I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I go downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up-to-date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 12X pro.

Here is the bottom line which I have been warning you about for months. In 2022, you are going to have to work twice as hard to earn half as much money with double the volatility.

It’s not that I’ve turned bearish. The cause of the next bear market, a recession, is at best years off. However, we are entering the third year of the greatest bull market of all time. Expectations have to be toned down and brought back to earth. Markets will no longer be so strong that they forgive all mistakes, even mine.

2022 will be a trading year. Play it right, and you will make a fortune. Get lazy and complacent and you’ll be lucky to get out with your skin still attached.

If you think I spend too much time absorbing conspiracy theories or fake news from the Internet, let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2022

1) How soon will the Omicron wave peak?

2) Will the end of the Fed’s quantitative easing knock the wind out of the bond market?

3) Will the Russians invade the Ukraine or just bluster as usual?

4) How much of a market diversion will the US midterm elections present?

5) Will technology stocks continue to dominate, or will domestic recovery, and value stocks take over for good?

6) Can the commodities boom get a second wind?

7) How long will the bull market for the US dollar continue?

8) Will the real estate boom continue, or are we headed for a crash?

9) Has international trade been permanently impaired or will it recover?

10) Is oil seeing a dead cat bounce or is this a sustainable recovery?

The Thumbnail Portfolio

Equities – buy dips Bonds – sell rallies Foreign Currencies – stand aside Commodities – buy dips Precious Metals – stand aside Energy – stand aside Real Estate – buy dips Bitcoin – Buy dips

1) The Economy

What happens after a surprise variant takes Covid cases to new all-time highs, the Fed tightens, and inflation soars?

Covid cases go to zero, the Fed flip flops to an ease and inflation moderates to its historical norm of 3% annually.

It all adds up to a 5% US GDP growth in 2022, less than last year’s ballistic 7% rate, but still one of the hottest growth rates in history.

If Joe Biden’s build-back batter plan passes, even in diminished form, that could add another 1%.

Once the supply chain chaos resolves inflation will cool. But after everyone takes delivery of their over orders conditions could cool.

This sets up a Goldilocks economy that could go on for years: high growth, low inflation, and full employment. Help wanted signs will slowly start to disappear. A 3% handle on Headline Unemployment is within easy reach.

The weak of heart may want to just index and take a one-year cruise around the world instead in 2022 (here's the link for Cunard).

So here is the perfect 2022 for stocks. A 10% dive in the first half, followed by a rip-roaring 20% rally in the second half. This will be the year when a big rainy-day fund, i.e., a mountain of cash to spend at market bottoms, will be worth its weight in gold.

That will enable us to load up with LEAPS at the bottom and go 100% invested every month in H2.

That should net us a 50% profit or better in 2022, or about half of what we made last year.

Why am I so cautious?

Because for the first time in seven years we are going to have to trade with a headwind of rising interest rates. However, I don’t think rates will rise enough to kill off the bull market, just give traders a serious scare.

The barbell strategy will keep working. When rates rise, financials, the cheapest sector in the market, will prosper. When they fall, Big Tech will take over, but not as much as last year.

The main support for the market right now is very simple. The investors who fell victim to capitulation selling that took place at the end of November never got back in. Shrinking volume figures prove that. Their efforts to get back in during the new year could take the S&P 500 as high as $5,000 in January.

After that the trading becomes treacherous. Patience is a virtue, and you should only continue new longs when the Volatility Index (VIX) tops $30. If that means doing nothing for months so be it.

We had four 10% corrections in 2021. 2022 will be the year of the 10% correction.

Energy, Big Tech, and financials will be the top-performing sectors of 2022. Big Tech saw a 20% decline in multiples in 2022 and will deliver another 30% rise in earnings in 2022, so they should remain at the core of any portfolio.

It will be a stock pickers market. But so was 2021, with 51% of S&P 500 performance coming from just two stocks, Tesla (TSLA) and Alphabet (GOOGL).

However, they are already so over-owned that they are prone to dead periods as long as eight months, as we saw last year. That makes a multipronged strategy essential.

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a 2022 business. This time, bonds face the gale force headwinds of three promised interest rates hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

For the first time in ages, I did no foreign exchange trades last year. That is a good thing because I was wrong about the direction of the dollar for the entire year.

Sometimes, passing on bad trades is more important than finding good ones.

I focused on exploding US debt and trade deficits undermining the greenback and igniting inflation. The market focused on delta and omicron variants heralding new recessions. The market won.

The market won’t stay wrong forever. Just as bond crash is temporarily in a holding pattern, so is a dollar collapse. When it does occur, it will happen in a hurry.

5) Commodities (FCX), (VALE), (DBA)

The global synchronized economic recovery now in play can mean only one thing, and that is sustainably higher commodity prices.

The twin Covid variants put commodities on hold in 2021 because of recession fears. So did the Chinese real estate slowdown, the world’s largest consumer of hard commodities.

The heady days of the 2011 commodity bubble top are now in play. Investors are already front running that move, loading the boat with Freeport McMoRan (FCX), US Steel (X), and BHP Group (BHP).

Now that this sector is convinced of an eventual weak US dollar and higher inflation, it is once more the apple of traders’ eyes.

China will still demand prodigious amounts of imported commodities once again, but not as much as in the past. Much of the country has seen its infrastructure build out, and it is turning from a heavy industrial to a service-based economy, like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase 11-fold in a decade to accommodate this increase, no easy task, or prices will have to ride.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate commodities on dips.

Snow Angel on the Continental Divide

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (USO), (XLE), (AMLP)

Energy may be the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero.

However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are drinking their own Kool-Aid. Instead of reinvesting profits back into their new exploration and development, as they have for the last century, they are paying out more in dividends.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and shares prices for the energy industry.

Energy stocks are also massively under-owned, making them prone to rip-you-face-off short squeezes. Energy now counts for only 3% of the S&P 500. Twenty years ago it boasted a 15% weighting.

The gradual shut down of the industry makes the supply/demand situation more volatile. Therefore, we could top $100 a barrel for oil in 2022, dragging the stocks up kicking and screaming all the way.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to them, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2021 was a terrible year for precious metals. With inflation soaring, stocks volatile, and interest rates going nowhere, gold had every reason to rise. Instead, it fell for almost all of the entire year.

Bitcoin stole gold’s thunder, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand was just not enough to keep gold afloat.

This will not be a permanent thing. Chart formations are starting to look encouraging, and they certainly win the price for a big laggard rotation. So, buy gold on dips if you have a stick of courage on you.

Would You Believe This is a Blue State?

8) Real Estate (ITB), (LEN)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

There is no doubt a long-term bull market in real estate will continue for another decade, although from here prices will appreciate at a 5%-10% slower rate.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xer’s who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xers since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis.

If they have prospered, banks won’t lend to them. Brokers used to say that their market was all about “location, location, location.” Now it is “financing, financing, financing.” Imminent deregulation is about to deep-six that problem.

There is a happy ending to this story.

Millennials now aged 26-44 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to Zoom, many are never returning to the cities. So has the migration from the coast to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market in 2021, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should rocket during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a coming labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are taken into account. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 13 years. The 50% of small home builders that went under during the crash aren’t building new homes today.

We are still operating at only a half of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with.

You will boast to your grandchildren how little you paid for your house, as my grandparents once did to me ($3,000 for a four-bedroom brownstone in Brooklyn in 1922), or I do to my kids ($180,000 for a two-bedroom Upper East Side Manhattan high rise with a great view of the Empire State Building in 1983).

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now. It’s also a great inflation play.

If you borrow at a 3.0% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free.

How hard is that to figure out? That math degree from UCLA is certainly earning its keep.

Crossing the Bridge to Home Sweet Home

9) Bitcoin

It’s not often that new asset classes are made out of whole cloth. That is what happened with Bitcoin, which, in 2021, became a core holding of many big institutional investors.

But get used to the volatility. After doubling in three months, Bitcoin gave up all its gains by year-end. You have to either trade Bitcoin like a demon or keep your positions so small you can sleep at night.

By the way, right now is a good place to establish a new position in Bitcoin.

10) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff has made the ten-mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 13 Pro, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above.

Good luck and good trading in 2022!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2022!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-05 13:00:512022-01-05 18:26:592022 Annual Asset Class Review

Below please find subscribers’ Q&A for the February 17 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are we buying gold on dips?

A: Not yet. As long as you have a ballistic move in bitcoin going on, you don't want to touch gold. Eventually gold does get dragged up by the global bull market in commodities, but silver is more preferable since it moves up at twice the rate of gold in bull markets.

Q: Is it time to buy Amazon (AMZN) LEAPS?

A: Yes, I am looking for a move to $5,000 a share in Amazon with the onset of enormous GDP figures. Exploding consumer spending may be what breaks Amazon out of its current six-month range. I would do something like a two-year LEAP with the $3,600-$3,700 in Amazon. Be cautious and stay near the money. You should get like a 400% or 500% return on that LEAP at expiration, or sooner.

Q: What's your view on Tesla (TSLA)?

A: It looks tired—lower lows, lower highs. We’re in a short-term downtrend that could last several months. I’m holding off on buying Tesla until we find a bottom. I just have one $150 out-of-the-money call spread that expires in 20 days, and that’s it. We paired our position way back on Tesla. Wait for the market to come to you, if you can get Tesla under $700, that's a great time to buy LEAPS on Tesla.

Q: Are you still bearish on energy (XLE)?

A: Short term no, long term yes. You’re trying to catch a rally in a long-term bear market. Some people can do that, some people can’t. It’s the next buggy whip industry, the next American Leather, which completely vaporized.

Q: What about the calls for $100 oil (USO)?

A: Yes, after the markets went up $10 dollars in a day you always see calls for $100 oil. If the energy crisis in Texas shows us anything, it’s that we have to move away from oil as an energy source much faster than we thought because its distribution and production system freeze.

Q: Are you expecting a short-term correction (SPY)?

A: Yes but no more than 4%; there is still too much cash on the sidelines.

Q: Have airline leisure stocks run too far?

A: No, they are coming off of much lower lows so they can go to much higher highs. Almost all restrictions should be gone in six months—I’m trying to time my Australia trips and I think in six months may get to the point where, if you show proof of vaccination and submit to a 3 day test, they will let you into the country. But in six months you won’t be able to get an airline or hotel reservation.

Q: What about the AT&T (T) yield play and 5G play?

A: Yes, I still like AT&T and you should probably buy it about here. All these legacy telecom companies are going to have big moves once 5G accelerates allowing a vast expansion of streaming and other high-end services.

Q: Is CRISPR (CRSP) a good LEAP candidate?

A: Yes, and you can do something like the $200-$210 two years out because it’ll almost certainly get taken over before then.

Q: What’s a good LEAP for Tesla?

A: Wait for it to drop to $700 first and then buy something like the $900-$1000 two years out.

Q: What do you think of Apple?

A: Apple (AAPL) is taking a rest waiting for the 5G rollout to reaccelerate. Our target for Apple this year is $200.

Q: Do we sell in May and go away?

A: I would just go away and keep all your longs. The trouble is, trying to be ultra-smart and time all this stuff in a runaway bull market, you find it a lot harder to get in when you come back; you go “oh my gosh these things are up so much,” you don’t buy anything, and then it doubles. I’ve seen that a lot in the past, New York in 1971, Tokyo in 1987, Dotcom stocks in 1985, add US stocks in 2015.

Q: What do you think of Riot (RIOT) stock?

A: Wouldn't touch it with a ten-foot pole. If I didn’t want to buy bitcoin at $1, I'm not going to want to buy it at $51,000. Go elsewhere for your bitcoin advice, except you’ll hear the same thing: it will go up because it’s gone up. You should use it as a risk indicator. That’s essentially what all bitcoin analysts will tell you because there's nothing to analyze. There are no earnings, there's not even any physical presence anywhere to analyze, no customer support. If you can get seven 10 baggers like we did last year, with Zoom (ZM), Roku (ROKU), Tesla (TSLA), and Nvidia (NVDA) —why bother with cryptocurrencies?

Q: What are your thoughts on travel?

A: My take is that leisure travel is returning in mass but that the business travelers will shy away; and that will be true for this year but probably not next year. I think business travel will come back once it’s 100% safe and once all the companies are making money again and can afford travel.

Q: Is Trilogy Metals Inc. (TMQ) a good buy? It has Copper, Zinc, and some exposure to Gold and Silver.

A: Yes, it is a buy. Most commodity prices should double from these levels; and probably the smartest ones to buy are the ones that haven't moved yet—gold and silver, but silver especially. The world will come roaring back and it needs every possible metal it can get its hands on.

Q: What do you think of the cannabis stocks (TLRY), (ACB)?

A: That is one of several small bubbles in the markets that I don't want to touch at all. How hard is it to grow a weed? Barriers to entry are zero. Massive competition from the black market, as about 30% of the cannabis demand is still going to your local drug dealer who doesn’t have to pay taxes, whereas you get double taxed with a pot company—35% retail sales taxes and then taxes on the profits on top of that. So no thank you, Mary Jane.

Q: Do you think Warren Buffet is still the leading thought contributor to personal finance, or is he outdated?

A: Berkshire Hathaway is up 10% this year, and the Dow is up only 2.8%, so I would say he’s still pretty well in touch with the markets; and he has very heavy weightings in Coca Cola (KO), Financials (XLF), and Apple (AAPL), as well as some energy stocks. Good discipline and good strategy never go out of style.

Q: Is the Texas energy disaster going to set the US’ way on renewable energy faster?

A: Yes, it does force people to consider the move into alternative energy sources much faster, especially when the old energy sources go to zero and then have whole states lose their power sources. Look how the governor of Texas is blaming frozen windmills, which only account for 7% of the Texas energy supply. What a joke! I’ll lend him my hairdryer and they’ll work. Notice the propensity to immediately blame others for their own mistakes. That is terrible leadership. Texas is going to turn blue.

Q: Is climate change overhyped in the US stock market?

A: Absolutely yes, that’s why I haven’t been buying any of these. They tend to be smaller companies, and ever since Biden got the lead in the primaries and the polls last spring this whole sector, and ESG investing in general, has been on an absolute tear and is wildly expensive. I call these feel-good stocks; people buy them because they make them feel good but very few of these actually make real money. I prefer to stick to the real money plays of which there are more than enough around.

Q: Do you like rare earth such as the Van Eck Vectors Rare Earth/Strategic Metals ETF (REMX)?

A: I do like rare earths. You need them for practically anything electronic. China's been withholding supplies again, which they like to do from time to time just to rattle our cage because we need them for all our weapons systems. But this is also prone to bubbles, so be careful when you buy it that you’re not paying up too much. By the way, the (REMX) ETF was brought out at the absolute peak of the last rare earth bubble, which we covered extensively 11 years ago. We got people in at the very bottom of rare earth, and things went up ten times. Then we got everybody out and people said I was being bearish too soon, so I never got invited to conferences again. After that, it went down for eight straight years.

Q: Don’t you think frozen windmills and solar speak for more reliance on oil than less? Biden administration limits on oil will drive up prices.

A: You’re right on the second part; creating shortage of supply will cause price increases. But frozen windmills are a result of lack of capital investment and planning. It turns out all of the windmills in the northern part of the US have electric heaters, so they don’t freeze because it gets colder up there. They didn’t do that in Texas to save money, and now they have lost about 7% of the total Texas energy supply. So bad management was the issue there. Penny-wise and pound-foolish.

Q: Are commodities in general in play? What is the best ETF for commodities?

A: The trouble with commodities is there is no one big catch all commodity ETF. However, you can expect one soon; as things peak or have big runs, they tend to generate new ETFs like new children because the demand is there. In the commodities world, there are lots of individual 1x and 2x ETFs like the gold ETF (GLD), the silver (SLV), the copper (CPER), and so on. But there isn’t one good basket I’ve found. You can always create your own by buying small amounts of each of the leading companies, which is probably the best thing to do.

Q: What is the best property value right now?

A: That would be Mississippi; they have the lowest housing prices in the United States. Unfortunately, low cost of living, low tax states also have the worst education systems, which doesn’t matter of course if you don't have kids. In the end, you get what you pay for. It’s OK if you don’t mind dealing with stupid people every day, which I do. I can always tell when I’m dealing with customer support in the deep south because literacy falls off a cliff.

Q: Should we get a 10% correction soon?

A: Probably not; the last 10% correction needed a presidential election to scare the daylights out of you, and there's nothing like that on the horizon now. Maybe we’ll get another 5% correction on a game stop type incident, but there's just too many people trying to get into the stock market now. People who were selling last March/April are the same people who are buying now.

Q: Is there a bright future for hydrogen?

A: No, electricity is infinitely scalable, and hydrogen isn’t. It’s about as scalable as gasoline because you have to move it around in big tankers, keep it at 434.5 degrees Fahrenheit below zero, which is very expensive and has an unfortunate tendency to blow up. So, I never bought into the hydrogen thesis, except for local use of fleets where everyone gets all their hydrogen from a central facility.

Q: What will be the best performing sector in the next 1-3 months?

A: Your bond short and your financials. It’s the same trade. And it’s the one sector that no one asked about today.

Q: Do you think bitcoin is a bubble poised to pop at some point?

A: Yes, but who knows where that is; bubble tops are impossible to predict, especially when there are no valuation metrics. Bottoms can be measured with valuation metrics, but tops can’t because greed is an immeasurable quantity. However, it will certainly pop when they suddenly decide to increase the total outstanding number of bitcoins, which may seem unlikely now but is inevitable.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/john-thomas-tropics.png432324Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-19 10:02:082021-02-19 10:28:48February 17 Biweekly Strategy Webinar Q&A

(LAST CHANCE TO ATTEND THE FRIDAY, FEBRUARY 7 PERTH, AUSTRALIA STRATEGY LUNCHEON)

(JANUARY 22 BIWEEKLY STRATEGY WEBINAR Q&A),

(BA), (IBM), (DAL), (RCL), (WFC),

(JPM), (USO), (UNG), (KOL), (XLF),

(SEE YOU IN TWO WEEKS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-01-24 04:08:542020-01-23 22:37:04January 24, 2020

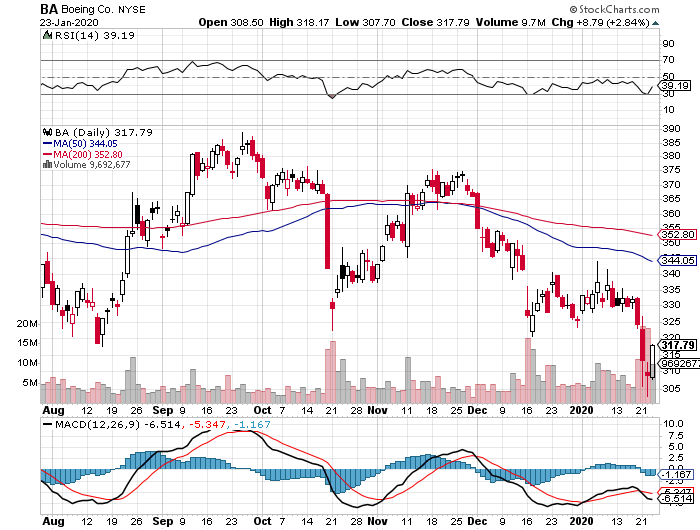

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 22Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming! Q: Are you concerned about a kitchen sink earnings report on Boeing (BA) next week?

A: No, every DAY has been a kitchen sink for Boeing for the past year! Everyone is expecting the worst, and I think we’re probably going to try to hold around the $300 level. You can’t imagine a company with more bad news than Boeing and it's actually acting as a serious drag on the entire economy since Boeing accounts for about 3% of US GDP. If (BA) doesn’t break $300, you should buy it with both hands as all the bad news will be priced in. That's why I am long Boeing.

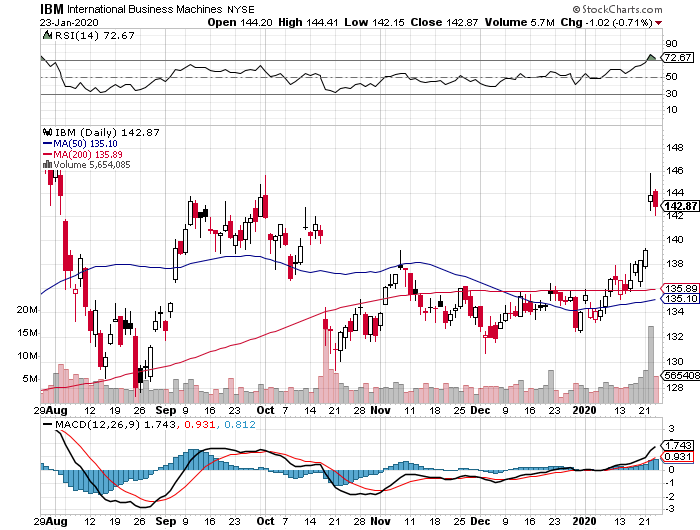

Q: Do you think IBM is turning around with its latest earnings report?

A: They may be—They could have finally figured out the cloud, which they are only 20 years late getting into. They’ve been a lagging technology stock for years. If they can figure out the cloud, then they may have a future. They obviously poured a lot into AI but have been unable to make any money off of it. Lots of PR but no profits. People are looking for cheap stuff with the market this high and (IBM) certainly qualifies.

Q: Will the travel stocks like airlines and cruise companies get hurt by the coronavirus?

A: Absolutely, yes; and you’re seeing some pretty terrible stock performance in these companies, like Delta (DAL), the cruise companies like Royal Caribbean Cruises (RCL), and the transports, which have all suffered major hits.

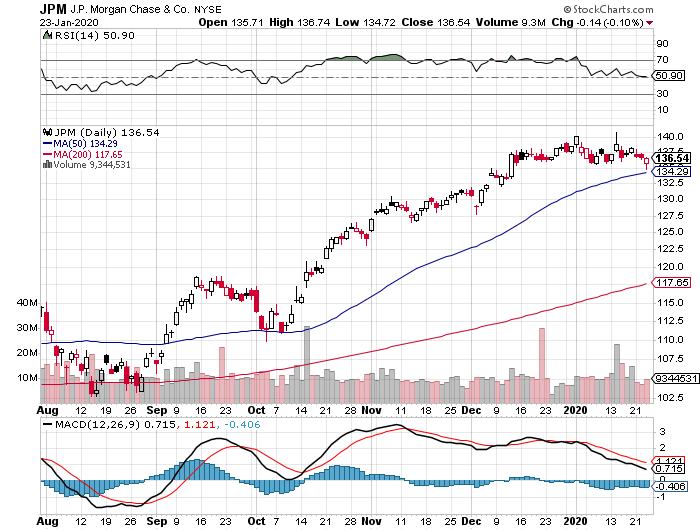

Q: Will the Wells Fargo (WFC) shares ever rebound? They are the cheapest of the major banks.

A: Someday, but they still have major management problems to deal with, and it seems like they’re getting $100 million fines every other month. I would stay away. There are better fish to fry, even in this sector, like JP Morgan (JPM).

Q: Will a decrease in foreign direct investment hurt global growth this year?

A: For sure. The total CEO loss of confidence in the economy triggered by the trade war brought capital investment worldwide to a complete halt last year. That will likely continue this year and will keep economic growth slow. We’re right around a 2% level right now and will probably see lower this quarter once we get the next set of numbers. To see the stock market rise in the face of falling capital spending is nothing short of amazing.

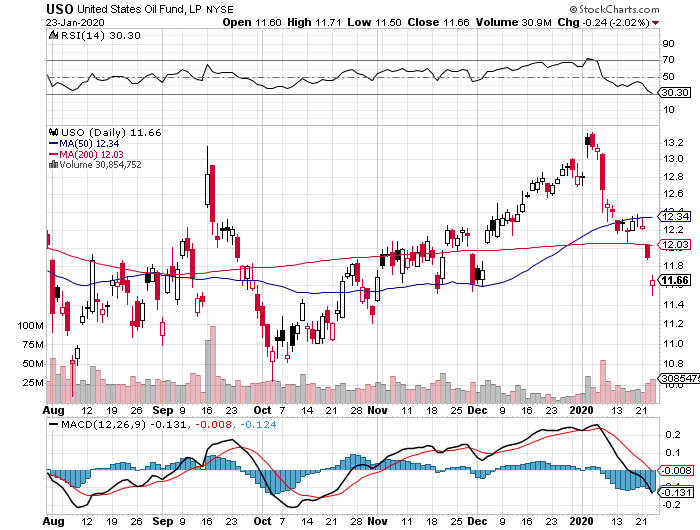

Q: Do you think regulation is getting too cumbersome for corporations?

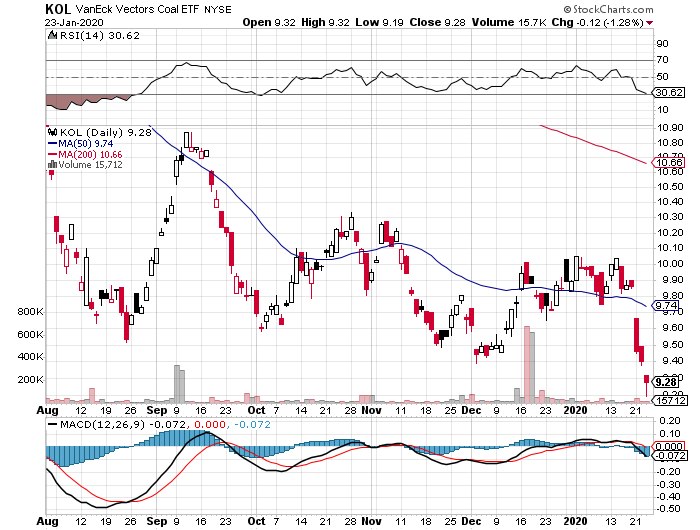

A: No, regulation is at a 20-year low for corporations, especially if you’re an oil (USO), gas (UNG) or coal producer (KOL), or in the financial industry (XLF). That’s one of the reasons that these stocks are rising as quickly as they have been. What follows a huge round of deregulation? A financial crisis, a crashing stock market, and a huge number of bankruptcies.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-01-24 04:04:362020-05-11 14:14:48January 22 Biweekly Strategy Webinar Q&A

Going into January 2018, the big banks were highlighted as the pocket of the equity market that would most likely benefit from a rising rate environment which in turn boosts net interest margins (NIM).

Fast forward a year and take a look at the charts of Bank of America (BAC), Citibank (C), JP Morgan (JPM), Goldman Sachs (GS), and Morgan Stanley (GS), and each one of these mainstay banking institutions are down between 10%-20% from January 2018.

Take a look at the Financial Select Sector SPDR ETF (XLF) that backs up my point.

And that was after a recent 10% move up at the turn of the calendar year.

As much as it pains me to say it, bloated American banks have been completely caught off-guard by the mesmerizing phenomenon that is FinTech.

Banking is the latest cohort of analog business to get torpedoes by the brash tech start-up culture.

This is another fitting example of what will happen when you fail to evolve and overstep your business capabilities allowing technology to move into the gaps of weakness.

Let me give you one example.

I was most recently in Tokyo, Japan and was out of cash in a country that cash is king.

Japan has gone a long way to promoting a cashless society, but some things like a classic sushi dinner outside the old Tsukiji Fish Market can’t always be paid by credit card.

I found an ATM to pull out a few hundred dollars’ worth of Japanese yen.

It was already bad enough that the December 2018 sell-off meant a huge rush into the safe haven currency of the Japanese Yen.

The Yen moved from 114 per $1 down to 107 in one month.

That was the beginning of the bad news.

I whipped out my Wells Fargo debit card to withdraw enough cash and the fees accrued were nonsensical.

Not only was I charged a $5 fixed fee for using a non-Wells Fargo ATM, but Wells Fargo also charged me 3% of the total amount of the transaction amount.

Then I was hit on the other side with the Japanese ATM slamming another $5 fixed fee on top of that for a non-Japanese ATM withdrawal.

For just a small withdrawal of a few hundred dollars, I was hit with a $20 fee just to receive my money in paper form.

Paper money is on their way to being artifacts.

This type of price gouging of banking fees is the next bastion of tech disruption and that is what the market is telling us with traditional banks getting hammered while a strong economy and record profits can’t entice investors to pour money into these stocks.

FinTech will do what most revolutionary technology does, create an enhanced user experience for cheaper prices to the consumers and wipe the greedy traditional competition that was laughing all the way to the bank.

The best example that most people can relate to on a daily basis is the transportation industry that was turned on its head by ride-sharing mavericks Uber and Lyft.

But don’t ask yellow cab drivers how they think about these tech companies.

Highlighting the strong aversion to traditional banking business is Slack, the workplace chat app, who will follow in the footsteps of online music streaming platform Spotify (SPOT) by going public this year without doing a traditional IPO.

What does this mean for the traditional banks?

Less revenue.

Slack will list directly and will set its own market for the sale of shares instead of leaning on an investment bank to stabilize the share price.

Recent tech IPOs such as Apptio, Nutanix and Twilio all paid 7% of the proceeds of their offering to the underwriting banks resulting in hundreds of millions of dollars in revenue.

Directly listings will cut that fee down to $10-20 million, a far cry from what was once status quo and a historical revenue generation machine for Wall Street.

This also layers nicely with my general theme of brokers of all types whether banking, transportation, or in the real estate market gradually be rooted out by technology.

In the world of pervasive technology and free information thanks to Google search, brokers have never before added less value than they do today.

Slowly but surely, this trend will systematically roam throughout the economic landscape culling new victims.

And then there are the actual FinTech companies who are vying to replace the traditional banks with leaner tech models saving money by avoiding costly brick and mortar branches that dot American suburbs.

PayPal (PYPL) has been around forever, but it is in the early stages of ramping up growth.

That doesn’t mean they have a weak balance sheet and their large embedded customer base approaching 250 million users has the network effect most smaller FinTech players lack.

PayPal is directly absorbing market share from the big banks as they have rolled out debit cards and other products that work well for millennials.

They are the owners of Venmo, the super-charged peer-to-peer payment app wildly popular amongst the youth.

Shares of PayPal’s have risen over 200% in the past 2 years and as you guessed, they don’t charge those ridiculous fees that banks do.

Wells Fargo and Bank of America charge a $12 monthly fee for balances that dip below $1,500 at the end of any business day.

Your account at PayPal can have a balance of 0 and there will never be any charge whatsoever.

Then there is the most innovative FinTech company Square who recently locked in a new lease at the Uptown Station in Downtown Oakland expanding their office space by 365,000 square feet for over 2,000 employees.

Square is led by one of the best tech CEOs in Silicon Valley Jack Dorsey.

Not only is the company madly innovative looking to pounce on any pocket of opportunity they observe, but they are extremely diversified in their offerings by selling point of sale (POS) systems and offering an online catering service called Caviar.

They also offer software for Square register for payroll services, large restaurants, analytics, location management, employee management, invoices, and Square capital that provides small loans to businesses and many more.

On average, each customer pays for 3.4 Square software services that are an incredible boon for their software-as-a-service (SaaS) portfolio.

An accelerating recurring revenue stream is the holy grail of software business models and companies who execute this model like Microsoft (MSFT) and Salesforce (CRM) are at the apex of their industry.

The problem with trading this stock is that it is mind-numbingly volatile. Shares sold off 40% in the December 2018 meltdown, but before that, the shares doubled twice in the past two years.

Therefore, I do not promote trading Square short-term unless you have a highly resistant stomach for elevated volatility.

This is a buy and hold stock for the long-term.

And that was only just two companies that are busy redrawing the demarcation lines.

There are others that are following in the same direction as PayPal and Square based in Europe.

French startup Shine is a company building an alternative to traditional bank accounts for freelancers working in France.

First, download the app.

The company will guide you through the simple process — you need to take a photo of your ID and fill out a form.

It almost feels like signing up to a social network and not an app that will store your money.

You can send and receive money from your Shine account just like in any banking app.

After registering, you receive a debit card.

You can temporarily lock the card or disable some features in the app, such as ATM withdrawals and online payments.

Since all these companies are software thoroughbreds, improvement to the platform is swift making the products more efficient and attractive.

There are other European mobile banks that are at the head of the innovation curve namely Revolut and N26.

Revolut, in just 6 months, raised its valuation from $350 million to $1.7 billion in a dazzling display of growth.

Revolut’s core product is a payment card that celebrates low fees when spending abroad—but even more, the company has swiftly added more and more additional financial services, from insurance to cryptocurrency trading and current accounts.

Remember my little anecdote of being price-gouged in Tokyo by Wells Fargo, here would be the solution.

Order a Revolut debit card, the card will come in the mail for a small fee.

Customers then can link a simple checking account to the Revolut debit card ala PayPal.

Why do this?

Because a customer armed with a Revolut debit card linked to a bank account can use the card globally and not be charged any fees.

It would be the same as going down to your local Albertson’s and buying a six-pack, there are no international or hidden fees.

There are no foreign transaction fees and the exchange rate is always the mid-market rate and not some manipulated rate that rips you off.

Ironically enough, the premise behind founding this online bank was exactly that, the originators were tired of meandering around Europe and getting hammered in every which way by inflexible banks who could care less about the user experience.

Revolut’s founder, Nikolay Storonsky, has doubled down on the firm’s growth prospects by claiming to reach the goal of 100 million customers by 2023 and a succession of new features.

To say this business has been wildly popular in Europe is an understatement and the American version just came out and is ready to go.

Since December 2018, Revolut won a specialized banking license from the European Central Bank, facilitated by the Bank of Lithuania which allows them to accept deposits and offer consumer credit products.

N26, a German like-minded online bank, echo the same principles as Revolut and eclipsed them as the most valuable FinTech startup with a $2.7 Billion Valuation.

N26 will come to America sometime in the spring and already boast 2.3 million users.

They execute in five languages across 24 countries with 700 staff, most recently launching in the U.K. last October with a high-profile marketing blitz across the capital.

Most of their revenue is subscription-based paying homage to the time-tested recurring revenue theme that I have harped on since the inception of the Mad Hedge Technology Letter.

And possibly the best part of their growth is that the average age of their customer is 31 which could be the beginning of a beautiful financial relationship that lasts a lifetime.

N26’s basic current account is free, while “Black” and “Metal” cards include higher ATM withdrawal limits overseas and benefits such as travel insurance and WeWork membership for a monthly fee.

Sad to say but Bank of America, Wells Fargo, and the others just can’t compete with the velocity of the new offerings let alone the software-backed talent.

We are at an inflection point in the banking system and there will be carnage to the hills, may I even say another Lehman moment for one of these stale business models.

Online banking is here to stay, and the momentum is only picking up steam.

If you want to take the easy way out, then buy the Global X FinTech ETF (FINX) with an assortment of companies exposed to FinTech such as PayPal, Square, and Intuit (INTU).

The death of cash is sooner than you think.

This year is the year of FinTech and I’m not afraid to say it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-17 01:06:502019-07-09 04:56:36Why FinTech is Eating the Banks’ Lunch

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-09 01:06:162019-01-08 17:51:11January 9, 2019

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.