Global Market Comments

June 24, 2025

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(WHAT EVER HAPPENED TO THE GREAT DEPRESSION DEBT?),

($TNX), (TLT), (TBT)

Global Market Comments

June 24, 2025

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(WHAT EVER HAPPENED TO THE GREAT DEPRESSION DEBT?),

($TNX), (TLT), (TBT)

Global Market Comments

December 18, 2024

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(WHAT EVER HAPPENED TO THE GREAT DEPRESSION DEBT?),

($TNX), (TLT), (TBT)

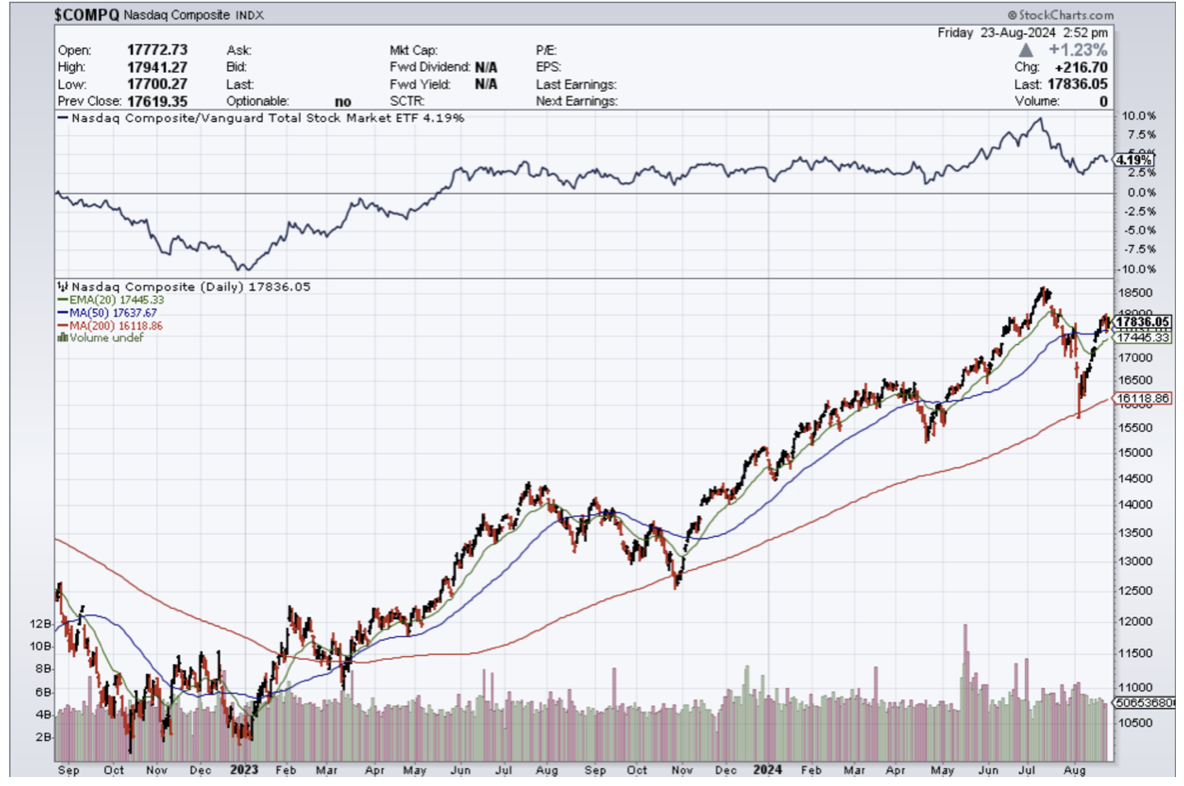

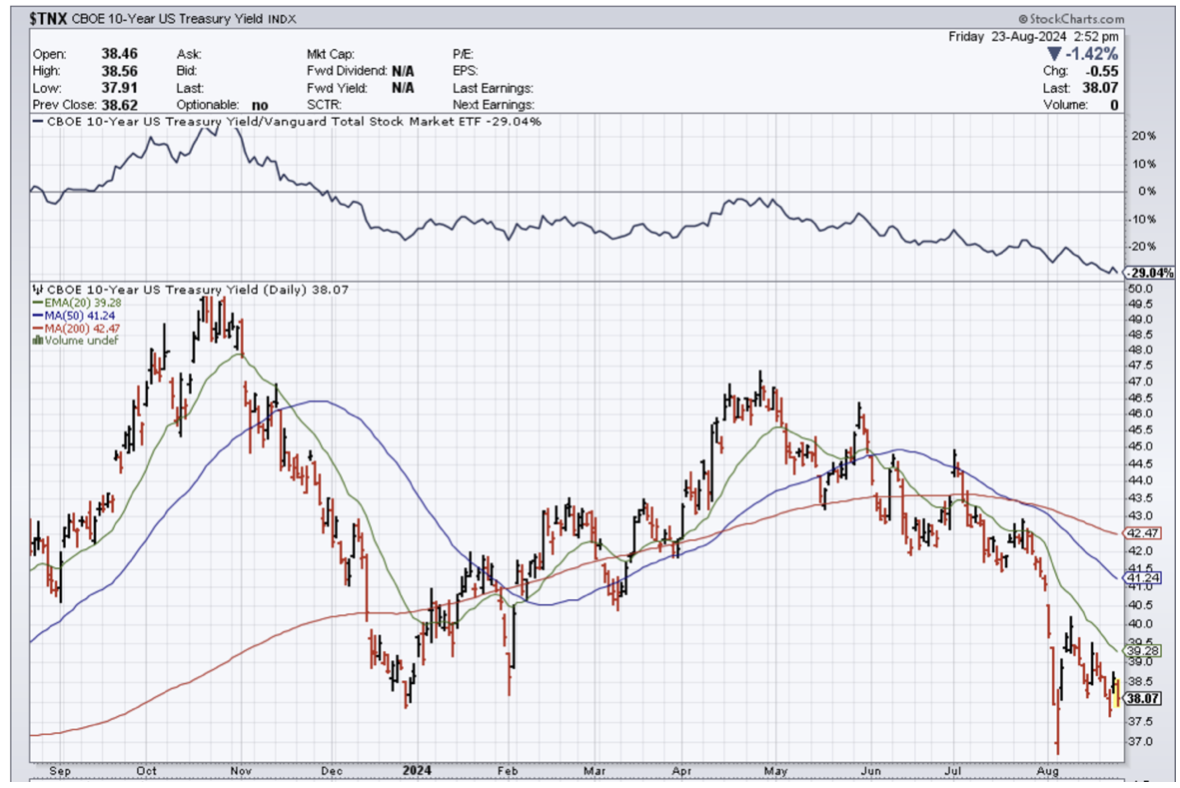

Mad Hedge Technology Letter

August 23, 2024

Fiat Lux

Featured Trade:

(TECH STOCKS LAUNCHED INTO ORBIT BY JEROME)

($COMPQ), ($TNX)

The job is done – The Fed won against inflation.

When is the parade?

That was largely the message that was delivered to us this morning by U.S. Federal Reserve Chairman Jerome Powell.

Migrating into rate-cutting mode means that tech stocks ($COMPQ) are about to explode into orbit.

We will only know how much higher tech stocks will go when we can understand how much Powell’s Fed will cut.

If he cuts the Fed Funds rate from 5.25% to 2% then tech stocks will be up at least another 50% from these levels.

What is bizarre is that Powell is cutting rates ($TNX) with housing prices, grocery costs, stock market, and a price for one ounce of gold at all-time highs.

Things are about to get more expensive – that is guaranteed.

Ironically, the Fed is planting the seeds for the next rip-roaring wave of inflation, because 3% inflation levels will be the new floor and not the ceiling.

Once the CPI hit 2.9% just a few days ago, the Fed went into the “the job is done” mode which is extremely dangerous.

Either way, tech stocks are in for a spectacular monster rally heading into the year's close and we just added a big position in chip stock Micron (MU).

There should be two to three .25% cuts by the end of the year which is highly bullish for equities.

"The direction of travel is clear," Powell added.

Powell acknowledged recent softness in the labor market in his speech and said the Fed does not "seek or welcome further cooling in labor market conditions."

The July jobs report rattled markets earlier this month, revealing that there were just 114,000 jobs added to the economy last month while the unemployment rate rose to 4.3%, the highest since October 2021.

Data earlier this week also showed that 818,000 fewer people were employed in the US economy as of March, suggesting reports have been overstating the strength of the job market over the last year.

Powell's remarks on Friday were reminiscent of those he delivered at Jackson Hole in 2022, in which the Fed chair offered a direct assessment of the economic outlook and, at the time, the need for additional rate increases.

The similar part of the speech was his call to action to change the direction of policy and he did just that.

We are about short-term trading and trade alerts here in what moves the market with tech trades.

I do believe long-term, what Fed chair Jerome Powell did, will turn out to be a policy mistake that will result in a lot higher bond yields.

The Fed's slow walking the rate hikes on the way up and then now slow walking the rate cuts on the way down is a recipe for disaster and the wrong way to approach this problem.

The ironic thing here is that tech stocks are the only equities, apart from energy and supermarket stocks, to do well in a higher inflation backdrop and part of that has to do with their monopolistic power which continues unabated.

Not that tech needed any help, but help is arriving in terms of lower rates and I do believe tech stocks will do well as we move closer to year-end.

Buckle up, put on your cowboy hat, and enjoy the tech rally!

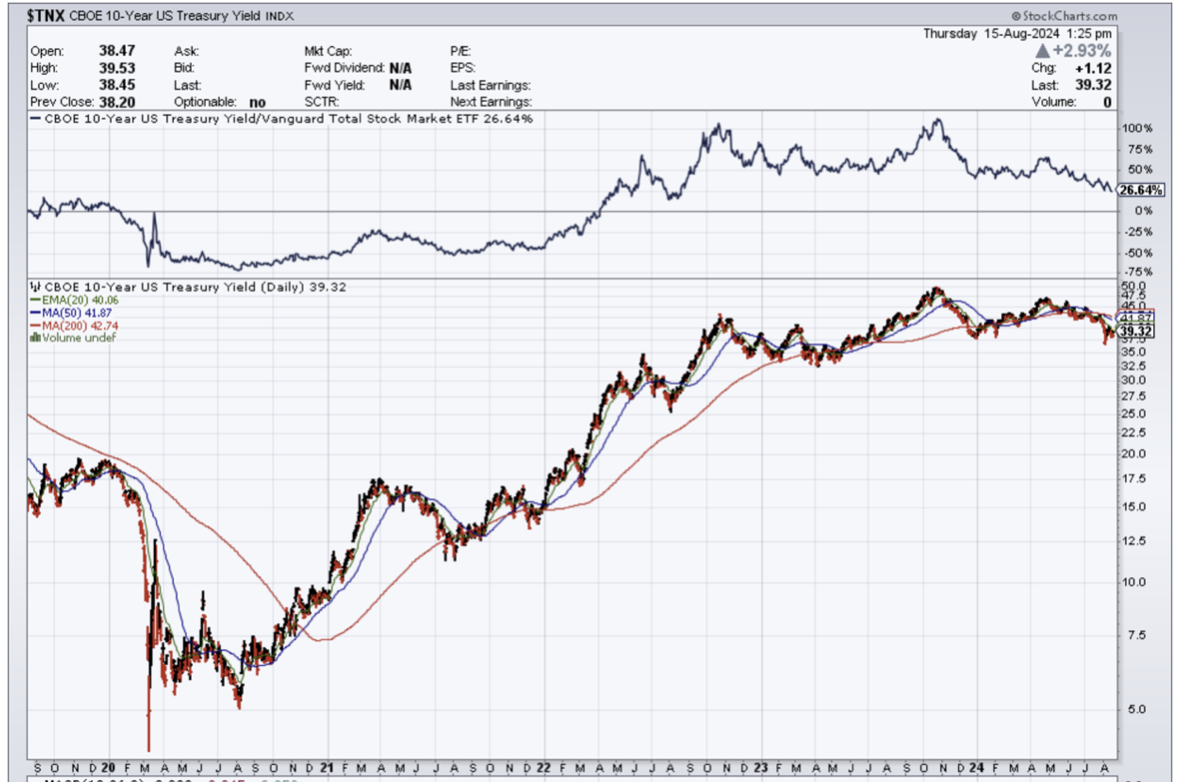

Mad Hedge Technology Letter

August 16, 2024

Fiat Lux

Featured Trade:

(BIG RISKS TO TECH DISSIPATE)

($COMPQ), ($TNX), (FXY)

I don’t believe the tech sector is toast and it isn’t true to say that the burnt crust is the only part left over.

There is still vitality in it at the core of the tech sector ($COMPQ).

Granted, the trajectory left isn’t enough to propel tech stocks to a meteoric rise, but tech stocks should perform quite robustly in the run-up to the next earnings report.

So for all that are waiting for the bubble to burst – wait a little longer my friends.

In the meantime, let’s take a quick barometer of some of the outsized risks to big tech and ponder about the idea that outside or indirect events could possibly takedown tech shares.

China bailed the world out of the last three recessions and now they are a risk to drag down the rest of the world.

In each case, China's high growth and massive issuance of stimulus kick-started global expansion, and now that is gone with the wind.

China's model of economic development which worked so brilliantly in the boost phase, is now out of potency.

If American tech shares are sideswiped by global contagion, don’t bet on China to come bail out the radical overlords of Silicon Valley. China has its own problems and is entirely focused on that.

The era of zero-interest rates and unlimited government borrowing has ended. As Japan has shown, even at insane low rates ($TNX) of 1%, interest payments on skyrocketing government debt eventually consume virtually all tax revenues.

Japan was the black swan that could have cratered the tech market. Instead, it was a mild selloff yet manageable selloff creating a beautiful entry point for most of tech stocks.

Money is coming off the sideline to join in on a sharp rally into the U.S. presidential election so in the end the Japanese currency (FXY) risk was basically much-a-do-about-nothing.

At the start of the cycle, global debt levels (government and private sector) were low. Now they are high. The boost phase of debt expansion and debt-funded spending is over, and we're in the stagnation-decline phase where adding debt generates diminishing returns.

The era of low inflation has also ended for multiple reasons, but the tech shares have proven they can unequivocally march higher in an era of high inflation.

This is ironically due to tech being better positioned than other industries on a relative basis, because of their strong moats and iron-clad balance sheets.

The resilience in tech also echoes the idea that every company has become a tech company by integrating its products and revenue streams into daily business operations.

Tech productivity boom is hardly a one-off so as readers fret, please don’t think shares will magically drop to zero.

Dips are being bought and prices will go higher in the short term.

Economists were in awe in the early 1990s by the productivity stemming from the tremendous investments made in personal and corporate computers, a boom launched in the mid-1980s with Apple's (AAPL) Macintosh and desktop publishing, and Microsoft's Mac-clone Windows operating system.

By the mid-1990s, productivity continued to rise and the emergence of the Internet triggered the adoption of most of the population to get online and do business.

All the doomsday prophets who said high debt and high interest rates were the cocktails to finally stop tech stocks in their tracks got it completely wrong.

I am not saying debt and high interest rates are positive for equities, but tech has been able to skillfully navigate the headwinds with their excellent management skills and pivot towards leanness.

The buzz around AI holds still has a lot to prove, but the market is still celebrating its deflection of the Japanese yen carry trade.

I am not saying that tech shares will never have to confront anything that can drag them down meaningfully, but many of the high risks have either been postponed or dealt with.

We are in a position where tech should steamroll into the end of the year barring some type of crazy event.

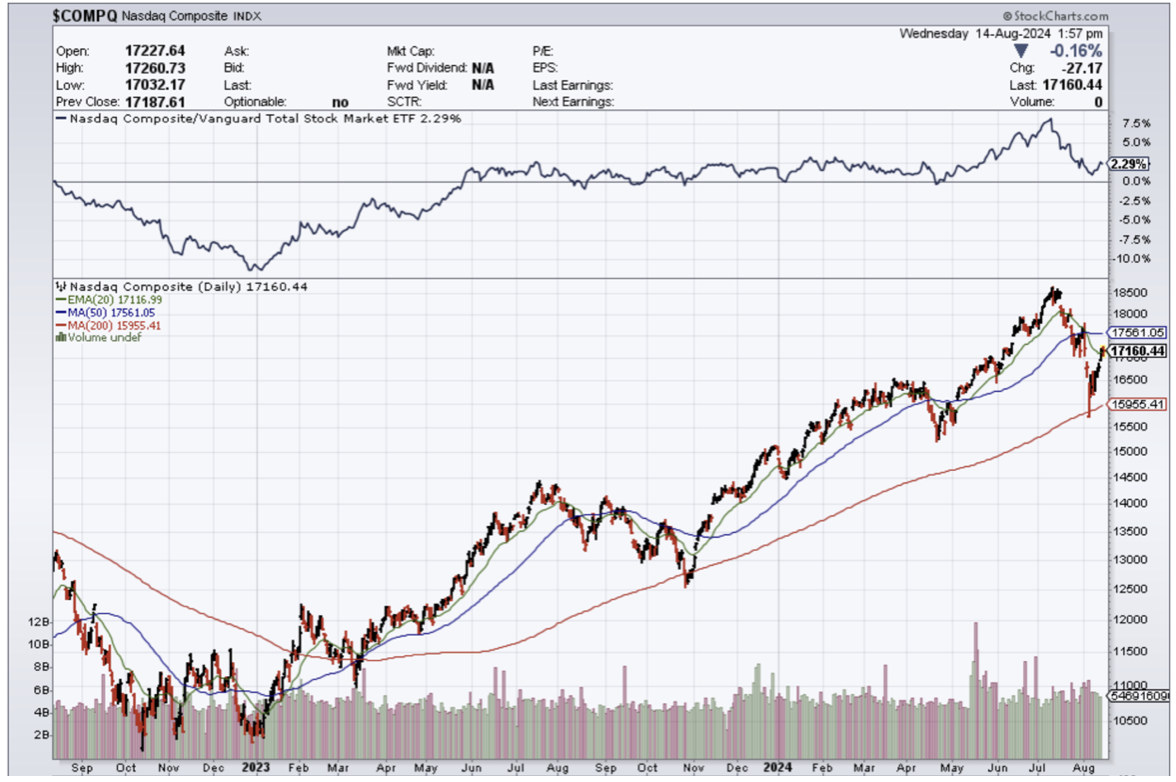

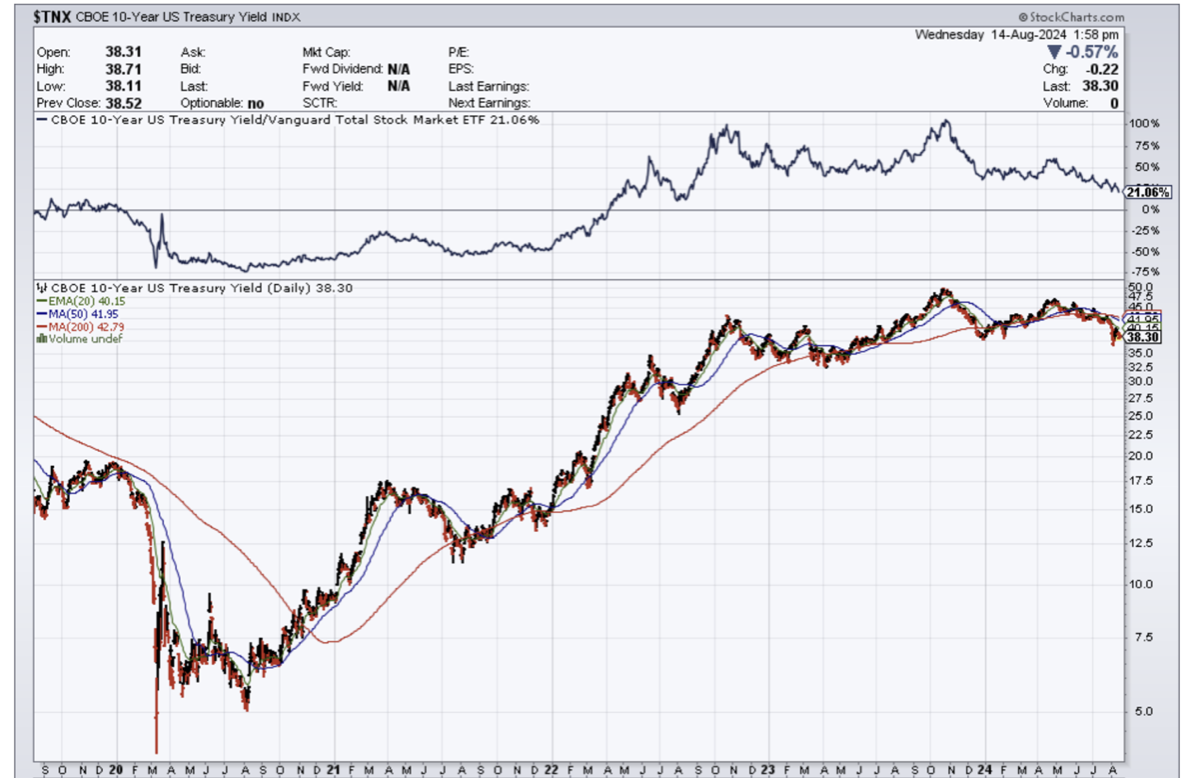

Mad Hedge Technology Letter

August 14, 2024

Fiat Lux

Featured Trade:

(POSITIVE SIGNAL FOR THE TECH RALLY)

($COMPQ), ($TNX)

We received highly bullish news from the fiscal policy side today.

Conditions are everything in the short-term which is why macro events sometimes steal the whole show by destroying or propping up market sentiment.

Scare events can shock investors and become the impetus to take profits to protect capital.

Fortunately, the data from the CPI index has most likely given the green light for the US Central Bank to officially initiate its easing cycle next month.

My guess is that Fed Governor Jerome Powell cuts by 25 basis points and it could turn out to be a hawkish cut.

This is massively bullish for tech stocks ($COMPQ) leading up to the next earnings report in October.

This sets the backdrop for tech stocks to motor towards the upper left in upcoming months.

Lower rates ($TNX) translate into lower costs of capital for tech stocks to borrow money for paying stuff like salaries, software, and hardware.

The high-rate environment has translated into a dearth of companies going public and has stifled the creative juices at the formative stages of Silicon Valley.

That last jobs report offered new signs of a cooling labor market, which stoked fears that the Fed may have waited too long to start lowering interest rates after keeping them at a 23-year high for the last year.

A milder inflation reading released Wednesday removes one of the last hurdles the Federal Reserve needed to clear before cutting rates in September.

The Consumer Price Index (CPI) increased 2.9% over the prior year in July, down from June's 3% annual gain in prices. On a "core" basis, which strips out the more volatile costs of food and gas, prices in July climbed 3.2% over last year — down from 3.3% in June. That was the smallest increase since April 2021.

The new numbers are the latest confirmation that inflation is in fact dropping off a cliff after heating back up during the first quarter of the year, a development that prompted the Fed to warn at one point that rates would likely stay higher for longer.

Fed Chair Jerome Powell made it clear at the end of last month that a cut in September was “on the table” as long as the data supported it. He and other policymakers have said they want to be sure that inflation is in fact moving “sustainably” down to their 2% goal.

Tech stocks have positively correlated with interest yields since 2020, which is counterintuitive.

What this really means is that the growth rate of tech has overpowered the 5% Fed Funds rate which is quite impressive.

That high rate was supposed to pummel tech stocks and that fear-mongering failed to materialize.

No doubt the AI boom delivered a helping hand to tech shares as well.

Tech stocks were one of the few sectors in the public market that remained attractive in the face of aggressive rate hikes.

With the Fed almost to the point of reversing hawkish policy, I do believe it is “all systems go” for tech stocks in the short-term and this removes yet another possible black swan event off the table.

I am bullish on tech shares in the short-term.

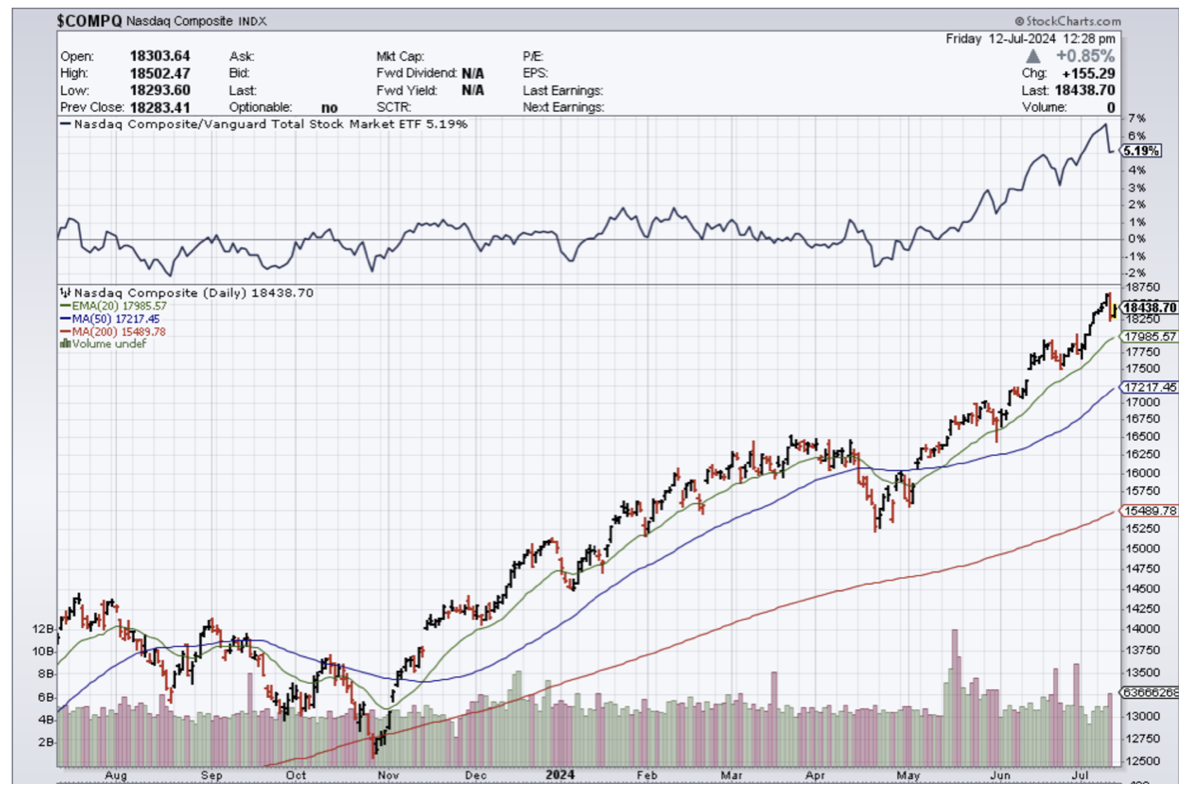

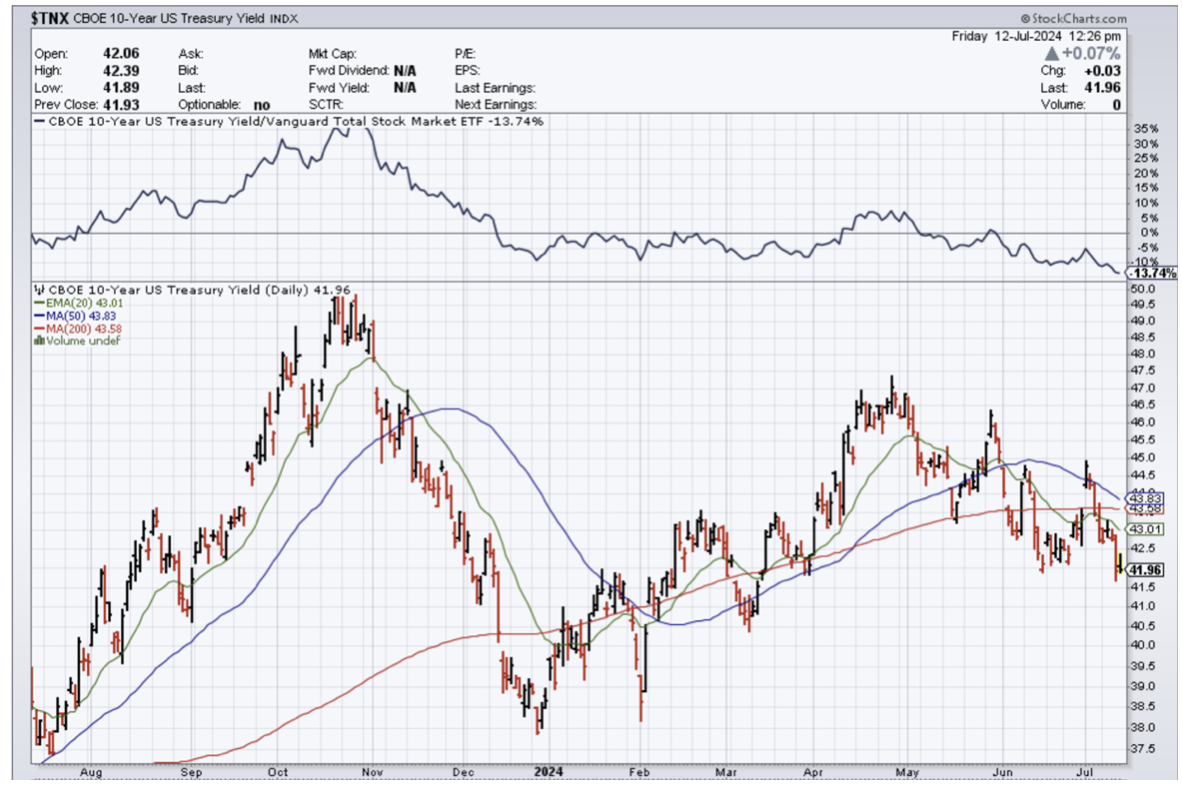

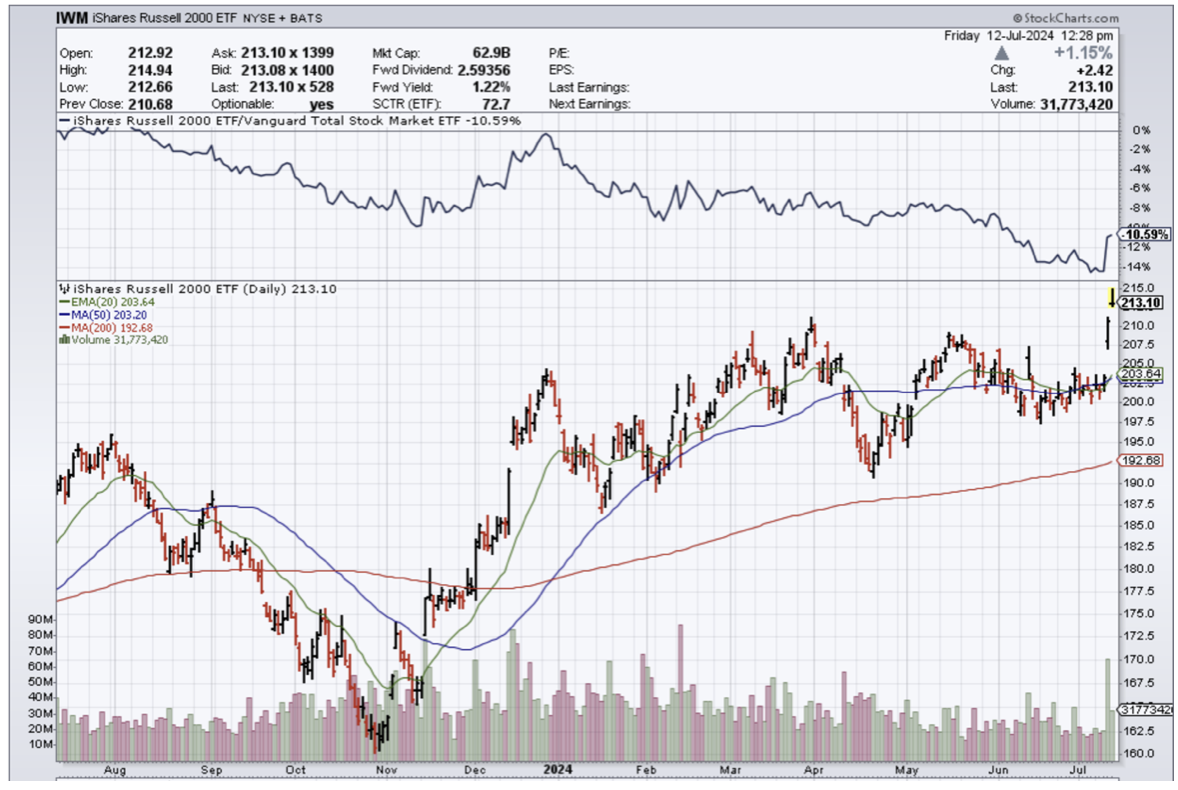

Mad Hedge Technology Letter

July 12, 2024

Fiat Lux

Featured Trade:

(ROTATION HITS THE TECH SECTOR)

($COMPQ), ($TNX), (IWM)

Bond yields ($TNX) diving and the market pricing in a 25 basis point rate cut in September surely translates into another swift leg up in tech stocks ($COMPQ), right?

Hold your horses.

The price action resulted in the exact opposite with big names like Tesla down over 4%.

It was ugly but orderly which is a victory and not of the pyrrhic sort.

The sharp selloff stemmed from a lower-than-expected CPI number.

Decreasing CPI is a strong signal that price inflation is coming down and that is highly conducive to higher stock prices.

However, every inflation report reflecting lower inflation doesn’t guarantee tech stocks in unison will go up.

Tech stocks have done exceptionally well during a backdrop of high rates and high inflation which is extremely unusual.

The market took this opportunity to rotate out of tech and into cheaper stocks that look to benefit more from lower rates.

That’s not saying that tech stocks don’t benefit from lower rates, they certainly do, but the best of the rest has been so beaten down behind the woodshed during this higher rate story that many companies have been on life support and are due for a quick bounce.

The bounce, however, could be short-lived and the bounce could also be given back swiftly.

I suspect a temporary slowdown of tech stocks for the moment will take place while beaten-down sectors get their 15 minutes of fame before they disappear into the background.

I do believe once this short event has worked itself through the system, tech will be off to the races again.

It’s hard to keep tech stocks down because nothing of note has and looks like toppling them.

Presiding over iron-clad balance sheets with Teflon business models and wielding cash cows is the secret recipe to success.

The worst-performing sector in 2024 — real estate — had its best day this year. The Russell 2000 (IWM) climbed 3.6% — the most since November.

US inflation cooled broadly in June to the slowest pace since 2021 on the back of a long-awaited slowdown in housing costs, sending the strongest signal yet that the Fed can cut interest rates soon.

I find this rotation highly beneficial for the overall health of the stock market and it is honestly about time.

Higher rates were starting to turn the screws on many smaller companies.

Many have been in survival mode forcing management into maneuvers like cutting staff, doubling up workloads, trimming expenses, and reducing prices for products.

I do believe that this scarcity mentality will come to an end and this does give more room for other tech companies other than the Magnificent 7 to overperform.

To be honest, the over-reliance on 7 tech stocks to power the tech market is getting a little long in the tooth, and the narrow concentration of alpha is highly irregular and negative for the long-term sustainability of the tech sector.

I would tell readers to get your gunpowder ready because we are setting up for an optimal entry point into tech stocks for the next leg up.

Just be patient.