There was so much enthusiasm for China only a month ago.

A stimulus package was announced, a massive short-covering rally ensured, and finally, after a three-year hiatus, China was back in play. Several hedge funds announced major commitments to the Middle Kingdom.

Here we are only three weeks after the US presidential election, and China now looks so much rubble. Asst prices returned to their starting points. The hedge funds have so much mud on their faces. It’s back to a long wait.

Which gives us all plenty of time to think about what China is really all about.

I ran into Minxin Pei, a scholar at the Carnegie Endowment for International Peace, who imparted to me some iconoclastic, out-of-consensus views on China’s position in the world today.

He thinks that power is not shifting from West to East; Asia is just lifting itself off the mat, with per capita GDP at $12,969, compared to $81,695 in the US.

We are simply moving from a unipolar to a multipolar world. China is not going to dominate the world, or even Asia, where there is a long history of regional rivalries and wars.

China can’t even control China, where recessions lead to revolutions, and 30% of the country, Tibet and the Uighurs want to secede.

China’s military is almost entirely devoted to controlling its own people, which makes US concerns about their recent military build-up laughable.

All of Asia’s progress, to date, has been built on selling to the US market. Take us out, and they’re nowhere.

With enormous resource, environmental, and demographic challenges constraining growth, Asia is not replacing the US anytime soon.

There is no miracle form of Asian capitalism; impoverished, younger populations are simply forced to save more because there is no social safety net.

Try filing a Chinese individual tax return, where a maximum rate of 40% kicks in at an income of $35,000 a year, with no deductions, and there is no social security or Medicare in return.

Ever heard of a Chinese unemployment office or jobs program?

Nor are benevolent dictatorships the answer, with the despots in Burma, Cambodia, North Korea, and Laos thoroughly trashing their countries.

The press often touts the 600,000 engineers that China graduates, joined by 350,000 in India. In fact, 90% of these are only educated to a trade school standard. Asia has just one world-class school, the University of Tokyo.

As much as we Americans despise ourselves and wallow in our failures, Asians see us as a bright, shining example for the world.

After all, it was our open trade policies and innovation that lifted them out of poverty and destitution. Walk the streets of China, as I have done for four decades, and you feel this vibrating from everything around you.

I’ll consider what Minxin Pei said next time I contemplate going back into the (FXI) and (EEM).

China: Not All Its Cracked Up to Be

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/China-Parade.jpg266401Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-11-29 09:02:432024-11-29 11:36:58China's View of China

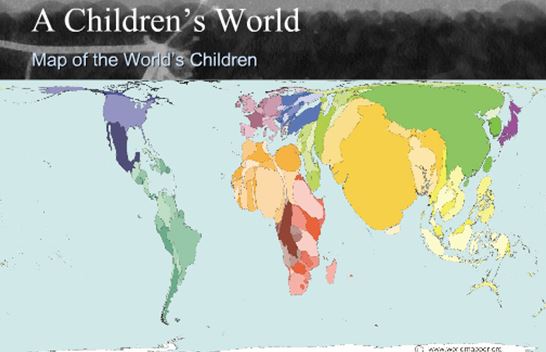

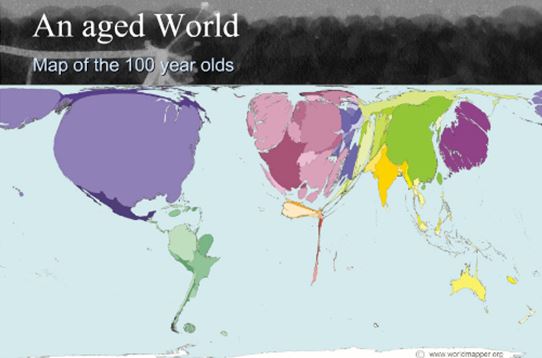

You can never underestimate the importance of demographics in shaping long term investment trends, so I thought I’d pass on these two highly instructive maps.

The first shows a map of the world drawn in terms of the population of children, while the second illustrates the globe in terms of its 100-year-olds.

Notice that China and India dominate the children’s map. Kids turn into consumers in 20 years, stay healthy for a long time, draw on few government services, and power economic growth.

The US, Japan, and Europe shrink to a fraction of their actual size on the children’s map, so economic growth is in a long-term secular downtrend there.

There is more bad news for the developed world on the centenarian’s map, which show these countries ballooning in size to grotesque, unnatural proportions.

This means higher social security and medical costs, plunging productivity, and falling GDP growth.

The bottom line is that you want to own equities and local currencies of emerging market countries and avoid developed countries like the plague.

Use any major meltdowns this year to increase your exposure to emerging markets, as I will.

Would You Rather Own Them?

Or Them?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/Senior-Citizens-playing-cards.jpg305405DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2024-02-28 09:04:022024-02-28 10:37:06America's Demographic Time Bomb

There is no limit to my desire to get an early and accurate read on the US economy, which at the end of the day is what dictates the future of all of our trades and investments.

I flew over one of my favorite leading economic indicators only last weekend at the controls of a vintage Cessna 172.

Honda (HMC) and Nissan (NSANY) import millions of cars each year through their Benicia, California facilities, where they are loaded onto thousands of rail cars for shipment to points inland as far as Chicago.

In 2009, when the US car market shrank to an annualized 8.5 million units, I flew over the site and it was choked with thousands of cars parked bumper to bumper, rusting in the blazing sun, bereft of buyers.

Then, “cash for clunkers” hit (remember that?).

The lots were emptied in a matter of weeks, with mile-long trains lumbering inland, only stopping to add extra engines to get over the High Sierras at Donner Pass.

The stock market took off like a rocket, with the auto companies leading.

I flew over the site last weekend, and guess what?

The lots are empty.

U.S. new vehicle sales, including retail and non-retail transactions, are estimated to reach 1,354,600 units in August, a 15.4% jump from a year earlier, according to the joint report by J.D. Power and GlobalData. Consumers are estimated to spend $47.8 billion on new vehicles, the highest on record for the month of August, and 10.5% higher than last year, the report said.

Japanese cars are suddenly selling so fast that vehicles are being sold even before they land on the dock.

It is all further evidence that my increasingly optimistic view on the US economy is correct, that multiple crises this year are fully discounted, and that the stock market is poised for new highs.

The conventional auto industry should lead to the upside, as it has already done, led by General Motors (GM) and Ford (F). But the move may not happen until the second half of 2024 when the market’s love affair with big tech stocks reaches the point of temporary exhaustion.

As for Tesla (TSLA), better to buy the car than the stock at these depressed prices. Once the EV price wars end, the stock should double again to new all-time highs.

This is a big deal because the auto industry directly and indirectly accounts for about 10% of the total US economy.

It is also the largest manufacturing employer, with the legacy Big Three accounting for 6 million jobs, 4.87% of the 124 million US total.

Not only do you have to include the big four automakers, but you also must include the vast number of parts suppliers, advertisers, and the national dealer networks.

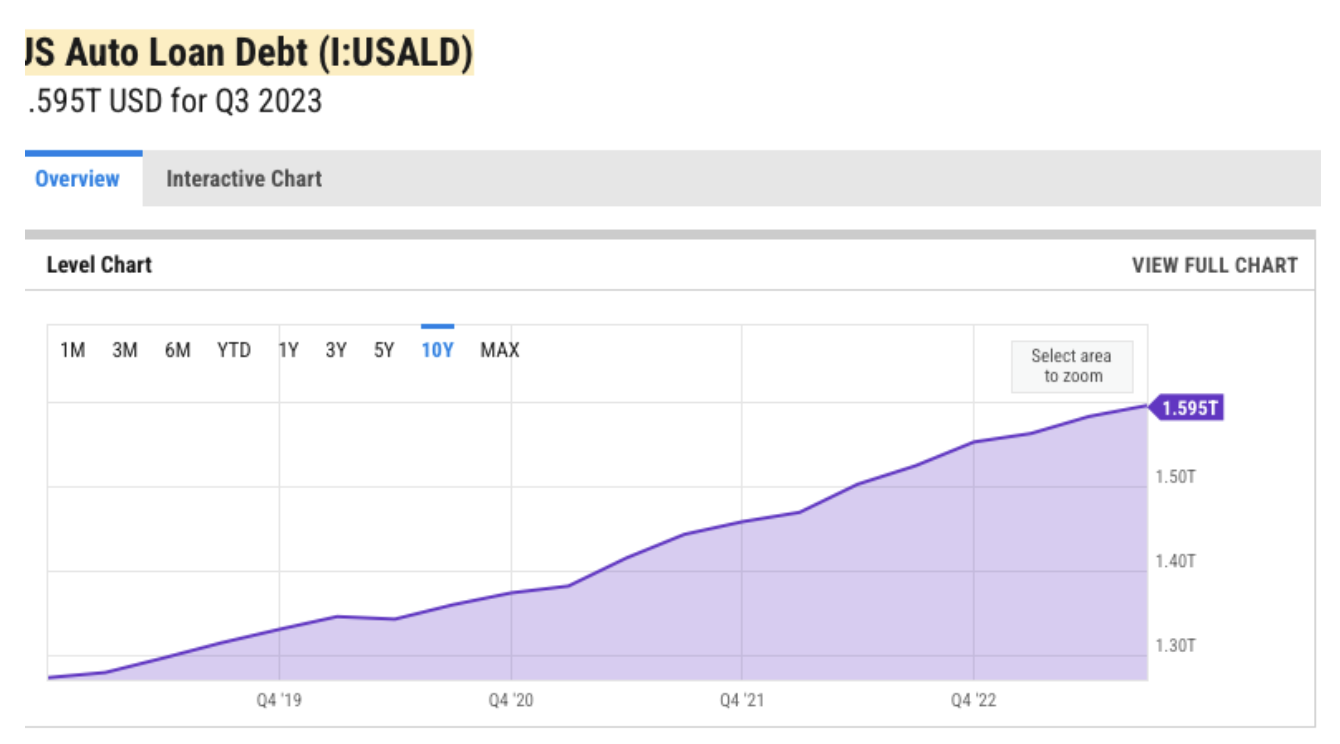

Since so many car purchases are financed with loans, it turns out that the industry is a great play on falling interest rates.

There are $1.6 trillion in subprime auto loans on lenders’ books now.

If you don’t believe me, check out the resale market price of your wheels at Kelly Blue Book (click here for the site)

You will see they have recently risen steadily in value.

It is all further evidence of the hard data/soft data conundrum, which I have written about extensively in the past.

Look no further than Consumer Sentiment, which has held up remarkably well for the past three consecutive months.

Sorry the photo below is a little crooked, but it's tough holding a camera in one hand and a plane's stick with the other, while flying through the never-ending turbulence of the San Francisco Bay’s Carquinez Straight.

Air traffic control at nearby Travis Air Force Base usually has a heart attack when I conduct my research in this way, with a few joyriding C-130s having more than one near miss in recent years.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/10/Honda-Car-Lot.jpg181603Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-24 09:06:002023-11-24 12:08:16My Updated Personal Leading Economic Indicator

If you think that an energy shortage is bad, it will pale in comparison to the next water crisis. So investment in fresh water infrastructure is going to be a great recurring long-term investment theme.

One theory about the endless wars in the Middle East since 1918 is that they have really been over water rights.

Although Earth is often referred to as the water planet, only 2.5% is fresh, and three quarters of that is locked up in ice at the North and South poles. Global warming is freeing up some of this, but not fast enough.

In places like China, with a quarter of the world's population, up to 90% of the fresh water is already polluted, some irretrievably so.

Some 18% of the world population lacks access to potable water, and demand is expected to rise by 40% in the next 20 years.

Aquifers in the US, which took nature millennia to create, are approaching exhaustion.

While membrane osmosis technologies exist to convert seawater into fresh, they use ten times more energy than current treatment processes, a real problem if you don't have any, and will easily double the end cost of water to consumers.

While it may take 16 pounds of grain to produce a pound of beef, it takes a staggering 2,416 gallons of water to do the same. Beef exports are really a way of shipping water abroad in concentrated form.

The UN says that $11 billion a year is needed for water infrastructure investment. It says a lot that when I went to the University of California at Berkeley School of Engineering to research this piece, most of the experts in the field had already been retained by major hedge funds!

At the top of the shopping list to participate here should be the Claymore S&P Global Water Index ETF (CGW). You can get is for a bargain now, as it has just fallen by more than 10% since the stock market melt down began.

You can also visit the PowerShares Water Resource Portfolio (PHO), the First Trust ISE Water Index Fund (FIW), or the individual stocks Veolia Environment (VE), Tetra-Tech (TTEK), and Pentair (PNR).

Who has the world's greatest per capita water resources? Siberia, which could become a major exporter of H2O to China in the decades to come.

The US is Still the Saudi Arabia of Fresh Water

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/Waterfall.jpg283432DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2023-10-05 09:04:312023-10-05 17:48:29Why Water Will Soon Become More Valuable Than Oil

I recently spent a weekend attending a graduation in Washington State, a stone’s throw from where the 2010 Vancouver Winter Olympics were held.

While sitting through the tedious reading of 550 names, I was struck by how many seemed to come from abroad.

As I listened to the wailing ceremonial bagpipes, I did several calculations on the back of the commencement program and was shocked with what I discovered.

Higher education has grown into a gigantic service industry for America, with a massively positive impact on our balance of payments, generating an impact on the world far beyond the dollar amounts involved.

According to the non-profit Institute of International Education, there are 819,644 foreign students in the US today, up an impressive 7.2% from last year.

This combined student body pays an average out-of-state tuition of $40,000 a year each totaling some $38 billion. The positive impact on the US balance of payments and the US dollar exchange rate is huge.

China is far and away the dominant origin of these students, accounting for 262,922, up 26% from the previous year. South Korea and India take the number two and three slots, thanks to the generous scholarships provided by their home governments. Saudi Arabia and Brazil are showing the fastest growth rates.

A fortunate few, backed by endowed chairs and buildings financed by wealthy and eager parents, land places at prestigious Universities like Harvard, Princeton, and Yale.

The top destinations of foreign students are the University of Southern California in Los Angeles, CA, the University of Illinois at Urbana-Champaign, Indiana’s Perdue University, and New York University, with each of these claiming 9,000 foreign students.

However, the overwhelming majority enroll in the provinces in a thousand rural state universities and junior colleges that most of us have never heard of. Many of these schools now have diligent admissions officers scouring the Chinese hinterlands looking for new applicants.

A college degree once was a uniquely American privilege. In 1974 the US led the world, with 24% of the population getting a sheepskin. Today, it has fallen to 16th, with 28% completing a four-year program, lagging countries like South Korea, Canada, and Japan.

The financial windfall has enabled once sleepy little schools to build themselves into world-class institutions of higher learning, with 30,000 or more students. They boast state of the art facilities, much to the joy of local residents and budget constrained state education officials. Furthermore, the overwhelming leadership of education industry is steadily Americanizing the global establishment.

I can’t tell you how many times over the decades I have run into the Persian Gulf sovereign fund manager who went to Florida State, the Asian CEO who attended Cal State Hayward, or the African finance minister who fondly recalled rooting for the Kansas State Wildcats.

Remember the recently ousted president of Egypt, Mohamed Morsi? He was a former classmate of mine at USC. Go Trojans! Do you think he was singing “Fight on For Old SC” in his jail cell?

Those who constantly bemoan the impending fall of the Great American Empire can take heart by merely looking inland at these impressive degree factories. These students are not clamoring to get into universities in Beijing, Moscow, or Tokyo.

Not a few marry and permanently settle in the US, while many others take their American brides home. Saudi Arabia is home to some 50,000 such wives, who had to agree to Sharia law and give up driving to obtain resident permits.

It also explains why the dollar is so strong in the face of absolutely gigantic, structural trade deficits. When a foreign student pays tuition to a US school, it is treated as an export of a service in terms of the US balance of payments, much like a car or an airplane, our country’s largest exports.

Rising exports mean that more dollars are staying home and fewer are going abroad, strengthening the value of the greenback. $24 billion and change offset a lot of imports of cheap electronics, clothing, and toys from China. This is why the US dollar is close to all-time highs in the foreign exchange markets.

The US has plenty of capacity to expand this trade in services. Over 70% of foreign students are concentrated in just 200 of the country’s 4,000 colleges.

The University of California has blazed a path that many other cash-strapped institutions are certain to follow. During the financial crisis, the world’s greatest public university saw two back-to-back 40% budget cuts from Sacramento.

So it made up the shortfall by bumping up foreign admissions from 5% to 10%, largely from Asia. They must pay $43,980 a year in tuition, compared to $15,444 for in-state residents.

What is the upshot of all of these for the locals? It is now a lot harder to get an “A” in Math at UC Berkeley.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/11/Graduation-Cap.jpg361303Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-27 09:04:412023-09-27 13:22:36The Bull Market in American College Degrees

I wanted to get the low down on clean coal (KOL) to see how clean it really is, so I visited some friends at Lawrence Livermore National Laboratory in California.

The modern-day descendent of the Atomic Energy Commission, where I had a student job in the early seventies, the leading researcher on laser-induced nuclear fission, and the administrator of our atomic weapons stockpile, I figured they’d know.

Dirty coal currently supplies us with 35% of our electricity, and total electricity demand is expected to go up 30% by 2030. The industry is spewing out 32 billion tons of carbon dioxide (CO2) a year and the great majority of independent scientists out there believe that the global warming it is causing will lead us to an environmental disaster within decades.

Carbon Capture and Storage technology (CCS) locks up these emissions deep underground forever. The problem is that there is only one of these plants in operation in North Dakota, a legacy of the Carter administration, and new ones would cost $4 billion each.

The low estimate to replace the 250 existing coal plants in the US is $1 trillion, and this will produce electricity that costs 50% more than we now pay. In a gridlocked constrained congress, this is a big ticket that is highly unlikely to get picked up.

While we can build a wall to keep out illegal immigrants from Latin America, it won’t keep out CO2. This is a big problem as China is currently completing one new coal-fired plant a week.

In fact, the Middle Kingdom is rushing to perfect cheaper CCS technologies, not only for their own use but also to sell to us. The bottom line is coal can be cleaned but at a frightful price.

Coal once had a huge price advantage over other energy sources that disappeared when the price of natural gas (UNG) collapsed for $17 BTU to $2/MM BTU. Yesterday, gas closed at a feeble $2.70.

Cost savings aside, virtually every utility in the country would love to get out of the coal business because of the litigation it invites. Read the prospectus for new securities issued by any of them, and you will find a litany of lawsuits over diseases caused by Sulfur Dioxide (SO2), Nitrous Oxides (NO2), and a host of other asthma and cancer-causing pollutants.

Burning natural gas only emits carbon dioxide (CO2) (only half the amount that crude oil derived bunker fuel does) and water (H2O). Sorry, but my inner chemist is speaking.

California closed its last coal-fueled power plant a 20 years ago, switching to natural gas, accidentally creating a windfall for consumers. Much of the money saved was used to modernize the grid buy installing statewide smart meters which allow customers to both buy and sell electricity back to utilities generated from home solar installations and charged up 1,000-pound 100 kWh lithium-ion Tesla batteries.

These moved are expected to save our local Pacific Gas and Electric (PGE) the capital cost of building two new major generating plants. This is not your father’s utility.

Although it is unlikely that another coal fired power plant will ever be built in the US again, don’t expect coal giants like Peabody Energy (BTU) to disappear anytime soon. There is still a massive export business to China, as the Burlington Northern freight trains that rumble near my home testify (love that midnight whistle).

But don’t ever confuse a stock price that has gone down a lot with “cheap.” The shares of these companies could remain in the dumps for a long time, and possibly forever, creating a classic value trap. That is, until the Chinese buy them out for pennies on the dollar.

These are jobs I don’t mind exporting to China. They can have them.

When I checked the price of the old coal ETF (KOL) I discovered that it had ceased trading in 2020 after its asset under management fell from $908 million to just $35 million. At that level Van Eck was losing money running the fund. Most pension funds had banned investing in coal companies.

That alone tells you a lot right there.

Coal's Popularity is Fading Fast

https://www.madhedgefundtrader.com/wp-content/uploads/2014/06/Smoke-Stacks.jpg300455Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-15 09:02:492023-09-15 17:13:33The Price Tag for Clean Coal

I just received a call from the Marine Corps to go on emergency standby. This is not something the Corps does lightly.

The word is that there may be a coup d'etat underway in Russia and the entire US military has gone to a heightened alert status.

The Wagner group is Marching on Moscow with the intent of overthrowing the government, or at least the military. Putin took off in a plane which then disappeared radar, meaning he has either been shot down, or is flying low level to keep his destination secret.

This thing could go nuclear very easily, but only in Russia. It also could mean the end of the Ukraine War. There is nothing to do here as intelligence pours in over the weekend. We have ample satellites overhead and human intel on the ground.

Expect market volatility today. The markets are ripe for a black swan-inducted selloff, which a Mad Hedge Market Timing Index at 82 was screaming at us.

I will be monitoring the situation closely.

My view that the markets were topping was vindicated last week. The “Magnificent Seven” which gained a record 25% in market capitalization in only eight weeks led the downturn, as they always do. But the AI surge that prompted the fastest equity creation in history is only just getting started.

This is against a backdrop of savage cost-cutting by Big Tech, which has had the effect of boosting earnings by an impressive 7% in only three months. My cleaning lady, gardener, dry cleaner, and shoe shine boy have started giving me stock tips yet, as they did in 2000, 2008, and 2020….but they are thinking about it.

While attention is focused elsewhere, one should not underestimate the importance of India Prime Minister Modi’s meeting with Joe Biden in Washington.

It signifies a major geopolitical shift out of the Russian orbit into the US one. Decades ago, India obtained all its weapon systems and nuclear power plants from Russia and was a major trading partner.

Now partnering up with Apple (AAPL), Google (GOOGL), Microsoft (MSFT), and General Electric (GE) is a much more attractive option. It is gaining a $2.7 billion factory from Micron Technology (MU) and presents a major market for its products. Amazon (AMZN) is investing $13 billion in cloud infrastructure there. The subcontinent graduates some 2.5 million STEM graduates a year and they need to be put to work in the global economy. It shows how limited Russia’s future really is. It’s a major win for the US.

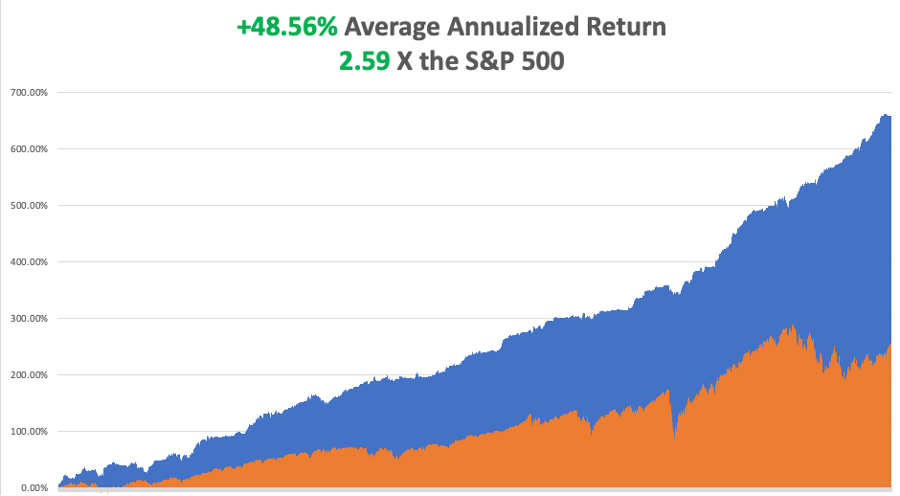

So far in June, we are up +0.47%. My 2023 year-to-date performance is still at an eye-popping +62.52%. The S&P 500 (SPY) is up only a respectable +14.00% so far in 2023. My trailing one-year return reached +96.63% versus +21.52% for the S&P 500.

That brings my 15-year total return to +659.71%. My average annualized return has blasted up to +48.56%, another new high, some 2.59 times the S&P 500 over the same period.

Some 42 of my 46 trades this year have been profitable. Only 23 of my last 24 consecutive trade alerts have been profitable.

The Mad Hedge December 6-8 Summit Replays are Up. Listen to all 28 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. It is a true smorgasbord of investment strategies. Find the best one to suit your own goals. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here and then choosing the speaker of your choice. We look forward to working with you.The next summit is scheduled for September 12-14.

$2 Billion Fled Stock Market Last Week, according to a Bank of America survey, in what it calls a “Baby Bubble.” The markets are showing all the signs of an interim top, with either a 10% correction or a three-month flat line ahead of us. Time to strap on those Buy Writes for long-term shareholders.

Short Bets on US stocks Hit $1 trillion, the highest since April 2022. Shorts have so far lost $101 billion in 2023, with much of this hedged. The market is way overdue for a correction so these guys may finally be right. Even a broken clock is right twice a day.

Germany Signs Massive US Natural Gas Contract, in a major move to end reliance on Russian natural gas. Venture Global LNG will supply EnBW with 1.5 million tons a year of LNG starting in 2026. The 20-year sales and purchase agreement is Germany’s first binding deal with a US developer since the government announced ambitious plans to begin importing the super-chilled fuel. The move does a lot to eliminate the glut of gas in the US currently plaguing producers. Buy (UNG) LEAPS on dips. When China comes back on line, watch out!

Volatility Index ($VIX) Hits the $12 Handle, in a new multiyear low. At the high for the year in the S&P 500, complacency is running rampant. Time to add some downside hedges.

Copper Should be a “Critical Metal”, says billionaire Robert Friedland. A looming structural shortage is the reason, with the world going to an all-electric auto fleet and doubling of the electrical grid to accommodate it. Buy more (FCX) LEAPS on dips.

Leading Economic Indicators Down 0.7% for the 15th consecutive negative month. We are approaching the bottom of the trough in this cycle. I’ll focus on the half of the economy that is growing.

Distressed Commercial Property Debt is Exploding, up 10% to Q1 to $64 billion. Another $155 billion is waiting in the wings. This will go away when interest rates start to drop in six months.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 26 at 8:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, June 27 at 6:00 PM, S&P Case-Shiller National Home Price Index is published.

On Wednesday, June 28 at 7:30 AM, the Fed Governor Jay Powell speaks.

On Thursday, June 29 at 8:30 AM, the Weekly Jobless Claims are announced. The Final Report for Q1 US GDP is printed.

On Friday, June 30 at 8:30 AM, Personal Income and Spending is announced.

As for me, when I first met Andrew Knight, the editor of The Economist magazine in London 45 years ago, he almost fell off his feet. Andrew was well known in the financial community because his father was a famous WWII Battle of Britain Spitfire pilot from New Zealand.

At 34, he had just been appointed the second youngest editor in the magazine’s 150-year history. I had been reporting from Tokyo for years, filing two stories a week about Japanese banking, finance, and politics.

The Economist shared an office in Tokyo with the Financial Times, and to pay the rent I had to file an additional two stories a week for them as well. That’s where I saw my first fax machine, which then was as large as a washing machine even though the actual electronics would fit in a notebook. It cost $5,000.

The Economist was the greatest calling card to the establishment one could ever have. Any president, prime minister, CEO, central banker, or war criminal was suddenly available for a one-hour chart about the important affairs of the world.

Some of my biggest catches? Presidents Gerald Ford, Jimmy Carter, Ronald Reagan, George Bush, and Bill Clinton, China’s Zhou Enlai and Deng Xiaoping, Japan’s Emperor Hirohito, terrorist Yasir Arafat, and Teddy Roosevelt’s oldest daughter, Alice Roosevelt Longworth, the first woman to smoke cigarettes in the White House in 1905.

Andrew thought that the quality of my posts was so good that I had to be a retired banker at least 55 years old. We didn’t meet in person until I was invited to work the summer out of the magazine’s St. James Street office tower, just down the street from the palace of then Prince Charles.

When he was introduced to a gangly 25-year-old instead, he thought it was a practical joke, which The Economist was famous for. As for me, I was impressed with Andrew’s ironed and creased blue jeans, an unheard-of concept in the Wild West where I came from.

The first unusual thing I noticed working in the office was that we were each handed a bottle of whisky, gin, and wine every Friday. That was to keep us in the office working and out of the pub next door, the former embassy of the Republic of Texas from pre-1845. There is still a big white star on the front door.

Andrew told me I had just saved the magazine.

After the first oil shock in 1973, a global recession ensued, and all magazine advertising was cancelled. But because of the shock, it was assumed that heavily oil-dependent Japan would go bankrupt. As a result, the country’s banks were forced to pay a ruinous 2% premium on all international borrowing. These were known as “Japan rates.”

To restore Japan’s reputation and credit rating, the government and the banks launched an advertising campaign unprecedented in modern times. At one point, Japan accounted for 80% of all business advertising worldwide. To attract these ads the global media was screaming for more Japanese banking stories, and I was the only person in the world writing them.

Not only did I bail out The Economist, I ended up writing for over 50 business and finance publications around the world in every English-speaking country. I was knocking out 60 stories a month, or about two a day. By 26, I became the highest paid journalist in the Foreign Correspondents’ Club of Japan and a familiar figure in every bank head office in Tokyo.

The Economist was notorious for running practical jokes as real news every April Fool’s Day. In the late 1970s, an April 1 issue once did a full-page survey on a country off the west coast of India called San Serif.

It warned that if the West coast kept eroding, and the East coast continued silting up, the country would eventually run into India, creating serious geopolitical problems.

It wasn’t until someone figured out that the country, the prime minister, and every town on the map were named after a type font that the hoax was uncovered.

This was way back, in the pre-Microsoft Word era, when no one outside the London Typesetter’s Union knew what Times Roman, Calibri, or Mangal meant.

Andrew is now 84 and I haven’t seen him in yonks. My business editor, the brilliant Peter Martin, died of cancer in 2002 at a very young 54, and the magazine still awards an annual journalism scholarship in his name.

My boss at The Economist Intelligence Unit, which was modeled on Britain’s MI5 spy service, was Marjorie Deane, who was one of the first women to work in business journalism. She passed away in 2008 at 94. Today, her foundation awards an annual internship at the magazine.

When I stopped by the London office a few years ago I asked if they still handed out the free alcohol on Fridays. A young writer ruefully told me, “No, they don’t do that anymore.”

Sometimes, change is for the worse, not the better.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-economist-e1664802946349.png285500Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-26 09:02:572023-06-26 12:08:01The Market Outlook for the Week Ahead, or Is there a Coup Underway in Russia?

Below please find subscribers’ Q&A for the June 21 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, NV.

Q: When do we buy Nvidia (NVDA) and Tesla (TSLA)?

A: On at least a 20% dip. We have had ballistic moves—some of the sharpest up moves in the history of the stock market for large stocks—and certainly the greatest creation of market caps since the market was invented under the Buttonwood Tree in 1792 at 68 Wall Street. Tesla’s almost at a triple now. Tripling one of the world's largest companies in 6 months? You have to live as long as me to see that.

Q: Is it a good time to invest in Bitcoin?

A: No, absolutely not. You only want to invest in Bitcoin when we have an excess of cash and a shortage of assets. Right now, we have the opposite, a shortage of cash and an excess of assets, and that will probably continue for several years.

Q: Should I short Apple (APPL)?

A: Only if you’re a day trader. It’s hugely overbought for the short term, but still in a multiyear long-term uptrend. I think we could see Apple at $300 in the next one or two years.

Q: Is it better to focus on single stocks or ETFs?

A: Single stocks always, because a single stock will outperform a basket that's in an ETF by 2 to 1 or even 3 to 1. That's always the case; whenever you add stocks to a basket, it diversifies risk and dilutes the performance. Better to just own Tesla, and if you want to diversify, diversify to Nvidia, but then I live next door to these two companies. That's what I tell my friends. You only diversify if you don’t know what is going to happen, which is most investors and financial advisors.

Q: Is the bottom of the housing market in, and are we due for a spike in home prices when interest rates can only go lower?

A: Yes, absolutely. In fact, we will enter a new 10-year bull leg for housing because we have a structural shortage of 10 million homes and 82 million millennials desperately trying to buy them at any price. I just got a call from my broker and she is panicking because she is running out of inventory. Even the lemons are starting to move.

Q: When do you think energy will rise?

A: Falling interest rates could be a good key because it sets the whole global economy on fire and increases energy demand.

Q: Outlook for the S&P 500 (SPY) second half of the year?

A: We hit 4,800 at least, maybe even higher. That's about a little more than 10% from here, so it’s not that much of a stretch, not like it was at the beginning of the year when it needed to rise 25% to reach my yearend target.

Q: Best time to invest from here on?

A: Either a 10% pullback in the market, or a sideways move of 3 months—that's called a time correction. It usually counts as a price correction because of course, over 3 months, earnings go up a lot, especially in tech.

Q: I’m seeing grains (WEAT) in rally mode.

A: Yes, that's true. They are commodities, and just like copper’s been rallying, and it’s yet another signal that we may get a much broader global commodity rally in everything: iron ore, coal, energy, gold, silver, you name it.

Q: Will inflation drop to 2%, causing stocks to go on another epic run?

A: The answer is yes, I do see inflation dropping to 2% —maybe not this year, but next year; not because of any action the Fed is doing, but because technology is hyper-accelerating, and technology is highly deflationary. The tech product you bought two years ago is now half the price, and they offer you twice as much functionality with an auto-renew for life. So, that is happening across the entire technology front and feeds into the inflation numbers big time, including labor. There's going to be a lot of labor replacement by machines and AI in the coming years.

Q: Is Airbnb (ABNB) a good stock to buy?

A: Well, if we’re going into the most perfect travel storm of all time, which is this summer, and which is why I’m going to remote places only like Cortina, Italy. Airbnb is the perfect stock to own. It’s a well-run company even in normal times.

Q: Should I buy gold here on the pullback?

A: Yes, you should. Gold is also highly sensitive to any decline in interest rates, and by the way: buy silver, it always moves 2.5x as much as the barbarous relic.

Q: How can inflation not go up if commodities and wage demands are going up due to state and federal unions? What about farm equipment and truck supplies? Costs keep rising, should we buy John Deere (DE)?

A: There are three questions here. Inflation will not go up because, though commodities will rise, they are only 0.6% of the $100 trillion global economy, or $660 billion in 2022. That will be more than offset by technology cutting prices, which is 30% of the stock market. You have to realize how important each individual element is in the global picture. And regarding wage demands going up caused by state and federal unions, less than 11.3% of the workforce is now unionized and that figure has been declining for 40 years. Most growth in the economy has been in non-unionized technology firms which largely depend on temporary workers, by design. What IS unionized is mostly teachers, the lowest paid workers in the economy, so incremental pay rises will be small. Unions were absolutely slaughtered when 25 million jobs were offshored to China during the Bush administration. Buy farm equipment and trucks? Absolutely, buy John Deere (DE) and buy Caterpillar (CAT) on the next dip. I was actually looking at Caterpillar for the next LEAPS the other day, but it’s already had a big run; I'm going to wait for a pullback before I get CAT and John Deere. So, again, people see headlines, see union wage headlines—I say focus on the 89% and not on the 11% if you want to make good decisions.

Q: Is Boeing (BA) a buy on the dip?

A: Yes, they got 1,000 new aircraft orders and the stock hasn't moved. So yes, if you get any kind of selloff down to $200, I'd be hoovering this thing up.

Q: Can you please explain how the profit predictor works?

A: It’s a long story; just go to our website, log in and do a search for “profit predictor,” and you’ll get a full explanation of how it works. It’s actually where Mad Hedge has been using artificial intelligence for 11 years, which is why our performance has doubled. Just for fun, I'll run the piece next week.

Q: Gold (GLD) is having a hard time going up because Russia is being squeezed by other governments. Since they need cash, they may be either selling their gold or stop buying new gold.

A: That is a good point, but at the end of the day, interest rates are the number one driver of all precious metals—period, end of story. We’re long gold too, I’ve got lots of gold coins stashed around the world in various safe deposit boxes, and I'm keeping them. I’ve got even more silver coins, which take up a lot of space.

Q: Do you like India (INDA) long term?

A: Yes, it’s the next China. But as Apple is finding out it is very difficult to get anything done there. A radical reforming Prime Minster Modi may be changing things there with his recent Biden visit and (GE) contract to build jet engines.

Q: What do you think of General Dynamics Corp (GD)?

A: I like General Dynamics because I think defense spending is in a permanent long term upcycle as a result of the Ukraine war. And it won’t end with the Ukraine war—the threat will always be out there, and the buying is done by not only us but all the other countries that think Russia is a threat.

Q: Do you like MP Materials Corp (MP)?

A: Yes, I do. The whole commodities space is ready to take off and go on fire.

Q: What about Square (SQ)?

A: The only reason I’m not recommending Square right now is huge competition in the entire sector, where all the stocks including PayPal (PYPL) are getting crushed. I will pass on Square for now, especially when I can buy US Steel (X) at close to its low for the year.

Q: If you had to pick one: Nvidia (NVDA), Tesla (TSLA), Microsoft (MSFT), Meta (META), and Google (GOOGL), which is the best to buy for next year?

A: All of them. Diversify. If I have to pick the top performer, it’s going to be either Tesla or Nvidia, probably Nvidia. But you need at least a 10% correction before you do anything. Actually, the split-adjusted price for our first (NVDA) recommendation eight years ago was $2 a share.

Q: Do you like Crown Castle International (CCI)?

A: Yes, I like it very much—it has very high dividend yield at 5.5%. The reason it hasn’t moved yet is that as long as interest rates are high, any REIT structure will suffer, and (CCI) has a REIT structure. Sure, it’s in a great sector—5G cell towers—but it is still a REIT nonetheless, and those will start to recover when interest rates go down; that’s why we did a 2.5-year LEAPS on CCI. For sure interest rates are going to go down in the next 2.5 years, and you will double your money on (CCI). That’s why we put it out.

Q: Which mid cap will do best over the long term: Airbnb (ABNB), Snowflake (SNOW), or Palantir (PLTR)?

A: That’s easy: Snowflake. They have such an overwhelming technology on the database and security front; I would be buying Snowflake all day long. Even Warren Buffet owns Snowflake, so that’s good enough for me.

Q: Could you comment on the pace of EV adoption/potential for (TSLA) robot fleet acceleration and implications for oil investments in holding pattern till the eventual collapse to near 0?

A: Yes, oil may collapse to near zero, but it may take twenty years to do it—that’s how long it takes to transition an energy source. That’s how long it took the move from horses and hay to gasoline-powered cars at the beginning of the 20th century. A national robot fleet of taxis with no drivers at all is a couple of years off. There are about 1,000 of them working in San Francisco right now, but they still have more work to do on the software. When it gets foggy, they often congregate at intersections causing traffic jams. Suffice it to say that eventually Tesla shares go to $1,000 and after that, $10,000—that’s my bet. By the way, my Tesla January 2025 $595-$600 LEAPS are starting to look pretty good.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2018 in Australia

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-03.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-23 09:02:392023-06-23 15:53:43June 21 Biweekly Strategy Webinar Q&A

As I write this to you, I am flying at 30,000 feet over the red clay of Georgia. The azure blue of the Gulf of Mexico is on the left and the Golden State of California lies straight ahead.

I am returning from a five-day whirlwind tour of Florida, which saw me speak at three Strategy Luncheons and countless private meetings.

It was a blast!

Not only did I learn the local lay of the land, I often pick up some great trading ideas.

I first hitchhiked across the Sunshine State in 1967. Except for a few small towns on the coasts, there was nobody there. The entire inland of the state was covered with small cattle ranches and the odd tourist trap (mermaids, alligator wrestling, snake shows etc).

People thought the extensive freeway system was only built because the state was just 90 miles away from Cuba, then a Cold War flash point (it is officially called the “Dwight D. Eisenhower National System of Interstate and Defense”). Suddenly, somebody secretly started buying up land around Orlando. The locals thought General Motors (GM) was going to build a car plant there.

Then Walt Disney Corp (DIS) swept in and announced they were building a second Disneyland to cater to the east coast, creating an astonishing 70,000 jobs and the freeways started to fill up (click here for the video).

Today, driving around the state is a dystopian nightmare. The US population has doubled since the first Interstates were built in the 1950s, and the US GDP has increased by ten times, a byproduct of the Interstates. That means ten times more heavy truck traffic which has been mercilessly beating the life out of the roads. In Florida, the population has risen by more than fourfold as well, from 5 million to 22.2 million so you get the picture.

You lurch from one traffic jam to the next, even in the middle of the night. Whatever time Google Maps says it will take to get somewhere, triple it. The only consolation is that the traffic is worse in California.

I loved Key West where a very happy Concierge member made available an 1859 mansion close to the waterfront, restored and modernized down to the studs. By this time of the year, anyone with money has decamped for New England leaving only the retirees and beach bums.

I made the pilgrimage to Earnest Hemmingway’s home where he produced 70% of his published writings in only seven years. Another two boxes of manuscripts were discovered in the basement of his favorite bar last year.

It’s ironic that this state is now known for banning books that include sex and violence. Steinbeck’s work has already hit the dustbin, so old Earnest can’t be far behind.

What’s next? The Bible? It has lots of sex and violence.

As for me, Hemingway’s granddaughter, Mariel, stands out as the only Playboy cover girl I ever dated (April, 1982, I think). She is now happily married with three grown kids.

And yes, I did prove that it is possible to eat Key Lime Pie four days in a row.

As for the stock market last week, there really isn’t much to say. The concentration of wealth at the top continues unabated, as it is in the rest of the country. Stocks are still discounting a soft landing, while commodities, energy, and bonds expect a recession.

Go figure.

The top five stocks continues to suck all the money out of the rest of the market, (AAPL), (GOOGL), (AMZN), (MSFT), and (NVIDIA), the early beneficiaries of AI, accounting for 80% of this year’s market gains. Of the other 495 stocks, 250 are below their 200-day moving averages, meaning they are still in bear markets.

This is what has crushed volatility, taking the ($VIX) from $34 down to $15. The last time volatility was this low was just before the Long Term Capital Management fiasco where it languished around $9 (read Liar’s Poker by my friend Michael Lewis). When LTCB went bust, volatility rocketed to $40 overnight and stayed there for two years.

Options traders made fortunes.

Mad Hedge has nailed every trend this year. We bought tech and Tesla (TSLA) in January when we should have. We shorted ($VIX) every time it approached $30. Then we bought the banking bottom in March (JPM), (BAC), (C) and carried those positions into April.

We’ve been shorting Tesla strangles every month. And now we are 80% in cash waiting for the world to end one more time in Washington DC so we can load the boat with LEAPS and replay the movie one more time.

By the way, Mad Hedge has issued 25 LEAPS over the past year and 24 made money with an average profit of about 300%. Our sole loser has been with Rivian (RIVN), but even it still has 18 months to run. Never own an EV stock during a price war.

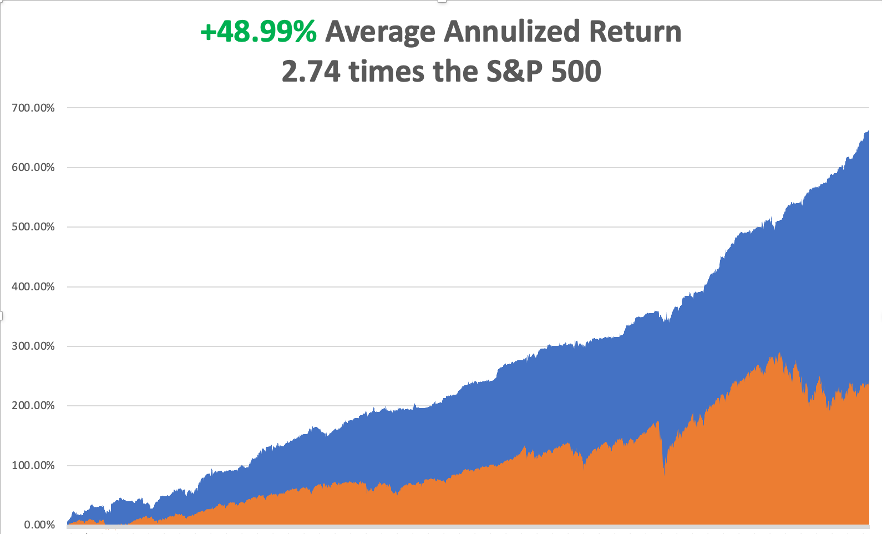

So far in May I have managed a modest 2.43% profit. My 2023 year-to-date performance is now at an eye-popping +64.18%. The S&P 500 (SPY) is up only a miniscule +9.00% so far in 2023. My trailing one-year return reached a 15-year high at +113.84% versus +10.87% for the S&P 500.

That brings my 15-year total return to +661.37%. My average annualized return has blasted up to +48.99%, another new high, some 2.74 times the S&P 500 over the same period.

Some 41 of my 44 trades this year have been profitable. My last 22 consecutive trade alerts have been profitable.

I closed out only one trade last week, a long in the (TLT) just short of max profit a day before expiration. That just leaves me with a long in Tesla and a short in Tesla, the “short strangle”. I now have a very rare 80% cash position due to the lack of high return, low risk trades.

There’s a 1,000 Point Drop in the Market Begging to Happen. That’s what happens when the market rallies on a Biden McCarthy debt ceiling deal, which McCarthy’s own party then votes down. After all, it took McCarthy 15 votes to get his job. Just watch volatility, it’s a coming.

Weekly Jobless Claims Fall to 242,000, down from 264,000. It’s a surprise slowdown. The rumor is that last week’s highpoint was the result of a surge in fraudulent online claims in Massachusetts.

NVIDIA Could Rise Fivefold in Ten years, say fund managers. I think that’s a low number. The Silicon Valley company makes the top performing GPU’s in the industry selling up to $60,000 each. (NVDA) is seeing a perfect storm of demand from the convergence of AI and Internet growth. The shares have already tripled off of the October low.

Tesla is Considering an India Factory, as part of its eventual build out to 10 plants worldwide. The country’s 100% import duty on cars has been a major roadblock. India is now pushing a “Made in India” initiative. Good luck getting anything done in India.

Homebuilder Sentiment Up for 10th Straight Month, as it will be for the next decade. There is no easy escape from a demographic wave. New homebuilders have figured out the new model.

India’s Tata to Build iPhones for Apple, in an accelerating diversification away from China. Apple has had too many of its eggs in one basket, especially given the recent political tensions between the US and the Middle Kingdom.

US Dollar Soars to Three Month High, as investors flee to safe haven short term investments. Rapidly worsening economic data is sparking recession fears. Ten consecutive months of falling inflation is another indicator of a slowdown.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 22 there is nothing of note to report.

On Tuesday, May 23 at 4:00 PM EST, the inaugural launch of Mad Hedge Jacquie’s Post takes place. Please click here to attend this strategy webinar. The Federal Reserve Open Market Committee minutes are out at 2:00 PM.

On Wednesday, May 24 at 2:00 PM, the Federal Reserve Open Market Committee minutes are out.

On Thursday, May 25 at 8:30 AM, the Weekly Jobless Claims are announced. The US GDP Q2 second estimate is also published.

On Friday, May 26 at 2:00 PM, the University of Personal Income & Spending and Durable Goods are released.

As for me, I am reminded of my own summer of 1967, back when I was 15, which may be the subject of a future book and movie.

My family summer vacation that year was on the slopes of Mount Rainier in Washington State. Since it was raining every day, the other kids wanted to go home early.

So my parents left me and my younger brother in the firm hands of Mount Everest veteran Jim Whitaker to summit the 14,411 peak (click here for this story ). The deal was for us to hitchhike back to Los Angeles as soon as we got off the mountain.

In those days, it wasn’t such an unreasonable plan. The Vietnam War was on, and a lot of soldiers were thumbing their way to report to duty. My parents figured that since I was an Eagle Scout, I could take care of myself anywhere.

When we got off the mountain, I looked at the map and saw there was this fascinating-sounding country called “Canada” just to the north. So, it was off to Vancouver. Once there I learned there was a world’s fair going on in Montreal some 2,843 away, so we hit the TransCanada Highway going east.

We ran out of money in Alberta, so we took jobs as ranch hands. There we learned the joys of running down lost cattle on horseback, working all day at a buzz saw, artificially inseminating cows, and eating steak three times a day.

I made friends with the cowboys by reading them their mail, which they were unable to do since they were all illiterate. There were lots of bills due, child support owed, and alimony demands.

In Saskatchewan, the roads ran out of cars, so we hopped a freight train in Manitoba, narrowly missing getting mugged in the rail yard. We camped out in a box car occupied by other rough sorts for three days. There’s nothing like opening the doors and watching the scenery go by with no billboards and the wind blowing through your hair!

When the engineer spotted us on a curve, he stopped the train and invited us to up the engine. There, we slept on the floor, and he even let us take turns driving! That’s how we made it to Ontario, the most mosquito-infested place on the face of the earth.

Our last ride into Montreal offered to let us stay in his boat house as long as we wanted so there we stayed. Thank you, WWII RAF Bomber Command pilot Group Captain John Chenier!

Broke again, we landed jobs at a hamburger stand at Expo 67 in front of the imposing Russian pavilion with the ski jump roof. The pay was $1 an hour and all we could eat.

At the end of the month, Madame Desjardin couldn’t balance her inventory, so she asked how many burgers I was eating a day. I answer 20, and my brother answered 21. “Well, there’s my inventory problem” she replied.

And then there was Suzanne Baribeau, the love of my life. I wonder whatever happened to her?

I had to allow two weeks to hitchhike home in time for school. When we crossed the border at Niagara Falls, we were arrested as draft dodgers as we were too young to have driver’s licenses. It took a long conversation between US Immigration and my dad to convince them we weren’t. It wasn’t the last time my dad had to talk me out of jail.

We developed a system where my parents could keep track of us across the continent. Long-distance calls were then enormously expensive. So, I called home collect and when my dad answered, he asked what city the call was coming from.

When the operator gave him the answer, he said he would NOT accept the call. I remember lots of surprised operators. But the calls were free, and Dad always knew where we were. At least he had a starting point to look for the bodies.

We had to divert around Detroit to avoid the race riots there. We got robbed in North Dakota, where we were in the only car for 50 miles. We made it as far as Seattle with only three days left until high school started.

Finally, my parents had a nervous breakdown. They bought us our first air tickets ever to get back to LA, then quite an investment.

I haven’t stopped traveling since, my tally now tops all 50 states and 135 countries.

And I learned an amazing thing about the United States. Almost everyone in the country is honest, kind, and generous. Virtually every night, our last ride of the day took us home and provided us with an extra bedroom, garage, barn or tool shed to sleep in. The next morning, they fed us a big breakfast and dropped us off at a good spot to catch the next ride.

It was the adventure of a lifetime and I profited enormously from it. As a result, I am a better man.

As for my brother Chris, he died of covid in early 2020 at the age of 65, right at the onset of the pandemic. Unfortunately, he lived very close to the initial Washington State hot spot.

People often ask me what makes me so different from others. I answer, “My parents taught me I could do anything with my life, and I proved them right.”

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Summit of Mt. Rainier 1967

McKinnon Ranch Bassano Alberta 1967

American Pavilion Expo 67

Hamburger Stand at Expo 67

Picking Cherries in Michigan 1967

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/hamburger-stand.jpg970983Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-22 09:02:142023-05-22 15:47:30The Market Outlook for the Week Ahead, or Concentration of Wealth at the Top

For those readers looking to improve their trading results and create the unfair advantage they deserve, I have posted a training video on How to Execute a Vertical Bull Call Spread.

This is a matched pair of positions in the options market that will be profitable when the underlying security goes up, sideways, or down a small amount in price over a defined limited period of time.

It is the perfect position to have onboard during markets that have declining or low volatility, much like we experienced in 2014, and will almost certainly see again.

I have strapped on quite a few of these across many asset classes this year, and they are a major reason why I am showing positive performance numbers for 2016.

To understand this trade, I will use the example of an Apple trade, which I executed on July 10, 2014. I then felt very strongly that Apple shares would rally into the release of its new iPhone 6 on September 9, 2014.

The same play kicked in again for the iPhone 12 release last October.

So followers of my Trade Alert service received text messages and emails to add the following position:

Buy the Apple (AAPL) August 2014 $85-$90 in-the-money bull call spread at $4.00 or best

To accomplish this, they had to execute the following trades:

Buy 25 August 2014 (AAPL) $85 calls at...............$9.60

Sell short 25 August 2014 (AAPL) $90 calls at......$5.60

Net Cost:...............................................................$4.00

This gets traders into the position at $4.00, which cost them $10,000 ($4.00 per option X 100 shares per option contract X 25 contracts).

The vertical part of the description of this trade refers to the fact that both options have the same underlying security (AAPL), the same expiration date (August 15, 2014) and only different strike prices ($85 and $90).

The breakeven point can be calculated as follows:

$85.00 - Lower strike price

+$4.00 - Price paid for the vertical call spread

$89.00 - Break even Apple share price

Another way of explaining this is that the call spread you bought for $4.00 is worth $5.00 at expiration on August 15, giving you a total return of 25% in 26 trading days. Not bad!

The great thing about these positions is that your risk is defined. You can't lose any more than the amount of capital you put up, in this case, $10,000.

If Apple goes bankrupt, we get a flash crash, or suffer another 9/11 type event, you will never get a margin call from your broker in the middle of the night asking for more money. This is why hedge funds like spreads so much.

As long as Apple traded at or above $89 on the August 14 expiration date, you would have made a profit on this trade.

As it turns out, my read on Apple shares proved dead-on, and the shares closed at $97.98 on expiration day or a healthy $8.98 above my breakeven point.

The total profit on the trade came to:

($1.00 profit X 100 shares X 25 contracts) = $2,500

This means that the position earned a 25% profit on your $10,000 investment in a little more than a month. Now you know why I like Vertical Bull Call Spreads so much. So do my followers.

Occasionally, these things don't work and wheels fall off. As hard as it may be to believe, I am not infallible.

So, if I'm wrong and I tell you to buy a vertical bull call spread, and the shares fall not a little, but a lot, you will lose money. On those rare occasions when that happens, I'll shoot out a Trade Alert to you with stop-loss instructions before the damage gets out of control.

That stop loss is usually at the lower strike price when there is still a lot of time to run to expiration, as the position still has a lot of time value remaining, and the upper strike price when there are only a few days left until expiration.

The most I have ever lost on paper with one of these vertical bull call spreads was 50% of my capital, or $5,000 on a $10,000 investment. That’s because the trade was with both long and short options which maintain time value, no matter what the market does. I also never put more than 10% of my portfolio into a single position, so the paper loss on the entire capital was only 5%.

But that was on one of the worst days in market history when the Dow Average opened down 1,300 points. As it turned out, I kept my position and ended up making the maximum profit by expiration day.

To watch the video edition of How to Execute a Vertical Bull Call Spread, complete with more detailed instructions on how to execute the position with your own online platform, please click here.

Vertical Bull Call Spreads Are the Way to Go in a Crazily Oversold Market

https://www.madhedgefundtrader.com/wp-content/uploads/2020/04/bull-figure-e1591705319591.png247450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-05 11:02:022023-04-05 14:53:39How to Execute a Vertical Bull Call Spread

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.