Mad Hedge Technology Letter

May 16, 2022

Fiat Lux

Featured Trade:

(INSANITY AT CALPERS)

(GME), (AMC), (NFLX)

Mad Hedge Technology Letter

May 16, 2022

Fiat Lux

Featured Trade:

(INSANITY AT CALPERS)

(GME), (AMC), (NFLX)

Pension funds are famous for being slow rollers, usually taking the safest of safest routes to preserve capital and slowly grow asset portfolios.

The people they serve, the pensioner, should be a microcosm of what the fund is about.

This would make sense since the capital in the first place comes from employees and is meant to fund these workers after retirement.

Many people don’t know that modern pension funds serve a dual mandate of, not only doling out monthly stipends to old people, but playing the role of trader on the active markets.

American states and sovereign countries usually have massive pension funds which can move markets.

The board usually hires qualified and credentialed management to oversee funds...or do they?

So one might ask, what on earth is going on with the largest pension fund in America, representing the state of California CALPERS?

CALPERS increased its meme stock and movie theatre company AMC (AMC) stake this first quarter again.

Last year the institution loaded up on AMC and GameStop (GME).

During this time, the California Public Employees’ Retirement System (CALPERS) had sold an 11% stake in Palantir (PLTR).

CALPERS is betting the ranch on meme stocks, and that is scary news.

It obviously means that the bottom is not in since there is more dumb money flooding into the system.

Once we flush out the weak hands then it will signify rock bottom, but as long as we have CALPERS buying up meme stocks then it’s hard not to be bearish.

Even more baffling was the decision to sell an extreme amount of Netflix (NFLX) after colossal losses.

Netflix stock is down almost 69% this year-to-date and it dropped 38% in the first quarter of 2022 alone.

Taking a major loss in Netflix only to roll money into GameStop and AMC is seriously what the California state pension fund is doing.

This is no joke.

At least they don’t own cryptos like Dogecoin or Shiba Inu coin.

I am not sure exactly what their plan is but movie theatre watching is dead.

Perhaps, CALPERS plan to offer their retirees free movie tickets along with a depreciating amount of monthly pension.

Suspicion runs deep into who is making decisions at the helm and that is the CEO of CALPERS Marcie Frost.

She spent 30 years as a public servant in Washington state. Her early leadership roles were in human resources with an emphasis on employee benefit programs and information technology.

In 2013 Marcie was named cabinet lead by Washington State Governor Jay Inslee for the Results Washington performance and accountability system, where she served as an early creator and architect for the platform that tracks goals and progress in education, the state's economy, sustainable energy, healthy and safe communities, and efficient government.

Basically, she has no idea about the stock market yet she is CEO of the biggest pension fund in America.

Her role as tracking the “progress in education” is somehow supposed to transfer over to stock market overperformance.

This screams a breach of fiduciary duty and it could end up in tatters for CALPERS.

CALPERS has been infamous for terrible management decisions and Marcie’s predecessor breached conflict of interest mandates by investing in Los Angeles real estate that he has an interest in.

Clearly, the board of CALPERS favors crony capitalism as a management style.

Any 14-year-old student would know under no circumstance, should a pension fund choose to voluntarily speculate on high-risk assets.

Is it really a thirst for yield?

If CALPERS blows up and is forced to mass unwind, don’t forget this story.

“I want to put a ding in the universe.” – Said Co-Founder of Apple Steve Jobs

Mad Hedge Technology Letter

May 13, 2022

Fiat Lux

Featured Trade:

(SPAC BUSINESS PULLS BACK)

(GS), (SEC), (SPAC), (SPXZ)

Never waste a crisis.

The SEC sure isn’t.

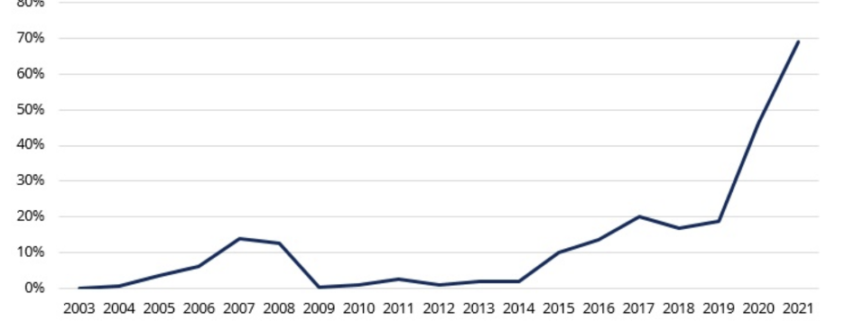

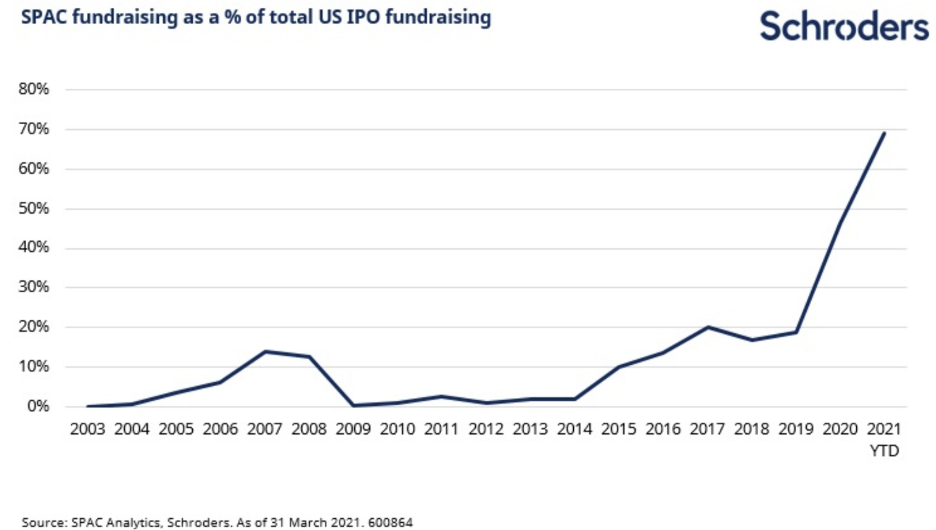

They are using this stock market meltdown to broaden out the risk to who is liable for special purpose acquisition companies (SPACs).

The new regulation has meant that investment bankers who do the deal then advise the companies post-IPO are bailing on this business in droves.

There have been whispers about this potential regulation for quite a while as many investment advisers were putting through low-quality companies that would never turn a profit in a million years.

Investors would be held with the bag as these SPACs were prone to severely underperforming in the stock market.

Powerful Wall Street banks like Goldman Sachs (GS) are pulling out of working with most SPACs it took public, the second-biggest underwriter of special purpose acquisition companies last year, has been telling sponsors of the vehicles it will be ending its involvement.

A SPAC works with its adviser even after going public to finish its merger with a participating firm, known as the de-SPAC transaction.

If it fails to complete that deal, it’s forced to return capital to investors. In cases where the public company is very close to completing the de-SPAC process, Goldman will fulfill its role.

SPACs were popular on Wall Street over the past couple of years, luring financiers, politicians, and celebrities who were able to profit from investors piling into the investment vehicles.

The SEC is tightening oversight of SPACs including exposing underwriters to greater liability risk.

Lawyer advocates have argued the listings were bypassing rules imposed on traditional initial public offerings and exposing retail shareholders to extra risks.

The SEC’s proposal would require SPACs to disclose more information about potential conflicts of interest and make it easier for investors to sue over false projections.

There is no visibility on what company might be acquired (this is a regulatory requirement). A SPAC’s prospectus often includes some wording about the type of company or industry it intends to focus on, but there’s nothing to stop it from going in a totally different direction.

In many cases, those same sponsors were courted by large banks to put their names behind their SPACs, with the structure allowing them to turn an initial investment of a few million dollars into many multiples of that. And their Wall Street underwriters could make more than 5% in fees for taking a SPAC public, helping the sponsor find a takeover target and complete the de-SPAC.

The SEC's concerns might be warranted just based on how awful SPAC stocks are performing.

Take for example, SPAC ETF Morgan Creek - Exos SPAC Originated ETF (SPXZ) whose shares have gone from $21 in the past year to $11 today.

There have been a few SPACs that are worth investing in partially because once the SPAC goes public, the company can turn its business 180 degrees and do something completely different.

They are not beholden to anything, unlike traditional IPOs which are strict in defining what they do and how they do it.

Naturally, a lot of fraud-type companies can go public quickly with the help of a famous celebrity marketing their SPAC and that’s exactly what has happened.

New York doesn’t need more IPOs, but it needs more high-quality IPOs and this will prevent many investors from losing all their money.

One of the big unintended consequences of this bear market is that regulation is finally focusing on the fringe elements in tech and that should mean a healthier tech sector moving forward.

Mad Hedge Technology Letter

May 11, 2022

Fiat Lux

Featured Trade:

TECH DESERVES WHAT IT DESERVES)

(RBLX), (ARKK), (ROKU), (TDOC), (ZM), (TSLA), (GM)

A bear market rally in tech would be an overwhelmingly healthy signal that the financial system is working in an orderly fashion.

Yet, as I say that, a looming recession inches closer.

How do I know that?

That was my first reaction when my eyes were stung by the headline of 8.3% inflation.

Sure, not a 10, but it is emblematic of the ongoing inflation concerns with items such as airplane tickets up 18% year over year in price.

Remember the consensus was that inflation pressures are trending towards peaking, potentially setting up for a nice bear market rally.

That narrative hit another catch-22, not as bad as it could have been, but clearly not great and prices biting at the backs of consumers.

The hope that inflation will be crammed back into the genie bottle is not going to happen until later this year and not for the right reasons.

Simply because comparables become easier to beat year over year.

Like I have mentioned in past tech letters, high-growth tech stocks are most sensitive to the fluctuation in rates and investors should be nowhere near growth funds like Cathy Wood’s ARK Innovation ETF (ARKK).

Another head-scratching move was ARK’s Cathy Wood selling Tesla (TSLA) shares and rolling them into GM (GM).

This is for the lady who likes to tell us that we aren’t “doing the research.”

Betting against Elon Musk is a fool’s game.

When it comes to EVs, I would put money on Musk to defy any odds.

Tesla will outperform GM, especially amid a backdrop of lithium prices spiking and supply chain issues going haywire.

Musk is simply the anointed guy that knows how to work miracles.

He only developed the EV industry as he saw fit, invented reusable space rockets, cut the price of space exploration by 10, and reimagined tunneling construction technology.

And by the way, his Neuralink brain interface company is working on implanting chips in human brains so we don’t need to use our fingers on keyboard anymore.

I wouldn’t want to compete with this man and to believe that GM will be able to nimbly outmaneuver Musk who has the audacity to aggressively solve anything no matter how many people he pisses off is not an incremental bet on “innovation” that Wood likes to tout she is participating in.

Neither is the purchase of Roku (ROKU), Zoom (ZM), or Roblox (RBLX) which have all tanked since she put new money to work in them in late April.

Inflation at 8.3% means that the real rate of inflation is still -7.55% and until that’s addressed, any bear market rally will be viciously sold breaching further levels down below.

The carnage in the tech world is indicative at the dregs of the barrel.

Tech IPOs are toxic.

Market for new issues has been bereft throughout the first four-plus months of this year, and nothing that would move the needle is on the tech IPO radar for the duration of the second quarter.

Companies that were aiming to go out in the first half of 2022 have no appetite to continue down that path because there simply won’t be a bid.

Going public today would require a complete revaluation of their business and leave many late-stage investors and employees with out-of-money stock.

Grocery deliverer Instacart is the only company in that class that’s been forthright with its slowing valuation. In March, the company said it cut its valuation by about 40% to $24 billion.

That’s how bad it is out there at the bush league end of the tech sector and many of these stocks that are public such as Teladoc are down 80%.

I do believe that many of these loss-making growth techs are rightfully down 80%.

They had time to show a profit and they failed in the allotted amount of time they were given.

Every window closes and the market moves forward with or without them.

In the near term, I am bearish on the market but I do believe we are oversold which could feed into a dead cat bounce to sell on.

“My relationship with the government is: Be in love with the governments, but do not marry them.” – Said Founder of Alibaba Jack Ma

Mad Hedge Technology Letter

May 9, 2022

Fiat Lux

Featured Trade:

(BUYER STRIKE HAS LEGS)

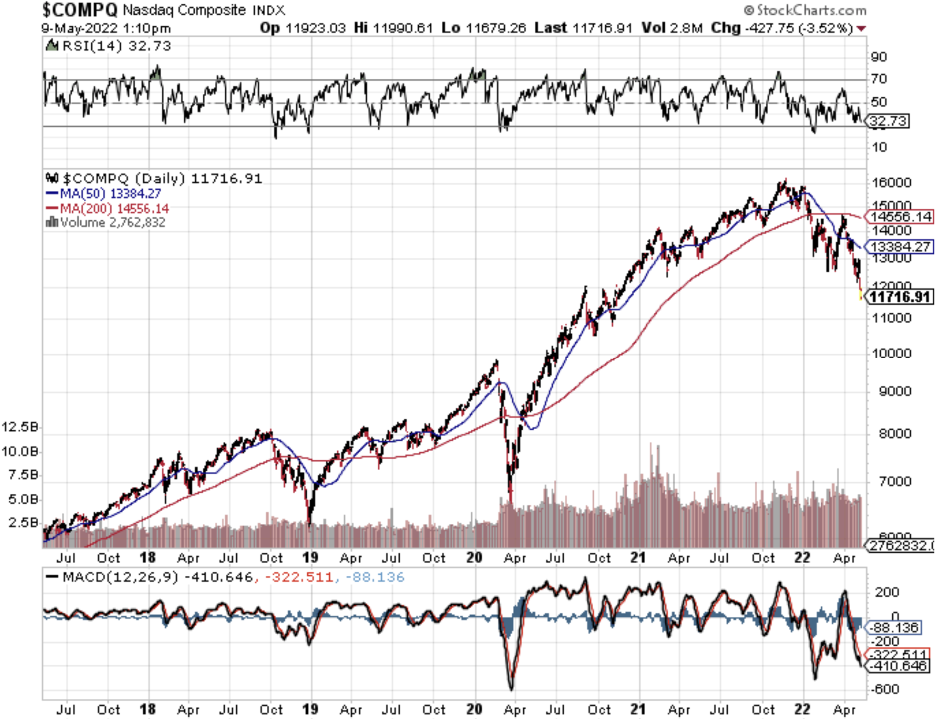

($COMPQ), (AMZN), (FB)

The buyer strike roars ahead as the 10-year U.S. treasure accelerates its rate of decline touching 3.2%.

We are dealing with a major deleveraging of the tech sector as a massive rotation flood into commodity-linked assets, the US dollar, and shorting bonds.

Sadly, we got another kick up the rear side when US Central Bank governor Jerome Powell committed yet another policy mistake by attempting to save the stock market.

Things could get ugly from here.

Many investors believed the Fed would self-correct after the “transitory” inflation nonsense.

It’s not so much the actual 3.2% rate today, but the velocity of the move which is creating many air pockets that are not being filled.

Why?

Investors are betting that Powell will most likely make a third policy mistake which could create another suicidal spiral downwards.

Investors have no incentive to buy stocks when the Fed has not only lost credibility but appears to not understand what is going on with real inflation tearing apart economic health.

This looks a lot like the 1970s just before former US Fed Chair Paul Volcker was brought in to slam the economy and raise interest rates to 18%.

Powell doesn’t seem like he has the guts to do that which is why the prolonging of this failed interest rate policy will mean a longer and more painful economic recession in the future.

I see many pundits going on record saying that the “risk reward has improved.”

Besides stating the obvious, this analysis doesn’t take into consideration that yields could go higher which would cause tech stocks to plummet further.

So yes, the risk reward has improved, but it can improve even more from here.

That doesn’t tell us much about anything.

All signs are now pointing to a souring paradigm shift among tech firms and dramatic changes under the hood.

Facebook (FB) is pausing hiring, a previously unthinkable prospect.

The company blamed macroeconomic challenges and Apple’s privacy changes for its slowest revenue growth in 10 years last quarter.

Almost 12 months after Apple launched App Tracking Transparency, a new analysis predicts its second year will still see big losses to advertisers on FB and YouTube and more collectively losing around $16 billion.

In total, FB will sink $10 billion into its new business with no revenue in 2022.

In February, Amazon (AMZN) announced it would raise its base pay cap from a maximum of $160,000 for most roles to $350,000.

The news comes after employees listed insufficient base pay as the second-most common reason they're looking to leave Amazon in an internal survey conducted last year.

I don’t have an issue with raising salaries, but AMZN had to boost it by far more than double showing readers the intense pressures on current expenses.

Even more problematic now is that new recruits won’t want to accept restricted stock options because of the tech selloff making their stock options less valuable.

Nobody wants to catch a falling knife, me included.

This will put more cash flow pressure on tech companies as new employees will reject stock options and demand a higher net cash salary.

The incremental micro negatives are causing tech companies to miss earnings and guide lower adding yet another negative layer to the grim outlook.

I would argue that even with earnings beats and positive guidance, the tech sector losses would be less.

However, we are experiencing a perfect storm of poor macro events and bad operational data.

Even though the risk reward has improved, it could improve more as the Fed will be forced to ratchet up rates more than expected to compensate for the latest policy mistake.

The market has sniffed this out and is unwilling to buy the dip until the Fed does what is necessary to seriously fight inflation.

The nonsense needs to stop.