Mad Hedge Technology Letter

January 26, 2024

Fiat Lux

Featured Trade:

(WESTERN DIGITAL HAS POTENTIAL)

(WDC), (NVDA), (AMD)

Mad Hedge Technology Letter

January 26, 2024

Fiat Lux

Featured Trade:

(WESTERN DIGITAL HAS POTENTIAL)

(WDC), (NVDA), (AMD)

Chip stocks have been the talk of the town in the tech world.

It’s hard not to notice as stock valuations skyrocket.

These aren’t normal times anymore.

A secular trend that could be the biggest we have seen for a generation is taking hold.

That trend today is AI, and this 800-pound gorilla in the room is causing institutional money to pour into the chips that will help AI and the top firm is clearly Nvidia (NVDA).

After NVDA, there is a solid group of others like AMD, but even after that, there is still more ammo left in the shotgun.

Investors could look at an intriguing name - something like Western Digital (WDC).

WDC has a $19 billion valuation and in the long term future could be considered a bargain looking back.

Its earnings weren’t great with another quarter of decelerating revenue.

Western Digital (WDC) reported a narrower-than-expected loss for its December quarter, with revenue just squeaking past expectations.

The business model has been affected due to the impact of structural changes the company implemented in its flash and HDD businesses.

Last quarter, the company said it would spin off its flash memory business, which has been grappling with a supply glut after talks of merging the unit with Japan's Kioxia stalled, by the second half of 2024.

The company said its second-quarter loss included $156 million underutilization-related charges in Flash and HDD.

Western Digital has struggled as demand for memory chips cooled in the past couple of years, but underlying shares have rallied in recent months.

WDC stock had gained nearly 40% since the end of October.

Cloud represented 35% of total revenue, with the quarterly growth attributed to higher “nearline” or onsite data storage shipments to data center customers and better nearline pricing. The increase in client revenue was driven by an increase in the average selling price of flash memory and customer revenue was driven by a seasonal surge in flash bit shipments.

Revenue came in at $3.023 billion, down 2.5% year-over-year but up 10% quarter-over-quarter.

In addition to the recovery in both Flash and HDD markets, I believe storage is entering a multi-year growth period.

Generative AI has quickly emerged as yet another growth driver and transformative technology that is reshaping all industries, all companies, and our daily lives.

Importantly, industry analysts estimate that the edge now represents approximately 80% of total NAND bit shipments, an increase from approximately 75% in 2022, which is another indication that cloud demand was significantly pulled in during the pandemic.

In addition, I believe the second wave of generative AI-driven storage deployments will spark a client and consumer device refresh cycle and reaccelerate content growth in PC, smartphone, gaming, and consumer in the coming years.

WDC has done some nice business specifically in the cloud division with some serious growth.

WDC is also at the center of the generative AI trend and they could be the recipient of “the tide lifts all boats.”

However, I don’t like how revenue as a whole isn’t growing causing major uproar in the investor community.

Splitting up the company should do the trick of weeding out the bad revenue from the good.

I do believe that WDC represents good value for buy-and-hold investors in the mid-$50 range.

This isn’t an ideal stock to trade in and out and even on an earnings beat, the stock sold off which isn’t what investors like to see in terms of price action.

There isn’t enough investor confidence in the stock yet, but that could change in the future.

Mad Hedge Technology Letter

March 3, 2021

Fiat Lux

Featured Trade:

(U.S. CHIP SHORTAGE IS REAL)

(WDC), (AMD), (MU)

Yes, the price is going up. And no, I am not talking about monthly grocery bills, but the price of semiconductor chips that help operate iPhones and will power autonomous driving vehicles.

The situation is so dire that US President Joe Biden signed an executive order calling for a supply chain review of semiconductors and IT technologies.

Yes, it’s that bad.

The drastic and imminent chip shortage is impacting a wide swath of tech firms we cover here at the Mad Hedge Technology Letter.

The order will also “facilitate needed investments to maintain America’s competitive edge and strengthen U.S. national security.”

Biden’s proactive decision to sign the executive order comes on the heels of several top U.S. semiconductor executives persuading US President Joe Biden earlier this month to resuscitate domestic chip manufacturing with “substantial funding” as part of the White House’s economic recovery and infrastructure plan.

In the fact sheet for the executive order, the White House said supply chains for semiconductors and advanced chip packaging technologies will be among four key areas where federal agencies will be directed to commence a 100-day review.

The White House acknowledged a massive underinvestment in semiconductor production that has caused manufacturing to shift abroad.

The critical issue was emphasized by U.S. semiconductor executives in a recent joint letter to Biden.

The US has leaned on foreign manufacturing for many products in the past 50 years, but semiconductor chips are the ones that could force US tech companies into a losing position and offer a pathway for Chinese tech firms to seize their chance as top dog.

The 100-day supply chain review will also look at critical minerals, including rare earths that are used for a variety of products, as well as large-capacity batteries and active pharmaceutical ingredients.

The shortages of chips and other components are a very real issue that can have a material impact on several adjacent industries, including bioinformatics companies and mechanical parts manufacturers that rely on simulation and modeling applications.

How does this affect chip companies?

Let’s take a look at one, Western Digital (WDC).

Shares are trading higher on signs of improving pricing in the flash-memory market.

I am short-term bullish on Western shares because a meaningful memory-chip price rise is in the cards for both flash NAND and DRAM.

A blast from the past Silicon Valley dinosaur that began as a disk-drive manufacturer, Western diversified into flash-memory products via its 2016 acquisition of SanDisk.

Encouraging NAND pricing also benefits Micron Technology (MU), which makes both NAND and DRAM chips.

The most important takeaway from my channel checks is that despite increased attempts by cloud and enterprise customers to lock in prices for second-half delivery, end contract numbers aren’t reflecting any good deals for the end buyer.

Manufacturers are convinced with their newfound pricing power and will wield it to full effect.

Expect significant price increases until the shortage is cured, and this could result in many end projects being shelved because of funding issues.

For semi chip firms, a bountiful harvest will make 2021 earnings report glisten in the form of meaningful expansion in margins, which have been under pressure since 2018.

My initial prediction is that prices will rise 5% to 10% from the fourth quarter—and that pricing for the second quarter is tracking up another 10% or more sequentially making it a 20% rise in less than half a year.

Memory manufacturers like Micron (MU), AMD (AMD), Samsung, and Western Digital (WDC) are in line to overperform in 2021.

Mad Hedge Technology Letter

February 5, 2020

Fiat Lux

Featured Trade:

(HOW TO TRADE THE CORONAVIRUS)

(APPL), (MSFT), (TSLA), (MU), (WDC), (ZM)

Like a powerful mule, I believe the American tech sector will muscle through the shock of the China coronavirus.

The tech sector will do what it does best, take the lead and put the entire American economy on its back and carry it through when doubts of decelerating global growth are asked of it.

I quantify this as an opportunity for the American tech sector.

Let’s look at some of the short-term contagion American tech companies are absorbing, as well as some opportunities in tech delivered by this sad pandemic.

Apple (AAPL) has made the decision to shutter all Apple stores in mainland China.

Their corporate offices have also gone into sleep mode and that means 10,000 people will need to make do with work stoppages which also include the component makers that supply Apple.

The stoppage is until February 9th, but only if the coronavirus has been effectively thwarted.

The Chinese populace isn’t willing to go out on the street and have barricaded themselves inside their apartments to avoid catching the virus.

Quarantining large areas is an unprecedented move from the Chinese communist party highlighting the poor handling of the situation in the early stages.

China is a critical revenue driver for Apple constituting 15% of revenue.

The delay in manufacturing will result in 3% of iPhone unit shipments being pushed out from March to June.

However, if the lockdown spills into late February or March, then there will be a major hit to the Chinese consumer which could muddy Apple’s bottom line.

Apple’s supply chain could get up-and-running if the shutdown lasts a few weeks but if we are talking months then project dates could get put on the permanent back burner.

Apple is arguably the most prominent American tech company to be affected deeply by the coronavirus but there are others.

The Chinese communist party has put the operation of the new Shanghai Tesla (TSLA) factory on ice which will delay the company’s production of the Model 3 there.

The ramp-up of the Model 3 production will be delayed by a week and a half and the shutdown may “slightly” impact the company’s profitability in the first quarter of 2020, said Tesla’s finance chief Zach Kirkhorn.

As of now Tesla has estimated a 10-day delay to the Shanghai-built Model 3s due to a government-required factory shutdown and the facility will remain locked until February 9th.

Tesla have been churning out cars at its Shanghai factory only since the end of 2019.

The deliveries are an emerging revenue driver as Tesla hopes to gain a foothold in China, the world’s largest market for electric vehicles.

Fortunately, Shanghai-produced Teslas only make up a tiny part of Tesla’s overall revenue, meaning there will be minimal impact to the financials.

The outbreak could have a positive effect for some domestic semiconductor companies.

The chaos resulting from the virus will likely upset operations at Wuhan-based Yangtze Memory Technologies Co. and Wuhan Xinxin Semiconductor Manufacturing Corp., who have been stealing market share from their American competitors.

Yangtze Memory Technologies is China’s leading NAND flash memory producer.

NAND chips are the flash memory chips used in USB drives and smaller devices such as digital cameras as opposed to DRAM, or dynamic random access memory, the type of memory commonly used in PCs and servers.

Micron (MU) and Western Digital (WFC) could swoop in to meet the extra demand.

Another company that could seize a great opportunity because of the coronavirus is Zoom Video Communications (ZM).

The CEO of Zoom Video said, “If you cannot travel ... you need to have a very reliable secure tool like Zoom” and product usage “is very, very high since the last of the month, last week. Almost every day - that’s a record usage.”

Since Chinese tech workers are barricading themselves indoors, Zoom has been the tool of choice to collaborate with coworkers who are in the same situation.

Not that the video conferencing software company needed help, I have recommended this company as a solid buy and hold since the stock dipped to $62.

This new boost will pour gas on the flames and the stock price reacted in lockstep by rocketing 15% in just one trading day.

When the likes of Alphabet’s Google, Facebook, Apple, Microsoft, and Ford Motor are ordered to work from home, videoconferencing, online meetings, chat and mobile collaboration services shoot through the roof.

Video conferencing will become a $43 billion total addressable market in the coming years, and I believe Zoom is easily a $150 stock.

In short, the coronavirus will hurt some tech companies short-term, benefits others, and have no effect on tech firms with negligible China exposure.

Facebook is a stock that I recently executed a call spread on, and they are blocked from operating in the mainland and will feel no difference from this virus outbreak.

Looking even deeper into the matter, the short-term hit to revenues will only be temporary unless this virus wipes out most of China.

The most likely scenario is that less than 1,000 people will eventually die from this and 99.9% of that will be deaths in mainland China.

Investors should look at buying on any substantial dip – the tech narrative is still unbroken.

Mad Hedge Technology Letter

November 4, 2019

Fiat Lux

Featured Trade:

(THE CHICKENS COME HOME TO ROOST WITH SMALL TECH),

(AAPL), (MSFT), (AMZN), (GOOGL), (WDC), (TXI), (ANET), (PINS)

The tech story is still intact, but the edges are losing its shine.

That is the takeaway from the recent slew of earnings reports from many of the prominent yet second-tier tech companies.

On one hand, companies like Apple (AAPL) have been holding the fort as it blasts through to new highs even amid the backdrop of the Chinese trade war that has dragged many of the strong tech names into the mud.

What we did see lately was a magnificent swan dive by chip names like Western Digital (WDC) and Texas Instruments (TXI) which were blindsided by 10-15% haircuts because of lackluster guidance.

The agony didn’t stop there with second rate cloud names like Pinterest (PINS) and Arista Networks, Inc. (ANET) reaching for scapegoats for their weak guidance. These took instant 20% haircuts.

The problem with smaller stocks like these besides having narrower spreads, they are slaves to just a few contracts and when one goes, their guidance and revenue estimates implode in their faces.

Arista slid more than 25% on news that they expect quarterly revenue of $540 million-$560 million, with the midpoint about 20% below the previous Street consensus at $686.2 million.

Arista CEO Jayshree Ullal said in a statement that the company expects “a sudden softening in Q4 with a specific cloud titan customer.”

That is Facebook who comprise about 10% of Arista’s revenue composition because Facebook has pulled back the reigns on cloud spend to cut costs amid a murky global backdrop and regulatory minefield.

Unfortunately, second tier cloud names must accept that they do not offer the best pricing when directly competing with the superior cloud names of Google Cloud, Microsoft Azure, and Amazon Web Services (AWS) because they simply can’t scale as well to the extent these monopolistic FANGs can.

Data storage often comes down to whoever has the cheapest cost of capital to pile into server farms allowing pricing to be ultra-cheap and these three companies win out.

If these firms lose one contract like Walmart’s switch over to Microsoft Azure from Amazon, it’s not a big deal.

It doesn’t put a 10% black hole in the revenue stream like for Arista.

Pinterest was one of the most overhyped IPOs of 2019 promising growth, growth and more growth.

Its digital ad business needs to deliver accelerating growth for its share price to rise and when the latest earnings report showed year-over-year growth slow from 62% to 47%, investors saw the writing on the wall.

The company only grew its users 8% in the lucrative North American market and 38% abroad.

But the foreign markets were tainted by the gruesome underbelly of earning only 13 cents per foreign users.

There is user growth but at the cost of an inferior quality of growth.

Analysts can clearly observe the accelerated erosion of Pinterest, and I can say from a personal point of view that the website isn’t that useful.

Management’s excuse was a tough comparison to the prior year but if a growth firm has a superior model, they should be able to grow past any minor problems if the secular trends stay hemmed in.

Weak excuses now and probably weak excuses next quarter as the global tech landscape gets squeezed even more at the periphery.

What does this all mean?

There has been a flight to tech quality into the Teflon names like Microsoft and Apple.

Names that are showing growth headaches saddled with too much competition and structural softness are getting killed.

Don’t even think about investing in the marginal names like Pinterest and Arista.

Better to be safe on your perch inside the moat than outside isolated from the drawbridge.

Not all tech is created equal and it's rearing its ugly face in a frothy market.

Mad Hedge Technology Letter

August 5, 2019

Fiat Lux

Featured Trade:

(THE CHINA TARIFF BOMBSHELL AND TECHNOLOGY),

(AAPL), (NVDA), (INTC), (MU), (WDC), (BBY)

With one little tweet, the state of technology and the companies that rely on the public markets that serve them went haywire.

U.S. President Donald Trump levied another 10% on the $300 billion that had not been tariffed up yet compounding the misery for anyone who has any vested interest in trade with mainland China.

The tariffs will take effect on September 1st.

How does this shake out for American technology?

Any brand tech name that has substantial supply chain operations can kiss their stay in the Middle Kingdom goodbye.

If management didn’t understand that before, then it's clear as night that they need to shift their supply chain out of the reaches of the Chinese communist party.

The U.S. Administration tripling down on China being our archnemesis means that any sort of cross-border economic trade or cultural exchange will be viewed through the prism of warped geopolitics.

The U.S. President Donald Trump has in fact taken a page out of the Chinese playbook turning everything he sees and touches into a transactional tool for what he is pursuing at the time or in the future.

Specific companies facing the wrath of the tariffs are companies as conspicuous as Apple filtering down to the SMEs that make local business local.

Semiconductor chips are a huge loser in this new development as the price of electronic goods will rise with the tariffs.

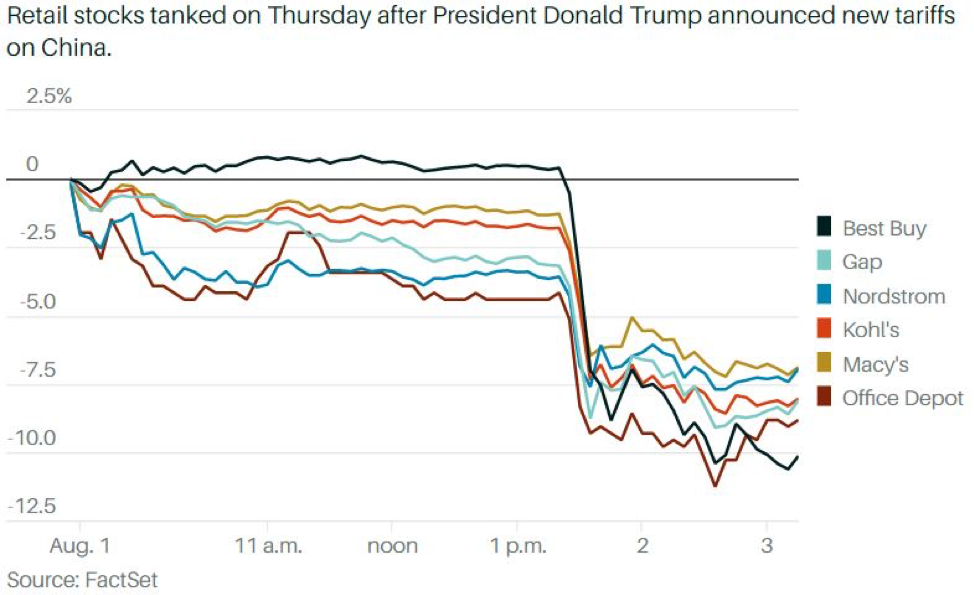

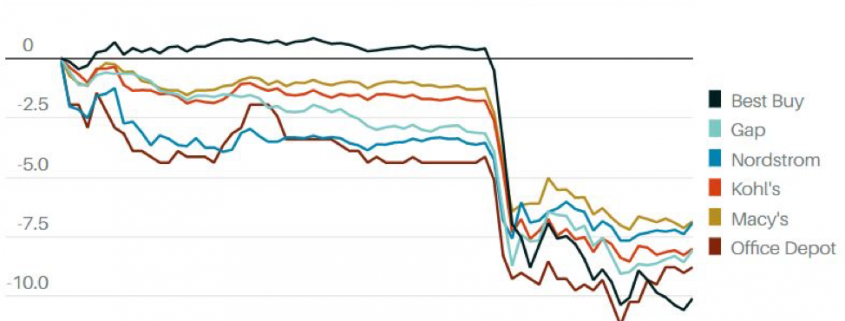

If you want a name that lies in the heart of electronic consumer goods, then BestBuy (BBY) would encapsulate this thesis and unsurprisingly they were taken out to the back of the woodshed and taught a lesson dropping 10% on the news.

Any technology outfit that imports goods from China will be hit as well and this means semiconductor chips along the lines of Nvidia (NVDA), Intel (INTC), Western Digital (WDC) and Micron (MU) among others.

Chips are the meat and bones that go into end products like iPads and a slew of smart devices.

Demand will be hit because of the cost of producing these types of consumer products will rise.

The softness is showing up in the numbers with Apple’s iPhone revenue down 12% year-over-year.

Samsung of Korea also showed that this isn’t just an American problem with their semiconductor division’s operating profits down 71% year-over-year.

The Korean conglomerate is in a spat with the Japanese government over war crimes from the second world war causing the Japanese government to bottleneck the supply of chemicals needed to produce high-level semiconductor chips.

The export restriction will drag down SK Hynix display business who is one of the largest producers of DRAM chips and also a Korean company.

Consumers are also using their phones longer with Apple iPhone customers holding their device up to 4 years delaying the refresh cycle.

The company that Steve Jobs built will have to repurpose themselves for a brave new tech landscape that includes heavier regulation, trade tariffs, and device saturation.

When investors talk about the “low hanging fruit,” at this point, Apple isn’t one of them.

And if you think the services business is a cakewalk, ponder about how many apps and behemoths that spit out a whole lineup of apps.

Apple still has its ecosystem and should guard it with its life, this is the same ecosystem that can charge Google around $10 billion per year to slap on Google search as the primary search engine on Apple devices.

Expect tech to telegraph a deceleration in revenue for the last quarter and next year.

The tech environment is brittle at this point and uncertainty wafts in the air like a hot stack of pancakes.