Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Below please find subscribers’ Q&A for the November 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: The country is running out of diesel fuel this month. Should I be stocking up on food?

A: No, any shortages of any fuel type are all deliberately engineered by the refiners to get higher fuel prices and will go away soon. I think there was a major effort to get energy prices up before the election. If that's the case, then look for a major decline after the election. The US has an energy glut. We are a net energy exporter. We’re supplying enormous amounts of natural gas to Europe right now, and natural gas is close to a one-year low. Shortages are not the problem, intentions are. And this is the problem with the whole energy industry, and the reason I'm not investing in it. Any moves up are short-term. And the industry's goal is to keep prices as high as possible for the next few years while demand goes to zero for their biggest selling products, like gasoline. I would be very wary about doing anything in the energy industry here, as you could get gigantic moves one way or the other with no warning.

Q Is the SPDR S&P 500 ETF (SPY) put spread, correct?

A: Yes, we had the November $400-$410 vertical bear put spread, which we just sold for a nice profit.

Q: I missed the LEAPS on J.P. Morgan (JPM) which has already doubled in value since last month, will we get another shot to buy?

A: Well you will get another shot to buy especially if another major selloff develops, but we’re not going down to the old October lows in the financial sector. I believe that a major long-term bull move has started in financials and other sectors, like healthcare. You won’t get the October lows, but you might get close to them.

Q: I’m waiting for a dip to get into Eli Lilly (LLY), but there are no dips.

A: Buy a little bit every day and you’ll get a nice average in a rising market. By the way, I just added Eli Lilly to my Mad Hedge long-term model portfolio, which you received on Thursday.

Q: Any thoughts about the conclusion of the Twitter deal and how it will affect tech and social media?

A: So far all of the indications are terrible. Advertisers have been canceling left and right, hate speech is up 500%, and Elon Musk personally responded to the Pelosi assassination attempt by trotting out a bunch of conspiracy theories for the sole purpose of raising traffic and not bringing light to the issue. All indications are bad, but I've been with Elon Musk on several startups in the last 25 years and they always look like they’re going bust in the beginning. It’s not even a public stock anymore and it shouldn’t be affecting Tesla (TSLA) prices either, which is still growing 50% a year, but it is.

Q: In terms of food commodities for 2023, where are prices headed?

A: Up. Not only do you have the war in Ukraine boosting wheat, soybean, and sunflower prices, but every year, global warming is going to take an increasing toll on the food supply. I know last summer when it hit 121 degrees in the Central Valley, huge amounts of crops were lost due to heat. They were literally cooked on the vine. We now have a tomato shortage and people can’t make pasta sauce because the tomatoes were all destroyed by the heat. That’s going to become an increasingly common issue in the future as temperatures rise as fast as they have been.

Q: Do I trade options in Alphabet (GOOG) or Alphabet (GOOGL)?

A: The one with the L is the holding company, the one without the L is the advertising company and the stock movements are really identical over the long term, so there really isn’t much differentiation there.

Q: Why can’t inflation be brought down by increasing the supply of all goods?

A: Because the companies won’t make them. The companies these days very carefully manage output to keep prices as high as possible. It’s not only the energy industry that does that but also all industries. So those in the manufacturing sector don’t have an interest in lowering their prices—they want high prices. If they see the prices fall, they will cut back supply.

Q: What do you think about growth plays?

A: As long as interest rates are rising, growth will lag and value will lead, and that has been clear as day for the last month. This is why we have an overwhelming value tilt to our model portfolio and our recent trade alerts. They’ve all been banks—JP Morgan (JPM), Bank of America (BAC), Citigroup (C), plus Berkshire Hathaway (BRK) and Visa (V) and virtually nothing in tech.

Q: I don’t know how to execute spread trades in options so how do I take advantage of your service?

A: Every trade alert we send out has a link to a video that shows you exactly how to do the trade. I have to admit, I’m not as young as I was when I made the videos, but they’re still valid.

Q: Is the US housing market about to crash?

A: There is a shortage of 10 million houses in the US, with the Millennials trying to buy them. If you sell your house now, you may not be able to buy another one without your mortgage going from 2.75% to 7.75%—that tends to dissuade a lot of potential selling. We also have this massive demographic wave of 85 million millennials trying to buy homes from 65 million gen x-ers. That creates a shortage of 20 million right there. That's why rents are going up at a tremendous rate, and that's why house prices have barely fallen despite the highest interest rates in 20 years.

Q: If we get good news from the Fed, should we invest in 3X ETFs such as the ProShares UltraPro QQQ (TQQQ)?

A: No, I never invest in 3X ETFs, because they are structured to screw the investor for the benefit of the issuer. These reset at the close every day, so do 2 Xs and not more. If you're not making enough money on the 2Xs, maybe you should consider another line of business.

Q: Do you think BlackRock Corporate High Yield Fund (HYT) will show the pain of slights because of their green positioning?

A: No I don’t, if anything green investing is going to accelerate as the entire economy goes green. And you’ll notice even the oil companies in their advertising are trying to paint themselves as green. They are really wolves in sheep’s clothing. They’ll never be green, but they’ll pretend to be green to cover up the fact that they just doubled the cost of gasoline.

Q: Where do you find the yield on Blackrock?

A: Just go to Yahoo Finance, type in (BLK), and it will show the yield right there under the product description. That’s recalculated by algorithms constantly, depending on the price.

Q: Do you like Cameco (CCJ)?

A: Yes, for the long term. Nuclear reactors have been given an extra five years of life worldwide thanks to the Russian invasion of Ukraine. Even Japan is opening theirs.

Q: Should I short the US dollar (UUP) here?

A: The answer is definitely maybe. I would look for the dollar to try to take one more run at the highs. If that fails, we could be beginning a 10-year bear market in the dollar, and bull market in the Japanese yen, Australian dollar, British pound, and euro. This could be the next big trade.

Q: What is your outlook on Real Estate Investment Trusts (REITs) now?

A: I think it looks great. REITs are now commonly yielding 10%. The worst-case scenario on interest rates has been priced in—buying a REIT is essentially the same thing as buying a treasury bond, but with twice the leverage, because they have commercial credits and not government credits. We’ll be doing a lot more work on REITS. We also have tons of research on REITS from 12 years ago, the last time interest rates spiked. I'll go in and see who’s still around, and I'll be putting out some research on it.

Q: How do you see the price development of gold (GLD)?

A: Lower—the charts are saying overwhelmingly lower. Gold has no place in a rising interest rate world. At least silver (SLV) has solar panel demand.

Q: Do you have any fear of Korea going into IT?

A: Yes, they will always occupy the low end of mass manufacturing, and you can see that in the cellphone area; Samsung actually sells more phones than Apple, but they’re cheaper phones with lower-end lagging technology, and that’s the way it’s always going to be. They make practically no money on these.

Q: When can we get some more trade alerts?

A: We are dead in the middle of my market timing index, so it says do nothing. I’m looking for either a big move down or big move up to get back into the market. This is a terrible environment to chase trades when you're trading, so I'm going to wait for the market to come to me.

Q: What about water as an investment? The Invesco Water Resources ETF (PHO)?

A: Long term I like it. There’s a chronic shortage of fresh water developing all over the world, and we, by the way, need major upgrades of a lot of water systems in the US, as we saw in Jackson, MS, and Flint, MI.

Q: Will REITs perform as well as buying rental properties over the next 10 to 20 years?

A: Yes, rental properties should do very well, as long as you’re not buying any city that has rent control. I have some rental properties in SF and dealing with rent control is a total nightmare, you’re basically waiting for your tenants to die before you raise the rent. I don’t think they have that in Nevada. But in Las Vegas, you have the other issue that is water. I think the shortage of water will start to drag on real estate prices in Las Vegas.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log on to www.madhedgefundtrader.com go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Tough Market

Global Market Comments

October 7, 2022

Fiat Lux

Featured Trade:

(OCTOBER 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (PLTR), (UUP), (ROM), (USO), (ARKK), (ROKU)

Below please find subscribers’ Q&A for the October 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Is the final low in, or could we retest yet again (SPY)?

A: We could retest yet again, but it’s very important to notice that the marginal new lows are very small. The low we had on Friday, the last day of September and Q3, was only 800 points lower than the low we had in June—you had to work 4 months just to get a new low of only 800 points. So I think that's the way it's going to go. If we do get new lows, it’ll be incremental new lows—we’re not crashing to 3,000 or anything like that.

Q: What do you think Tesla (TSLA) will bottom at in the short term?

A: $200 or $210. The Tesla deal is a disaster for Elon Musk. It will amount to a huge diversion of management time; he’s going to be facing regulatory hurdles, and even though he said we’re going ahead for the deal, a lot of people still don’t believe it because the financing for the deal may have vaporized in the massive increase in interest rates that has occurred since February. So, there are still a lot of non-believers in this deal. I’d rather have him making solar panels, electric cars and launching rockets, not getting into the social media morass and taking over a broken company. The shareholders clearly don’t like it either, taking the shares down $30 in two days. By the way, if you look at the charts, you notice that people were front-running the Twitter deal by dumping Tesla stock the day before. So yes, it kind of peed on our Tesla parade for the short term; long term it keeps going up and the bad news is in the price.

Q: How do we get the concierge service?

A: Just contact customer support at support@madhedgefundtrader.com or call (347) 480-1034.

Q: Have you revised Tesla’s (TSLA) price target?

A: No, not the long-term ones, just the short-term ones.

Q: Is it possible that bonds are bottoming here, even if we expect further Fed rate rises?

A: Yes, the Fed only has control of overnight rates, and those are rising. In fact, overnight rates are now higher than 10-year rates, and could go much higher still—that's called inversion of the yield curve. We’re almost certainly getting another 150-basis point rise in overnight rates. 10-year bonds or 20-year bonds could well stay around this level, or maybe just a little bit lower. So yes, the bond short is gone. It worked great for us for 2.5 years, we caught a 43% decline in the TLT, but it’s game over. Time to find other trades, like buying stocks.

Q: Does Elon Musk have to sell more Tesla to buy more Twitter?

A: That is the big question being asked today because he already sold $16 billion worth of stock in Tesla to cover the Twitter purchase this year. With the debt markets having fundamentally changed in the last 6 months, the question is: does he have to raise more equity (i.e. sell more Tesla), or can he bring in other equity investors? Hopefully, if he does have to sell more Tesla, it’s not very much—it’s a $44 billion deal and he’s already put $16 billion into it, so maybe he raises another $6 billion to get up to a 50% control level, which the market can easily handle in a day or two. He’s handled all of his past Tesla share sales fairly easily, and he tends to do these at market tops when demand for the shares is overwhelming. Longer term, the much greater demand for selling Tesla shares will come from the equity raises he will need to do to build another six Tesla factories around the world. That could be anywhere from $400 billion to $800 billion, so that will be the much larger cash call, but those are years off at best.

Q: With so many big techs breaking down, how should we play the (ROM) (ProShares Ultra Technology ETF)?

A: From the long side is how you play it. But you really need these capitulation days, especially if you’re involved in 2X ETFs. There is a spectacular play setting up for the (ROM) because it’ll go from $24 (or whatever the final bottom is) to $100 in the next upcycle, so that is a great leverage play that you really want to get involved in.

Q: If I don’t have time to babysit my portfolio, am I better in LEAPS or physical stocks?

A: Well the LEAPS I’m putting out now have a 2 years 4 months expiration date, so you can literally just buy them and forget about them. On the other hand, if we don’t get an economic recovery in 2 years and 4 months, you’re better off buying stocks outright on 2:1 margin. You make less profit, but if we don’t get a recovery for 3, 4, 5 years, then you have no expiration problem with stocks, as opposed to with LEAPS. Now, there are ways to trade around your LEAPS, like financing the long and by shorting puts and getting in for zero, but that requires smaller positions because you have to maintain the margin for the short put side. So, if you want to play it safe, buy the stocks. You can even handle a lost decade with stocks, especially if their dividend pays. With LEAPS, you need a fairly immediate economic recovery, which we should get, especially if the Fed lowers interest rates next year, which it should.

Q: What is your view on the US dollar (UUP)?

A: The dollar seems close to peaking right around here. It will peak on the last day that the Fed raises interest rates, which could be on December 14th. In fact, they may not even wait until then. Depending on the inflation rate, they could only do a quarter or a half-point rate rise in December, thus giving the market their signal that way. Or not do it at all, and the sudden selloff that we had in the dollar, and the stabilization of bonds we had last week is telling you that’s on the table as a possibility. So, we saw really important moves for long-term trend considerations in the markets since last week.

Q: Time for Palantir (PLTR)?

A: No, because the CEO doesn’t give a damn about his stock, and the stock reacts accordingly. I gave up on Palantir for that reason.

Q: How do you see the Ukraine/Russia situation developing?

A: It drags on for another year, Russia keeps losing and throwing men into the meat grinder until Putin gets removed, which should happen next year at which point oil prices collapse. That may be why he blew up the Nordstream One pipeline, to tie the hands of a future Russian government.

Q: Is it safe to buy 30-day Treasury bills in November going into the next F1C meeting?

A: Yes, because they essentially have no risk—that’s basically a cash type investment. And if your broker goes bust you can just force them to hand over your Treasury bonds and not get tied up in any three-year bankruptcy proceeding. It’s an asset, not cash.

Q: Will it be time to buy LEAPS on the next market selloff?

A: Absolutely, yes.

Q: Do you believe Putin would use nukes?

A: No I don’t, because the radioactive cloud would fall back on him immediately. There are very few people who are both stock market experts and nuclear weapons experts; I happen to be one of those—probably the only one in the world in fact—because of my time spent with the atomic energy commission at the Nuclear Test Site in Nevada. The problem with bombing your next-door neighbor with nukes is that the nuclear fallout comes right back on you the next day. Most of Russia’s nukes don’t even work, they only have a handful that actually does, and if he does use one, I bet it would be a tiny one just to demonstrate that he has a working nuke—like just a one-megaton one as opposed to Hiroshima which was 20 kilotons. Or he could drop it in the Black Sea or do an above-ground test at their old nuclear test site that wouldn’t kill anyone, just to show that he has working nukes. I don’t think he will, because we would react in kind in twice the size.

Q: Time to buy ARK Innovation ETF (ARKK)?

A: You might start with a small starter position, just to get it into your portfolio so you remember to buy it on the next dip. Cathy Woods’s leverage in this fund is tremendous. You really want to own it at a market bottom, but picking the actual bottom is going to be tough. One way to achieve this is to just go out and buy Tesla—that way you don’t have to pay the management fee—or buy the top 5 holdings in ARK directly, which includes Roku (ROKU) among others. So yes, I’m watching it; I prefer buying things on the way up and missing the first 10% than to catch a falling knife, and boy has this thing been a falling knife this year.

Q: Do you like biotech here?

A: Absolutely; please subscribe to the Mad Hedge Biotech Letter for biotech recommendations plus LEAPS on biotech plays by clicking here.

Q: Energy is still the best sector now?

A: Yes, but for how long? You don’t want to be left standing when the music stops playing, and that is imminent in the oil industry. It will be illegal to sell gasoline cars in California after 2035, and gas makes up half the oil use in the US.

Q: Did you know that oil reserves (USO) are the lowest since 1984?

A: Yes, I think you may have read that in my newsletter, and that’s because of Biden’s efforts to reduce US gasoline prices through a million barrel per day release from the strategic petroleum reserves in Texas and Louisiana. If we are a net energy producer, why do we even have reserves? It’s an out-of-date holdover from the Cold War.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tokyo 1975

Global Market Comments

October 3, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or BET THE RANCH TIME IS APPROACHING),

(SPY), (VIX), (UUP), (TSLA), (RIVN), (USO), (TLT), (FCX), (SPY), (NVDA), (BRKB)

September is notorious as the worst month of the year for the market. Boy, did it deliver, down a gut busting 9.7%!

As for the Mad Hedge Fund Trader, September was one of the best trading months of my 54-year career. But then I knew what was coming.

So did you.

With some of the greatest market volatility in market history, my September month-to-date performance exploded to exactly +9.72%.

I used last week’s extreme volatility and move to a Volatility Index (VIX) of $34 to add longs in Freeport McMoRan (FCX), S&P 500 (SPY), NVIDIA (NVDA), and Berkshire Hathaway (BRKB). I added shorts in the (SPY) and the (TLT). That takes me to 70% long, 20% short, and 10% cash. I am holding back my cash for any kind of rally to sell into.

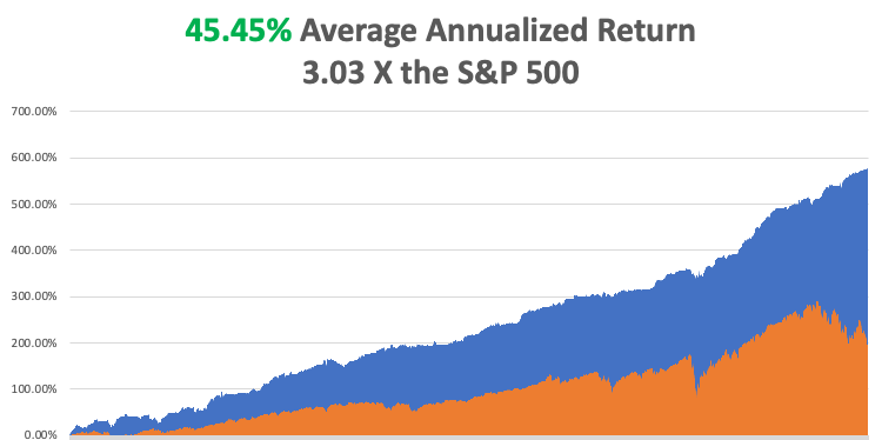

My 2022 year-to-date performance ballooned to +69.68%, a new high. The Dow Average is down -23.44% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky high +80.08%.

That brings my 14-year total return to +582.24%, some 3.03 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.45%, easily the highest in the industry.

It was in May of 2020 when 34 of my clients became millionaires through buying TESLA at precisely the right time…

Well, the stars have aligned once again!!!!

In my TESLA free report, I list 10 reasons I’d tell my grandmother to mortgage her house and go all in.

Go to MADHEDGERADIO.com and download my “Tesla takes over the world” free report…that’s

madhedgeradio.com.

At the end of the month, the market was down six days in a row. That has only happened 20 times since 1950.

However, bet the ranch time is approaching. It’s time to start scaling in in a small way into your favorite long term names where the value is the greatest.

The Fed has taken away the free put that the stock market has enjoyed for the last 13 years. Now, it’s the bond market that has the free put. Hint: always own the market where the Fed is giving you free, unlimited downside protection.

People often ask what I do for a living. I always answer, “Talking people out of selling stocks at the bottom.” Here is the cycle I see repeating endlessly. They tell me they are long term investors. Then the markets take a sudden dive, like to (SPX) $3,300, a geopolitical event takes place, and the TV networks only run nonstop Armageddon gurus. They sell everything.

Then the market turns sharply, and they helplessly watch stocks soar. When they get frustrated enough, they buy, usually near a market top.

Sell low, buy high, they are perfect money destruction machines. And they wonder why they never make money in the stock market!

If any of this sounds familiar you have a problem and need to read more Mad Hedge newsletters. The people who ignore me I never hear from again. Those who follow me stick with me for decades.

Don’t make the mistake here of only looking at real GDP growth which, in recessions, is always negative. Nominal GDP is growing like a bat out of hell, 12% in 2021 and 8% in 2022. That’s 20% in two years, nothing to be sneezed at.

The problem is that all economic data has been rendered useless by the pandemic, even for legitimate and accomplished Wall Street analysts. The US economy was put through a massive restructuring practically overnight, the long-term consequences of which nobody will understand for years. Typical is the recently released Consumer Price Index, which said that real estate prices are rocketing, when in fact they are crashing.

A lot of people have asked me about the comments from my old friend, hedge fund legend Paul Tudor Jones, that the Dow Average would show a zero return for the next decade.

For Paul to be right, technological innovation would have to completely cease for the next decade. Sitting here in the middle of Silicon Valley, I can tell you that is absolutely not happening. In fact, I’m seeing the opposite. Innovation is accelerating at an exponential rate. For goodness sakes, Apple just brought out a satellite phone with its iPhone 14 pro for a $100 upgrade!

Remember, Paul got famous, and rich, from the trades he did 40 years ago with me, not because of anything he did recently. Paul has in fact been bearish for at least five years.

Still, we have a long way to go on earnings multiples. The trailing S&P 500 market multiple is now at 19. The historic low is at 15. Current earnings are $245 per (SPX) share. The 3,000 target the bears are shouting from the rooftops assumes that a severe recession takes earnings down to $200 a share ($3,000/$200 = 15X).

I don’t think earnings will get that bad. Big chunks of the economy are still growing nicely. Companies are commanding premium prices for practically everything. There is no unemployment because the jobs market is booming.

That suggests to me a final low in this market of $3,000-$3,300. That means you can buy 15%-20% deep in-the-money vertical bull call spreads RIGHT HERE and make a killing, as Mad Hedge has done all year.

Let me plant a thought in your mind.

After easing for too long, then tightening for too long, what does the Fed do next? It eases for too long….again. You definitely want to be long stocks when that happens, which will probably start some time next year.

Let me give you one more data point. The (SPY) has been down 7% or more in September only seven times since 1950. In six of the Octobers that followed, the market was up 8% or more.

Sounds like it’s time to bet the ranch to me.

Capitulation Indicators are Starting to Flash. Cash levels at mutual funds are at all-time highs. The Bank of America Investors Survey shows the high number of managers expecting a recession since the 2020 pandemic low, the last great buying opportunity. Commercial hedgers are showing the largest short positions since 2020. And of course, my old favorite, the Volatility Index (VIX) hit $34.00 on Tuesday. The risks of NOT being invested are rising.

Bank of England Moves to Support a Crashing Pound (FXB), by flipping from a seller to a buyer in the long-dated bond market, thus dropping interest rates. The move is designed to offset the new Truss government’s plan to cut taxes and boost deficit spending. The BOE also indicated that interest rate hikes are coming. The bond vigilantes are back.

Here’s the Next Financial Crisis, massive unrealized losses in the bond market. The (TLT) alone has lost 43% in 2 ½ years. Apply that to a global $150 trillion bond market and it adds up to a lot of money. Anybody who used leverage is now gone. How many investors without swimsuits will be discovered when the tide goes out?

Will the Strong Dollar (UUP) Do the Fed’s Work, forestalling a 75-basis point rate rise? It will if the buck continues to appreciate at the current rate, up a record five cents against the British pound, taking it to a record low of $1.03. Such is the deflationary impact of weak foreign currencies, which are seriously eating into US multination earnings.

Weekly Jobless Claims Hit Five-Month Low at 195,000, far below expectations. If the Fed is waiting for the job market to roll over before it quits raising interest rates, it could be a long wait.

EV Sales to Hit New All-Time High in 2022, to 13% of global new vehicle sales, up from 9% last year. The IEA expects this figure to reach 50% by 2030. That works out to 6.6 million EVs in 2021, 9.5 million in 2022, and 36 million by 2030. Buy (TSLA), the world’s largest EV seller, and (RIVN), the fastest grower in percentage terms, on dips.

EVs Take 25% of China New Vehicle Sales, and Tesla’s Shanghai factory is a major participant. Tesla just double production there. Some 403,000 EVs were sold in China in May alone. China is also ramping up its own EV production, up 183% YOY. China is much more dependent on imported oil than other large nations, most of which goes to transportation. Global EV production is expected to soar from 8 to 60 million vehicles in five years and Tesla is the overwhelming leader. Buy (TSLA) on dips again.

Oil (USO) Hits New 2022 Low at $78 a Barrel, cheaper than pre–Ukraine War prices, thanks to exploding recession fears. Is Jay Powell the most effective weapon against Russia with his most rapid interest rate rises in history?

Consumer Sentiment Hits Record Low at 59.1 according to the University of Michigan. That’s worse than the pandemic low and the 2009 Great Recession low. It could be that politics has ruined this data source making everyone permanently negative about the future. Inflation at a 40-year high isn’t helping either, nor is the prospect of nuclear war.

Case Shiller Delivers a Shocking Fall, down from 18.7% to 16.1% in June. The other shoe is falling with the sharpest drop in this data series in history. Tampa was up (31.8%), Miami (31.7%), and Dallas (24.7%). Many more declines to come.

30-Year Fixed Rate Mortgage Hits 7.08%, up from 2.75% a year ago. You can kiss those retirement dreams goodbye. It has been the sharpest rise in mortgage rates in history. Real estate has just become an all-cash market. That screeching juddering sound you hear is the existing home market shutting down.

Pending Home Sales Drop, down 2.0% in August on a signed contract basis. Sales are down for the third month in a row and are off 24% YOY. Only the west gained. Mortgage interest rates are now at 20-year highs. Buyers catching recession fears are breaking contracts and walking away from deposits.

Stock Crash Wipes Out $9 Trillion in Personal Wealth, which is the fall in equity holdings and mutual funds as of the end of June. The drop has been from $42 to $33 trillion. The bad news: it’s still going down, putting a dent in consumer spending.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil in a sharp downtrend and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 3 at 8:30 AM, the ISM Manufacturing PMI for September is released.

On Tuesday, October 4 at 7:00 AM, the JOLTS Report for private job openings for September is out.

On Wednesday, October 5 at 7:00 AM, ADP Private Employment Report for September is published.

On Thursday, October 6 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, October at 8.30 AM, the Nonfarm Payroll Report for September is disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, while working for The Economist magazine in London, I was invited to interview some pretty amazing people: Margaret Thatcher, Ronald Reagan, Yasir Arafat, Zhou Enlai.

But one stands out as an all time favorite.

In 1982, I was working out of the magazine’s New York Bureau off on Third Avenue and 47th Street, just seven blocks from my home on Sutton Place, when a surprise call came in from the editor in London, Andrew Knight. International calls were very expensive then, so it had to be important.

Did anyone in the company happen to have a US top secret clearance?

I answer that it just so happened that I did, a holdover from my days at the the Nuclear Test Site in Nevada. “What’s the deal,” I asked?

A person they had been pursuing for decades had just retired and finally agreed to an interview, but only with someone who had clearance. Who was it? He couldn’t say now. I was ordered to fly to Los Angeles and await further instructions.

Intrigued, I boarded the next flight to LA wondering what this was all about. What I remember about that flight is that sitting next to me in first class was the Hollywood director Oliver Stone, a Vietnam veteran who made the movie Platoon. When Stone learned I was from The Economist, he spent the entire six hours grilling me on every conspiracy theory under the sun, which I shot down one right after the other.

Once in LA, I checked into my favorite haunt, the Beverly Hills Hotel, requesting the suite that Marilyn Monroe used to live in. The call came in the middle of the night. Rent a four-wheel drive asap and head out to a remote ranch in the mountains 20 miles east of Santa Barbara. And who was I interviewing?

Kelly Johnson from Lockheed Aircraft (LMT).

Suddenly, everything became clear.

Kelly Johnson was a legend in the aviation community. He grew up on a farm in Michigan and obtained one of the first masters degrees in Aeronautical Engineering in 1933 at the University of Michigan.

He cold called Lockheed Aircraft in Los Angeles begging for a job, then on the verge of bankruptcy in the depths of the Great Depression. Lockheed hired him for $80 a month. What was one of his early projects? Assisting Amelia Earhart with customization of her Lockheed Electra for her coming around-the-world trip, from which she never returned.

Impressed with his performance, Lockheed assigned him to the company’s most secret project, the twin engine P-38 Lightning, the first American fighter to top 400 miles per hour. With counter rotating props, the plane was so advanced that it killed a quarter of the pilots who trained on it. But it allowed the US do dominate the air war in the Pacific early on.

Kelley’s next big job was the Lockheed Constellation (the “Connie” to us veterans), the plane that entered civil aviation after WWII. It was the first pressurized civilian plane that could fly over the weather and carried an astonishing 44 passengers. Howard Hughes bought 50 just off of the plans to found Trans World Airlines. Every airline eventually had to fly Connie’s or go out of business.

The Cold War was a golden age for Lockheed. Johnson created the famed “Skunkworks” at Edwards Air Force base in the Mojave Desert where America’s most secret aircraft were developed. He launched the C-130 Hercules, which I flew in Desert Storm, the F-104 Starfighter, and the high altitude U-2 spy plane.

The highlight of his career was the SR-71 Blackbird spy plane where every known technology was pushed to the limit. It could fly at Mach 3.0 at 100,000 feet. The Russians hated it because they couldn’t shoot it down. It was eventually put out of business by low earth satellites. The closest I ever got to the SR-71 was the National Air & Space Museum in Washington DC at Dulles airport where I spent an hour grilling a retired Blackbird pilot.

Johnson greeted me warmly and complimented me on my ability to find the place. I replied, “I’m an Eagle Scout.” He didn’t mind chatting as long as I accompanied him on his morning chores. No problem. We moved a herd of cattle from one field to another, milked a few cows, and fertilized the vegetables.

When I confessed to growing up on a ranch, he really opened up. It didn’t hurt that I was also an engineer and a scientist, so we spoke the same language. He proudly showed off his barn, probably the most technologically advanced one ever built. It looked like a Lockheed R&D lab with every imageable power tool. Clearly Kelley took work home on weekends.

Johnson recited one amazing story after the other. In 1943, the British had managed to construct two Whittle jet engines and asked Kelly to build the first jet fighter. The country that could build jet fighters first would win the war. It was the world’s most valuable machine.

Johnson clamped the engine down to a test bench and fired it up surrounded by fascinated engineers. The engine immediately sucked in a lab coat and blew up. Johnson got on the phone to England and said “Send the other one.”

The Royal Air Force placed their sole remaining jet engine on a plane which flew directly to Burbank airport. It arrived on a Sunday, so the scientist charged with the delivery took the day off and rode a taxi into Hollywood to sightsee.

There, the Los Angeles police arrested him for jaywalking. In the middle of WWII with no passport, no ID, a foreign accent, and no uniform, they hauled him straight off to jail.

It took two days for Lockheed to find him. Johnson eventually attached the jet engine to a P-51 Mustang, creating the P-80, and eventually the F-80 Shooting Star (Lockheed always uses astronomical names). Only four made it to England before the war ended. They were only allowed to fly over England because the Allies were afraid the Germans would shoot one down and gain the technology.

But the Germans did have one thing on their side. The Los Angeles Police Department delayed the development of America’s first jet fighter by two days.

Germany did eventually build 1,000 Messerschmitt Me 262 jet fighters, but too late. Over half were destroyed on the ground and the engines, made of steel and not the necessary titanium, only had a ten hour life.

That evening, I enjoyed a fabulous steak dinner from a freshly slaughtered steer before I made my way home. I even helped Kelly slaughter the animal, just like I used to do on our ranch in Montana. Steaks are always better when the meat is fresh and we picked the best cuts. I went back to the hotel and wrote a story for the ages.

It was never published.

One of the preconditions of the interview was to obtain prior clearance from the National Security Agency. They were horrified with what Johnson had told me. He had gotten so old he couldn’t remember what was declassified and what was still secret.

The NSC already knew me well from our previous encounters, but MI-6 showed up at The Economist office in London and seized all papers related to the interview. That certainly amused my editor.

Johnson died at age 80 in 1990. As for me, it was just another day in my unbelievable life.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

SR-71 Blackbird

My Former Employer

Global Market Comments

August 15, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or WHAT THE MARKET IS REALLY DISCOUNTING NOW),

(SPY), (TLT), (AAPL), (AXP), (KO), (XOM). (TBT), (SNOW), (NFLX), (ARKK), (ETHE),

(NLR), (CCR), CORN), (WEAT), (SOYB), (DBA), (UUP), (FXA), (FXC), (BA), (TSLA)

After a half-century in the markets, I have noticed that it is the investors with the correct long-term views who make the biggest money. My favorite example is my friend, Warren Buffet, who doesn’t care if an investment turns good in five minutes or five years.

Buffet’s Berkshire Hathaway (BRKB) is the largest outside investor in Apple (AAPL). And guess what his cost has been? By the time you add up the compounded dividends he has collected since he started buying the stock in 2011, it's zero. The value today? $15.5 billion.

Buffet didn’t buy Apple for its hardware, iPhone, or iTunes. He bought it for the brand, which has improved astronomically. Look at Berkshire’s portfolio and it is packed with brands, like American Express (AXP), Coca-Cola (KO), and Exxon (XOM).

When did Buffet last buy Apple? In May when it hit $130.

That’s why Warren Buffet is Warren Buffet and you are you.

While the inflation news last week has been great and it is likely to get better, I believe that investors are missing the bigger, more important long-term picture.

The fact is that markets are now discounting an earlier than expected end to the Ukraine War, much earlier.

I get constant updates on the war from the Joint Chiefs of Staff, Britain’s Defense Committee, and NATO headquarters and I can tell you that the war has taken a dramatic turn in Ukraine’s favor just in the last two weeks.

Russian casualties have topped 80,000, nearly half the standing army. They have lost 2,200 of their 2,800 operational tanks. Some 120 front line aircraft have been destroyed. This week, Ukraine attacked the principal Russian air base in Crimea, leaving the smoking ruins of seven more aircraft there.

Russia is in effect fighting a modern digitized war with 50-year-old Cold War weapons and it isn’t working. Its generals have no experience fighting wars against determined opposition. Putin would do better listening to the retired generals on CNN for military advice.

America’s High HIMARS (the M142 High Mobility Artillery Rocket System) has become the Stinger missile of this war. The Lockheed Martin (LMT) factory in Camden, Arkansas that makes these missiles is running 24/7 on doubled orders.

The sanctions against Russia have been wildly successful. The Russian economy is utterly collapsing. What oil they are selling now is at half price. Aircraft are being cannibalized for parts to keep others flying. Much of the educated middle class has fled the country. Draft dodging is rampant.

What does all this mean for you and me?

The commodity price spike the war prompted has ended and most are now in steep downtrends. Gold (GLD), where the Russians were major buyers, has been flat as a pancake. This has put our inflation numbers into freefall. Interest rate fears peaked in June and are now in the rear-view mirror.

As is always the case, markets have seen these developments and correctly ascertained their consequences far before we humans did (except for maybe me). It has been no surprise that they have been tracking the Russian defeat day by day and have been on an absolute tear since June 15.

Even small techs suffering 18-month bear markets have now begun major recoveries, with companies like Snowflake (SNOW), up 50%, Netflix (NFLX), up 39%, and Cathie Wood’s Innovation Fund (ARKK) up 57%. Even crypto has returned from the grave, with Ethereum (ETHE) up an eye-popping 105%.

But don’t go gaga over stocks just yet.

The Fed ramps up quantitative tightening in September to $95 billion a month and will deliver another interest rate hike. That's why I am running a double short in the bond market (TLT), (TBT) once again.

We also have the midterms to worry about which, with recent developments, promise to be more contentious than ever. Look for another round of tiring new election fraud claims.

That’s great because these events will give us good entry points lower down for trade alerts, not the short-term top we are looking at right now.

It helps that with ten-year US Treasury yields at 2.80%, it has an effective price earning multiple of 37, while stocks growing earnings at 10% a year boast a price earnings multiple of only 16. That sets up a massive, long stock/short bond trade which Mad Hedge will be pushing well on into 2023.

And you know what?

The smart guys I know in the hedge fund community are starting to model for the next Fed interest rate CUT. Markets will love it and discount this far in advance.

If you want to get on the train with me before it leaves the station, just keep reading this newsletter.

Yes, markets are now being driven by rate cuts and peace prospects, not rate rises and war!

Your retirement fund will love it.

I just thought you’d like to know.

CPI Dives to 8.5%, down 0.6% in July. The peak is in, and stocks rallied 500. Look for another drop in August, with gasoline prices falling daily. The 800-pound gorilla in the room has exited.

The Producer Price Index Dives 0.5%, confirming last week’s weak CPI number. And many core prices are indicating that we will get another drop when the August numbers are reported in September. It was worth another 300-point rally in the Dow Average, which is getting seriously overbought.

Consumer Inflation Expectations dive to 6.2% for the coming year and only 3.2% for three years. according to a New York Fed Survey. Expectations for food costs saw the largest decline. The CPI is out on Wednesday. No doubt a media onslaught over a coming recession has a lot to do with it.

Elon Musk Sells $6.9 billion worth of Tesla (TSLA) Stock, explaining the $100 drop in the shares last week. Ostensibly, this is to pay for Twitter if he loses his court case. Musk clearing took advantage of a 60% rise in (TSLA) to head off distress sales in the future. Musk also opened the door to share buy backs in the future. Buy (TSLA) on dips.

85,000 IRS Agents are Headed Your Way, but only if the government can hire them and only if you are a billionaire or a profitable large oil company. The rest of us will be ignored by this unpublicized portion of the Biden inflation bill.

US Dollar (UUP) Takes a Hit on CPI Report, which effectively showed that the US saw deflation in July. The greenback is pulling back the 20-year highs which gave you the cheapest European vacation in your lives. The prospect of interest rates rising at a slower pace is dollar negative. Buy (FXA) and (FXC) on dips.

Boeing (BA) Delivered its First 787 Dreamliner in a year, after long-awaited regulatory approval. The monster 30% rise in the shares off the June low predicted as much. A global aircraft shortage helps. Airbus is going to have to start earnings its money again. Keep buying (BA) on dips.

Weekly Jobless Claims Pop 12,000 to 262,000, a new high for the year. It’s not at concerning levels yet but is definitely headed in the wrong direction. Maybe it’s just a summer slowdown? Maybe not.

Shipping Container Charges are Plunging Everywhere, except in the US, which currently has the world’s strongest economy. It’s a sign that global supply chain problems are easing. But the US leads the world in demurrage, or delays, with New York the worst, followed by Long Beach.

Import Prices are Plunging, thanks to a super strong dollar, taking more pressure off of inflation. They fell 1.4% in July according to the Department of Labor. Easing supply chain problems are helping. Biden has had the run of the table for months now

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil prices now rapidly declining, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

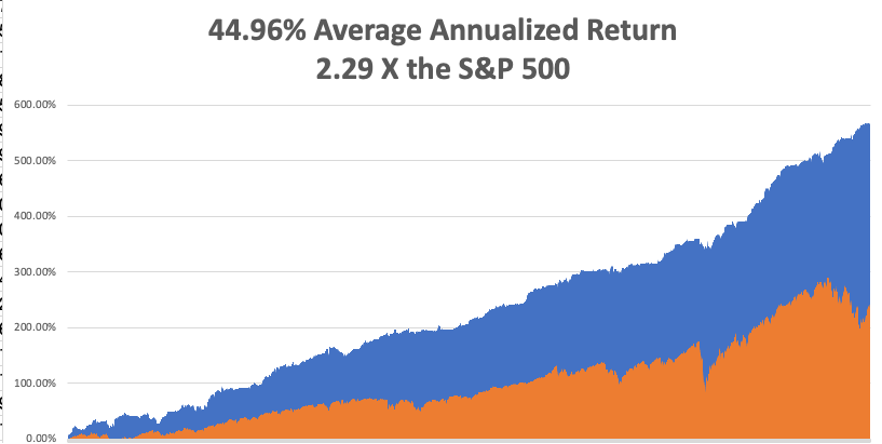

My August performance climbed to +2.14%. My 2022 year-to-date performance ballooned to +56.97%, a new high. The Dow Average is down -7.0% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 74.76%.

That brings my 14-year total return to 569.53%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.96%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 93 million, up 300,000 in a week and deaths topping 1,037,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, August 15 at 8:30 AM EDT, the New York Empire State Manufacturing Index for August is released.

On Tuesday, August 16 at 8:30 AM, the Housing Starts for July are out.

On Wednesday, August 17 at 8:30 AM, Retail Sales for July are published. At 11:00 AM the Fed Minutes from the last meeting are printed.

On Thursday, August 18 at 8:30 AM, Weekly Jobless Claims are announced. Existing Home Sales for July are announced.

On Friday, August 19 at 2:00 the Baker Hughes Oil Rig Count is out.

As for me, while we’re all waiting for the dog days of August to end, it is time to reminisce about my old friend George Schultz who passed away last year at the age of 101.

My friend was having a hard time finding someone to attend a reception who was knowledgeable about financial markets, White House intrigue, international politics, and nuclear weapons.

I asked who was coming. She said Reagan’s Treasury Secretary George Shultz. I said I’d be there wearing my darkest suit, cleanest shirt, and would be on my best behavior, to boot.

It was a rare opportunity to grill a high-level official on a range of top-secret issues that I would have killed for during my days as a journalist for The Economist magazine. I guess arms control is not exactly a hot button issue these days.

I moved in for the kill.

I have known George Shultz for decades, back when he was the CEO of the San Francisco-based heavy engineering company, Bechtel Corp in the 1970s.

I saluted him as “Captain Schultz”, his WWII Marine Corp rank, which has been our inside joke for years. Now that I am a major, I guess I outrank him.

Since the Marine Corps didn’t know what to do with a PhD in economics from MIT, they put him in charge of an anti-aircraft unit in the South Pacific, as he was already familiar with ballistics, trajectories, and apogees.

I asked him why Reagan was so obsessed with Nicaragua, and if he really believed that if we didn’t fight them there, would we be fighting them in the streets of Los Angeles as the then-president claimed.

He replied that the socialist regime had granted the Soviets bases for listening posts that would be used to monitor US West Coast military movements in exchange for free arms supplies. Closing those bases was the true motivation for the entire Nicaragua policy.

To his credit, George was the only senior official to threaten resignation when he learned of the Iran-contra scandal.

I asked his reaction when he met Soviet premier Mikhail Gorbachev in Reykjavik in 1986 when he proposed total nuclear disarmament.

Shultz said he knew the breakthrough was coming because the KGB analyzed a Reagan speech in which he had made just such a proposal.

Reagan had in fact pursued this as a lifetime goal, wanting to return the world to the pre nuclear age he knew in the 1930s, although he never mentioned this in any election campaign. Reagan didn’t mention a lot of things.

As a result of the Reykjavik Treaty, the number of nuclear warheads in the world has dropped from 70,000 to under 10,000. The Soviets then sold their excess plutonium to the US, which has generated 20% of the total US electric power generation for two decades.

Shultz argued that nuclear weapons were not all they were cracked up to be. Despite the US being armed to the teeth, they did nothing to stop the invasions of Korea, Hungary, Vietnam, Afghanistan, and Kuwait.

Schultz told me that the world has been far closer to an accidental Armageddon than people realize.

Twice during his term as Secretary of State, he was awoken in the middle of the night by officers at the NORAD early warning system in Colorado to be told that there were 200 nuclear missiles inbound from the Soviet Union.

He was given five minutes to recommend to the president to launch a counterstrike. Four minutes later, they called back to tell him that there were no missiles, that it was just a computer glitch projecting ghost images on a screen.

When the US bombed Belgrade in 1989, Russian president Boris Yeltsin, in a drunken rage, ordered a full-scale nuclear alert, which would have triggered an immediate American counter-response. Fortunately, his generals ignored him.

I told Schultz that I doubted Iran had the depth of engineering talent needed to run a full-scale nuclear program of any substance.

He said that aid from North Korea and past contributions from the AQ Khan network in Pakistan had helped them address this shortfall.

Ever in search of the profitable trade, I asked Schultz if there was an opportunity in nuclear plays, like the Market Vectors Uranium and Nuclear Energy ETF (NLR) and Cameco Corp. (CCR), that have been severely beaten down by the Fukushima nuclear disaster.

He said there definitely was. In fact, he was personally going to lead efforts to restart the moribund US nuclear industry. The key here is to promote 5th generation technology that uses small, modular designs, and alternative low-risk fuels like thorium.

Schultz believed that the most likely nuclear war will occur between India and Pakistan. Islamic terrorists are planning another attack on Mumbai. This time, India will retaliate by invading Pakistan. The Pakistanis plan on wiping out this army by dropping an atomic bomb on their own territory, not expecting retaliation in kind.

But India will escalate and go nuclear too. Over 100 million would die from the initial exchange. But when you add in unforeseen factors, like the broader environmental effects and crop failures (CORN), (WEAT), (SOYB), (DBA), that number could rise to 1-2 billion. This could happen as early as 2023.

Schultz argued that further arms control talks with the Russians could be tough. They value these weapons more than we do because that’s all they have left.

Schultz delivered a stunner in telling me that Warren Buffet had contributed $50 million of his own money to enhance security at nuclear power plants in emerging markets.

I hadn’t heard that.

As the event ended, I returned to Secretary Shultz to grill him some more about the details of the Reykjavik conference held some 36 years ago.

He responded with incredible detail about names, numbers, and negotiating postures. I then asked him how old he was. He said he was 100.

I responded, “I want to be like you when I grow up”.

He answered that I was “a promising young man.” I took that as encouragement in the extreme.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We’re Getting Pretty High

Global Market Comments

June 3, 2022

Fiat Lux

Featured Trade:

(JUNE 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(AAPL), (GOOGL), (MSFT), (JPM), (BAC), (C), (UUP), (FXA), (FXC), (EEM),

(VIX), (CRM), (AAPL), (TSLA), (COIN), (EDIT), (CRSP), (LMT), (RTX), (GD)

Below please find subscribers’ Q&A for the June 1 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: What are the 3 best stocks to own for the end of the year?

A: Apple (AAPL), Alphabet Inc. (GOOGL), and Microsoft (MSFT). Those you want to buy on meltdown days, kind of like today. Make sure you scale into these—so maybe buy 20% on every down-500-point Dow day. Eventually, you’ll end up with a pretty decent position at a market low in a stock that will double in 3-5 years.

Q: Why these three stocks?

A: Lots of reasons: They’re huge, they’re safe, two out of three pay dividends, Alphabet is about to split, and they have huge moats so nobody can get into their sectors. They have near monopolies in what they do, and they have immense cash on the balance sheet. These are the kind of stocks that portfolio managers dream about. And watch what rallied the hardest in the last dead cat bounce we had—it was these three names. That tells you that they will lead any long-term bull market in the future. These are the stocks that people want to own.

Q: What will bring your predicted second half-bull market in the stock market?

A: Inflation drops from 8% to 4%. That will happen for a couple of reasons. The year-on-year comparisons become highly favorable starting from next month when inflation started to take off a year ago. Inflation numbers are going to be climbing the wall of worry from here on out. That could get us down to 4% by the end of the year. The second reason is the Ukraine War either ends or becomes a stalemate and is no longer a factor in the global markets, and we’ve had time to replace all the Russian oil and Ukrainian wheat.

Q: Are banks positioned to benefit from the coming rally?

A: Absolutely. I think big tech and banks will be the top-performing stock sectors for the next five years because inflation will go away, recession fears will go expire, and credit quality will improve, but interest rates will remain 300 basis points higher than they were during the pandemic. Buy (JPM), (BAC), and (C) on dips.

Q: What will be the worst performing sector?

A: Energy—anything energy-related will get absolutely slaughtered, which is why I don't want to touch it with a ten-foot pole right now. That includes oil companies, exploration companies, E&P companies, and master limited partnerships, as well as coal and other natural gas stocks. So, if you’re long these names don’t forget to sit down when the music stops playing. You could get your head handed to you at the end.

Q: Can we make lower lows?

A: Yes, that’s entirely possible. Market moves are basically random when you get down to these levels— down more than 20%. And on all future downturns, I would be spending your cash going back into the market expecting a second half rally.

Q: What about green energy?

A: Unfortunately, green energy is very tied to old energy because $120 oil makes green companies much more competitive from a cost point of view. So, I’m not going to go piling into green companies right here, especially if I think oil is topping out in the near future. Buying green energy companies here is the same as buying oil at $120 a barrel.

Q: What is the best way to play the declining US dollar?

A: Buy the iShares MSCI Emerging Markets ETF (EEM). Also, the Aussie dollar (FXA) and the Canadian Dollar (FXC), which benefit tremendously from commodity prices, which will rise for another decade in a global economic recovery.

Q: Why will energy be the worst sector?

A: If you end the war in the Ukraine or you replace Russian oil, either by finding new sources of oil, getting other producers to increase production which they can do (including the US), or by accelerating the move to alternatives, then you move oil back to pre-invasion prices which were about $70 a barrel or $50 lower than they are here.

Q: Best way to hedge a falling market?

A: Do what I'm doing: keep a balanced portfolio of longs and shorts, that way you always have something that’s going up. And if you do it through the options, you have time decay working for you on both sides of the equation. If you want to go outright, buy outright puts on individual stocks because they had double the moves of the indexes. And go to my short selling school which you can find by going to my website at https://www.madhedgefundtrader.com. There’s actually 12 different ways to benefit from falling markets.

Q: How deep in the money can we go on our call spreads?

A: Wait for the Volatility Index (VIX) to go over $30, and then go 15-20% in the money. And yes, you only make 10, 15, or 20% on those positions in a month but then you put together ten of them and that adds up to quite a lot of money. You want to find the position that has the greatest probability of happening—i.e. something that’s 20% in the money. Do that when the market has just dropped 20%, which it already has, and then you have a position that has a minuscule chance of losing money.

Q: How much longer do you see this current bear market bounce lasting?

A: Until yesterday.

Q: What's your favorite commodity ETF?

A: My favorite commodity stock is Freeport McMoRan (FCX), the world’s largest copper producer. Rather than pay the extra management fees for an ETF, I prefer just to go straight to the source and buy (FCX).

Q: When do you think the Fed will pivot to dovish or neutral?

A: This summer. It’s just a question of whether it’s the July or the September meeting.

Q: When you say “buy on dips”, what does that mean? 1%, 3%, 5%?

A: Well in this market, a dip would be a retest of the previous lows which is going to be down 10% or 15% on the major positions in your portfolio. If you’re day trading, a dip is only 1%, so it really depends on your timeframe and your risk tolerance. That’s why I always tell people to scale by doing everything in incremental pieces—20%, 25%, and so on. You never know what the market’s actually going to do on a short-term basis. Randomness can’t be predicted.

Q: If you plan to enter a LEAPS on Apple, what strikes would you do?

A: Well, first of all, I want to see if Apple drops all the way to $125, which is a lot of people’s downside target. If it did, then I would do the $125/$135 call spread two years out, and that will probably double. And if it starts a long term up trend, then I’ll keep rolling up the strike prices. If, say, Apple goes to $125, you put your LEAPS on. If the stock rises to 150, then take profits on the $125/$135 and roll into the $150/$160. That’s how you can get like 1,000% returns like we got on Tesla (TESLA) a few years ago. You just keep rolling up your strike prices on every weak day and maintain your leverage.

Q: When do we bet the farms on Editas Medicine Inc. (EDIT) and Crispr (CRSP) Therapeutics?

A: Never. These are small, highly speculative companies which will make money someday, but if the someday is in five years and you’re betting the farm with a LEAPS, you lose the farm. It's going to take a long time for these smaller biotech stocks to come back. If you want to play biotech, go with the big ones like Amgen. It takes a long time to convert cutting-edge technology into profits. The big companies already have a stable of reliable money-making drugs on hand.

Q: Salesforce Inc. (CRM) is up big on earnings—what should I do with the stock?

A: Buy the dips. It’s still way, way below its all-time highs, so use the weekdays to accumulate Salesforce for the long term. It’s one of the best cloud plays out there.

Q: What do you think about NVIDIA Corporation (NVDA)?

A: I absolutely love it. It rallied 20% off the bottom. Use any other additional weak days like today to increase your position. This stock someday is worth $1,000, up from today’s $195.

Q: Do you like SPACS?

A: No, I hate them and think they’re a rip-off. And a lot of them have become totally illiquid and untradable, so you have no choice but for them to shut down and return their money if they have any left. I’ve hated SPACS from day one and people are now getting their comeuppance on these.

Q: What do you think about the weakness in Coinbase Global Inc. (COIN) down here?

A: It’s just going down with all the other high-risk, speculative, meme stock type plays, which include all of the crypto plays like Bitcoin. I would avoid all of those. You want to buy quality at the discount now, and you want to buy the Cadillacs at Volkswagen prices and leave the speculative plays for the next generation, Gen Z, who are already highly interested in stocks.

Q: What is your favorite non-US country to invest in?

A: Australia, because you get a double play there on the currency, which should go up 30% from here, and they will benefit from a global commodity boom which continues for another ten years. They pretty much sell a lot of the major commodities like iron ore, wheat, sheep, and so on. It’s also a really nice country to visit. The only negative with Australia are the sharks.

Q: Biotech takeover targets?

A: Well (EDIT) and (CRSP) would be two of them. Things in the sector are so cheap that they are all potential takeover targets. M&A (Mergers and Acquisitions) will be a major play in the biotech sector for the foreseeable future.

Q: Should we sell short the defense industry here?

A: No, even if the war ends tomorrow, you might get some profit-taking, but the fact is that long term military spending is increasing permanently. The peace dividend now has to be paid back, and that is great for all the defense companies, so I would not be shorting them. If anything, I’d be buying on dips. Buy Lockheed Martin (LMT), Raytheon (RTX), who make the Javelin antitank missile for which there is now a two-year order backlog. You can also throw in General Dynamics (GD) for good measure which builds nuclear submarines and the Stryker armored vehicle.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Keep Those Defense Plays