“It has become appallingly obvious that our technology has exceeded our humanity.” – Said Scientist Albert Einstein

“It has become appallingly obvious that our technology has exceeded our humanity.” – Said Scientist Albert Einstein

Mad Hedge Technology Letter

April 20, 2022

Fiat Lux

Featured Trade:

(PEAK EYEBALLS)

(DIS), (CURI), (ROKU), (PTON), (ZM), (WBD), (FUBO), (NFLX)

Online streamers now have no pricing power.

Remove jacking up prices from the equation and streamers like Netflix (NFLX) and Disney (DIS) look quite mediocre and that’s what the 35% drop in NFLX shares are telling us.

NFLX Ahh factor has vanished.

It used to be that they knew they could raise prices whenever they wanted and that tool in their kit kept investors on board.

CNN+’s dismal foray into pay tv was another red flag when owner Warner Bros. Discovery (WBD) decided to pull all marketing spend because of the paltry viewing results.

There’s just too much competition out there and instead of creating more leeway, growth was pulled forward the past 2 years, and now the chickens are coming home to roost.

Shelter-at-home stocks like Peloton (PTON) and Zoom (ZM) are now surplus to requirements.

It was just not that long ago, that fresh streaming TV options launched at a frenzied pace.

With many subscription services available, streaming entertainment became ubiquitous in U.S. homes as consumers spent large quantities of time and money on streaming media.

As economies reopen following the end of the health situation, and consumers spend more time outside of their homes, there still are just other things to do like going outside.

The idea that there are still many years of streaming growth lie ahead for the streaming industry has turned out to be an utter fallacy.

These are some tech companies impacted.

The much-anticipated Disney+ streaming service was launched in late 2019, just in time for the health situation.

It added tens of millions of subscribers worldwide in its first year and quickly became the second-largest subscription streaming service after Netflix. Disney also owns the streaming services Hulu and ESPN+ in the U.S. but they still don’t turn a profit on many of these streaming assets yet.

It is unlikely that new content will reverse generating excessive losses.

Better Disney stick to the amusement parks.

Streaming TV has been a boon for the smart TV and streaming device maker.

Roku has become the largest TV platform in the U.S., distributing content via The Roku Channel and acting as a hub for households to manage all of their streaming subscriptions.

Roku distributes its smart TV software and streaming devices at minimal cost, making money instead on advertising and by managing subscriptions.

With peak eyeballs on streaming, don’t expect any explosive growth from Roku, in fact, they could go with a whimper and wait for a buyout.

This is a warning sign for any tech company that chooses to not produce their own in-house content and relying on others to draft the narrative of future health is awfully dangerous in a zero sum game.

Streaming service fuboTV, a relative newcomer to the streaming media industry, went public in 2020.

This small service has gained popularity as a live TV platform, and it’s a top option for those who want to watch live sporting events.

The smaller they come, the harder they fall.

Smaller streaming companies have little recourse when multiple exogenous forces impact the company.

fuboTV is nowhere near profitability and has lost close to half a billion dollars in each of the past 2 years.

Public companies are often harangued for going ex-growth the second they are tradable in New York, and this is the epitome of what I am talking about.

The stock has gone from $35 to $5 today in the past 5 months.

Don’t catch a falling knife here.

CURI is another newbie to the dying streaming industry.

This streaming media company focuses on documentaries and science content and was founded by Discovery’s

CURI is competing against some well-entrenched rivals in the non-fiction TV space, including Discovery and Disney’s National Geographic (available on Disney+).

The young company keeps its content creation costs relatively low since it focuses on educational material and partners with universities, but who really wants to see this type of content anyway.

This company sounds boring and naïve.

CURI’s stock price has gone from $17 to $2 in the past 5 months.

Avoid like the plague!

Mad Hedge Technology Letter

April 18, 2022

Fiat Lux

Featured Trade:

(OMINOUS SIGN FOR TECH EARNINGS)

(NFLX)

A market nostrum I religiously follow of not catching a falling knife could not resonate more with the current situation at streaming giant Netflix (NFLX).

The stock has imploded from $690 to $330 in less than 6 months.

November 2021 represented the high-water mark for many tech growth stocks and NFLX has been dragged into this mess as institutions and hedge funds rush to de-lever their tech portfolio as the panic of higher rates sets into the trading environment.

Does this mark the end to the NFLX model that was the darling of this bull market for so long?

Investors must grapple with this salient question.

NFLX must tap into the bond market to secure funding in order to supply us with high-quality content, so this question is really the crux of the issue.

We are certainly reaching an inflection point where many questions are still in need of answers.

As we approach NFLX’s earnings report tomorrow, the bar has been set extremely low for NFLX.

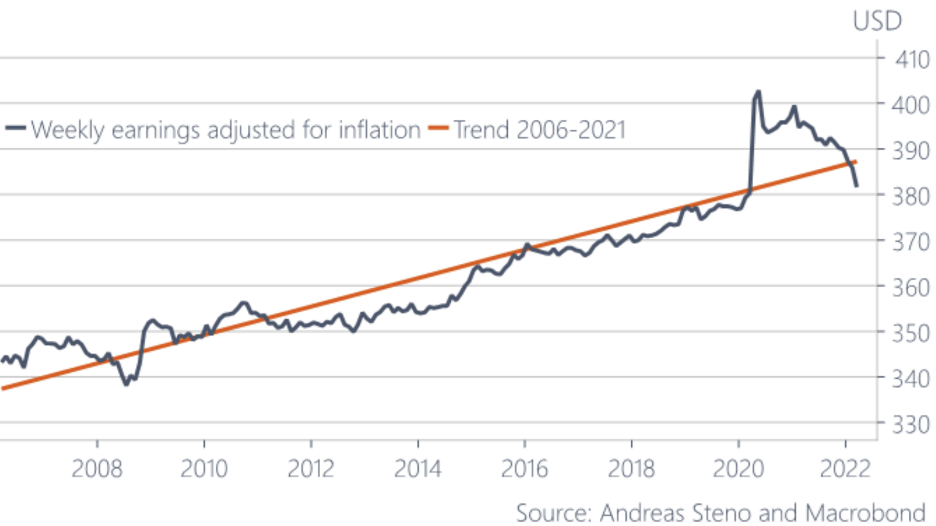

The backdrop is poor with weekly earnings adjusted for inflation decelerating at the fastest since the housing crisis of 2008.

There’s not a lot to look forward to in the tech world as higher expenses are destroying demand, delaying capital investments, and wage increases are depressing the bottom line at a time when supply chain bottlenecks are going from bad to awful.

NFLX is a product that isn’t essential to daily life like energy or food and non-essential services are the services that are getting cut in 2022.

NFLX also has a Russia problem as the company suspended operations in Russia on March 6 with no end in sight to when or if they might return.

Russia had 1 million NFLX subscribers which only represents a drop in the bucket of the 221 million total NFLX subscribers.

Therefore, I must say that the hit to the bottom line will be miniscule if anything.

However, this proves the point of NFLXs arduous slog through iterating in the emerging world. It’s not as easy when you enter a territory with different rules, currency, culture, and rule of law.

For instance, NFLX isn’t even allowed in China and India has fierce competition from local streaming bulwarks.

If they want to return to Russia, NFLX must first answer to breaking Russian law when they refused to abide by a new law that would require the streamer to include 20 "free-to-air" Russian State TV channels.

NFLX remains heavily focused on the emerging world as it looks to aggressively expand its footprint overseas. Four Russian originals were in the midst of production prior to the suspension. The projects have since been put on ice indefinitely.

Sadly, the saturation of NFLX’s cash cow in America and other rich Western democracies has reared its ugly head.

A multipronged revenue slowdown could spiral out of control.

The low-hanging fruit has been plucked and NFLX is still a model that relies on explosive growth to net the incremental subscriber.

It’s not working anymore and there is no plan B which could result in underperformance of the content quality.

Most of the bullishness in the stock’s price action coalesces around higher than expected subscription adds and without that, there is a dark future waiting for NFLX.

In addition to subscriber growth, analysts predict that management will have to answer other key questions, with a particular focus on business operations and profitability, the company's password sharing crackdown, gaming strategy, M&A, and more.

In the near term, NFLX’s guide is more important than ever.

In the heat of deglobalization, a leveraged globalized strategy triggers cognitive dissonance. A strategic reset is needed.

I can envision NFLX winning in some countries and losing in others, but to copy and paste that strategy to every emerging country, which usually has a weak rule of law, sounds like a recipe for continuous weak guidance in the new normal we are in.

Even more worrisome, as high inflation bites more at home, Americans might start to cut back on their NFLX and substitute it with free ads on YouTube and that’s the tail risk that’s not baked into the price of the stock yet.

“Don't be afraid to change the model.” – Said Co-Founder and Co-CEO of Netflix Reed Hastings

Mad Hedge Technology Letter

April 13, 2022

Fiat Lux

Featured Trade:

(THE RISE AND FALL OF SEMICONDUCTORS)

(NVDA), (AMD), (SMH)

The once smoking hot semiconductor industry and its stock prices have rolled over.

First, let me refresh some memories of how we got here in the first place.

During the pandemic and lockdowns, it was thought that semiconductor companies were the winners as consumers, unable to leave their homes, were forced to huddle inside glued to their screens.

Never had the world’s demand for electronics been so elevated and the bringing forward of economic overperformance is now on the downtrend.

It appears that chip companies will be unable to follow up that performance with an encore.

November 2021 represented the short-term high-water mark for chip companies as many stocks in the best of breed have cratered by 50% since then.

AMD (AMD) has dropped to $97 from $155 and the price action is emblematic of boom-bust cycles that chip companies are infamous for.

Now the short-term future doesn’t seem as rosy as it once was and the current uncertainty has delayed investments as chip companies have read the tea leaves and given up capital investments like new chip factories.

Top dog Nvidia (NVDA) which produces CPUs and is at the core of every cutting-edge technology in the world has also been stung by its share price dropping around 30% since the peak in November 2021.

This isn’t the death of the chip industry, and the share price will need to digest the confluence of bad news.

Chip companies are also highly volatile in their price action with the same type of pullback in Apple or Microsoft 3X less volatile.

Peeling back the layers, what is the situation closer to the ground?

The US Central Bank turning on the hawkish turbo boosters mean that many parts of the equity market are feeling their impulsive reaction.

No doubt the Fed has been behind the curve for almost a year, but that’s another topic.

Their sudden reversal means they have no choice but to bring forward a recession by hiking rates faster than expectations and the losers in this is growth tech.

At the consumer level, higher inflation means that sticker prices for electronics have trended higher for various items.

Not only that, the inflation across the board and deep hits to the overall cost of living have taken purchasing power out of the pockets of the median US shopper.

The math simply doesn’t work out if shoppers are paying more for gas, groceries, and housing, they are simply less inclined to refresh their phones, iPads, TVs, and so on.

Other big-ticket items on the chopping block are products like appliances.

There is a major guzzler of chips like washing machines, fridges, and heating and cooling systems that all require sensors.

The semiconductor market is cyclical. When the economy is thriving, it is doing well because when consumers are confident, they tend to spend on the incremental device.

Adding insult to industry is that the tightening of capital markets will make borrowing more expensive and the path to profits narrower.

Just as critical, no CEO or CFO likes to discover that the cost of capital has jumped to a prohibitive rate, because these are the tool they tap to build multi-billion dollar factories.

Holding off on investments sacrifices long-term growth and capacity for short-term balance sheet strength.

Without too much pretentious banter, high interest rates mean relatively less profit.

Much of the decline is starting to get priced into the stock prices of NVDA and AMD.

I believe investors should be dollar cost averaging as these stocks fall possibly another 5-10%.

I would be shocked if these stocks fall another 20% from here.

“Our industry does not respect tradition – it only respects innovation.” – Said CEO of Microsoft Satya Nadella

Mad Hedge Technology Letter

April 11, 2022

Fiat Lux

Featured Trade:

(SMALL EV PLAYERS HIT HARD)

(RIVN), (TSLA), (NIO)