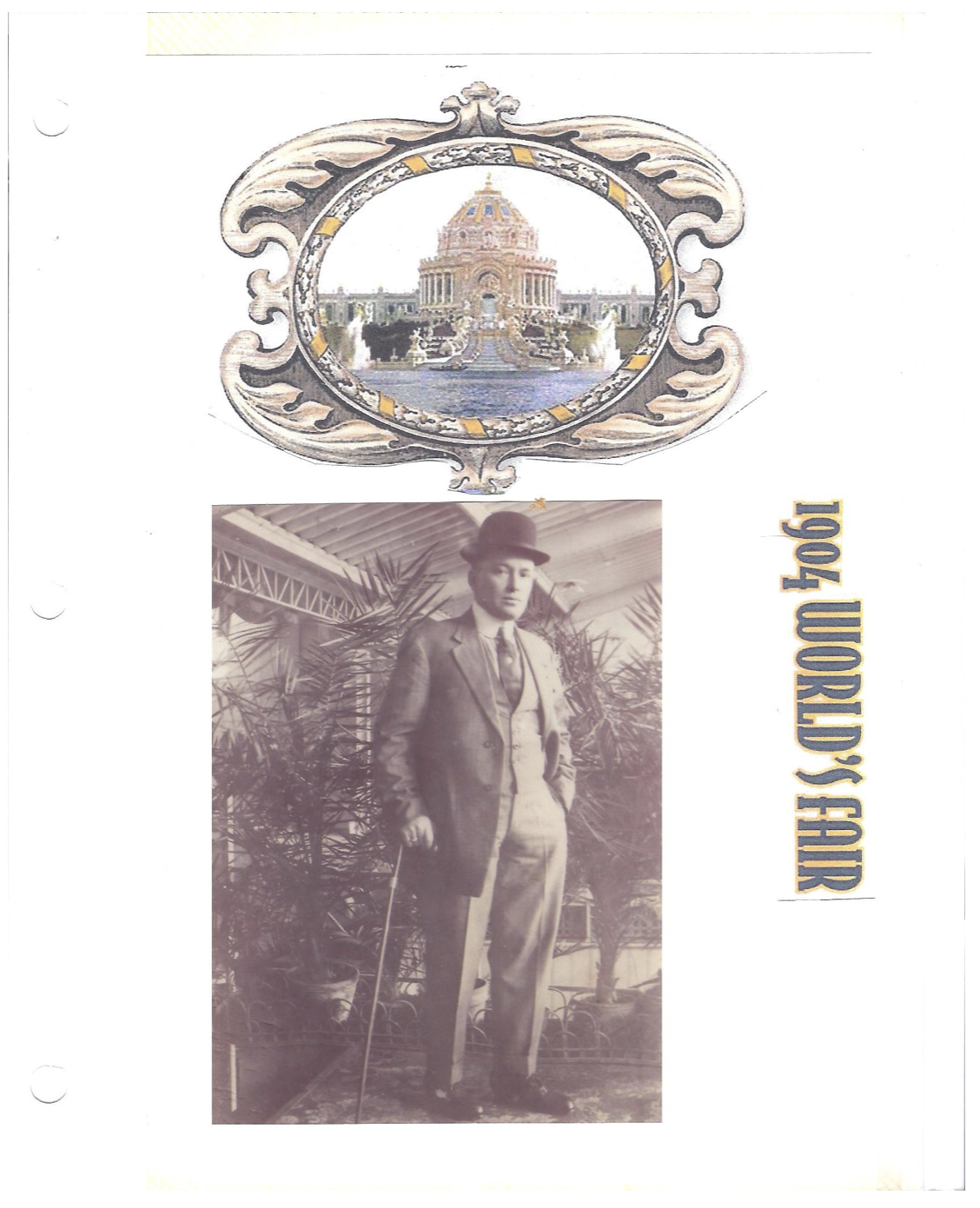

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity. By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 19, 2023

Fiat Lux

Featured Trade:

(WHO WAS THE GREATEST WEALTH CREATOR IN HISTORY?)

(FB), (AAPL), (GOOG), (AMZON),

(XOM), (BRKY), (T), (GM), (VZ), (CCA),

(WHY DOCTORS MAKE TERRIBLE TRADERS?)

Who’s been buttering your bread more than any other?

Which publicly listed company has created the most wealth in history?

I’ll give you some hints.

The founder never took a bath, was a devout vegetarian, and dropped out of college after the first semester. The only class he finished was for calligraphy. And he was a first-class asshole.

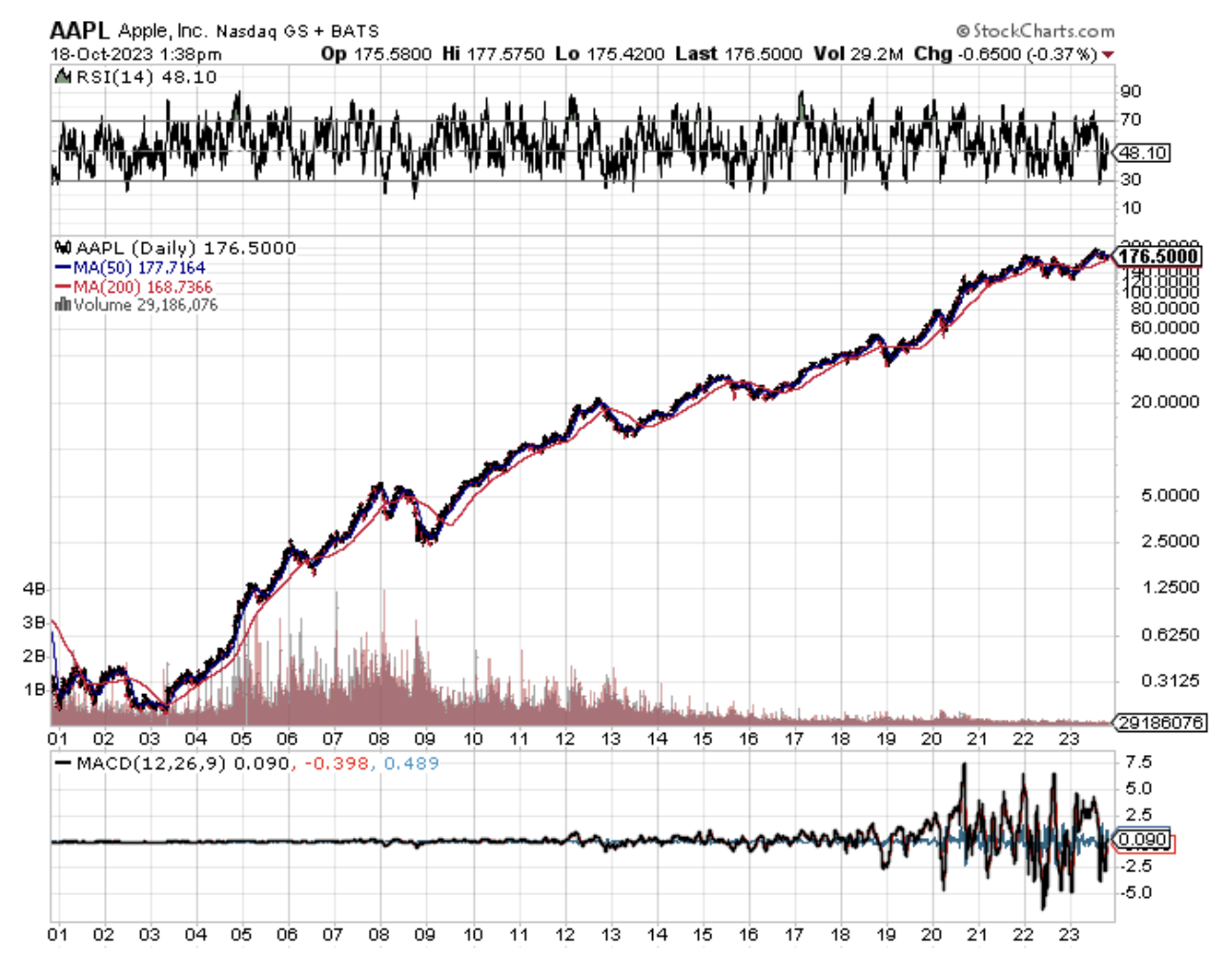

Silicon Valley residents will immediately recognize this character as Steve Jobs, the co-founder of Apple (AAPL).

In 43 years, his firm created over $3 trillion of wealth for his shareholders, making it the largest in the world.

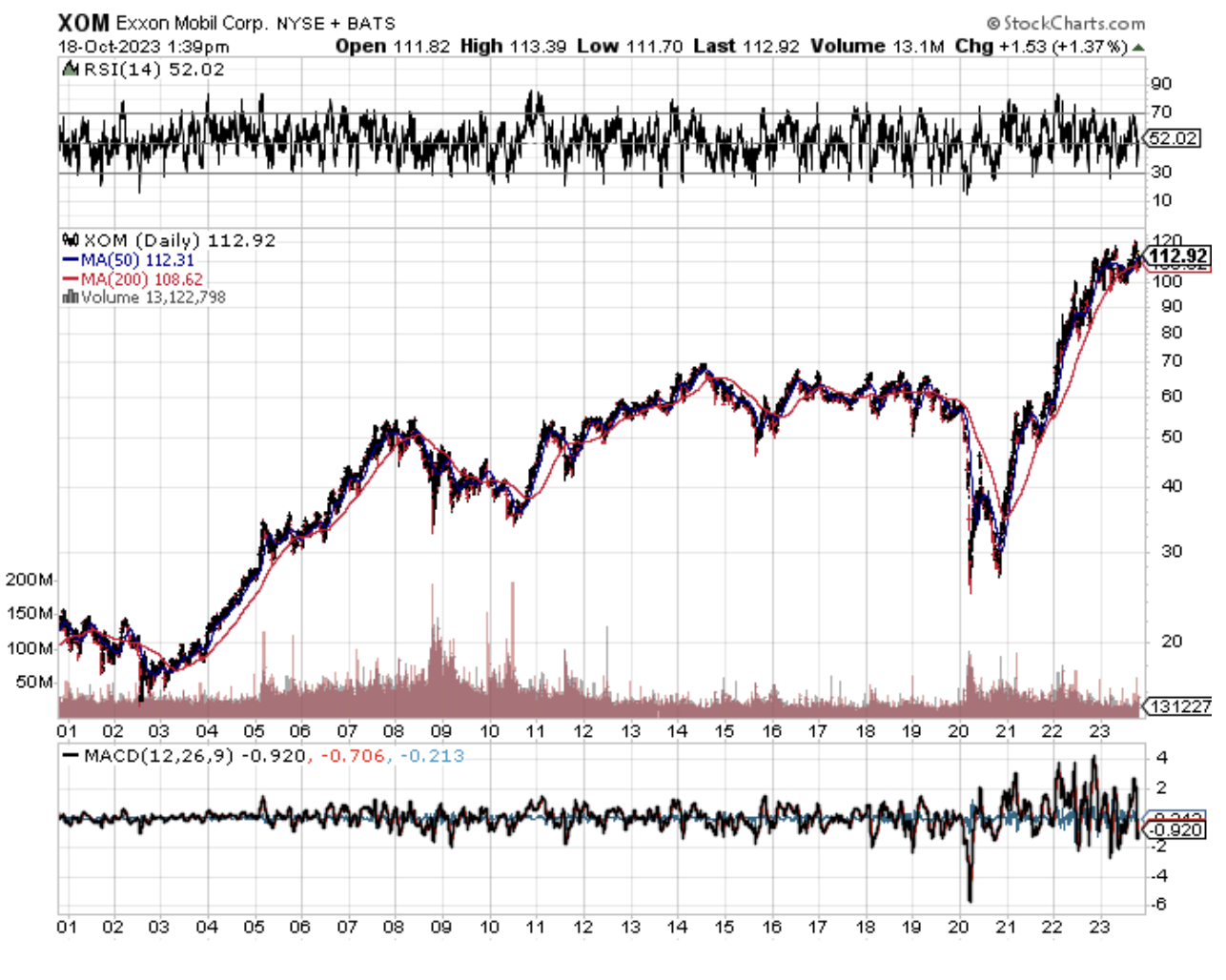

Until a decade ago, Exxon (XOM) held the top spot, creating $900 million in new wealth, although to be fair, it took 100 years to do it.

To be completely and historically accurate, most of the original seven sister oil companies are decedents of John D. Rockefeller’s Standard Oil Company.

Add the present value of these together, and Rockefeller is far and away the biggest money maker of all time. And he made most of this before income taxes were invented in 1913!

Reviewing the performance of other top-performing companies, it is truly amazing how much wealth was created from a technology boom that started in the 1980s.

Investors’ laser-like focus on the Magnificent Seven is well justified.

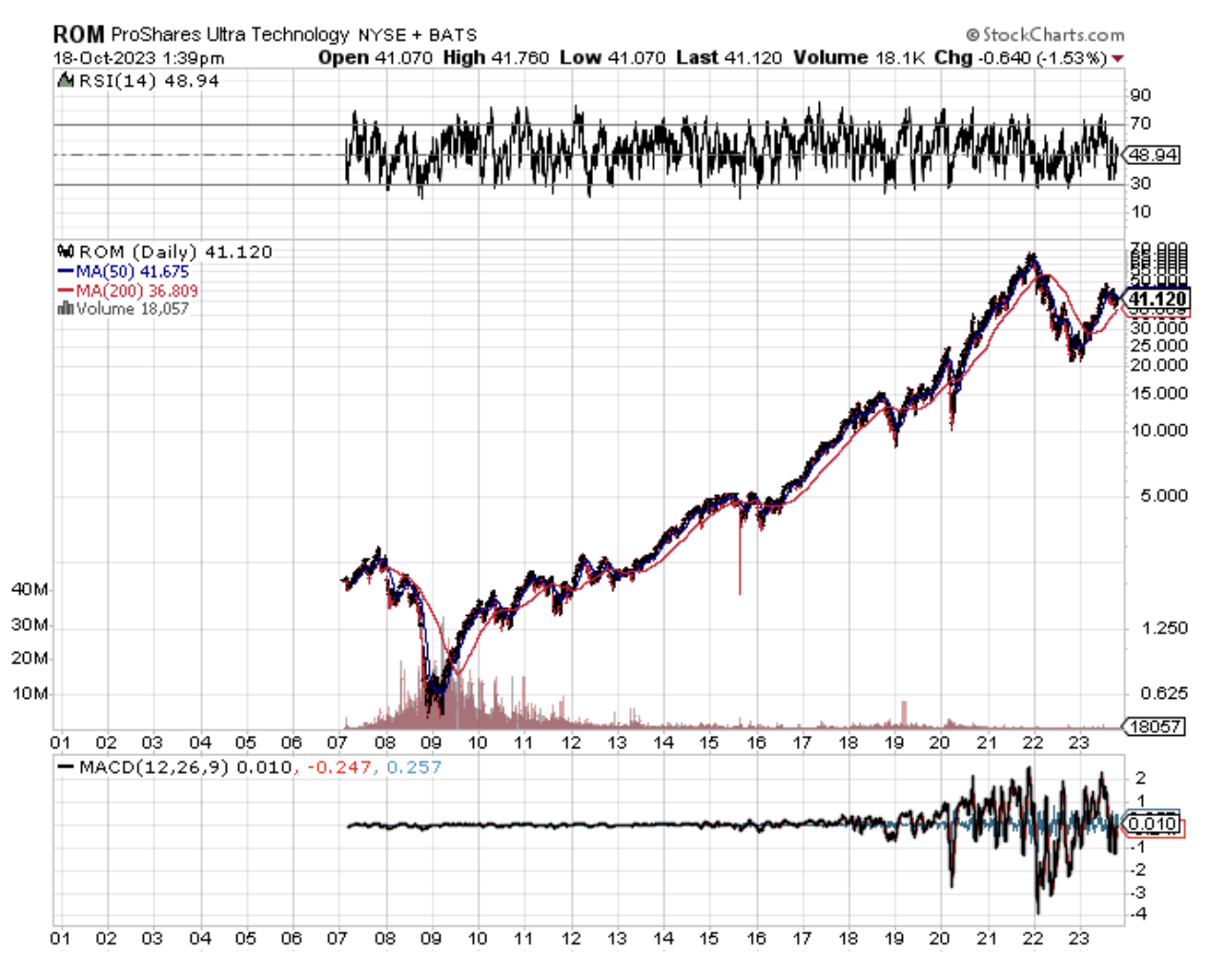

That’s why I often tell guests during my lectures around the world that if they really want to be lazy, just buy the ProShares Ultra Technology ETF (ROM) and forget everything else.

Another college dropout’s efforts, those of Bill Gates Microsoft (MSFT), produced an annualized return of 25% since 1986. That made him the third greatest wealth creator in history.

It also made him the world's richest man, until Jeff Bezos and Elon Musk came along. Gates is thought to have single-handedly created an additional 1,000 millionaires as so many employees were aided in stock options.

Facebook (FB) is the youngest on the list of top money makers, creating an annualized 34.5% return since it went public in 2012.

Alphabet (GOOG) is the second newest on the list, racking up a 24.9% annualized return since 2004.

Amazon (AMZN) is 14th on the list of all-time wealth creators and has just entered its 20th year as a public company.

Being an armchair business and financial historian, many runners-up were major companies in my day, but generate snores among Millennials now.

Believe it or not, General Motors (GM) still ranks as the 8th greatest wealth creator of all time, even though it went bankrupt in 2008.

Ma Bell or AT&T (T) ranks number 17th but was merged out of existence in 2005. A regrouping of Bell System spinoffs possesses the (T) ticker symbol today.

Among its distant relatives are Comcast (CCV) and Verizon Communications (VZ).

Warren Buffet’s Berkshire Hathaway (BRKY) ranks 12th as an income generator, with an annualized return of only 11.94%.

Its performance is diluted by the low returns afforded by the textile business before Buffet took it over in 1962. Buffet’s returns since then have been double that.

Analyzing the vast expanse of data over the last 100 years proves that single stock picking is a mug's game.

Since 1926, only 4% of publically traded stocks made ALL of the wealth generated by the stock market.

The other 96% either made no money to speak of, or went out of business.

This is why the Mad Hedge Fund Trader focuses on only 10%-20% of the market at any given time, the money-making part.

In other words, you have a one in 25 chance of picking a winner.

A modest 30 companies accounted for 30% of this wealth, while 50 stocks accounted for 40%.

You can only conclude that stocks make terrible investments, not even coming close to beating the minimal returns of one-month Treasury bills, a cash equivalent.

It also is a strong argument in favor of indexed investment in that through investing in all major companies, you are guaranteed to grab the outsized winners.

That is unless you follow the Diary of a Mad Hedge Fund Trader, which picked Amazon, Apple, Facebook, Google, NVIDIA, and Tesla right out of the gate.

If you want to learn more about the number crunching behind this piece, please visit the research of Hendrik Bessembinder at the W.P. Carey School of Business at Arizona State University.

Such a Money Maker!

Global Market Comments

December 17, 2021

Fiat Lux

Featured Trade:

(DECEMBER 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(FCX), (FCI), (TLT), (TBT), (BITO), (AAPL), (AMZN), (T), (TSLA), (BABA), (BLOK), (MSTR), (COIN)

Below please find subscribers’ Q&A for the December 15 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: With interest rates going up, would it make sense to short heavily indebted companies as a class?

A: Yes it does; those would be old-line industrials and auto companies with very heavy debts. Technology companies essentially have no debt unless they’re startups. So yeah, that’s a good idea; unless of course inflation is peaking right now, which it may be if you solve these supply chain problems, and it becomes evident that retailers overordered to beat the supply chain problems and now have a ton of excess inventory they can’t meet—then the inflation plays will crash. So, not a low-risk environment right now. No matter where you look, you’re screwed if you do, you’re screwed if you don't. So that is an issue to keep in mind.

Q: What do you think of Freeport McMoRan (FCX) short-term?

A: Short term, (FCX) only sees the Chinese (FXI) real estate crisis, which is getting worse before it gets better and could bring a complete halt to all known construction in China. The government is forcing the real estate companies there to run at losses in order to bring the bottom part of their society into the middle class with houses in third and fourth-tier cities. Long term, as annual electric car production goes from a million cars a year to 25 million cars a year and each car needs 200 lbs. of copper, we have to triple world production practically overnight to accommodate that. That can’t happen, therefore that means much higher prices. If you’re willing to take some pain, picking up freeport McMoRan in the low $30s has to be the trade of the century.

Q: Do you see a Christmas rally or a bigger correction?

A: Rally first. Once we get the Fed out of the way today, we could get our Christmas rally resumed and go to new highs by the end of the year. But, January is starting to look a little bit scary with all the unknowns going forward and massive long positions. January could be okay as hedge funds put positions back on in tech that they’re dumping right now. If they don’t show up…Houston, we might have a problem.

Q: Thoughts on the iShares 20 Plus Year Treasury Bond ETF (TLT) Dec 2022 $150-$155 vertical bear put spread?

A: Since I'm in low-risk mode, I would go up $5 or $10 points and not be greedy. Not being greedy is going to be one of the principal themes of 2022 therefore I’m recommending that people do the $160-$165 or even the $165-$170, which still gives you a 30% return in a year, and I think next year this will be seen as a fabulous return.

Q: What about the $100,000 target for Bitcoin (BITO) by the end of the year?

A: That’s off the table thanks to the Fed tightening and Omicron triggering a massive “RISK OFF” and flight to safety move. Non-yielding instruments tend not to do well during periods of rising interest rates, so gold along with crypto is getting crushed.

Q: What will happen in the case of a black swan event in early 2022, like Russia invading Ukraine?

A: Market impact for that would be a bad couple of days, a buying opportunity, and then you’d want to pile into stocks. Every geopolitical event that’s happened in the last 20 years has been a buying opportunity for stocks. Of course, I would feel bad for the Ukrainians, but it’s kind of like Florida seceding from the US, then the US invading Florida to take it back, and the rest of the world not really caring. Plus, it doesn’t help that their heavily nationalist post-coup government has some fascist tendencies. However, we could get global economic sanctions against Russia like an import/export embargo, which would hurt them and destroy their economy.

Q: Will the European natural gas shortage continue?

A: Yes because the Europeans are at the mercy of the Russians, who have all the gas and none of the economy. Therefore, they can export as much or as little as they want, depending on how much political control they’re trying to exert in Europe.

Q: Apple Inc. (AAPL) price target?

A: Well, my price target for next year was $200; we could hit that by the end of the year if we get a rally after the Fed meeting.

Q: 33% of the population is in collection status with personal debt, credit cards, etc—is that a harbinger of a 2008 crash?

A: No, it is a harbinger of excess liquidity, interest rates being too low, and lenders being too lax. However, we aren’t at the level where it could wipe out the entire economy like with defaulting on a third of all housing market debt in 2008.

Q: What should I do with my call spreads for Amazon.com, Inc. (AMZN)?

A: Well, November would have been a great sell. Down here, I’d be inclined to hold onto the spreads you have, looking for a yearend rally and a new year rally. But remember, with all these short-dated plays risk is rising, so keep that in mind.

Q: What do you think of AT&T Inc (T)?

A: The whole sector has just been treated horrifically; I don’t want to try to catch a falling knife here even though AT&T pays a 10% dividend.

Q: What about quad witching day?

A: Expect a battle by big hedge funds trying to push single stocks options just above or below strike prices. It’s totally unpredictable because of the rise of front-month trading, which is now 80% of all options trading with the participation of algorithms.

Q: Is the Alibaba Group Holding Limited (BABA) $230-$250 LEAP in June 2023 worth keeping?

A: I would say yes, I think the Chinese will come to their senses by then, and all the Chinese tech plays will double, but there’s no guarantee. That is still a high-risk trade.

Q: Does the US have an opportunity to export petroleum products?

A: The answer is yes, we are already a net energy exporter thanks to fracking. But, it is a multi-year infrastructure build-out to add foreign export destinations like Europe, which hasn’t bought our petroleum since WWII. Right now, almost all of our exports are going to Asia. No easy fixes here.

Q: Is Tesla Inc (TSLA) a buy at 935 down 300 in change?

A: Not yet; 45% seems to be the magic number for Tesla correction. We had one this year. And Elon Musk hasn’t quit selling yet, although I suspect he’ll end his selling by the end of the year because he’ll have met all his tax obligations for the year. He has to sell these options before they expire and are rendered useless. So that is what’s happening with Tesla, Elon Musk selling. And can you blame him? He almost worked himself to death making that company, time to spend some money and have a good time, like me.

Q: What if your Chinese company gets delisted?

A: Try to get out before it is delisted. Otherwise, the domicile moves to Hong Kong and you’ll have to sell equivalent shares there. I don’t know what the details of that are going to be, but the Chinese companies are trying to force companies to delist from the US and list in Hong Kong so they have complete control over what's going on. Also, I never liked these New York listings anyway because the disclosures were terrible, with Cayman Island PO Boxes and so on…

Q: Is the ProShares UltraShort 20+ Year Treasury (TBT) a good long-term position to hold?

A: It is to an extent—only if you expect any big moves up in interest rates, which I kind of am. This is because the cost of carry for (TBT) is quite high; you have to pay double the 10-year US Treasury rates, which is double 1.45% or about 2.90%, and then another management fee of 1%, so you have kind of a 4% a year headwind on that because of cost. Remember, if you’re short a bond, you’re short a coupon; if you’re double short a bond you’re short twice the coupon and you have to pay that and they take it out of the share price. But, if you’re expecting bonds to go down more than 4%, you’ll cover that and then some and I think bonds could drop 10-20% this year.

Q: What’s the difference between GBTC and BITO?

A: Nothing, both are Bitcoin plays that are tracking reasonably well. I prefer to go with the miners—the Bitcoin providers, that’s a selling-shovels-to-the-gold-miners play. They tend to have more volatility than the underlying Bitcoin, so that’s why I’m in (BLOK) and (MSTR) when I’m in it.

Q: What’s the best way to buy Crypto?

A: If you really want to buy Crypto directly, the really easy way is to go through one of the top crypto brokerage houses, and we’ve recommended several of those. Coinbase (COIN) is the one I’m in. It literally takes you five minutes to set up an account and you can instantly buy Bitcoin linked to your bank account.

Q: What are the fees like for Coinbase?

A: The fees at (COIN) are exorbitant only if you’re buying $10 worth of Bitcoin. If you’re buying like $1 million worth, they’re much, much smaller. But I recommend you start at $10 and work your way up as I did, and sooner or later you’ll be buying million-dollar chunks of Bitcoin which then double in three months, which happened to me this year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader