Mad Hedge Technology Letter

January 17, 2020

Fiat Lux

Featured Trade:

(WHY ZOOM IS ZOOMING)

(ZM)

Mad Hedge Technology Letter

January 17, 2020

Fiat Lux

Featured Trade:

(WHY ZOOM IS ZOOMING)

(ZM)

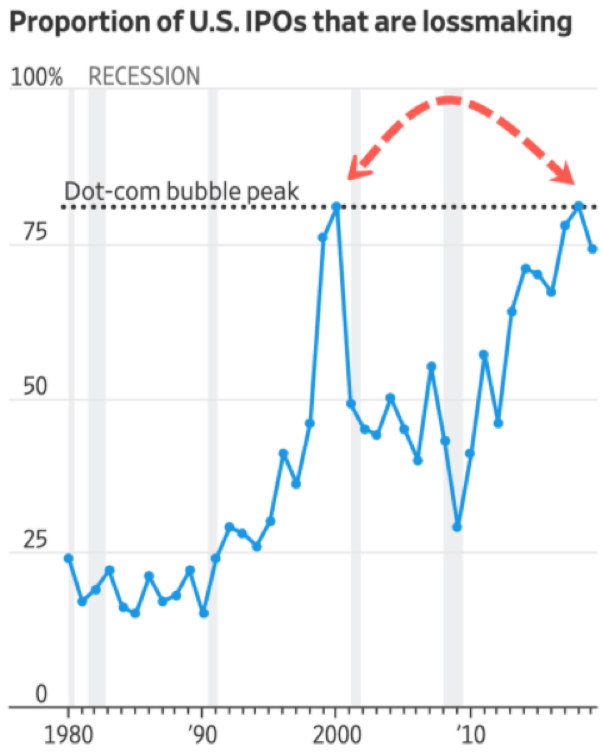

A report from a prominent new source reveals that in the past 12 months, 40% of all US-listed companies were losing money and of these, 17% were tech firms, the highest level since the Dot Com bubble.

That is why software gems like Zoom Video Communications, Inc. (ZM) should be bought and held, never to see the light of day ever again.

The company makes money at such an early stage of their development that it's hard not to get excited about the future.

Readers can indulge themselves in this high caliber tech growth stock, especially after they demonstrated that they are hitting on all cylinders after a high-flying earnings report.

Another prominent new source recently said that this company’s products are “changing the entire landscape” of U.S. business.

Just one instance they have infiltrated deep into real American business is the U.S. Postal Service.

They are starting to deploy Zoom Meetings more broadly across the organization after an extensive proof-of-concept.

The USPS is Zoom’s first major agency and major business win since they received FedRAMP approval in May.

Why did they pick Zoom?

Easy! Simply for Zoom’s high-quality video and audio.

Zoom’s share price cratered 40% since hitting the heights of $102 in July 2019 which was coincidentally the high for most post-IPO tech stocks of 2019.

It was an elevator straight down to no man’s land – but investors would be foolish to paint all hyper-growth companies with the same brush.

Filtering out the wheat from the chaff is critical and Zoom is the stock that still has the gloss on its outside package buttressed by its best-in-show video conferencing software.

There are no other proper alternatives in this sub-sector of software.

The volatility can be extreme making this name difficult to trade and constantly has dips of 7% even though the company crushes expectations.

I called for readers to scoop up shares in the low $60s and the stock is now healthily trading in the upper $70s as we hit the back half of January.

Remember that this company grew 96% just 3 quarters ago and it would be illogical to believe that the stock is being penalized from faltering to 85% today.

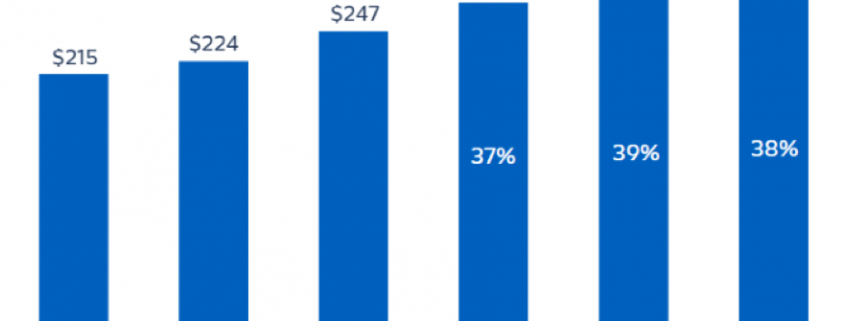

The report on January 6th showed a strong quarter as evidenced by a combination of high revenue growth of 85%, with increased profitability and free cash flow of $54.7 million.

They continue to have success with customers of all sizes and one metric that has continued to stick out is customers with more than $100,000 of trailing 12 months revenue – that metric grew 97% from Q3 last year.

Any tech company would give a left thigh for 85% growth in this climate which is why many have resorted to inorganic growth.

Buying growth is not necessarily a bad strategy now but buying growth at this point in the economic cycle naturally means that companies will need to overpay for growth because of expensive valuations.

Zoom is perfectly positioned to outperform in the next 1-3 years.

The advancing runway is wide open with no competition in sight and a generous growth trajectory is firmly on their side.

At some point, this software company could become a takeover target for a larger corporate.

I am impressed with Zoom's superior products, growth prospects, and scalable business model, and the stock’s near-term risk/reward trade-off is mildly bullish after the jump from $62.

There is an actionable and manageable clear path to a $2 billion revenue run rate with strong margin expansion potential and with its flagship product growing around 80-90%, its next growth driver in Zoom Phone could translate well into a meaningful revenue stream.

Zoom Phone is the next springboard to further success for this company, meaning there won’t be any cliff edge with future revenue streams.

Anyone that has used Zoom as a product can confirm the veracity of its superior performance standards.

This isn’t the type of stock to trade short-term - the volatility undermines any potential entry points.

If the broader market holds up in 2020, Zoom’s value extraction potential is substantially robust, and shares should reach $90.

Growth stocks can only be pinned down for so long before the beast is unleashed.

Buy this stock on any short-term dip.

Mad Hedge Technology Letter

December 11, 2019

Fiat Lux

Featured Trade:

(CHERRY-PICKING IN TECH TODAY)

(ZM), (CRM), (GOOGL), (AAPL)

The valedictorian of the IPO class Zoom Video Communications, Inc. (ZM) is finally on sale at a discount.

If readers want to indulge themselves in a high caliber tech growth stock to buy and hold stock, this is the one for you.

This one has no regulatory headwinds as well as an added bonus.

Zoom’s share price has dropped 40% since hitting the heights of $102 in July which was coincidentally the high for most post-IPO tech stocks of 2019.

It’s been an elevator straight down to no man’s land since then, but investors would be foolish to paint all hyper-growth companies with the same brush.

Filtering out the wheat from the chaff is critical and Zoom is the stock that still has the gloss on its outside package buttressed by its best in show video conferencing software.

There are no other proper alternatives in this sub-sector of software.

A few days ago, the stock slid 9% even though the company crushed expectations with its latest quarterly result and outlook.

Zoom generated revenue of $166.6 million representing a growth rate year on year of 85%.

The company then offered a forecast of $175 million next quarter when analysts only estimated $165 million.

Remember that this company grew 96% just 2 quarters ago and it would be illogical to believe that the stock is being penalized from faltering to 85% today.

Any tech company would give a left leg for 85% growth.

Zoom was trading at 33.5 times my calendar 2020 estimates compared to the fast growth software as a service (SaaS) median at 12.9 times.

Then software stocks started indiscriminately selling off on earnings over the past few weeks irrelevant to the quality of news because of worries to the broader bull market in tech stocks.

It’s true that tech stocks aren’t cheap now, and the skittishness rears its ugly head when bullet-proof earnings’ results are met with a cascade of selling.

Salesforce (CRM) was a software company that was penalized for pricey M&A because the company has been unable to organically grow forcing them to buy growth.

Buying growth is not necessarily a bad strategy but buying growth at this point in the economic cycle naturally means that companies will need to overpay for growth because of expensive valuations.

Zoom is perfectly positioned to outperform in the next 2-3 years.

The advancing runway is wide open with no competition in sight and a generous growth trajectory is firmly on their side.

We Company singlehandedly destroyed positive biased market momentum for any tech growth stock this summer, but on the bright side, quality post-IPO growth stocks are more reasonably priced with compelling entry points.

At around $60, Zoom looks appetizing and is a convincing buy and hold. At some point, this software company could become a takeover target for a larger corporate because companies such as Google (GOOGL) and Apple (AAPL) will need to acquire growth moving forward.

I am impressed with Zoom's superior products, growth prospects, and scalable business model, and the stock’s near-term risk/reward trade-off is attractive after the 9% haircut this past week.

There is an actionable and manageable clear path to a $2 billion revenue run rate with strong margin expansion potential and with its flagship product growing around 80-90%, its next growth driver in Zoom Phone could translate well into a meaningful revenue stream.

Zoom Phone is the next springboard to further success for this company.

Anyone that has used Zoom as a product can confirm the veracity of its superior performance standards.

This isn’t the type of stock to trade short-term, the volatility undermines any potential entry points.

If the broader market holds up in 2020, and Zoom isn’t a $100 stock by yearend, then the stars should align by 2021 because the value extraction potential is substantially robust in Zoom’s business model.

We finally have a reasonable level to scale into Zoom, and if it drops into the $50 range, it’s not just a scale-in type of scenario, investors should buy as much as they can with two hands.

Growth stocks can only be pinned down for so long and the best and brightest have been unfairly penalized with the rest. And let me remind you, this patch of softness in shares is only ephemeral and now is the time to act.

Mad Hedge Technology Letter

November 1, 2019

Fiat Lux

Featured Trade:

(ZOOM ZOOMS IN THE IPO MARKET),

(ZM)

The 2019 IPO class delivered some charlatans but Zoom Video Communications (ZM) is by far and away the valedictorian of this cohort.

It’s not even close.

Sadly, the rest of the IPO class of 2019 is littered with failures and overhyped companies dumped onto the retail investors by the venture capitalists.

Let’s explore why Zoom Video Communications is a best of breed firm in their sub-sector.

Zoom Video is a video conferencing service headquartered in San Jose, California and founded by Eric Yuan.

Eric was previously vice president of engineering at Cisco for collaboration software development and realized there was no high-end video conferencing software at the time.

He took his show on the road and was able to nab 1 million users within the first 2 years after starting Zoom.

This is a real tech company with legitimate proprietary technology and unique source code.

The revaluation from growth to value has hit the entire class of software growth stocks who over-rely on growth as a mechanism to boost shares.

Some have been unfairly punished like Zoom in the downgrade even though the company delivered a strong second-quarter earnings report.

Revenue exploded 96% to $145.8 million, which destroyed expectations of $130.3 million, and management boasted that the number of customers spending more than $100,000 annually on the cloud-based platform more than doubled, a signal that customers are juicing up their use of the service.

Most of the carnage from the rerouting out of growth stocks were specifically in loss-making, high cash burn stocks with the absence of sensible unit economics.

Well, Zoom easily passes this acid test as they have been profitable since the day they went public and even before then.

Even though Zoom has yet to tap the profitability Gods, the $5 million of profits last quarter is just the beginning and as they scale up, the bottom line will beef up.

Therefore, Zoom will not be reliant on outside capital to survive.

In another harbinger of a higher future stock price, adjusted earnings per share rose from $0.02 to $0.08, which also easily beat estimates of $0.01.

Zoom audaciously hiked their outlook for the year at a time when many companies of its ilk are guiding lower to insulate themselves from the global uncertainty permeating throughout the global corporate landscape.

The consolidation in this best of breed software stock will only be temporary aided by the fact that We Company has bottomed out and found a value after its horrendously botched IPO.

I am impressed with Zoom's superior products, growth prospects, and scalable business model, and the stock’s near-term risk/reward trade-off is attractive after the recent sell-off.

There is an obvious and manageable clear path to a $2 billion revenue run rate with strong margin expansion potential and with its flagship product growing around 100%, its next growth driver in Zoom Phone could translate well into a meaningful revenue stream.

Companies are increasingly allowing remote workers to traverse into a mobile lifestyle and Zoom Phone slots seamlessly into this equation.

Anyone that has used Zoom as a product can verify its superior performance standards which is head and shoulders above any competition.

If shares float down to the low 60s, it would be a great buy and hold stock, since actively trading new IPOs are often too volatile to lock in proper entry points.

Mad Hedge Technology Letter

April 23, 2019

Fiat Lux

Featured Trade:

(WHY YOU SHOULD KNOW ABOUT ATLASSIAN CORPORATION)

(TEAM), (ZM),

Next on deck is Atlassian Corporation (TEAM).

What do they do?

They design, develop, license, and maintain global software products.

Part of the functions they provide are project tracking, content creation and sharing, and service management products.

The company's products include JIRA, a workflow management system that enables teams to plan, organize, track, and manage work and projects.

To complement JIRA, Confluence is a piece of software that acts as a content collaboration platform that is used to create, share, organize, and discuss projects.

Also, under its umbrella of software products is Trello, a web-based project management application for capturing and adding structure to fluid, fast-forming work for teams.

Cloud software has become ubiquitous because it is simpler to set up and operate, and benefits from the latest iterations through scheduled updates, and scales easily.

Most crucially, it allows customers to focus scarce time and resources on core businesses, instead of frittering it away solving infrastructure and hardware problems that often mutate into whack-a-mole by nature.

These collection of software products are uplifting Atlassian into a border line company that I would classify as a conviction buy.

Shares have demonstrated the success of the company by bursting with life, shares have doubled in the last 365 days and if you look at its performance all the way back to October 2015, shares have skyrocketed from 20 cents on the dollar to over $100 at the time of this writing.

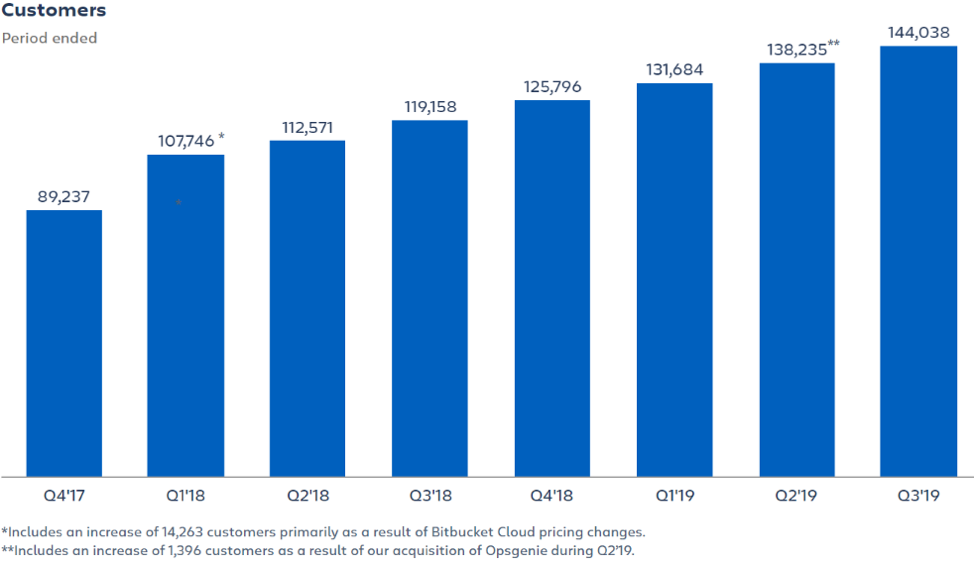

I took a quick glance at the paying customer metrics to gain an insight into why Atlassian is turning into a dominant company.

In Q3 2018, Atlassian racked up paid customers totaling 119,158 and followed that up a year later by totaling 144,038 in Q3 2019.

Atlassian’s clients represent diverse industries and geographies, from start-ups to blue chip companies, the highly automated sales model has given them a chance to target the Fortune 500 for growing margins.

Even on a sequential basis, sales are looking bright with Atlassian adding 5,803 from Q2 2019, combined with the revealing fact that over 90% of new customers in Q3 2019 chose one or more of Atlassian’s Cloud products.

Let me roll through some of the highlight deals with the ink still drying on the paper as we speak.

Flagship customers added to the all-star line-up include European online consumer lending company Sun Finance Group, shipping and logistics services supplier Cosco Shipping, retailer Dollar General, automobile manufacturer Isuzu, financial services firm Wedbush Securities, and New Zealand-based technology solutions provider Spark Digital just to name a few.

These companies don’t use Atlassian products in the same way, while it would be difficult to list the thousands of use cases for Atlassian products, examples illustrate the breadth of application and versatility of Atlassian products and demonstrate how the cloud software can expand across teams, departments, customer organizations, and hemispheres.

To offer one example that encapsulates what Atlassian services can actually achieve for burgeoning companies insistent on digitizing is vehicle history provider CARFAX.

When the Delivery Team at CARFAX doubled in just four years, the weaknesses in its work management system reached an inflection point.

As the team grew, so did the demand for a more robust, integrated system and they had been using several types of tools, none of which were in-tune with each other or aligned well with CARFAX’s entrenched processes.

Product managers lacked transparency into portfolio-wide metrics making it impossible for top executives to make guided decisions on major transformative initiatives.

After collaborating with Atlassian solution partner cPrime and standardizing workflow challenges on JIRA and Confluence, CARFAX discovered the optimal way to streamline their toolkit, connect its departments and systems, and reach its goals.

CARFAX teams now operate through JIRA daily, managing backlogs and keeping afloat with projects enterprise-wide.

Confluence has mushroomed into the go-to collaboration tool, and now has almost the same number of users as JIRA at CARFAX.

The broad absorption of Atlassian tools is unlike anything CARFAX has ever experienced before.

CARFAX has been the recipient of double-digit revenue growth and close to 90% customer satisfaction while hoisting the pillars to scale in the future.

Atlassian and its makeover for CARFAX is a crucial reason for the additional engineering efficiency to more regular updates and scalability without interruption for IT, to consistent and real-time analytics for the C-suite.

The software enhancements are a valuable source of enhanced productivity, and CARFAX continues to eagerly grab new product updates from Atlassian to embed into a myriad of automated processes.

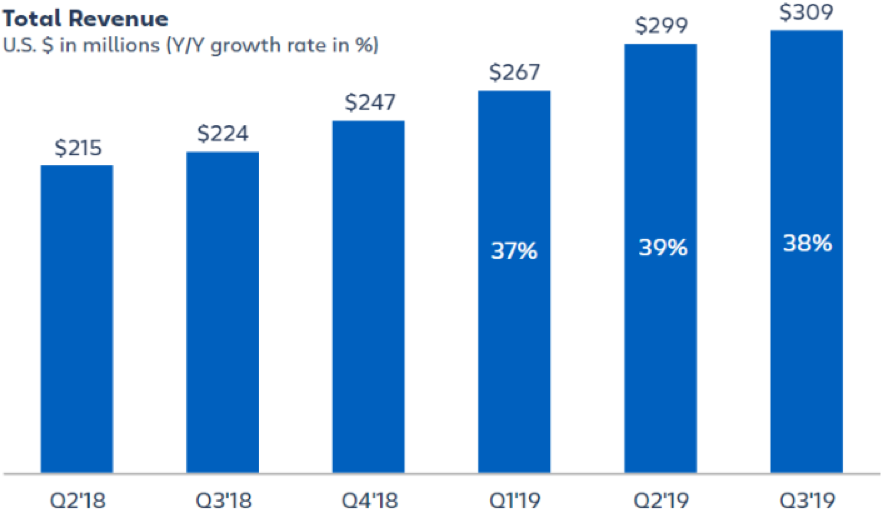

When many industries are on the brink of an earnings recession, Atlassian has bucked the trend with Q3 2018 revenues expanding 38% YOY to $309.3 million.

The company is even executing more efficiently by revealing healthier gross margins that increased from 79.8% in Q3 2018 to 82.5% in Q3 2019.

Even though Atlassian guided revenue to around $330 million for next quarter’s earnings, they guided down to 16 cents per share, lower than the 19 cents per share that analysts were estimating.

The expected earnings recession has offered an opportunistic chance for management to guide down, giving shares some breathing room before they march higher again which I believe is inevitable.

Atlassian is a robust enterprise software company in the early stages of hyper-growth with a long runway.

Not every company can enter into monopolies or duopolies in the tech world like Google, but the next best thing is the enterprise software market where analog companies need help juicing up products by automating the back, middle, and front end.

Companies such as Atlassian are at the forefront of this dynamic revolution and recent tech IPOs, such as video conferencing software for business users Zoom (ZM), epitomize where the pockets of growth have nestled in the current American economy.

This year is truly the year of enterprise software so enjoy the ride with Atlassian.