Below please find subscribers’ Q&A for the January 6 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV.

Q: Any thoughts on lithium now that Tesla (TSLA) is doing so well?

A: Lithium stocks like Sociedad Qimica Y Minera (SQM) have been hot because of their Tesla connection. The added value in lithium mining is minimal. It basically depends on the amount of toxic waste you’re allowed to dump to maintain profit margins—nowhere close to added value compared to Tesla. However, in a bubble, you can't underestimate the possibility that money will pour into any sector massively at any time, and the entire electric car sector has just exploded. Many of these ETFs or SPACs have gone up 10 times, so who knows how far that will go. Long term I expect Tesla to wildly outperform any lithium play you can find for me. I’m working on a new research piece that raises my long-term target from $2,500 to $10,000, or 12.5X from here, Tesla becomes a Dow stock, and Elon Musk becomes the richest man in the world.

Q: Won’t rising interest rates hurt gold (GLD)? Or are inflation and a weak dollar more important?

A: You nailed it. As long as the rate rise is slow and doesn't get above 1.25% or 1.50% on the ten-year, gold will continue to rally for fears of inflation. Also, if you get Bitcoin topping out at any time, you will have huge amounts of money pour out of Bitcoin into the precious metals. We saw that happen for a day on Monday. So that is your play on precious metals. Silver (SLV) will do even better.

Q: What are your thoughts on TIPS (Treasury Inflation Protected Securities) as a hedge?

A: TIPS has been a huge disappointment over the years because the rate of rise in inflation has been so slow that the TIPS really didn’t give you much of a profit opportunity. The time to own TIPS is when you think that a very large increase in inflation is imminent. That is when TIPS really takes off like a rocket, which is probably a couple of years off.

Q: Will Freeport McMoRan (FCX) continue to do well in this environment?

A: Absolutely, yes. We are in a secular decade-long commodity bull market. Any dip you get in Freeport you should buy. The last peak in the previous cycle ten years ago was $50, so there's another potential double in (FCX). I know people have been playing the LEAPS in the calendars since it was $4 a share in March and they have made absolute fortunes in the last 9 months.

Q: Is it a good time to take out a bear put debit spread in Tesla?

A: Actually, if you go way out of the money, something like a $1,000-$900 vertical bear put spread, with the 76% implied volatility in the options market one week out, you probably will make some pretty decent money. I bet you could get $1,500 from that. However, everyone who has gone to short Tesla has had their head handed to them. So, it's a high risk, high return trade. Good thought, and I will actually run the numbers on that. However, the last time I went short on Tesla, I got slaughtered.

Q: Any thoughts on why biotech (IBB) has been so volatile lately?

A: Fears about what the Biden government will do to regulate the healthcare and biotech industry is a negative; however, we’re entering a golden age for biotech invention and innovation which is extremely positive. I bet the positives outweigh the negatives in the long term.

Q: Oil is now over $50; is it a good time to buy Exxon Mobil (XOM)?

A: Absolutely not. It was a good time to buy when it was at $30 dollars and oil was at negative $37 in the futures market. Now is when you want to start thinking about shorting (XOM) because I think any rally in energy is short term in nature. If you’re a fast trader then you probably can make money going long and then short. But most of you aren't fast traders, you’re long-term investors, and I would avoid it. By the way, it’s actually now illegal for a large part of institutional America to touch energy stocks because of the ESG investing trend, and also because it’s the next American leather. It’s the next former Dow stock that’s about to completely disappear. I believe in the all-electric grid by 2030 and oil doesn't fit anywhere in that, unless they get into the windmill business or something.

Q: With Amazon buying 11 planes, should we be going short United Parcel Service (UPS) and FedEx (FDX)?

A: Absolutely not. The market is growing so fast as a result of an unprecedented economic recovery, it will grow enough to accommodate everyone. And we have already had huge performance in (UPS); we actually caught some of this in one of our trade alerts. So again, this is also a stay-at-home stock. These stocks benefited hugely when the entire US economy essentially went home to go to work.

Q: Should we keep our stay-at-home stocks like DocuSign (DOCU), Zoom (ZM), and UPS (UPS)?

A: They are way overdue for profit-taking and we will probably see some of that; but long term, staying at home is a permanent fixture of the US economy now. Up to 30% of the people who were sent to work at home are never coming back. They like it, and companies are cutting their salaries and increasing their profits. So, stay at home is overdone for the short term, but I think they’ll keep going long term. You do have Zoom up 10 times in a year from when we recommended it, it’s up 20 times from its bottom, DocuSign is up like 600%. So way overdone, in bubble-type territory for all of these things.

Q: Are telecom stocks like Verizon (VZ) and AT&T (T) safe here?

A: Actually they are; they will benefit from any increase in infrastructure spending. They do have the 5G trend as a massive tailwind, increasing the demand for their services. They’re moving into streaming, among other things, and they had very high dividends. AT&T has a monster 7% dividend, so if that's what you’re looking for, we’re kind of at the bottom of the range on (T), so I would get involved there.

Q: Should we sell all our defense stocks with the Biden administration capping the defense budget?

A: I probably would hold them for the long term—Biden won’t be president forever—but short term the action is just going to be elsewhere, and the stocks are already reflecting that. So, Raytheon (RTX), United Technologies (UT), and Northrop Grumman (NOC), all of those, you don’t really want to play here. Yes, they do have long term government contracts providing a guaranteed income stream, but the market is looking for more immediate profits, or profit growth like you have been getting in a lot of the domestic stocks. So, I expect a long sideways move in the defense sector for years. Time to become a pacifist.

Q: Is it safe to buy hotels like Marriott (MAR), Hyatt (H), and Hilton (HLT)?

A: Yes, unlike the airlines and cruise lines, which have massive amounts of debt, the hotels from a balance sheet point of view actually have come through this pretty well. I expect a decent recovery in the shares, probably a double. Remember you’re not going to see any return of business travel until at least 2022 or 2023, and that was the bread and butter for these big premium hotel chains. They will recover, but that will take a bit longer.

Q: How about online booking companies like Expedia (EXPE) and Booking Holdings Inc, owner of booking.com, Open Table, and Priceline (BKNG)?

A: Absolutely; these are all recovery stocks and being online companies, their overhead is minimal and easily adjustable. They essentially had to shut down when global travel stopped, but they don’t have massive debts like airlines and cruise lines. I actually have a research piece in the works telling you to buy the peripheral travel stocks like Expedia (EXPE), Booking Holdings (BKNG), Live Nation (LYV), Madison Square Garden (MSGE) and, indirectly, casinos (WYNN), (MGM) and Uber (UBER).

Q: What about Regeneron (REGN) long term?

A: They really need to invent a new drug to cure a new disease, or we have to cure COVID so all the non-COVID biotech stocks can get some attention. The problem for Regeneron is that when you cure a disease, you wipe out the market for that drug. That happened to Gilead Sciences (GILD) with hepatitis and it’s happening with Regeneron now with Remdesivir as the pandemic peaks out and goes away.

Q: What about Chinese stocks (FXI)?

A: Absolutely yes; I think China will outperform the US this year, especially now that the new Biden administration will no longer incite trade wars with China. And that is of course the biggest element of the emerging markets ETF (EEM).

Q: Will manufacturing jobs ever come back to the US?

A: Yes, when American workers are happy to work for $3/hour and dump unions, which is what they’re working for in China today. Better that America focuses on high added value creation like designing operating systems—new iPhones, computers, electric cars, and services like DocuSign, Zoom—new everything, and leave all the $3/hour work to the Chinese.

Q: What about long-term LEAPS?

A: The only thing I would do long term LEAPS in today would be gold (GOLD) and silver miners (WPM). They are just coming out of a 5-month correction and are looking to go to all-time highs.

Q: What about your long-term portfolio?

A: I should be doing my long-term portfolio update in 2 weeks, which is much deserved since we have had massive changes in the US economy and market since the last one 6 months ago.

Q: Do you have any suggestions for futures?

A: I suggest you go to your online broker and they will happily tell you how to do futures for free. We don’t do futures recommendations because only about 25% of our followers are in the futures market. What they do is take my trade alerts and use them for market timing in the futures market and these are the people who get 1,000% a year returns. Every year, we get several people who deliver those types of results.

Q: Will people go back to work in the office?

A: People mostly won’t go back to the office. The ones who do go back probably won't until the end of the summer, like August/September, when more than half the US population has the Covid-19 vaccination. By the way, getting a vaccine shot will become mandatory for working in an office, as it will in order to do anything going forward, including getting on any international flights.

Q: What is the best way to short the US dollar?

A: Buy the (FXE), the (FXY), the (FXA), or the (UUP) basket.

Q: Silver LEAP set up?

A: I would do something like a $32-$35 vertical bull call spread on options expiring in 2023, or as long as possible, and that increases the chance you’ll get a profit. You should be able to get a 500% profit on that LEAP if silver keeps going up.

Q: What about agricultural commodities?

A: Ah yes, I remember orange juice futures well, from Trading Places, where I also once made a killing myself. Something about frozen iguanas falling out of trees was the tip-off. We don’t cover the ags anymore, which I did for many years. They are basically going down 90% of the time because of the increasing profitability and efficiency of US farmers. Except for the rare weather disaster or an out of the blue crop disease, the ags are a loser’s game.

Q: Can we view these slides?

A: Yes, we load these up on the website within two hours. If you need help finding it just send an email or text to our ever loyal and faithful Filomena at support@madhedgefundtrader.com and she will direct you.

Q: Do you have concerns about Democrats regulating bitcoin?

A: Yes, I would say that is definitely a risk for Bitcoin. It is still a wild west right now and there are massive amounts of theft going on. It is a controlled market, with bitcoin miners able to increase the total number of points at any time on a whim.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/02/john-thomas-old-plane.png358466Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-08 10:02:392021-01-08 10:51:48January 6 Biweekly Strategy Webinar Q&A

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

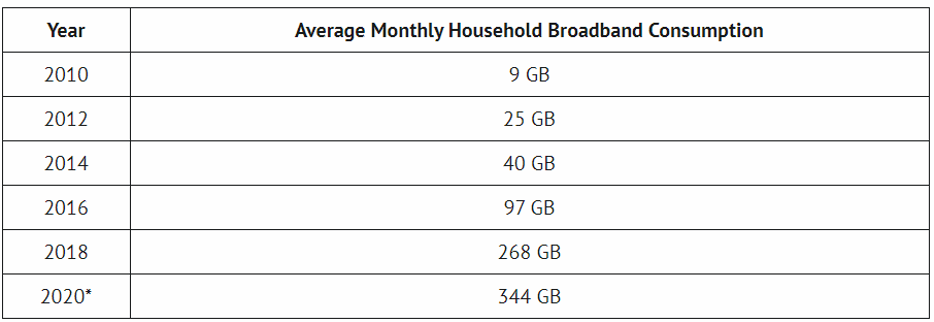

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-18 11:02:262020-12-19 00:05:37Tech in 2021

Below please find subscribers’ Q&A for the October 28 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you think if Trump contests the election, it will be bad for stocks?

A: Yes, count on that knocking another 10% off of stocks. The market has spent the last six months pricing in a Biden win. Take that away and you have to price that back out again, about 6,000 Dow Average points (INDU). We’ve already dropped 2,500 points so that leaves another 3,500 points of downside t0 go in the event of a Trump win.

Q: Will that result in a crash?

A: Yes. At least 1,000 points in the overnight session following.

Q: Do you think it’s going to happen?

A: No. According to the polls, Trump will lose by at least 15 million votes. While the polls missed the Electoral College result last time, they were dead on with the popular vote, with Hillary Clinton winning by 3 million votes. If the margin were only a few hundred or thousand votes in a single battleground state, Trump might win a court fight. But he can’t win if the margin is in ten states and tens of millions of votes. That is too much to fudge. That is how markets react: they hate surprises, and a second Trump win would be the surprise of the century.

Q: With all of the earnings positive, do you think markets will stay positive?

A: Earnings aren’t important right now. Everyone knew earnings would be great because we were coming off of hundred-year lows caused by the pandemic. So yes, we knew they’d be up 50%, 100%, 150%; that's not the surprise. The bigger issue is what the pandemic is going to do, and of course, only biochemists know that—most stock traders have no idea, which is reflected in these gigantic swings we’re seeing in the market both on the upside and the downside. As a biochemist, I can tell you that this is our final wave that's coming up and it could last several months. After that, we get a vaccine or herd immunity. When it's done, you have the bull market of a lifetime—up 400% in ten years from these levels. Dow 120,000 here we come!

Q: Do you see a tax selloff if Biden gets in? Should we get short?

A: Definitely; there will be a tax selloff. Past ones have only lasted a week or two and those were the last two weeks of December, so it really won’t be that bad. It’s not like it’s a surprise that Biden is ahead in the polls, because he has been for 6 months. Nor is it a surprise that he is going to raise taxes on the wealthy. I wouldn’t get short though. The short play was last week and the week before; and I did manage to get out three shorts but didn't want to get too big in front of an election. So those all worked. I'm out of all of them now, and now we’re looking only at long plays. And with the Volatility Index (VIX) over $40, you can go 20% or 30% in-the-money on these call spreads and still look to make 10%-20% profit on the position in a month.

Q: Isn’t the pandemic great for Amazon (AMZN)?

A: Yes, Amazon was taking over the world anyway, and forcing everyone to an online-only economy which couldn’t be better for them. A lot of this shifting is permanent and won’t be going back to the way it was before the pandemic with brick and mortar shops and malls. So yes, we love Amazon and I would buy on the dips. There’s a double from here.

Q: Do you have long term names I can buy to sit on?

A: Yes, we actually do have a long-term portfolio posted on the website. It would be listed under your subscription area once you log in—we rebalance that twice a year. And of course, we had a 10% holding in Tesla (TSLA) which went up ten times, so the performance of the long-term portfolio is through the roof. To find the long-term portfolio, please click here.

Q: Do you still like the Internet security stocks like FireEye (FEYE)?

A: Yes. Hacking is growing faster than the Internet itself. You should also look at Palo Alto Networks (PANW) and the ETF (HACK).

Q: Should we hold on to the Visa (V) spread hoping it will come back after the election drop?

A: Hope is not an investment strategy. I always stop out of positions when they hit a 2% loss. The only time I have 4% losses is when we get these gigantic gap moves overnight, which tend to happen once every one or two years. In this case, Visa got hit with a surprise antitrust suit from the Department of Justice that knocked $10 off of the stock. So no, I will not hold on to it in the hope that it does better; I will try to minimize my losses, get out, and get into the next winning position. Hope is what turns a 4% loss into a complete 10% write off.

Q: What’s your view on the Canadian dollar (FXC)?

A: I like it, but it’s not as good as the Australian dollar (FXA) because Canada has a major oil exposure, and actually the worst kind of oil exposure—tar sands in northern Alberta. The outlook for oil is poor and that will be a drag on the currency in the form of fewer exports. Buy the (FXA). No oil troubles here. Kangaroos are another story.

Q: Will you be looking to sell short on the United States Treasury Bond Fund (TLT)?

A: Yes, if we can just get a little bit higher. We’re looking at an economic recovery next year, so we’d expect the (TLT) to be lower by at least $20 points in 2021.

Q: Do you think the San Francisco and New York housing markets will return to what they were before with so many people are moving out of the city?

A: Yes, they will come back, I’ve been through many of these cycles in San Francisco over the past 50 years; it always comes back. Once the pandemic is over, people will say, “Oh my gosh, I can’t believe you can get a two-bedroom apartment in San Francisco for only $2 million.” That's probably another year or two off after a vaccine is in widespread distribution.

Q: Is real estate in a bubble?

A: Absolutely, but real estate bubbles can go on for a long time, like ten years. The bubble in Australia has been going on for 30 years. Ultimately, real estate prices are driven by the earnings power of the local economy which, in the case of San Francisco, is huge. This time around, we have a record large millennial generation looking for real estate. There are 85 million millennia buyers with only 65 million Gen X-er’s selling homes. So, we have to make up a shortfall of 20 million houses at some point. That’s why building permits are through the roof every month.

Q: Zoom (ZM) and DocuSign (DOCU) are the darling stocks of COVID 2020—what do you think about them at these high prices?

A: Very high risk. If you bought these a year ago when we first started covering them, good for you as they're up ten times. However, there are better fish to fry than chasing these big pandemic winners at all-time highs.

Q: If Biden wins, what happens to defense stocks like Raytheon Technology (RTX)?

A: They go down. It turns out a lot of the defense business is in very long term contracts that can’t be broken. They have to supply so many planes a year to the government for a decade or more. However, the sentiment on these sectors sours under democratic administrations because they are not initiating new weapons systems where the big money is made. Lockheed Martin (LMT), Northrop Grumman (NOC), and General Dynamics (GD) all have the same problem. I grew up with these companies. They were the FANGs of their day.

Q: How does a Biden win affect Tesla (TSLA)?

A: Then $2,500 a share for Tesla looks cheap (it’s now at $410). Biden will do everything he can to slow climate change and accelerate alternative energy. Tesla is front and center on that. Under current law, car manufacturers are limited on the number of units they can sell to get the $7,500 tax break per vehicle. Tesla used up all their subsidies five years ago. My bet is that the limits will be eliminated and that leads to a huge surge in Tesla sales in the U.S., which is why the stock has gone up 10 times in the last year. Tesla has promised to drop their car price to $25,000 in three years. If you throw in $10,000 in federal and state tax subsidies you get the car for free. Then you can write off General Motors (GM) and Ford (F).

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Bear Sighting

https://www.madhedgefundtrader.com/wp-content/uploads/2020/10/bearsighting.jpg622665Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-10-30 11:02:122020-10-30 12:18:46October 28 Biweekly Strategy Webinar Q&A

The good news is that investors are thirsting for new cloud IPOs boding well for tech firms like Airbnb who plans to go public later this year.

The long-term health of the U.S. tech sector is on solid footing.

Most recently we had Snowflake (SNOW) who is a cloud provider and has an impressive enterprise business.

The public cloud is the data storage unit which literally everyone stores their operations on that has benefited from a massive wave of digital migration.

Many of the cloud-targeted tech firms of recent years have been 10-baggers and have dominated the overall market's returns.

Typically, these companies trade at high premiums, and rightly so, because of the corresponding growth trajectories and Snowflake is no different.

The stock has doubled after less than half a month as a tradable market-moving instrument.

Even by the standards of the most expensive software companies on the Nasdaq index, Snowflake is not cheap, although it’s a growth monster.

Snowflake was valued at $12.4 billion in February and even has investor Warren Buffett, the Oracle of Omaha, among its investors.

Buffett dove headfirst into tech investments in Apple and even some Indian fintech firms as well.

Snowflake is the largest software IPO on record and the largest since Uber's $8.1 billion IPO in May 2019.

The firm was striving for a valuation of $20 billion. In total, Snowflake has raised $1.4 billion from investors including Sequoia and Iconiq Capital.

Snowflake even makes the high-flying Zoom (ZM) Video Communications look cheap which is hard to do.

Zoom is growing three times faster than Snowflake, but trades at roughly half of Snowflake's price-to-sales ratio.

Zoom is also profitable, whereas Snowflake is a huge loss maker and that is a staple of many tech startups. This is an economic environment that is more conducive to profit drive companies instead of the tech model of promising future growth.

Snowflake is over four times more expensive than cloud company Datadog.

Snowflake's market is thought to be bigger than most other niche software applications, and therefore it may have a longer runway. In the regulatory filing, Snowflake claimed its total addressable market was around $81 billion.

Along with many other growth companies, Snowflake's ultimate margin potential is still hard to fathom and more passengers are starting to arrive in the sector than drivers.

Even worse, Snowflake not only competes with legacy data warehouse companies such as Oracle (ORCL) and Dell but also with products from the cloud infrastructure company it collaborates with.

Since shares have already doubled, I do believe that investors will need to wait for a pullback to put money to work in Snowflake.

The company said it had about 3,100 customers, including 56 clients that contributed about $1 million in a 12-month period.

Even with the pricey valuations, Snowflake is the pre-eminent cloud listing of the second half of 2020 and its enterprise business is sustainable.

If a broader sell-off drags this name down into the $180s, pull the trigger and start wading into this one.

The stock is currently priced as such that it represents flawless execution quarter after quarter for many years, and they would have to live up to lofty expectations to grow into its valuation.

While the management is stellar and is known for its execution, the odds of Snowflake's stock faltering are high because of the high bar.

Keep this one on your hot list because with all the variables waiting to pull down the market, there will be a time when the price is right in Snowflake.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-23 10:02:592020-09-23 19:02:59The Hot Cloud IPOP of Fall 2020

All signs point to green – that is the big investing takeaway from Zoom’s (ZM) outstanding earnings report.

It also means you cannot be bearish technology stocks.

Investors can lose their shorts trying to short the monopolies of Amazon, Google, and now the mega growth video communications company Zoom.

I still maintain a nuanced strategy of neutrality with a tactically bullish stance because of the rapid run-up from the March 23 lows.

Zoom has been one of the stalwarts of the work-at-home revolution and the numbers back it up.

Quarterly revenue guidance was up a juicy 64%.

The stunning 169% quarterly revenue increase year-over-year are numbers that dreams are made of.

I would like any reader to dig through the collection of companies trading on the New York Stock Exchange and find me one that beat its quarterly revenue target by over 300% during the pandemic.

That is why you invest in tech and that is why you read my technology letter.

What does this really mean?

There is still money to be made in technology.

This isn’t just a fly-by-night, smash-and-grab ploy to only burn down tomorrow like a Potemkin village.

The staying power is real and the stay-at-home movement will be stickier than ever moving forward as companies cut costs, digitize to the extremes, and hope to stave off the next mega-crisis when it threatens to take the food off our tables again.

Even Zoom itself couldn’t wrap their heads around the dramatic transition from enterprise use to consumers' necessity to keep in touch with family and friends.

The company became the “can’t live without” app of the year and grew from 10 million users to over 300 million users this quarter.

If any analyst had them rated as neutral before, this was the signal to issue a buy recommendation.

It is without exaggeration to say these are the most impressive financial results I’ve ever seen in software, and likely will never be repeated in our lifetimes.

Fresh opportunities also come in the form of education and telemedicine as reasons for a bullish outlook moving forward.

Zoom will need to fend off competitive concerns from Microsoft and Google, but Zoom’s scalable technology and ease of use have created a strong moat around its business model.

The company has an installed base of 265,000 customers with 10 or more employees with ample chances to cross-sell its Zoom Phone and Zoom Rooms services.

There is a basket of stay-at-home stocks that have outperformed the market since the Covid-19 pandemic began, and I am highly convinced that Zoom is the purest way to play this theme.

Even as lockdowns ease, many workers will demand the new normal of working remotely.

A taste of a good life isn’t enough, and the coronavirus proved that companies could function just as well without the traditional cubicle and office space.

The biggest problem with Zoom’s shares is finding a reasonable investing entry point into the best tech story of 2020.

There is just not enough superlatives to say about Zoom and investors would need to wait for the stock to dip near resistant levels at the 50-day moving average around $160 to put new money to work in Zoom shares.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-08 11:02:002020-06-10 01:07:15Zoom's Lesson for Tech Stocks

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.