Global Market Comments

September 29, 2025 Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOVERNMENT SHUTDOWN IS HERE)

(SPY), ($INDU), (IWM), (V), (MA), (AXP), (UNG),

(CCJ) (XOM), (OXY) (DUK) (TAN), (FSLR)

Below, please find subscribers’ Q&A for the April 30 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q:Why is the Australian dollar not moving against the US dollar as much as the other currencies?

A: Australia is too closely tied to the Chinese economy (FXI), which is now weak. When the Chinese economy slows, Australia slows. Australia is basically a call option on the Chinese economy. So they're not getting the ballistic moves that we've seen in, say, the Euro and the British pound, which are up about 20%. Live by the sword, die by the sword. If you rely on China as your largest customer for your export commodities, you have to take the good and the bad.

Q: I see we had a terrible GDP print on the economy this morning, down 0.3%. When are we officially in a recession?

A: Well, the classical definition of a recession is two back-to-back quarters of negative GDP growth. We now have one in the bank. One to go. And this quarter is almost certain to be much worse than the last quarter, because the tariffs basically brought all international trade to a complete halt. On top of that, you have all of the damage to the economy done by the DOGE cuts in government spending. Approximately 80% of the US states, mostly in the Midwest and South,are very highly dependent on Washington spending for a healthy economy, and they are going to really get hit hard. So the question now is not “do we get a recession?”, but “how long and how deep will it be?” Two quarters, three quarters, four quarters? We have no idea. Even if trade deals do get negotiated, those usually take years to complete and even longer to implement. It just leaves a giant question mark over the economy in the meantime.

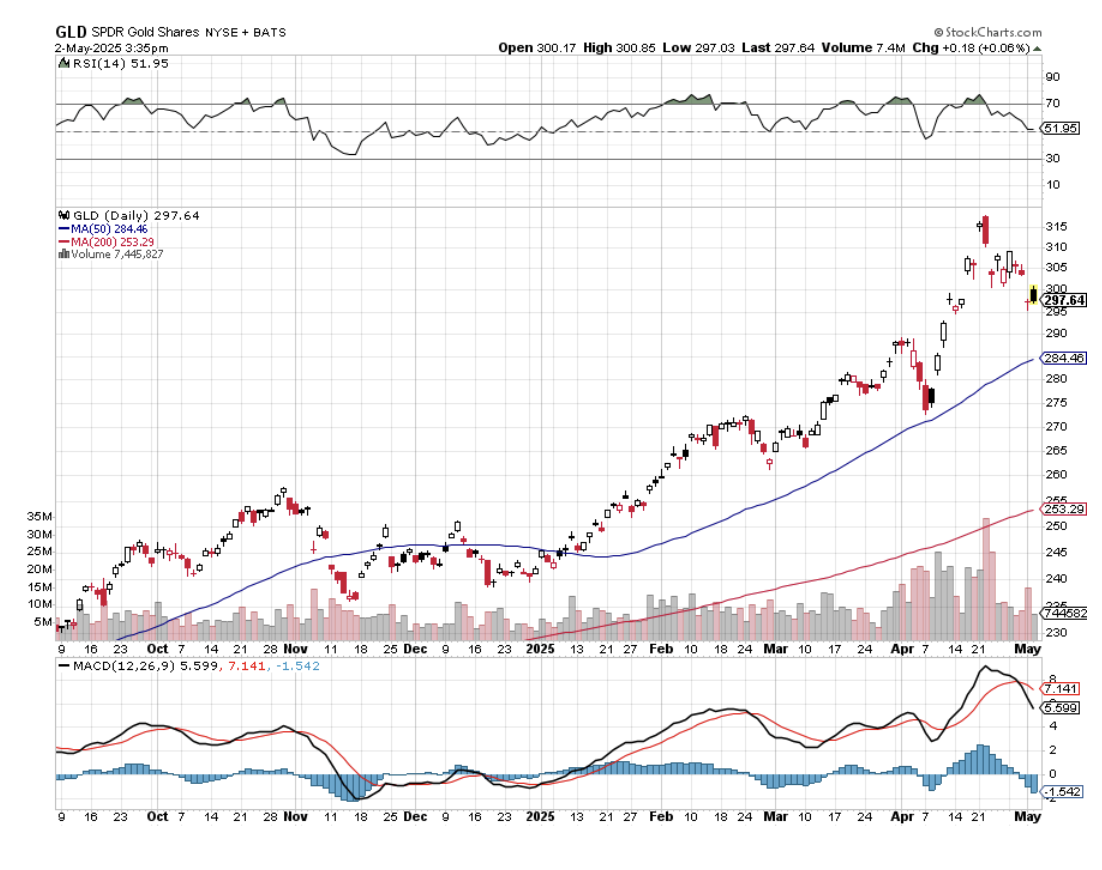

Q: Is SPDR Gold Trust (GLD) the best way to play gold, or is physical better?

A: I always go for the (GLD) because you get 24-hour settlement and free custody. With physical gold, you have to take delivery, shipping is expensive, and insurance is more expensive. Plus, then you have to put it in a vault. Private vaults have a bad habit of going bankrupt and disappearing with your gold. You keep it in the house, and then if the house burns down, all your gold is gone there. Plus, it can get stolen. There's also a very wide dealing spread between bid and offer on physical gold coins or bars; usually it's at least 10%, often more. So I often prefer the ease of trading with the GLD, which owns futures on physical gold, which is held in London, England. So that is my call on that.

Q: Is ProShares Ultra Silver (AGQ) the leveraged silver play?

A: It absolutely is, but beware: (AGQ) is only good for short, sharp rises because the contango and the storage operating costs of any 2x are very, very high—like 10% a year. So, good if you're doing a day trade, not good for a one-year hold. Then you're just better off buying silver (SLV).

Q: What is more important with the Fed's mandate—unemployment or fear of inflation?

A: That's an easy one. Historically, the number one priority at the Fed has been inflation. That is their job to maintain the full faith and credit of the U.S. Dollar, and inflation erodes the value, or at least the purchasing power of the US dollar, so that has always historically been the priority. Until we see inflation figures fall, I think the chance of them cutting interest rates is zero, and we may not see actual falls until the end of the year, because the next influence on prices is up because of the trade war. The trade war is raising prices everywhere, all at the same time. So that will at least add 1 or 2% to inflation first before it starts to fall. You can imagine how if we get a 6% inflation rate, there's no way in the world the Fed can cut rates, at least for a year, until we get a new Fed governor. So that has always historically been the priority.

Q: Do you think the 10-year yield is going down to 5%?

A: You know, we're really in a no-man's-land here. Recession fears will drive rates down as they did yesterday. I haven't even had a chance to see where the bond market is this morning because. So, rates are rising on a recessionary GDP, which is the worst possible outcome. Rates should be falling on a recessionary GDP print. Of course, Washington’s efforts to undermine the U.S. dollar aren't helping. Threatening to withhold taxes on interest payments to foreign owners is what caused the 10% down move in bonds in one week—the worst move in the bond market in 25 years. So, the mere fact that they're even thinking about doing something like that scares foreign investors, not only from the bond market, but all US investments period. And certainly, we've seen some absolutely massive stock selling from them.

Q: Why won't the market go down to 4,000 in the S&P 500?

A: Absolutely, it could; that is definitely within range. That would put us down 30% from the February highs, it just depends on how long the recession lasts. If you just get a two-quarter shallow recession, we could bounce off 4800 for the (SPX) until we come out. If the recession continues for several quarters, and it's looking like it will, then 4,000 is definitely within range. So, it's all about the economy. And remember, stocks are expensive. They don't get cheap until we get a PE multiple of 16, and even then, that alone, just a multiple shrinkage would take us down to 4,000.

Q: Would it be a good idea to buy the S&P 500 (SPY) as it falls?

A: I'm getting emails from readers asking if it's time to buy Nvidia (NVDA) or time to buy Tesla (TSLA). What I've noticed is that investors are constantly fighting the last battle. They're always looking for what worked last time, and that does not succeed as an investment strategy. As long as I'm selling rallies, I'm not even thinking about what to buy on the bottom. The world could look completely different on the other side. The MAG-7 may not be the leadership in the future, especially with the Trump administration trying to dismantle four out of seven companies through antitrust, and the rest are tied up in the trade wars. So, tech is still expensive relative to the main market, and we're going to need to look for new leaders. My picks are going to be mining shares, gold, and banking. Those are the ones I'm looking to buy on dips, but right now, cash is king unless you want to play on the short side. Being paid 4.3% to stay away sounds pretty good to me, especially when your neighbors have 30% losses. You know, I've heard of people having all of their retirement funds in just two stocks: Nvidia and Tesla, and they're getting wiped out. So, you don't want to become one of them.

Q: After a tremendous run in Gold, is Silver a better risk-reward right now?

A: I would say yes, it is. Silver has been lagging gold all year because central banks, the most consistent buyers for the past decade,buy gold—they don't buy silver. But what we may be in store for here now is a prolonged sideways move in gold while the technicals catch up with it. And in the meantime, the money goes elsewhere into silver and Bitcoin. That's my bet.

Q: Is Apple (APPL) a no-touch now?

A: I’d say yes. The trade war is changing by the day, and Apple probably does more international trade than any other company in the world. Also, Apple gets hit with recessions like everybody else. There was a big front run to buy Apple products ahead of tariffs—my company bought all its computer and telephone needs for the whole year ahead of the tariffs. We're not buying anything else this year. And I would imagine millions more are planning to do the same, so you could get some really big hits in Apple earnings going forward.

Q: Should I sell my August Proshares Short S&P 500 (SH) LEAPS?

A: No, I would keep them. If the (SPX) IS trading between 5,000 to 5,800, your $4-$42 SH LEAPS should expire at max profit in August, so I'm hanging on to mine. Next time we take a run at 5,000, you should be able to get out of your SH LEAPS at 80% to 90% of the max profit.

Q: What car company stock will do the best in a high-tariff global economy?

A: Tesla (TSLA), because 100% of their cars are made in the US with 90% US parts (the screens come from Panasonic in Japan). Their foreign components are only about 10%, so they can eat that. For General Motors (GM), it's more like 30% of all components are made abroad, and they can't eat that; their profit margins are too low. (GM) expects to lose $5 billion because of tariffs. By the way, the profit margins on Tesla have fallen dramatically from 30% down to 10% in two years, so it's not like they're in great shape either. Also, Tesla hasn’t had a CEO for ten months, which is why the board is looking for a replacement.

Q: Is it a good time to buy the dip in oil (USO)?

A: Absolutely not. Oil is the most sensitive sector to recessions, because if you can't sell oil, you have to store it, very expensively. It costs 30 to 40% a year to store oil—that's the contango; and once all the storage is full, then you have to cap wells, which then damages the long-term production of the wells. I think at some point you will expect an announcement from Washington to refill the Strategic Petroleum Reserve, which was basically sold by Biden at $100 a barrel. You can now get it back for $60. That may not be a bad idea if you're going to have a strategic petroleum reserve. What's better is just to quit using oil completely, which we were on trend to do.

Q: Will interest rates drop by year-end?

A: They may drop by year-end once unemployment runs up to 5% or 6% —which is likely to happen in a recession—and inflation starts to decline, even if it declines from a higher level. Even if they don't cut by year end, they'll still cut in a year when the president can appoint a new Fed governor. What the Trump really needs to do is appoint Janet Yellen as the Fed governor. She kept interest rates near zero for practically all of her term. We need another Yellen monetary policy.

Q: The job market here seems to be slowing quite fast. Is there any way this will rebound and stave off recession?

A: No, there is not. Companies are going to be looking to cut costs as fast as they can to offset the shrinkage in sales, but also to help cope with tariffs. So no, the job market is actually surprisingly strong now. That means future data releases are probably going to get a lot worse. In April, we saw job gains in Health care, adding 51,000 jobs. Other sectors posting gains included transportation and warehousing (29,000), financial activities (14,000), and social assistance. I highly doubt any of these sectors will show gains next month.

Q: What about nuclear energy plays?

A: I like them, partly because people are buying stocks like Cameco Corp (CCJ) as a flight to safety commodity play, like they're buying gold, silver, and copper. But also, this administration is supposed to be deregulation-friendly, and the only thing holding back nuclear (at least new modular reactors) is regulation. That and the fact that no one wants to live next door to a nuclear power plant, for some strange reason.

Q: What do I think about natural gas (UNG)?

A: Don't touch. Don't buy the dip. All energy plays look terrible right here, going into recession.

Q: What are your thoughts on manufacturing returning to the U.S? And how will that affect the stock market?

A:I think there's zero chance that any manufacturing returns to the U.S. Companies would rather just shut down than operate money-losing businesses. You know, if your labor cost goes from $5 to $75 an hour, there's no chance anyone can make money doing that, and no shareholders are going to want to touch that stock. That is the basic flaw in having a government where no one is actually running a manufacturing business anywhere in the government. They don't know how things are actually made. They're all real estate or financial people.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have a comfortable seat next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini can navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

Chicago’s Union Station

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way, like Omaha, Salt Lake City, and Reno, to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my favorite photos from the trip below, although there is only so much you can do from a moving train and an iPhone 16 Pro.

Somewhere in Iowa

The Thumbnail Portfolio

Equities – buy dips, but sell rallies too Bonds – avoid Foreign Currencies – avoid Commodities – avoid Precious Metals – avoid Energy – avoid Real Estate – avoid

1) The Economy – Cooling

I expect a modest 2.0% real GDP growth with a 4.0% inflation rate, giving an unadjusted shrinkage of the economy of negative -2% for 2025. That is down from 0% in in 2024. This may sound discouraging, but believe me, this is the optimistic view. Some of my hedge fund buddies are expecting a zero return over the next four years.

Virtually all independent economists expect the new administration's economic policies will be a drag on both the US and global economies. Trade wars are bad for everyone. When your customers are impoverished, your own business turns south. This is a big deal, since the Magnificent Seven, which accounted for 70% of stock market gains last year, get 60% of their profits from abroad.

The ballooning National Debt is another concern. The last time Trump was in office, he added $10 trillion to the deficit through aggressive tax cuts and spending increases. If this time, he adds another $10-$15 trillion, the National Debt could reach $50 trillion by 2030.

There are two issues here. For a start, Trump will find it a lot harder and more expensive to fund a National Debt at $50 trillion than $20 trillion. Second, borrowing of this unprecedented magnitude, double US GDP, will send interest rates soaring, causing a recession.

The only question then is whether this will be a pandemic-style recession, which took stocks down 30% and recovered quickly, or a 2008 recession which demolished stocks by 52% and dragged on for years.

Hope for the best but expect the worst, unless you want to consider a future career as an Uber driver.

The outlook for stocks for 2025 is pretty simple. You are going to have to work twice as hard to make half the money you did last year with twice the volatility. You will not be able to be as nowhere near aggressive in 2025 as you were in 2024It’s a dream scenario for somebody like me. For you, I’m not so sure.

It’s not that US companies aren't growing gangbusters. I expect 2% GDP growth, 15% profit growth, and 12% net margin growth in 2025. But let’s face reality. Stocks are the most expensive they have been in 17 years and we know what happened after 2008. Much of the stock market gain achieved last year was through hefty multiple expansions. This is not good.

Big tech companies might be able to deliver 20% gains and are still the lead sector for the market. Normally that should deliver you a 15%, or $800 gain in the S&P 500 (SPX). We might be able to capture this in the first half of 2025.

Financials will remain the sector with the best risk/reward, and I mean the broader definition of the term, including banks, brokers, money managers, and some small-cap regional banks. The reason is very simple. Their income statements will get juiced at both ends as revenues soar and costs plunge, thanks to deregulation.

No passage of new laws is required to achieve this, just a failure to enforce existing ones. The hint for this is a new SEC chair whose primary interest is promoting the Bitcoin bubble. Buy (GS), (MS), (JPM), (BAC), (C), and (BLK).

However, this is anything but a normal year. Uncertainty is at an eight-year high, thanks to an incoming administration. If the promised policies are delivered, inflation will soar and interest rates will rise, as they already have. We could lose half or all of our stock market gains by the end of 2025.

The big “tell” for this was the awful market performance in December, down 5%. The Dow Average was down ten days in a row for the first time in 70 years. Santa Claus was unceremoniously sent packing. People Are clearly nervous. But then they should be with a bull market that is approaching a decrepit five years in age.

There is a bullish scenario out there and that has Trump doing absolutely nothing in 2025, either because he is unwilling or unable to take action. After all, if the economy isn’t actually broken, why fix it? Better yet, if you own an economy it is better not to break it in the first place.

Nothing substantial can pass Congress with a minuscule one-seat majority in the House of Representatives. There will be no new presidential action through tariffs and only a few token, highly televised deportations, not enough to affect the labor market.

Stocks will not only hold, but they may add to the 15% first-half gains for the year. I give this scenario maybe a 50% probability.

The first indication this is happening is when the presidential characterization of the economy flips in a few months from the world’s worst to the world’s best with no actual change in the numbers. Trump will take all the credit.

You heard it here first.

Frozen Headwaters of the Colorado River

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD) Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, or dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites returned home by train because their religion forbade travel by automobiles or airplanes.

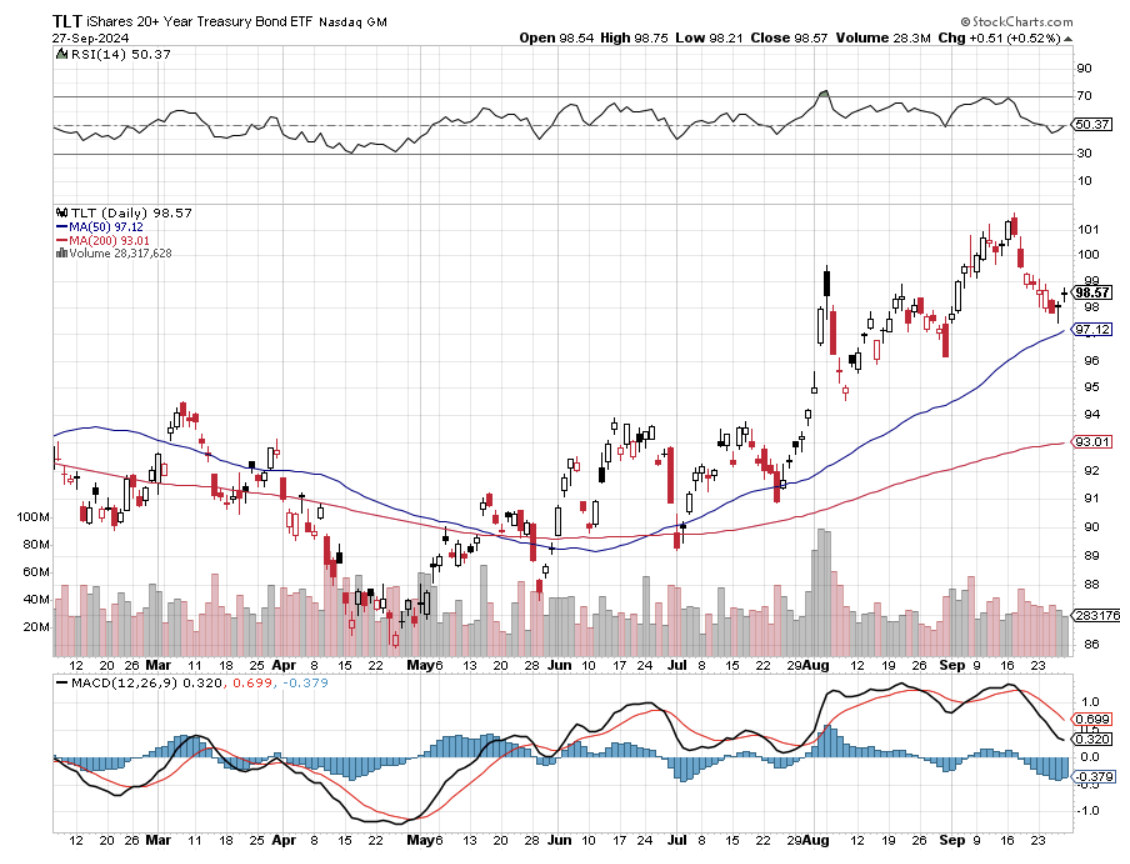

The big question to ask here after a 100-basis point rise in bond yields in only three months is whether the (TLT) has suffered enough. The short answer is no, not quite yet, but we’re getting close. Fear of Trump policies should eventually take ten-year US Treasury bond yields to 5.00%, and then we will be ready for a pause at a nine-month bottom. After that, it depends on how history unfolds.

If Trump gets everything he wants, inflation will soar, bonds will crash, and 5.00% will be just a pit stop on the way to 6.00%, 7.00%, and who knows what? On the other hand, if Trump gets nothing he says he wants, then both bonds stocks and bonds will rise, creating a Goldilocks scenario for all balanced portfolios and investors.

That also sets up a sweet spot for entry into (TLT) call spreads close to 5.00% yields. A politician campaigning on one policy, then doing the opposite once elected? Stranger things have happened. The black swans will live.

If your basic assumption for interest rates is that they stay flat or rise, then you have to love the US dollar. Currencies are all about expected interest rate differentials and money always pours into the highest-paying ones. Tariffs will add fat to the fire because any reduction in international trade automatically reduces American trade deficits and is therefore pro-dollar.

This means that you should avoid all foreign currency plays like the plague, including the Euro (FXE), Japanese yen (FXY), British Pound (FXB), Canadian dollar (FXE), and Australian dollar (FXA).

A strong greenback comes with pluses and minuses. It makes our exports expensive and less competitive and therefore creates another drag on the economy. It demolishes traditional weak dollar plays like emerging markets and precious metals. On the other hand, it attracts substantial foreign investments into US stocks and bonds, which has been continuing for the past decade.

Above all, be happy you are paid in US dollars. My foreign clients are getting crushed in an increasingly expensive world.

5) Commodities (FCX), (BHP), (RIO), (VALE), (DBA) Look at the chart of any commodity stock and you see grim death. Freeport McMoRan (FCX), BHP (BHP), and Rio Tinto (RIO), they’re all the same. They’re all afflicted with the same disease, over-dependence on a robustly growing China, which isn’t growing robustly, if at all.

I firmly believe that this will continue until the current leadership by President Xi Zheng Ping ends. He has spent the last decade globally expanding Chinese interests, engaging in abusive trade practices, hacking, and attacking American allies like Taiwan and the Philippines.You can only wave a red flag in front of the US before it comes back to bite you. A trade war with the US is now imminent.

This will happen sooner than later. The Chinese people don’t like being poor for very long. This is why I didn’t get sucked in on the Chinese long side in the fall, as many hedge funds did.

If China wants to go back to playing nice, as they did in the eighties and nineties, China should return to return to high growth and commodities will look like great “Buys” down here. If they don’t, American growth alone should eventually pull commodities up, as our economy is now growing at a long-term average gross unadjusted 6.00% rate. So the question is how long this takes.

It may pay to start nibbling on the best quality bombed-out names now, like those above.

Snow Angel on the Continental Divide

6) Energy (DIG), (USO), (DUG), (UNG), (USO), (XLE), (LNG), (CCJ), (VST), (SMR) Energy was one of the worst-performing sectors in the market for the second year in a row and 2025 is looking no better. New supplies are surging, while demand remains stuck in the mud, with the US now producing an incredible 13.5 million barrels a day. OPEC is dead.

EVs now make up 10% of the US auto fleet, and much more in other countries, are making a big dent. Some 50% of all new car sales in China, the world’s largest market, are EVs. The number of barrels of oil needed to increase a unit of American GDP is plunging, as it has done for 25 years, through increased efficiencies. Remember your old Lincoln Continental that used to get eight miles per gallon? Now it gets 27.

Worse yet, a major black swan hovers over the sector. If the Ukraine War somehow ends, some ten million barrels a day of Russian oil will hit the market. Oil prices should plunge to $50 a barrel.

There are always exceptions to the rule, and energy plays not dependent on the price of oil would be a good one. So is natural gas, which will benefit from Cheniere Energy’s (LNG) third export terminal coming online, increasing exports to China. Ukraine cutting off Russian gas flowing to Europe will assure there is plenty of new demand.

But I prefer investing in sectors that have tailwinds and not headwinds. Better leave energy to the pros who have the inside information they need to make money here.

If someone is holding a gun to your head tell you that you MUST invest in energy, go for the new nuclear plays like (CCJ), (VST), and (SMR). We are only at the becoming of the small modular reactor trend, which could accelerate for decades.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side. In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year. We also see countless abandoned 19th-century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

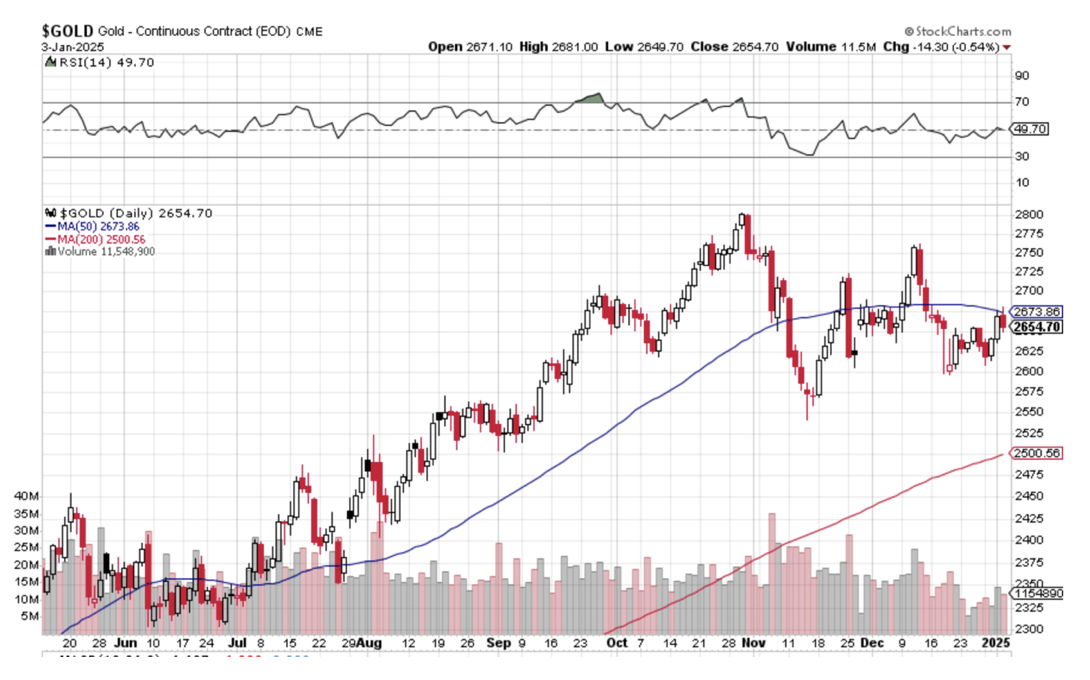

We certainly got a terrific run on precious metals in 2025, with gold at its highs up 33% and silver up 65%. The miners did even better. Even after the post-election selloff, it was still one of the best-performing asset classes of the year.

But the heat has definitely gone out of this trade. The prospect of higher interest rates for longer in 2025 has sent short-term traders elsewhere. That’s because the opportunity cost of owning precious metals is rising since they pay no interest rates or dividends. And let’s face it, there was definitely new competition for hot money from crypto, which doubled after the election.

The sector is not dead, it is resting. Central bank buying of the barbarous relic continues unabated, especially among sanctioned countries, like Russia and China. Gold is still the principal savings vehicle for many Chinese. They are not going to recover confidence in their own currency, banks, or government anytime soon. And there is still slow but steadily rising industrial demand from solar sectors.

Gold supply has also been falling for years, while costs are rising at least at double the headline inflation rate. So it’s just a matter of time before the supply/demand balance comes back in our favor. Where the final bottom is anyone’s guess as gold lacks the traditional valuation parameters of other asset classes, like dividends or interest paid. We’ll just have to wait for Mr. Market to tell us, who is always right.

Give (GLD), (SLV), (GDX), (GOLD), and (WPM) a rest for now but I’ll be back.

Crossing the Great Nevada Desert Near Area 51

8) Real Estate (ITB), (LEN), (KBH), (PHM), (DHI)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada. It is a route long traversed by roving bands of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley, California. Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Real estate was a nice earner for us in 2024 in the new homes sector. The election promptly demolished this trade with the prospect of higher interest rates for longer. Expect this unwelcome drag to continue in 2025.

I am not expecting a housing crash unless interest rates take off. More likely it will continue to grind sideways on low volume. That’s because the market has support from a structural shortage of 10 million homes in the US, the debris left over from the 2008 housing crash. That’s why there is still a Millennial living in your basement. Homebuilders now prioritize profit margins over market share.

I expect this sector to come back someday. New homebuilders have the advantage of offering free upgrades and discounted in-house financing. Avoid for now (DHI), (KBH), (TOL), and (PHM).

Crossing the Bridge to Home Sweet Home

9) Postscript We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff have made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been cooling in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 80 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just coming into view across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro, iPad, and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak tonight and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2025!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2025!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Zephyr.jpg342451april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-01-08 09:00:172025-02-20 12:40:412025 Annual Asset Class Review

Global Market Comments

September 30, 2024 Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or CHINA IS BACK! plus MY ENCOUNTER WITH ALIENS),

(GLD), (CCJ), (NEM), (TSLA), TLT), (DHI), (FXI), (BIDU), (TNE)

(USO), (BTU), (UNG), (CORN), (WEAT), (SOYB), (LVS), (WYNN) (LVUY) (HESAF)

There are always many unintended consequences to any Fed move, such as the 50-basis point interest rate cut on September 18. This time, a big one is that China would match and then exceed our own central bank’s move with a blockbuster stimulus package of their own. China has finally reached the “whatever it takes” moment, and the programs are squarely aimed at stimulating consumption.

You will hear from the talking heads on TV that the package is inadequate, a weak effort, an hour late, and a Yuan short, and will fail. But China has massive resources and will follow up with a second, larger package if they need to.

For a start, they own $860 billion worth of our US Treasury bonds, more than any foreign country, and unimaginable amounts of rapidly appreciating gold (GLD), which they have been accumulating since it was $1,020 an ounce (it is now $2,600).

China really pulled out all the stops on this one. The People's Bank of China on Wednesday cut its medium-term lending facility -- the interest for one-year loans to financial institutions -- from 2.3% to 2.0%, the lowest since 2020. The rate cuts are going to bring $140 billion in new lending.

They reduced deposits for new investment property purchases to 10% in a move clearly aimed at resuscitating their moribund real estate market. For the first time ever, they are handing out cash payments to poor people. It is the most stimulus since Covid.

China is not to be taken lightly.

Certainly, the stock market is buying it….at least for now. The main China ETF, the (FXI) had its best week in history, up 20%. Most of this was short covering. The short interest in the leading Chinese stocks like Alibaba (BABA), Baidu (BIDU), and Tencent Music Holdings (TNE) was running close to an eye-popping 50%.

So, why bother with a country half the size of our own, where the writing looks like chicken scratching, and the food has way too much MSG? Because the Middle Kingdom is the largest buyer of almost everything, including oil (USO), coal (BTU), natural gas (UNG), corn (CORN), wheat (WEAT), and soybeans (SOYB), most of which is supplied by the United States.

So, have I been burying you with China-oriented trade alerts this week? No, not really. First of all, I never buy on top of a 20% move in five days. It just goes against my bargain-hunting character. More importantly, the best China plays are here in the US. You can start with all of the ticker symbols I listed above.

There are also quite a few indirect China plays available in the West. Notice that the casinos Las Vegas Sands (LVS) and Wynn Resorts (WYNN) are up 20% across the board. The luxury stocks like LVMH Moet Hennessy (LVUY) and Hermes International (HESAF) also saw monster moves.

Dare I say it? Buy China on dips, especially blue-chip names like Alibaba (BABA) and Baidu (BIDU). If this Beijing stimulus fails, they’ll probably follow up with another one.

And what do newly enriched Chinese consumers do? They buy more gold. In fact, the gold story keeps getting better the higher it goes.

Another gold positive is the US National Debt, now at $35 trillion. Whichever candidate wins the presidential election, the national debt will keep rising, either by $500 billion a year or $2.5 trillion. Foreigners seem more worried about our debt than we are and are finding any non-dollar asset more attractive by the day. Gold is at the very top of that list.

It turns out that in a world of falling interest rates, a declining dollar, and fading faith in financial institutions, quite a few Americans like gold as well. Hey, Costco (CSCO) is selling it. How bad can it be?

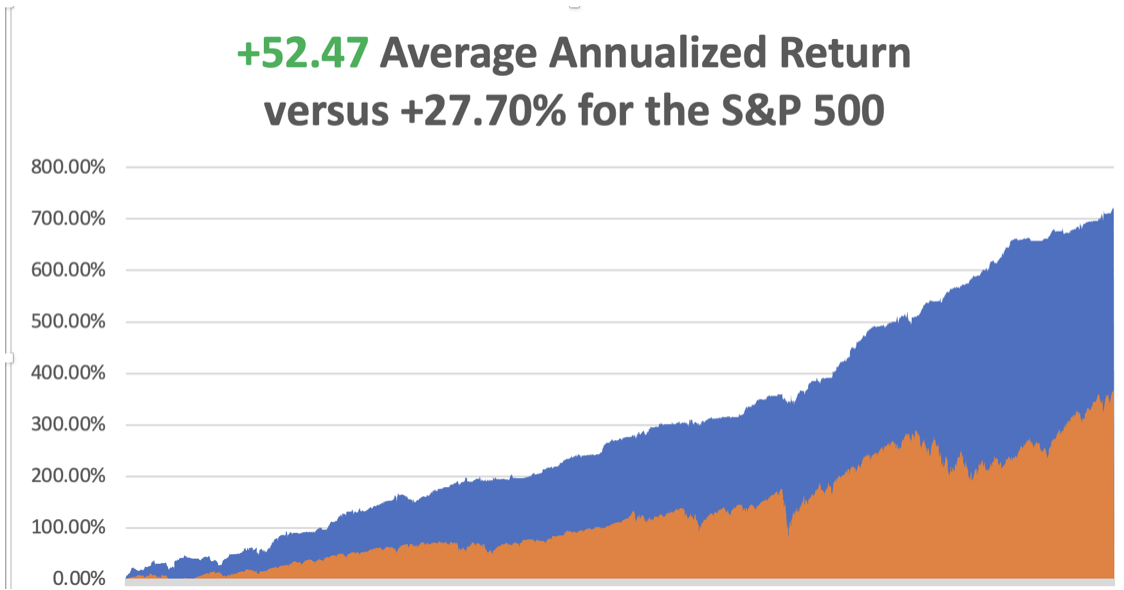

So far in September, we are up by a spectacular +9.54%. My 2024 year-to-date performance is at +44.23%.The S&P 500 (SPY) is up +20.33%so far in 2024. My trailing one-year return reached +62.87%. That brings my 16-year total return to +720.86%.My average annualized return has recovered to +52.47%.

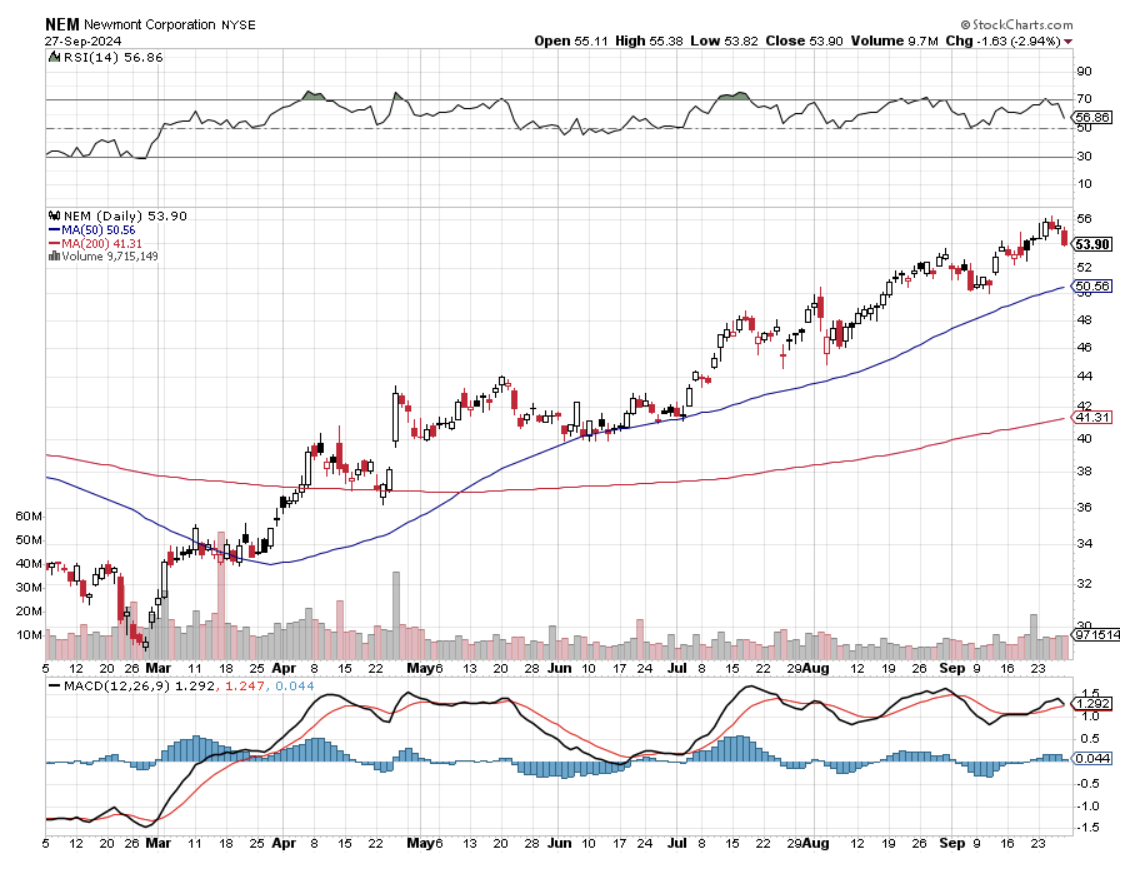

Last week was mostly about running existing successful long positions. Those would include (CCJ), (NEM), (TLT), (TSLA), and (DHI). I have one short position in (TLT).

I did add a (TLT) call spread, taking advantage of a rapid $4 dip. I also increased my Tesla (TSLA) long to a double, believing that the stock will keep running into the October 10 Robotaxi announcement.

Some 63 of my 75 round trips, or 90%, were profitable in 2023. Some 59 of 77 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of +76.62%.

Try beating that anywhere.

Are Markets Melting Up? So thinks my friend Ed Yardeni. The latest policy decision lifted the odds of an “outright melt-up” in equity prices — like during the dot-com bubble when the (SPY) roared 220% from 1995 to the end of the century — to 30% from 20%. Another 50-basis point rate cut might do it. One can only hope.

What Happens When Gold Hits $3,000? It then moves on to $4,400 an ounce. Chinese savers will still have nowhere else to go. The real estate market is still dead, Chinese stocks are moribund, and they don’t trust their own currency. Keep buying (GLD), (NEM), and (GOLD) on dips.

The Core Personal Consumption Expenditures Price Index Falls, to a 2.2% annual rate, much lower than expected. The Federal Reserve’s preferred gauge to measure underlying inflation,rose 0.1% for the month, putting the 12-month inflation rate at 2.2%. Excluding food and energy, core PCE rose 0.1% in August and was up 2.7% from a year ago. The all-items inflation gauge was below Wall Street estimates and the lowest since early 2021.

American China Plays Roar, like commodities plays Freeport McMoRan (FCX), the Copper ETF, COPX), Peabody Energy (BTU), and the Platinum ETF. Indirect plays like the casinos Las Vegas Sands (LVS) and Wynn Resorts (WYNN). Dare I say it? Buy China on dips, like Alibaba (BABA) and Baidu (BIDU). If this Beijing stimulus fails, they’ll probably follow up with another one. Silver is on a Roll, and is finally outperforming gold, as it has historically done. Silver just hit its highest price in more than a decade, and growing demand and falling interest rates mean it could have more room to run.

On Thursday, silver hit $32.43 an ounce, its highest price since 2012. The metal is up 35% so far this year. That beats a 30% rally for gold, which has been trading at all-time highs. Silver is much more sensitive to an industrial recovery than gold. Buy (SLV), (AGQ), (SIL), and (WPM) on dips. Oil Gets Crushed on Saudi Output Burst. After a brief bounce back last week, it looks like oil is in a bearish pattern now that will be hard to break for the next few months. OPEC and its allies have been holding at least 5 million barrels of daily output off the market to prop prices, but they are expected to start bringing back production soon. Saudi Arabia, the strongest member of OPEC in that it has the most capacity to pump oil, is no longer willing to hold back production to try to push the price up to $100 a barrel.

US GDP Revised up to 5.5% Growth, since the second quarter of 2020, when the pandemic began through 2023. It was spurred mainly by bigger consumer-driven growth fueled by robust incomes. The revised figure is compared with a previously published 5.1% advance. You can’t beat America. Electrification is the Latest Hot Investment Theme, seeking to cash in on AI demands on the power grid. Issuer Global X last week filed for its U.S. Electrification ETF, which would track an index of conventional companies in the sector, as well as those involved in alternative or cleaner energy sources — such as wind and solar — and grid infrastructure firms. Fund firm Tema also recently submitted paperwork for an ETF that would invest in companies “tied to global electrification.” These funds could become big winners. US Homes Plunge, down 4.7% in August. Buyers are clearly remaining patient amid steadily declining mortgage rates. New single-family home sales decreased last month to an annualized rate of 716,000 after rising at the fastest pace since early 2022. The median sales price, in the meantime, decreased by 4.6% from a year earlier to $420,600. That marked the seventh straight month of annual price declines, extending what was already the longest streak since 2009 Home Mortgage Rates are in Free Fall, with the 30-year fixed at 6.08% and adjustable well into the fives. Refi activity is also exploding. Expect a real estate boom to ensue. Can Tesla Reach $300? With (TSLA) possibly looking at a great quarter in China, Wall Street pros are rushing to increase their outlooks for the electric vehicle maker’s quarterly sales. At least four analysts have boosted their estimates for Tesla’s third-quarter delivery numbers, which are due next week. All point to signs that sales are starting to pick up in China, a key area for Tesla and a major market for electric cars globally. Vistra Tops Nvidia, as the top S&P 500 stock this year. Vistra is a utility company based in Irving, Tex. that just so happens to be the second-largest owner of independent nuclear plants after buying three nuclear plants in Pennsylvania last year, and these days nuclear power is all the rage. Buy (VST) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 30 at 8:30 AM EST, the Chicago PMI is out On Tuesday, October 1 at 6:00 AM, the JOLTS Job OpeningsReport is released.

On Wednesday, October 2 at 7:30 PM, ADP Employment Change is printed.

On Thursday, October 3 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the ISM Services PMI.

On Friday, October 4 at 8:30 AM, we get the September Nonfarm Payroll Report. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I am often told that I am the most interesting man people ever met, sometimes daily. I had the good fortune to know someone far more interesting than myself.

When I was 14, I decided to start earning merit badges if I was ever going to become an Eagle Scout. I decided to begin with an easy one, Reading Merit Badge, where you only had to read four books and write one review. I loved reading, so “piece of cake”, I thought.

I was directed to Kent Cullers, a high school kid who had been blind since birth. During the late 1940s, the medical community thought it would be a great idea to give newborns pure oxygen. It was months before it was discovered that the procedure caused the clouding of corneas and total blindness in infants.

Kent was one of these kids.

It turned out that everyone in the troop already had Reading Merit Badge and that Kent had exhausted our supply of readers. Fresh meat was needed.

So, I rode my bicycle over to Kent’s house and started reading. It was all science fiction. America’s Space Program ignited a science fiction boom during the early 1960s and writers like Isaac Asimov, Jules Verne, Arthur C. Clark, and H.G. Wells were in huge demand. Star Trek came out the following year, in 1966. That was the year I became an Eagle Scout.

It only took a week for me to blow through the first four books. In the end, I read hundreds of books to Kent. Kent didn’t just listen to me read. He explained the implications of what I was reading (got to watch out for those non-carbon-based life forms).

Having listened to thousands of books on the subject Kent gave me a first class education and I credit him with moving me towards a career in science. Kent is also the reason why I got an 800 SAT score in Math.

When we got tired of reading, we played around with Kent’s radio. His dad was a physicist and had bought him a state-of-the-art high-powered short-wave radio. I always found Kent’s house from the 50 foot tall radio antenna.

That led to another merit badge, one for Radio, where I had to transmit in Morse Code at five words a minute. Kent could do 50. On the badge below the Morse Code says “BSA.” In those days, when you made a new contact, you traded addresses and sent each other postcards.

Kent had postcards with colorful call signs from more than 100 countries plastered all over his wall. One of our regular correspondents was the president of the Palo Alto High School Radio Club, Steve Wozniak, who later went on to co-found Apple (AAPL) with Steve Jobs.

It was a sad day in 1999 when the US Navy retired the Morse Code and replaced it with satellites and digital communication far faster than any human could send. However, it is still used as beacon identifiers at US airfields.

Kent’s great ambition was to become an astronomer. I asked how he would become an astronomer when he couldn’t see anything. He responded that Galileo, the inventor of the telescope, was blind in his later years.

I replied, “Good point”.

Kent went on to get a PhD in Physics from UC Berkeley, no mean accomplishment even for sighted people. He lobbied heavily for the creation of SETI, or the Search for Extra-Terrestrial Intelligence, once an arm of NASA.He became its first director in 1985 and worked there for 20 years.

In the 1987 movie Contact written by Carl Sagan and starring Jodie Foster, the movie was filmed at the Very Large Array in western New Mexico. The algorithms Kent developed there are still in widespread use today. I’ve never been there because I never had the time to drive an hour and a half down a dirt road.

Out here in the West, aliens have been a big deal, ever since that weather balloon crashed in Roswell, New Mexico in 1947. In fact, it was a spy balloon meant to overfly and photograph Russia, but it blew back on the US, thus its top secret status.

When people learn I used to work at Area 51, I am constantly asked if I have seen any spaceships. The road there, Nevada State Route 375, is called the Extra Terrestrial Highway. Who says we don’t have a sense of humor in Nevada?

After devoting his entire life to searching, Kent gave me the inside story on searching for aliens. We will never meet them but we will talk to them. That’s because the acceleration needed to get to a high enough speed to reach outer space would tear apart a human body. On the other hand, radio waves travel effortlessly at the speed of light.

Sadly, Kent passed away in 2021 at the age of 72. Kent, ever the optimist, had his body cryogenically frozen in Hawaii where he will remain until the technology evolves to wake him up. Minor planet 35056 Cullers is named in his honor.

There are no movies being made about my life…. yet. But there are a couple of scripts out there under development.

Watch this space.

Dr. Kent Cullers

New Mexico Very Large Array

Reading Merit Badge

Radio Merit Badge

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/kent-cullers.jpg300480april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-30 09:02:252024-09-30 11:22:40The Market Outlook for the Week Ahead, or China is Back!

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BEST WEEK OF THE YEAR),

(PANW), (NVDA), (LNG), (UNG), (FCX), (TLT), (XOM), (AAPL), (GOOG), (MSTR), (BA), (FXY)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.