Global Market Comments

November 20, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT WAS)

(SPY), (TLT), (JNK), (NLY) (BA), (UUP),

(TLT), (FCX), (GLD), (GDX), (GOLD)

Global Market Comments

November 20, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT WAS)

(SPY), (TLT), (JNK), (NLY) (BA), (UUP),

(TLT), (FCX), (GLD), (GDX), (GOLD)

In the long history of stock markets, last week will be viewed as one of the pivotal ones of the 21st century. That was when investors flipped from anticipating the end of interest rate rises to the beginning of interest rate cuts.

That is a big deal.

I have been anticipating this for months, putting all my chips on the most interest rate-sensitive sectors: US Treasury bonds (TLT), Junk bonds (JNK), REITS (NLY), and big tech. The payoff has been huge, with some followers calling me up daily with literal tears of joy. They have just made the most money in their lives.

November has been the best month of the year, up 10% from the October low, and it's only half over.

And here is the good news. We are not only in the first inning of a new bull market for all risk assets but also the first pitch of the first at-bat of the first inning. 2024 should be one of the easiest trading years in a decade. This could go on for a decade.

This is how things will play out.

After the hottest quarter of GDP growth in three years at 4.9% in Q3, the economy is slowing. Virtually every business sector is seeing sales weaken, especially real estate and EVs.

That sets up a sharp drop in the inflation rate from the current 3.2% to the Fed’s target of 2%. Get a few months of that and the Fed starts cutting interest rates from the current 5.25%-5.5%. Fed futures are currently indicating a 40% probability that will happen in March.

We could be at 4.0% overnight interest rates by the end of 2024 and 3.0% by the end of 2025 when they stabilize. Stocks and bonds will eat this up.

Better hope that the Fed stays data dependent as promised, because coming data is weak, even if it doesn’t arrive for months. We only need one weak quarter to kill off inflation, and that quarter began on October 1.

Priority One is for the Fed to de-invert the yield curve or get short-term interest rates below long rates. For encouragement, the Fed should look at the most rapidly shrinking money supply in history, which I have been glued to.

There has been no monetary growth for two years, and zero bank deposit growth for three years. The Fed's balance sheet has plunged by $1.5 trillion in 18 months. Fed quantitative tightening continues at $120 billion a month. This is unprecedented in economic history.

The biggest risk to markets is that Powell delays cutting rates as much as he delayed raising rates two years ago. This is a very slow-moving, backward-looking Fed.

If you have a ten-year view of the markets, as I do, this is all meaningless. You need to buy stocks right now. If the Fed does play hardball and rigidly holds to the 2% target it risks causing a recession.

If you see any reasons to shoot down my bull case please, please email me. I’d love to hear them.

It’s not that stocks are expensive. 2024 S&P 500 (SPY) earnings are now 18X. If you take out the Magnificent Seven, they are at 15X earnings, close to the 2008 crash low. Small cap stocks are at a bargain basement 12X earnings and are already priced for recession.

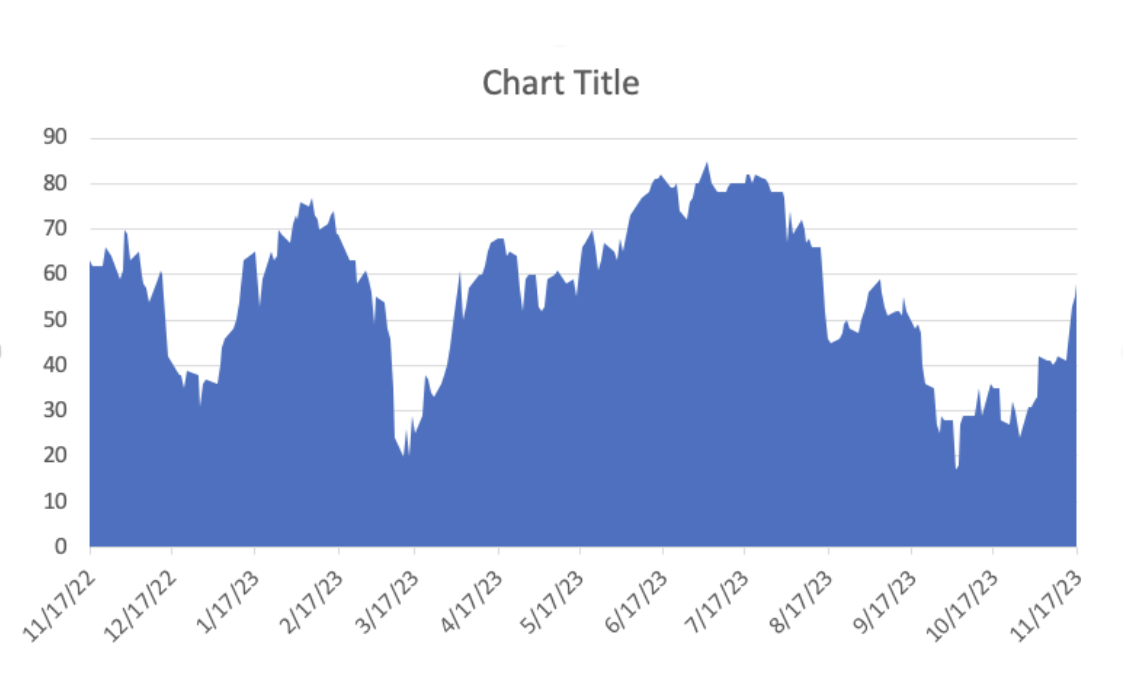

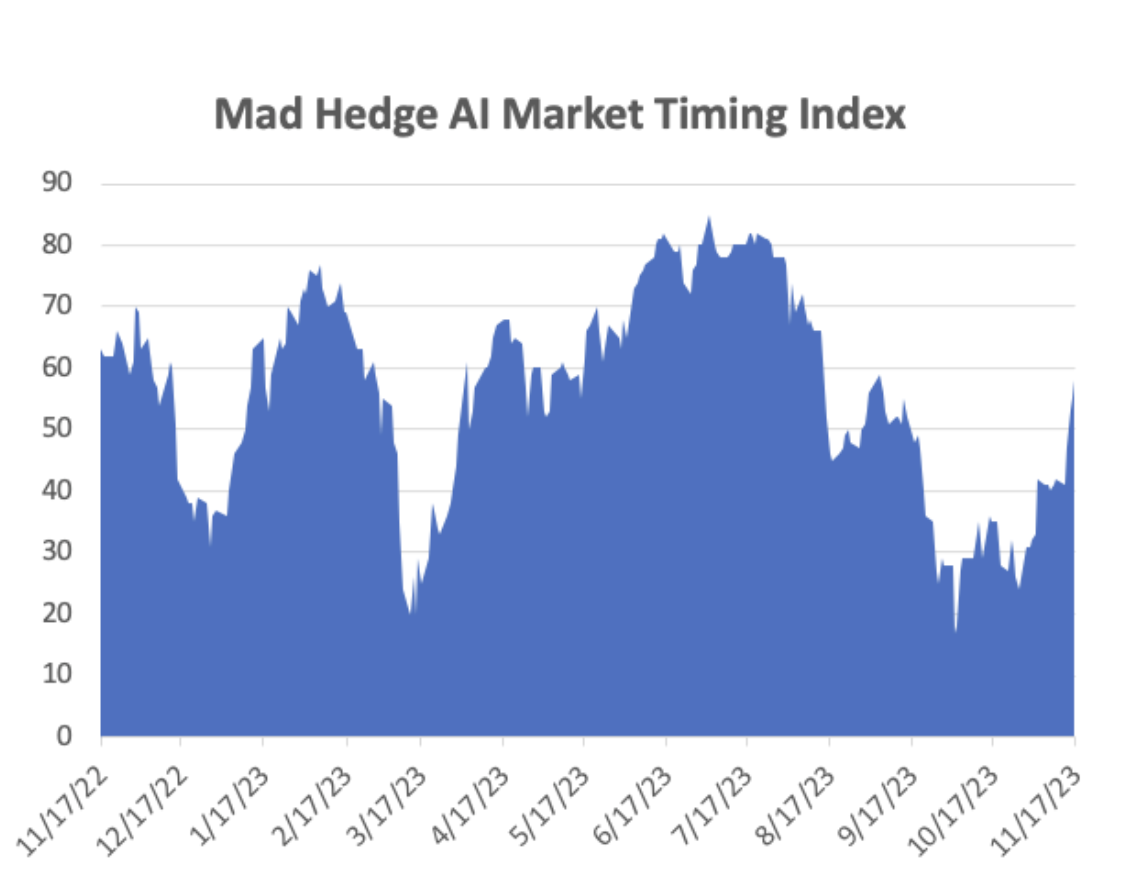

So a strong case for a new decade-long bull market is there. All you have to do is believe it. To see how this will play out look at the chart below as tech stocks are now extremely overbought short term. We no longer have the luxury of waiting for big dips. Small ones will have to do.

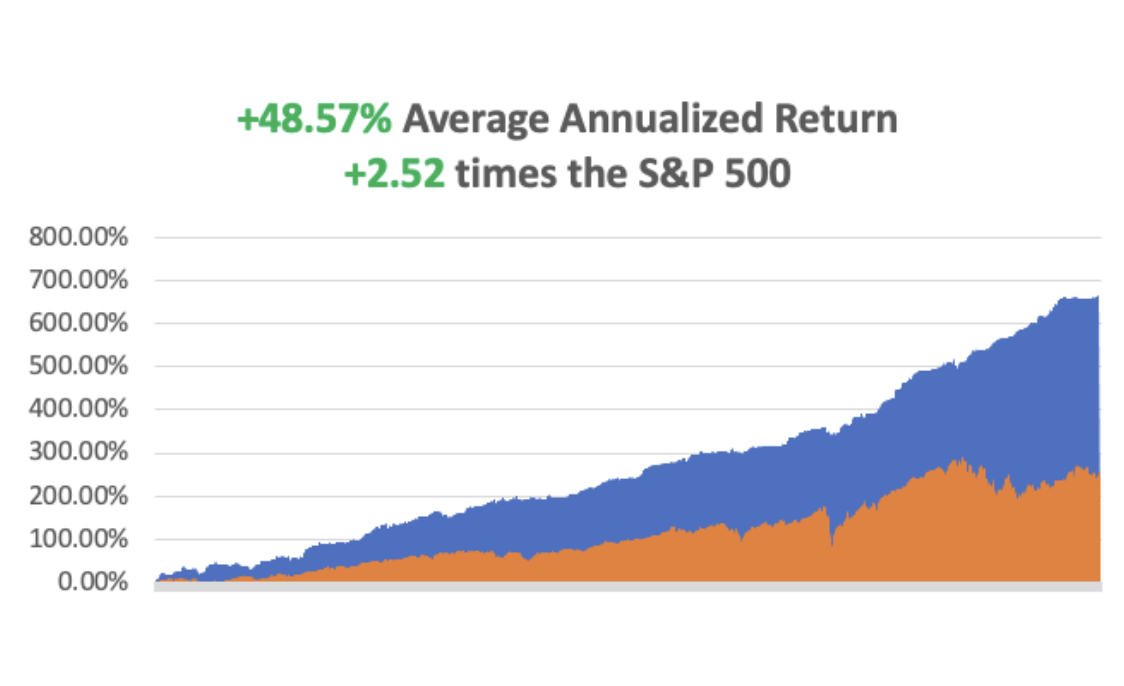

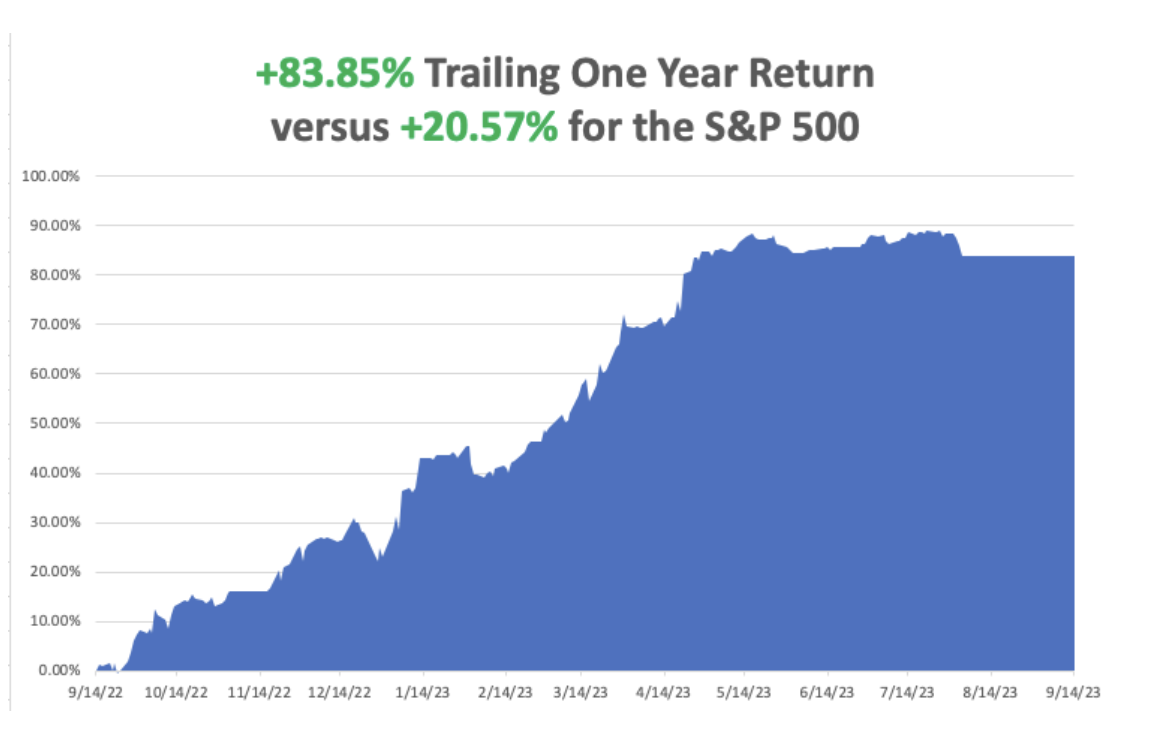

So far in November, we are up a breathtaking +12.59%. My 2023 year-to-date performance is still at an eye-popping +78.76%. The S&P 500 (SPY) is up +18.42% so far in 2023. My trailing one-year return reached +85.42% versus +20% for the S&P 500.

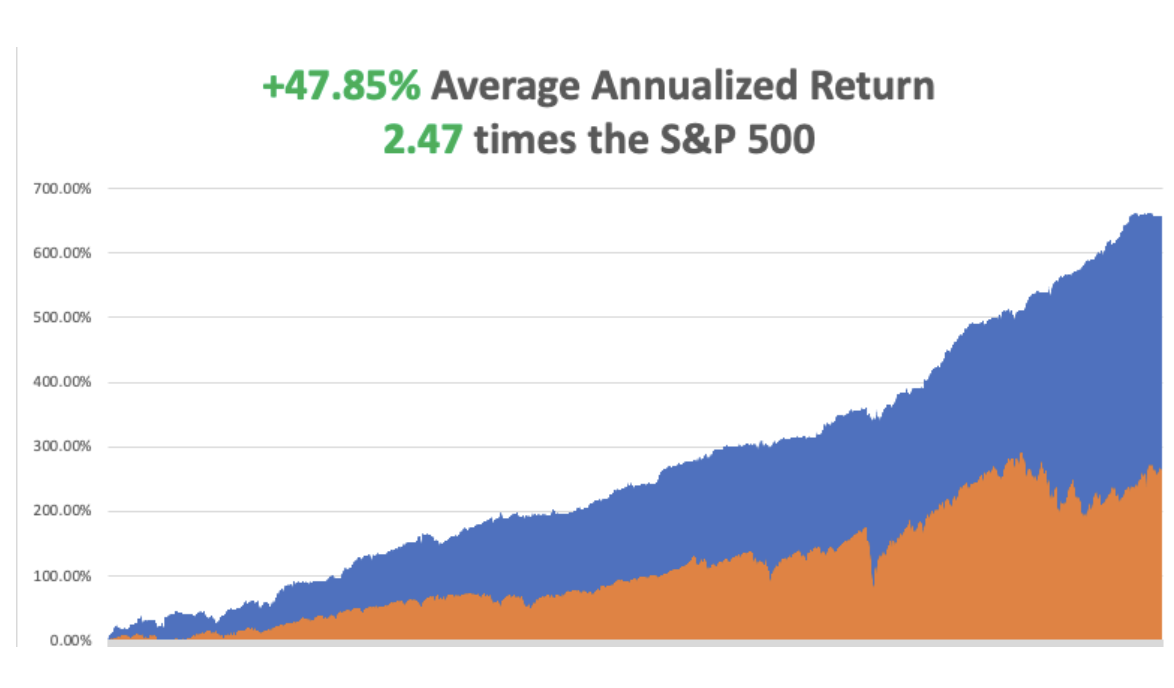

That brings my 15-year total return to +675.95%. My average annualized return ballooned to +48.57%, another new high, some 2.52 times the S&P 500 over the same period.

Some 60 of my 65 trades this year have been profitable.

CPI Comes in Flat at 3.2%, much weaker than expected. This is a game-changer. The first Fed rate cut has been moved up to May. Stocks and bonds loved it, taking ten-year US Treasury yield down to a six-week low at 4.44%. Shelter prices, which make up about a third of the overall CPI index, climbed 0.3%, half the prior month’s pace. Taking profits on my long in (TLT).

Fed to Cut Interest Rates as Early as March, or so says the futures market, which gives this a 40% probability. The (TLT) should top $100 and stocks will rocket, especially the interest sensitives. The most recent indications on the CME Group’s FedWatch gauge point to a full percentage point of interest rate cuts by the end of 2024.

Weekly Jobless Claims Hit Three Month High, up 13,000 to 231,000, as the US economy backs off from the superheated Q3. The path for a lower inflation rate is opening up. Do I hear 2%.

PPI Fell by 0.5% in October, a much bigger than expected drop, a three-year low. Inflation is fading fast. YOY came in at 1.3%. Stocks loved the news. 2024 is shaping up to be a great year for risk after two miserable ones.

Government Shutdown Delayed Until 2024, with the passage of a temporary spending bill by the House. It looks like there is a new coalition of the middle of both parties, as the bill passed with 339 votes, topping a two-thirds majority. The Johnson bill would fund some parts of the government through Jan. 19 and others through Feb. 2, setting up the possibility of yet another shutdown deadline on Groundhog Day.

The US Dollar (UUP) Takes a hit as the falling interest rate scenario starts to unfold. Even the Japanese yen rose. This could be a new decade-long trade. Currencies with falling interest rates are always the weakest.

Goldman Sachs Goes Bullish on Gold. The investment bank expects the S&P GSCI, a commodities markets index, to deliver a 21% return over the next 12 months as the broader economic environment improves, OPEC moves to support crude prices as refining is tight and with energy and gold acting as hedges against supply shocks. Buy (GLD), (GDX), and (GOLD) on dips.

Copper Bull Predicts 80% Gain in the Coming Decade, to $15,000 per metric tonne, up from $8,277 says Trafigura’s Kotas Bintas, the world’s largest metal trader. Exploding demand from EV makers is the reason, set to hit 20 million vehicles a year. Electrification of global energy sources is another. Buy (FCX) on dips.

Boeing Lands Monster Order, some $52 billion from Emirates Airlines for 90 new 777x’s and five 787’s. The stock rose 5% on the news. A giant China order is also lurking in the wings. Buy (BA) on dips.

Moody’s Rating Service Downgrades the US, citing deteriorating fiscal conditions and worsening chaos in Washington. However, it maintained its AAA Rating. Oh, and the government shut down on Friday. Buy (TLT) on the dip. Where else are investors going to go for quality?

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, November 20, no data of note were published.

On Tuesday, November 21 at 11:00 AM EST, the Minutes from the previous Fed meeting are released.

On Wednesday, November 22 at 8:30 AM, the Durable Goods are published.

On Thursday, November 23 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, November 24 at 2:30 PM the November S&P Flash PMI’s are published and the Baker Hughes Rig Count is printed.

As for me, I was invited to breakfast last week at the Incline Village Hyatt Hotel and was told to expect someone special, but they couldn’t tell me who for security reasons.

I was nursing a strong black coffee when a bulky figure with white hair wearing a Hawaiian shirt and thermal vest sat down at the table. It was Mike Love, lead singer of the Beach Boys.

During the 1950s, Mike’s dad was a regular visitor to Lake Tahoe, bringing his family up to camp on the then-vacant beaches. My family couldn’t have been far away.

When Mike made his fortune with one of the top rock groups of the 1960s, the natural thing to do was to buy an estate high up the mountain in Incline Village, Nevada with a great lake view. Like me, Mike fell for crystal-clear lake views in summer and spectacular snow-covered mountain vistas in winter. Local real estate agents refer to it as a “poor man’s Aspen.”

Mike ended up raising a family here, his kids eventually growing up and heading out to start their music groups. One was Wilson Phillips, made up of two of Mike’s daughters and the daughter of John Phillips of the Mamas and the Papas, who I taught how to swim at summer camp one year.

But Mike stayed. He loved the lake too much to leave so he made Incline his base for a touring schedule that ran up to a punishing 200 gigs a year.

Mike’s residence was something of a Tahoe insider’s secret. Those who knew where he lived kept the closely guarded secret. We have plenty of celebrities here, Larry Ellison, Mike Milliken, and Peoplesoft’s David Duffield, but Mike is the one everyone loves.

Mike, now 82, is not your typical rock star and I have known many. He is humble, self-effacing, and an alright guy. He avoided drugs and smoking to preserve his voice. He is a health fanatic. He has also been fighting a lifelong battle with depression which kept him off the touring circuit for years at a time and led to contemplations of suicide.

The Beach Boys formed in Hawthorne, California, a beachside suburb of Los Angeles in 1961. The group's original lineup consisted of brothers Brian, Dennis, and Carl Wilson, their cousin Mike Love, and friend Al Jardine. They were the original garage band. Together they created one of the greatest vocal harmonies of all time.

In 1963, the band enjoyed their first national hit with “Surfin USA”, beginning a string of top ten singles that reflected a southern California youth culture of surfing, cars, and teenage romance dubbed the “California sound.”

Those included "I Get Around", "Fun, Fun, Fun", "Help Me Rhonda", "Good Vibrations" and "Don't Worry Baby, which I’m sure you remember well. If you don’t, look them up on iTunes. Their 1966 album “Pet Sounds” was considered one of the most innovative ever produced.

I remember it like it was yesterday. They were one of the few groups that could stand up to the Beatles, who they became friends with. The Beach Boys were regulars on my car’s AM radio.

Buzz kill: the Beach Boys didn’t know how to surf.

All of the early Beach Boys songs were inspired by the Southern California beaches, but only half the country had beaches. So a new manager encouraged them to sing about cars, extending the life of the group by another decade. That is how we got “Little Deuce Coup,” and “409.” After all, the entire country owned cars.

The Beach Boys would eventually sell 100 million records second only to the Beatles. They were also one of the first groups to wrest production control away from the studios, a revolution for the industry that opened doors for generations of successive musicians.

In the late 1960s, the group took a religious bent, traveling to India to study under the celebrity guru Maharishi Mahesh Yogi. Mike has since been practicing transcendental meditation, and it probably saved his life.

By the 1970s, the California sound faded and was eventually killed off by disco. Their last album together was Endless Summer in 1974.

There are only three original Beach Boys left, and Mike Love alone is still touring. In 1983, Dennis Wilson drowned in a boating accident which is thought to be drug-related. In 1998, Carl Wilson died of lung and brain cancer after years of heavy smoking.

Mike was pleased that I recalled his 1980 London concert at Wembley Stadium. I had front-row seats; unaware that I would meet Mike 43 years later. In 1988, Mike was inducted into the Rock and Roll Hall of Fame.

Mike was very annoyed by the pandemic shutdown in 2020 because it prompted the cancelation of over 200 concerts worldwide. He still thinks Covid was fake. He doesn’t need to work as his royalties from 60 years of work are worth a fortune. He tours simply for the love of it.

Mike is now touring with a reconstituted Beach Boys. For their tour schedule, please click here. On November 17, 2023, Love released a special double album entitled “Unleash the Love” featuring 13 previously unreleased songs and 14 Beach Boys classics.

It was a pleasant way to spend a morning recalling the 1960s. It’s a miracle we both survived. It’s all proof that if you live long enough, you meet everyone.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 16, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TAKING SOME FIRE)

(USO), (UUP), (JPM),

I am writing this letter in a Ukrainian army truck on the banks of the Black Sea right where the Dnieper River flows in. Crimea is 20 miles across the water. We just watched an American HIMERS missile destroy a Russian facility there and the black smoke is billowing upward.

We’ve been stuck here at this army checkpoint for two hours on this gorgeous autumn day so they can check my papers and decide if I’m a Russian spy. I definitely don’t look like your average Ukrainian. What better time to knock a newsletter? After I finished my letter I took a nap.

I have to admit I have been somewhat remiss in following the market the past week.

Whenever I had the choice of checking my stock market app or Look Out Ukraine, which tracks incoming Russian missiles, the latter usually won out. Not always, but usually. Then it’s on to the next app, which gives the location of the nearest bomb shelter.

Some people go to the beach for vacations, while I choose war zones. Different strokes for different folks, I guess. Maybe I’m trying to relive my long-lost youth as a war correspondent in Southeast Asia all those years ago.

It’s Becoming increasingly obvious to all that the Fed is done raising interest rates. The only question is how long they will remain at this elevated level. Then year US Treasury yields, which hit a 17-year high of 4.80% last week, might visit 5.0% and then that’s it.

I must apologize to owners of the (TLT) October $89-$92 vertical bear put spread. I should have sent out a trade alert to take profits on Thursday during the bond market meltdown when the price hit $2.92. I know it hit this price because several followers emailed me to say thanks for the trade.

But I was pinned down by Russian fire on the west bank of the Dnieper River and couldn’t escape until after nightfall. Yes, I know, excuses, excuses.

Technical analysts are having a field day with the (SPY) seemingly trapped between the 50 and 200-day moving averages in a narrowing range. Something big is going to happen eventually.

Indexes could get resolved to the upside when big tech earnings come out the week of October 28, which are expected to be great. It could also be resolved to the downside on November 17 when the House of Representatives shuts down the US government.

Maybe this is why markets are going nowhere. In any case, the disaster in the Middle East is blotting out all other news.

Another matter on which traders increasingly agree is that big tech will lead any upside breakout. A sure sign is that they have been moving sideways for the last 2 1/2 months while interest rates-sensitive sectors have been getting slaughtered. Indeed, Alphabet (GOOGL) is down only 3% from its high for the year, a huge AI winner.

Look no further than Microsoft (MSFT), which trades at only 28.2 times earnings. The company expects 16.2% annual growth for the next three years and is the best growth and AI play out there with its ownership of OpenAI. That’s boosting Mr. Softy’s Azure cloud business enormously.

So far in August, we are up +2.23%. My 2023 year-to-date performance is still at an eye-popping +63.03%. The S&P 500 (SPY) is up +13.42% so far in 2023. My trailing one-year return reached +xx% versus +xx% for the S&P 500.

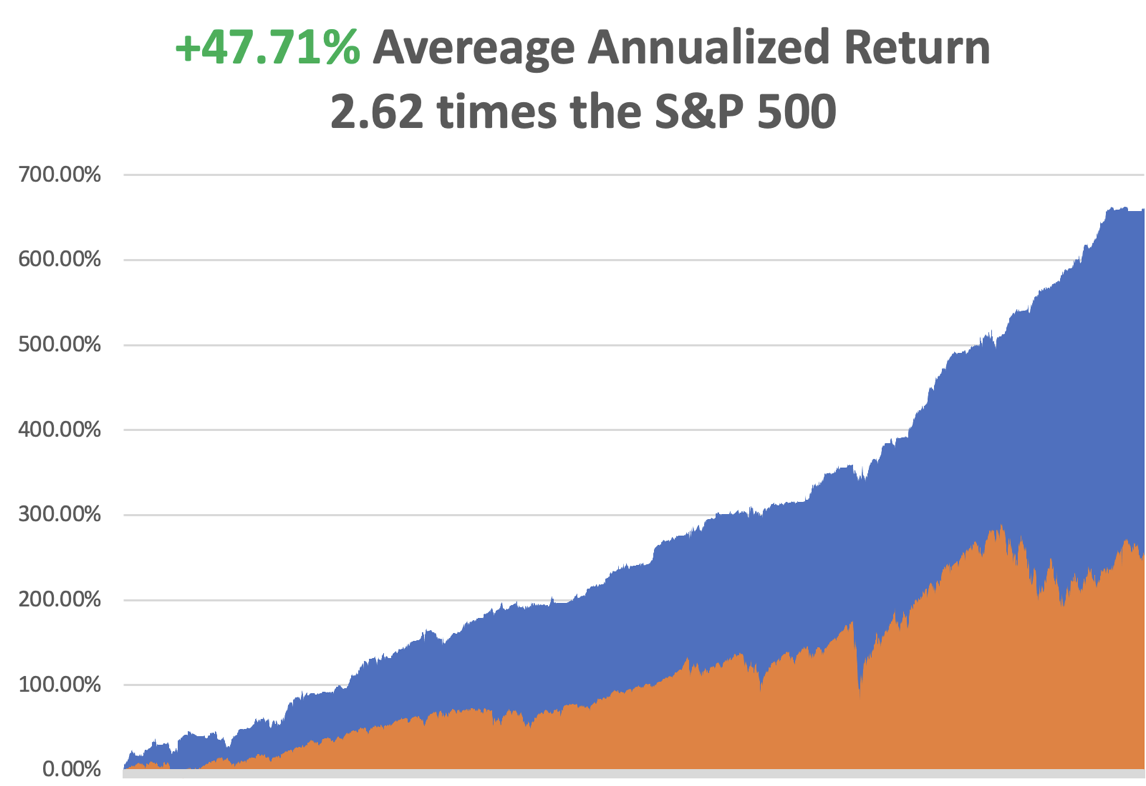

That brings my 15-year total return to +660.22%. My average annualized return has recovered to +47.71%, another new high, some 2.62 times the S&P 500 over the same period.

Some 44 of my 49 trades this year have been profitable.

It’s a Black Swan a Week that is conspiring to keep markets trapped in narrow ranges. The natural tendency seems to be up into a yearend rally, but they keep getting slammed by shocks, like a government shutdown, a leaderless house, and the Middle East War. The trade has been long big tech, long oil, and short small tech and bonds, of which Mad Hedge caught all four through its various services.

The Middle East Descends on Wall Street, and so far, the damage is limited to a few big techs. Oil (USO) is up 3% and gold caught a bid as well. If this develops into a major regional war expect more downside. It paid to buy every geopolitical crisis over the last 30 years.

Dollar (UUP) Soars on Mid East Chaos, as it catches its traditional flight to safety bid. We could be approaching a top here.

IMF Hikes US Growth Forecast. The International Monetary Fund raised its U.S. growth projection for this year by 0.3 percentage points compared with its July update, to 2.1%. It lowered its euro zone forecast by 0.2 percentage points, to 0.7%. China gets a downgrade too. For the US, 2024 is looking better and better.

The Producer Price Index Jumps 0.5%, more than expected. Markets didn’t really care. Gasoline as the biggest gainer.

The Consumer Price Index Explodes to 3.7%, Inflation is still transitory after over 3 years. Strip out food and energy and core inflation is over 4% year over year. The big question moving into 2024 is if the US consumer can handle these uncontrollable price rises and coalesce a Democratic government that parades around prices not going up less than before. The Fed hasn’t budged from their 2% inflation target, but they are taking their sweet time to get there.

JP Morgan (JPM) Announced Record Earnings, boosting the stock by 5%. With high rates, net interest income is the big winner. Reserves for loan losses were also cut. But (JPM) on dips.

Oil (USO) Jumps 4%, on a tightening of US sanctions against Russia. The goal is to deprive Russia of excess profits used to fund its war against Ukraine. Two foreign-flagged ships were barred from moving their cargo.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 16, at 2:30 PM EST, the New York State Manufacturing Index is out.

On Tuesday, October 17 at 2:30 PM, the US Retail Sales are released.

On Wednesday, October 18 at 2:30 PM, the US Building Permits are published.

On Thursday, October 19 at 8:30 AM, the Weekly Jobless Claims are announced. We also get Existing Home Sales.

On Friday, October 20 at 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I’ll record the Story of John Thomas’s Wild Ride, which took place only last Thursday.

We had just finished delivering the last of our food bags to starving peasants in the Kherson region, which is a 12-hour train ride east of Kiev. I received maybe 100 kisses and hugs from aging babushkas who had been cut off from their food supply for months. Most of their homes had been destroyed by Russian fire and they were living in basements.

They said, “Thank you.” I replied, “Stay strong.” They cried.

Then my army escort, a major who we called “Vitally”, got a call. A Russian mortar was harassing Kerson with intermittent fire inflicting casualties, and they were unable to spot it. Would we be willing to act as a decoy and draw fire?

The major looked at me to ask permission. I was on a humanitarian mission and had no obligation to engage in combat. What did I think?

I did the math. A mortar is a notoriously inaccurate weapon, plus we’d be doing at least 80 miles an hour. I decided it was more likely that I win the California lottery than get hit. So I told the major “Sure, why not.” I looked at the rest of my team and they agreed wholeheartedly. So, we headed down to the waterfront in Kherson.

The city has this long street which follows the banks of the Dnieper River. The Russian Army occupies the eastern bank and are well fortified. Kherson was completely deserted without a person or vehicle in sight. It was like a ghost town. Every statue in town had been stolen when the Russians retreated. Once we turned north, we poured on the gas.

We raced along the river as fast as the car would go, weaving left and right to avoid shell craters in the road. Occasionally we hit one and our heads bumped up against the ceiling. We sped through every red light. It was the thrill of a lifetime!

As we approached the bridge over the Dnieper River, which had already been blown up, sure enough, a mortar shell went sailing right overhead, hitting a building 100 yards to our left. Then we screeched to a halt, did a rapid 180, and tore off in the opposite direction. The Ukrainian Army’s 155 mm shells fired over our heads seconds later.

A minute later, we found a bomb shelter and jammed on the brakes. As we piled out of the car the air raid sirens were wailing. Once we got inside, we all burst into laughter. We couldn’t believe what we had just gotten away with.

And I got the whole thing on video.

Sitting in the bomb shelter I felt a stinging in my right hip. I looked down to find an AK 47 7.62mm copper jacketed bullet embedded in my flak jacket about an inch from the edge. When we left the bomb shelter, I inspected the car and sure enough, we had been sprayed with machine gun fire from across the river (see picture below).

It was a lucky hit. The bullet lost much of its velocity crossing the river and the sheet metal of the car slowed it down even further. The Kevlar bulletproof vest did its job. I got away with only a nice bruise.

As we drove out of town the major received another call. Thanks to our effort the mortar had been silenced. He gave me a big smile and a thumbs-up.

At the edge of town, we stopped for a victory photo at the city gates. That’s my team holding the American flag. The major has a scarf covering his face to keep his identity secret.

The major told me I was the bravest man he ever met. Then he turned and started walking back into Kherson.

If you want to watch the video of John Thomas’s Wild Ride please tune into my biweekly webinar on Wednesday, October 18 at 12:00 noon EST.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 2, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or BACK IN BUSINESS)

(TLT), (GLD), (SLV), (XLU), (IWM), (EEM), (FXA), (FXE), (FXB), (USO), (UUP), (AMZN), (TSLA), (F)

It’s a good thing I don’t rely on my Social Security Check to cover my extravagant cost of living, which is the maximum $4,555 a month. For it came within hours of coming to a halt when an agreement was passed by Congress to renew funding for another 45 days. It was almost an entirely Democratic bill, passing 335 to 91 in the House and the Senate by 88 to 9.

Unfortunately, that does put me in the uncomfortable position of delivering humanitarian aid to Ukraine right when $6.2 billion in US assistance is cut off. That was the price the Dems had to pay to get the Republicans on board needed to pass the bill. Better a half a loaf than no loaf at all. Still, I am going to have some explaining to do next week in Kiev, Mykolaiv, and Kherson. It’s a big win for Vladimir Putin.

Funding now ends on November 17, when the next crisis begins. The big question is when the markets will deliver a sigh of relief rally on Congress hitting the “snooze” button, or whether it will focus on the next disaster in November.

We’ll have to wait and see.

In the meantime, all eyes are on the market’s leading falling interest rate plays, which continue to go from bad to worse. Those include bonds (TLT), precious metals (GLD), (SLV), utilities (XLU), small-cap stocks (IWM), emerging markets (EEM), and foreign currencies (FXA), (FXE), (FXB).

Consider this your 2024 shopping list.

Ten-year US Treasury bond yields reached a stratospheric 4.70% last week a 17-year high and up a monster 0.90% since the end of June. Summer proved a fantastic time to take a vacation from the bond market.

They could easily reach 5% before the crying is all over. Perhaps this is why my old friend, hedge fund legend David Tepper, said his best investment right now is a subprime six-month certificate of deposit yielding 7.0%.

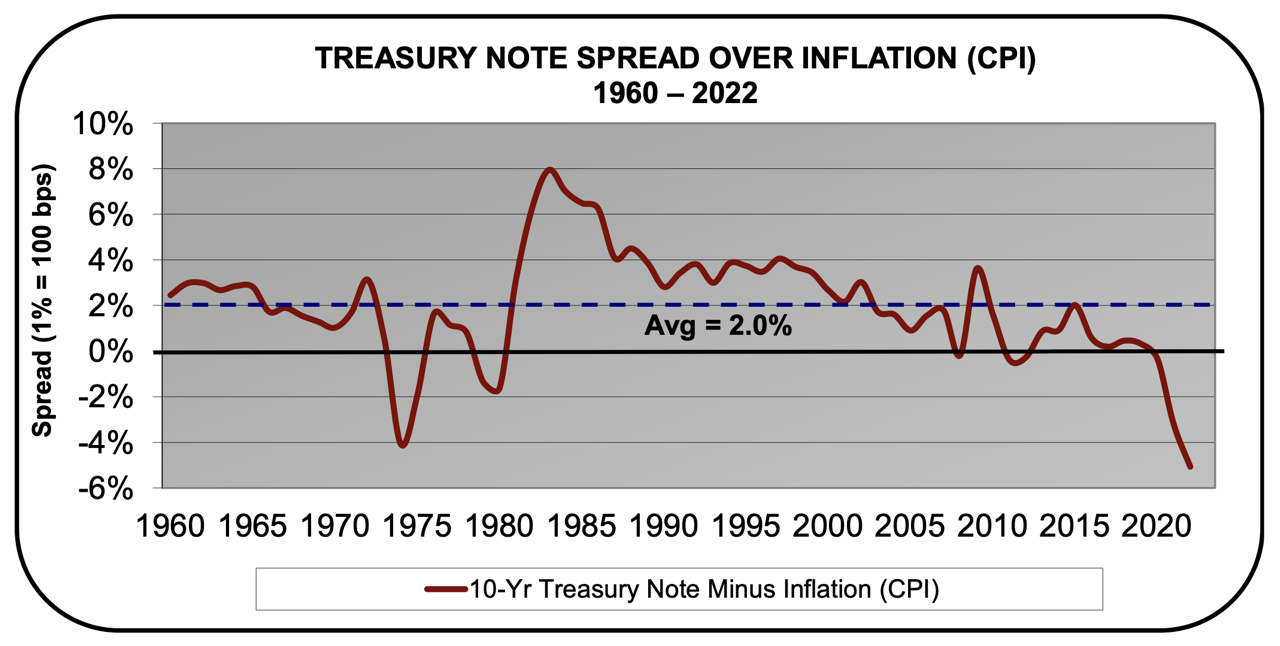

What we might be witnessing here is a return to the “old normal” when bonds spent most of their time ranging between 2%-6%. The 60-year historic average bond yield is 2% over the inflation rate (see chart below). That alone takes us to a 5.0% bond yield.

Interest rates have been kept artificially low for 15 years because no one wanted a recession in 2008 and no one wanted a recession during the pandemic in 2000. It all melded into one big decade-and-a-half period of easy money. Pain avoidance wasn’t just the universal American monetary policy, it was the global policy.

Now it’s time to pay the piper and unwind the thousands of business models that depended on free money. There will be widespread pain, as we are now witnessing in commercial real estate and private equity. Perhaps it is best to take the 5.5% bribe 90-day Treasury bond yield is offering you and stay out of the market.

While Detroit remains mired by the UAW strike, EVs have catapulted to an amazing 8% of the new car market. They have been helped by a never-ending price war and generous government subsidies. EV sales are now up a miraculous 48% YOY and are projected to account for a stunning 23% of all California sales in Q3.

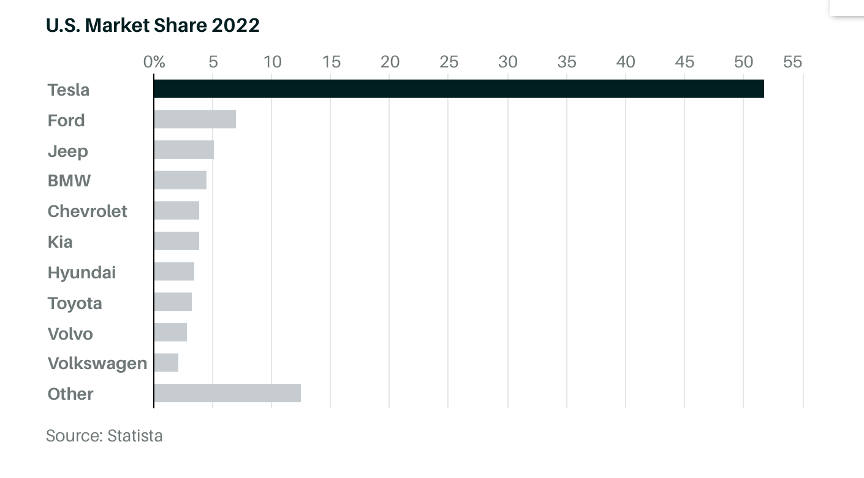

Tesla is the overwhelming leader with a 52% share in a rapidly growing market, distantly followed by Ford (F) at 7% and Jeep at 5%.

However, a slowdown may be at hand, with EV inventories running at 97 days, double that of conventional ICE cars. This could create a rare entry point for what will be the leading industry of this decade, if not the century. Buy more Tesla (TSLA) on bigger dips, if we get them.

Hedge Funds are Cutting Risk at Fastest Pace Since 2020, when the pandemic began. From retail investors to rules-based systematic traders, appetite for equities is subsiding after a 20% rally this year that’s fueled by euphoria over artificial intelligence. Fast money investors increased their bearish wagers to drive down their net leverage — a gauge of risk appetite that measures long versus short positions — by 4.2 percentage points to 50.1%, according to Goldman Sachs Group Inc.’s prime brokerage. That’s the biggest week-on-week decline in portfolio leverage since the depths of the pandemic bear market.

The Treasury Bond Freefall Continues, as long-term yields probe new highs. New issue of $134 billion this week didn’t help. Nothing can move on the risk until rates top out, even if we have to wait until 2024.

Oil (USO) Hits $95, a one-year high, as the Saudi/Russian short squeeze continues. $100 a barrel is a chipshot and much higher if we get a cold winter. Inventories at the Cushing hub are at a minimum.

The US Dollar (UUP) Hits New Highs, as “high for longer” interest rates keep powering the greenback. The buck is also catching a flight to safety bid from a potential government shutdown. It should be topping soon.

Moody’s Warns of Further US Government Downgrades, in the run up to the Saturday government shutdown. The shutdown lasts, the more negative its impact would be on the broader economy. Unemployment could soar. It would also render all US government data releases useless for the next three months.

ChatGPT Can Now Browse the Internet, according to its creator, OpenAI. Until now, the chatbot could only access data posted before September 2021. The move will exponentially improve the quality and effectiveness of AI apps, including my own Mad Hedge AI

Amazon (AMZN) Pouring $4 Billion into AI, with an investment in Anthropic, a ChatGPT competitor. (AMZN) is racing to catch up with (MSFT) and (GOOGL). Its chatbot is caused Claude 2. Amazon’s card to play here is its massive web services business AWS. The AI wars are heating up.

Hollywood Screenwriters Guild Strike Ends, after 150 days, which is thought to have cost the US economy $5 billion in output. The hit was mostly taken by Los Angeles, where 200,000 are employed. The Actor’s union is still on strike. Talk shows should be offering new content in a few days.

S&P Case Shiller Rises to New All-Time High, for the sixth consecutive month as inventory shortages drove up competition. In July, the index in increased 0.6% month over month and 1% over the last 12 months, on a seasonally adjusted basis. July’s movement reached a new high for the nationwide home index, surpassing the record set in June 2022. Chicago (+4.4%), Cleveland (+4.0%), and New York (+3.8%) delivered the biggest gains. The median home price for existing homes rose to 1.9 to $406,700 according to the National Association of Realtors (NAR). The robust housing market suggests that while some buyers pulled back due to high borrowing costs, demand continues to outweigh supply.

This is the Unit I Will be Joining at the Front in Ukraine, as made clear by their YouTube recruiting video. They asked me to assist with mine removal on territory formerly occupied by Russia. I really don’t know what I’m getting into. Improvision is key. It’s better than playing golf in retirement. Polish up your Ukrainian first.

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, another new high, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 2, at 8:30 PM EST, the ISM Manufacturing PMI is out.

On Tuesday, October 3 at 8:30 AM, the JOLTS Job Openings Report is released.

On Wednesday, October 4 at 2:30 PM, the ISM Services Report is published.

On Thursday, October 5 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, October 6 at 2:30 PM the September Nonfarm Payroll Report is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I will try to knock out a few memories early this morning while waiting for the Matterhorn to warm up so I can launch on another ten-mile hike. So I will reach back into the distant year of 1968 in Sweden.

My trip to Europe was supposed to limit me to staying with a family friend, Pat, in Brighton, England for the summer. His family lived in impoverished council housing.

I remember that you had to put a ten pence coin into the hot water heater for a shower, which inevitably ran out when you were fully soaped up. The trick was to insert another ten pence without getting soap in your eyes.

After a week there, we decided the gravel beach and the games arcade on Brighton Pier were pretty boring, so we decided to hitchhike to Paris.

Once there, Pat met a beautiful English girl named Sandy, and they both took off to some obscure Greek island, the ultimate destination if you lived in a cold, foggy country.

That left me stranded in Paris with little money.

So, I hitchhiked to Sweden to meet up with a girl I had run into while she was studying English in Brighton. It was a long trip north of Stockholm, but I eventually made it.

When I finally arrived, I was met at the front door by her boyfriend, a 6’6” Swedish weightlifter. That night found me bedding down in a birch forest in my sleeping bag to ward off the mosquitoes that hovered in clouds.

I started hitchhiking to Berlin, Germany the next day, which offered paying jobs. I was picked up by Ronny Carlson in a beat-up white Volkswagen bug to make the all-night drive to Goteborg where I could catch the ferry to Denmark.

1968 was the year that Sweden switched from driving English style on the left side of the road to the right. There were signs every few miles with a big letter “H”, which stood for “hurger”, or right. The problem was that after 11:00 PM, everyone in the country was drunk and forgot what side of the road to drive on.

Two guys on a motorcycle driving at least 80 mph pulled out to pass a semi-truck on a curve and slammed head-on to us, then were thrown under the wheels of the semi. The motorcycle driver was killed instantly, and his passenger had both legs cut off at the knees.

As for me, our front left wheel was sheared off and we shot off the mountain road, rolled a few times, and was stopped by this enormous pine tree.

The motorcycle riders got the two spots in the only ambulance. A police car took me to a hospital in Goteborg and whenever we hit a bump in the road bolts of pain shot across my chest and neck.

I woke up in the hospital the next day, with a compound fracture of my neck, a dislocated collar bone, and paralyzed from the waist down. The hospital called my mom after booking the call 16 hours in advance and told me I might never walk again. She later told me it was the worst day of her life.

Tall blonde Swedish nurses gave me sponge baths and delighted in teaching me to say Swedish swear words and then laughed uproariously when I made the attempt.

Sweden had a National Health care system then called Scandia, so it was all free.

Decades later a Marine Corps post-traumatic stress psychiatrist told me that this is where I obtained my obsession with tall, blond women with foreign accents.

I thought everyone had that problem.

I ended up spending a month there. The TV was only in Swedish, and after an extensive search, they turned up only one book in English, Madame Bovary. I read it four times but still don’t get the ending. And she killed herself because….?

The only problem was sleeping because I had to share my room with the guy who lost his legs in the same accident. He screamed all night because they wouldn’t give him any morphine.

When I was released, Ronny picked me up and I ended up spending another week at his home, sailing off the Swedish west coast. Then I took off for Berlin to get a job since I was broke. Few Germans wanted to live in West Berlin because of the ever-present risk of a Russian invasion so there we always good-paying jobs.

I ended up recovering completely. But to this day whenever I buy a new Brioni suit in Milan they have to measure me twice because the numbers come out so odd. My bones never returned to their pre-accident position and my right arm is an inch longer than my left. The compound fracture still shows up on X-rays.

And I still have this obsession with tall, blond women with foreign accents.

Go figure.

Brighton 1968

Ronny Carlson in Sweden

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

September 20, 2023

Fiat Lux

Featured Trade:

(THE BOND KING IS WRONG ABOUT TECH STOCKS)

($COMPQ), (UUP), (MSFT)

At the Future Proof conference last week, Bond King Jeffrey Gundlach gave his expert take on some of the variables in the markets today.

It’s hard for to understand how Gundlach made his money with the amount of fear mongering he is promoting.

He is basically scared of everything in todays market including the stock market, the US dollar (UUP), the upcoming recession that still hasn’t hit, high housing prices, and layoffs just the name the start.

First, the unemployment rate is at 3.8% in the US so to say that this is a canary in the coalmine is quite hilarious.

Tech, even drastically over hired, and they had to take a machete to staff numbers just to get back to the 2020 employment levels.

I would even say that they need to go back to 2015 staff levels with artificial intelligence contributing more efficiency.

I hardly believe it’s time to ring to alarm on tech unemployment.

Look across the Atlantic where Spanish youth unemployment is 30% and Italians, on average, live with their parents until 45 years old because they can’t afford to move out of the house.

The United States is not that and will not become like that.

The Nasdaq Composite ($COMPQ) has surged 31% respectively this year, as investors price in the potential boost to companies from artificial intelligence and future cuts to interest rates.

However, they're overlooking "demons on the horizon," Gundlach cautioned.

We are nearing the top of the interest rate cycle and no other OECD economy has been able to push rates to 5.25% while keeping the economy churning.

Therefore, it might be plausible to say that the demons aren’t on the horizon, but in the rearview mirror.

Japan is still at 0% which has resulted in a massive invisible tax to the Japanese middle class which is basically the whole country.

He also noted the chilling effect of higher mortgage rates on the housing market, and the challenge for small businesses of having to refinance their debts at much higher interest rates.

It’s true that 7% mortgage rates has extraordinarily hit left wing coastal cities.

Combine high mortgage rates with work from home, and Silicon Valley has now moved everywhere with everyone becoming a digital nomad.

This has actually transferred new tech wealth to many other new areas such as Nashville, Austin, and of all places Boise, Idaho.

This trend can’t be understated and is now a growing contributor to the overall economy.

"The economy is definitely weakening" is something I definitely agree with Gundlach, but that doesn’t reveal the whole story.

The internals are slowing down from a very high peak which he failed to mention.

Instead of Microsoft (MSFT) cloud division Azure growing at 40% year over year, we are only getting about 18% these days.

Coming off of Himalayan highs is a tough pill to swallow when many tech investors often expect growth metrics of over 30% year over year, but that’s hard to achieve in 2023.

The strong dollar has also exerted a fierce deflation affect across many tech products making computers and so on cheap. Tech products in Europe and abroad are higher priced even though these places have incomes that a many times lower.

Relatively speaking, US tech companies and US consumers are better placed than any other comparable city or country in the world in the post-covid world.

Fear mongering never got anybody rich. US tech will continue to be the best of breed and in no plausible scenario will a foreign company or country knock any of the top 7 Silicon Valley tech firms off their perch in the next 30 years. I would even argue that as rates peak and interest rates expectation ratchet lower, tech stocks will become the safety trade again like it did in March.

Global Market Comments

September 11, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BIG PULL FORWARD)

(AAPL), (UUP), (TSLA), (USO), (BYDDF)

Somehow, the summer got moved this year.

For here it is September, and the stock market is behaving like it is only July. July was different from normal as well, going straight up almost every day when it is usually asleep. This year, July acted like May, when you’re supposed to sell and go away.

If you’re thoroughly confused by all of this, so am I. The historic cyclicality of the markets, the ebb and flow of share prices according to the calendar, has gone out the window. But then, what isn’t confusing these days?

I went to buy a green drink from Whole Foods on Friday and the counter was closed because of staff shortages. Whole Foods unable to sell a green drink?

I tried to climb the Matterhorn this summer but was told that the guides weren’t taking anyone up because of the extreme heat. The mountain was literally melting, dropping rocks on the heads of climbers. No climbing the Matterhorn in Switzerland? I went to the Dolomites instead where you climb ice-free shear rock faces.

I tried to get into the Pantheon in Rome this summer and was met with a five-hour line. The Sistine Chapel in the Vatican was worse. When I first went there in the 1960’s the place was empty. The fact is that Italy now has more tourists than Italians. Oh, and the pope is from Argentina.

Has the world gone mad?

What has happened is that there has been a great pull forward that took place in financial markets during the first half of the year. I’ve seen this before. When a conclusion becomes obvious, everyone jumps on the bandwagon and brings everything forward.

So from January to July stock markets saw the blatantly obvious future that inflation would fall, interest rates decline, the US dollar weaken, and commodities and precious metals would rise. That’s why the “Magnificent Seven” led.

What happens next?

Now shares have to wait until these predictions actually happen before they can move any further. Markets have moved as far as they can on faith alone. Next, we need facts. This could take weeks or even months.

I knew this was going to happen. That’s why I went pedal to the metal, full speed ahead, damn the torpedoes aggressive during the first half of the year and clocked a 60% profit. I expected that if you didn’t make a profit in the first half of the year, you wouldn’t have any profits in 2023 at all.

And the trade alert drought continues.

There isn’t a day that goes by when I am not asked if America’s $33 trillion national debt will destroy the economy, cause the stock market to crash, and bring the end of Western Civilization. The answer is no, never, not in our lifetimes.

The reason is very simple. Any dollar the government borrows today sees its purchasing power go to zero in 30 years. That’s where the massive Civil War debt went, that's where the WWI debt went, and that’s where the gigantic WWII debt went, some 105% of GDP. Today’s debt will similarly vaporize over time.

Who pays for this cataclysmic decline in value? US government debt holders, who similarly see their purchasing power disappear over time. It turns out that the ultimate avoiders of risk, investors in US government debt, not only don’t get paid for their cowardice, they lose their entire principal as well, at least in terms of purchasing power.

There is a wonderful article in Barron’s this week entitled “Government Debt Needs to Be Repaid, And Other Myths About the Federal Deficit” by Paul Sheard which explains how all this works, which I quote below in its entirety.

“The U.S. national debt currently stands at $32.91 trillion, and 10 months into this fiscal year, the U.S. government has spent $1.6 trillion more than it has collected in revenue. Those intimidating figures animate political battles that can shut down the government and even bring it to the brink of default. But the meaning of this money isn’t as simple as it seems. Five myths in particular deserve straightening out.

The first is that the government has to borrow in order to spend and run deficits. It’s the other way around. The government creates money (injects it into the economy) when it spends and destroys money (withdraws it from the economy) when it taxes. The government taxes variously to correct for negative externalities, to redistribute income, and to modulate aggregate demand; “raising revenue” is just a cover story.

A related myth is that the government needs to repay its debt. “Debt” is a misnomer; government debt is just money (or purchasing power) in another form. A $20 bill is a liability of the Fed, which makes it a liability of the federal government. A $20 bill never has to be repaid; it just is. Fundamentally, Treasuries aren’t much different.

That government debt never needs to be repaid doesn’t mean the government can or should create as much of it as it likes.

Too big a pile of debt because of prior and ongoing budget deficits may be inflationary, as too much money chases insufficient goods and services. That will require some combination of monetary and fiscal tightening. A mountain of debt may indicate a government that is too big and intrusive in the economy for many people’s liking, an issue that can be fought out at the ballot box.

A third myth is that the Fed prints money when it does quantitative easing. The money-printing happens when the government runs a budget deficit; QE just changes the form of that money.

QE is really just a debt refinancing operation of the consolidated government—that is, the government including the Fed—whereby it refinances one form of debt (government bonds or guarantees) into another (reserves). QE changes the composition of the (consolidated) government debt in the hands of the private sector, but it doesn’t directly add one iota of new purchasing power. For every dollar the Fed “pumps into” the economy by doing QE, it “sucks out” a dollar of assets. Conversely, quantitative tightening just returns assets to private sector portfolios, expunging reserves in the process.

Reserves are like banknotes: The Fed can withdraw them, but it never has to repay them as such. It looks like the government has to repay Treasuries, but this is an institutional artifact. In extremis, the Fed could convert all outstanding Treasuries into reserves, and it could maintain monetary control by it, rather than the fiscal authorities, paying interest on reserves.

Japan is the poster child for a miserable-looking fiscal picture. Yet, the Bank of Japan, the pioneer of QE, owns almost half of the stock of outstanding Japanese government securities and, at the same time, since 2016 has managed the 10-year yield, with some leeway, to be “around zero percent.”

It is precisely because the government can create money at will that the modern monetary and fiscal architecture has been designed to put shackles on its ability to do so: The creation of an “independent” central bank within the government, the central bank not allowing the government’s account with it to go into overdraft, the central bank not buying bonds directly from the government, and governments issuing debt securities rather than leaving their deficits in the form of reserves all serve that purpose. But what the government taketh away, it can give back. Faced with the need, it could loosen those shackles.

A fourth, and related, myth is that banks could, if so moved, “lend out” the excess reserves created by QE. Banks can lend these reserves to one another but they cannot turn them into lending to companies and households in the broader economy.

It isn’t just the government that creates money. Banks do, too. A fifth myth is that banks are just financial intermediaries “taking in” deposits and “lending them out.” Not so. Banks create money when they lend. For an individual bank making a new loan, it may not feel like this, because the first thing borrowers do is spend their money. If none of that money flows back into the same bank, its reserves at the central bank will decline by the amount of the loan. It will then probably want to attract deposits to “fund” the loan, but doing so will just top up its lost reserves. Bank lending for the system is entirely self-funding (so long as none of the money created leaks into bank notes).

The U.S. economy currently produces about $27 trillion of goods and services annually, a little more than the amount of federal debt held by the public and the QE-embracing Fed. The money needed to sustain this giant prosperity-generating machine comes from the government running deficits and from banks extending credit, with the Fed’s activities linking the two. Political debates and decisions currently are based on a befuddled grasp of how this monetary system works. The stakes for society are too high for that.”

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, another new high, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

Beige Book Shows Consumer Spending Slowing, long a pillar of this recovery, as the last of the pandemic bonuses work their way for the system. It’s putting a dent in corporate profits and hints at a shrinking economy, contrary to recent economic data.

The US Dollar (UUP) is Soaring, thanks to “higher interest rates for longer” and a strengthening US economy. Asian currencies are at ten-month lows and central bank intervention is looking. The dollar shorting selling opportunity of the decade is setting up.

China Restricts Sales of iPhones (AAPL), barring sales to government agencies. It’s only a small nick in overall sales, but certainly casts of cloud over doing business in the Middle Kingdom. Some $200 billion, (AAPL)’s market cap has been vaporized.

Weekly Jobless Claims Dive, down 13,000 to 216,000, a seven-month low. It’s the fourth consecutive decline and not what the Fed wanted to hear.

Rate Hikes Will Drag on the Economy for at Least a Decade, as the Fed's $8.24 trillion balance sheet unwinds, according to the San Francisco Fed. The balance sheet was only at $800 million before the 2008 Great Recession.

Saudi Arabia and Russia Engineer Short Squeeze on Oil (USO), taking the price over $90 a barrel this year. Large production cuts announced in June will be maintained until yearend. Will Biden counter with a release from the Strategic Petroleum Reserve, or SPR?

Tesla’s Chinese EV Deliveries Rise 9.3% in August, thanks to aggressive price cuts. There is a two-month wait for the Model Y. Chinese rival BYD (BYD), with its Dynasty and Ocean series of EVs and petrol-electric hybrid models, recorded deliveries of 274,086 passenger vehicles in August, a jump of 57.5% year-on-year. China has the world’s largest car market.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 11, US Consumer Inflation Expectations are announced.

On Tuesday, September 12 at 8:30 PM EST, NFIB Business Optimism Index is released. Apple announced the new iPhone 15.

On Wednesday, September 13 at 8:30 AM, the Core Inflation Rate for August is published.

On Thursday, September 14 at 8:30 AM, the Weekly Jobless Claims are announced. ARM started trading after its IPO, which was five times oversubscribed. NVIDIA tried but failed to take over the chip maker.

On Friday, September 15 at 2:30 PM, the Producer Price Index for August is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, not just anybody is allowed to fly an aircraft in Hawaii. You have to undergo special training and obtain a license endorsement to cope with the Aloha State’s many aviation challenges.

You must learn how to fly around an erupting volcano, as it can swing your compass by 30 degrees. You must master the fine art of not getting hit by a wave on takeoff since it will bend your wingtips forward. And you’re not allowed to harass pods of migrating humpback whales at a low level, a sight I will never forget.

Traveling interisland can be highly embarrassing when pronouncing reporting points that have 16 vowels. And better make sure your navigation is good. Once a plane ditched interisland and the crew was found six months later off the coast of Australia. Many are never heard from again.

And when landing on the Navy base at Ford Island you were told to do so lightly, as they still hadn’t found all the bombs the Japanese had dropped during their Pearl Harbor attack in 1941.

You are also informed that there is one airfield on the north shore of Molokai you can never land at unless you have the written permission from the Hawaii Department of Public Health. I asked why and was told that it was the last leper colony operating in the United States.

My interest piqued, the next day found me at the Hawaiian state agency with an application in hand. I still carried my UCLA ID which described me as a DNA researcher, which did the trick.

When I read my flight clearance to the controller at Honolulu International Airport, he blanched, asking if I had authorization because he’d never seen one before. I answered that yes, I did, I really was headed to the dreaded Kalaupapa Airport, the Airport of no Return.

Getting into Kalaupapa is no mean feat. You have to follow the north coast of Molokai, a 3,000-foot-high series of vertical cliffs punctuated by spectacular waterfalls. Then you have to cut your engine and dive for the runway in order to land into the wind. You can only do this on clear days, as the airport has no navigational aids. The crosswind is horrific.

If you don’t have a plane it is a 20-mile hike down a slippery trail to get into the leper colony. It wasn’t always so easy.

During the 19th century, Hawaiians were terrified of leprosy, believing it caused the horrifying loss of appendages, like fingers, toes, and noses, leaving bloody open wounds. So, King Kamehameha I exiled lepers to Kalaupapa, the most isolated place in the Pacific.

Sailing ships were too scared to dock. They simply threw their passengers overboard and forced them to swim for it. Once on the beach, they were beaten a clubbed for their possessions. Many starved.

Leprosy was once thought to be a result of sinfulness or infidelity. In 1873, Dr. Gerhard Henrik Armauer Hansen of Norway was the first person to identify the germ that causes leprosy, the Mycobacterium leprae.

Thereafter, it became known as Hanson’s Disease. A multidrug treatment that arrested the disease, but never cured it, did not become available until 1981.

Leprosy doesn’t actually cause appendages to drop off as once feared. Instead, it deadens the nerves, and then rats eat the fingers, toes, and noses of the sufferers when they are sleeping. It can only be contracted through eating or drinking live bacteria.

When I taxied to the modest one-hut airport, I noticed a huge sign warning “Closed by the Department of Health.” As they so rarely get visitors the mayor came out to greet me. I shook his hand but there was nothing there. He was missing three fingers.

He looked at me, smiled, and asked, “How did you know?”

I answered, “I studied it in college.” Even today, most are terrified of shaking hands with lepers.

Not me.

He then proceeded to give me a personal tour of the colony. The first thing you notice is that there are cemeteries everywhere filled with thousands of wooden crosses. Death is the town’s main industry.

There are no jobs. Everyone lives on food stamps. A boat comes once from Oahu a week to resupply the commissary. The government stopped sending new lepers to the colony in 1969 and is just waiting for the existing population to die off before they close it down.

Needless to say, it is one of the most beautiful places on the planet.

The highlight of the day was a stop at Father Damien’s church, the 19th century Belgian catholic missionary who came to care for the lepers. He stayed until the disease claimed him and was later sainted. My late friend Robin Williams made a movie about him, but it was never released to the public.

The mayor invited me to stay for lunch, but I said I would pass. I had to take off from Kalaupapa before the winds shifted.

It was an experience I will never forget.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Airport of No Return

Father Damien