“Based on my experience, I would say that rather than taking lessons in how to become an entrepreneur, you should jump into the pool and start swimming.” – Said Co-Founder and Former CEO of Uber Travis Kalanick

“Based on my experience, I would say that rather than taking lessons in how to become an entrepreneur, you should jump into the pool and start swimming.” – Said Co-Founder and Former CEO of Uber Travis Kalanick

Mad Hedge Technology Letter

January 31, 2022

Fiat Lux

Featured Trade:

(THE NEXT WAVE OF LITHIUM BATTERY DEMAND IS HERE)

(LAC), (ALB), (LTHM), (LIT), (BAT)

The theme of consumer price inflation is here to stay as the largest increase in inflation since 1982 has been fueled by major price spikes.

Energy and mobility are high up on the list of inflationary items and in 2022, when you combine these two, the result is electric vehicles.

2022 is the year of the EV and that means the world needs to produce more lithium batteries.

Inflation has penetrated deep into the consumer psyche and consumers have started to mentally adjust to the realities that we must pay higher prices permanently.

In phone interviews with a random sample of more than 800 Americans, energy prices were one of the leading items of discontent because of the reliance on gas-guzzling cars.

High oil prices along with global government policy is promising to be a boon for EV makers.

We sit here on the precipice of a massive transformation into advanced mobility.

I believe that lithium stocks are poised for higher highs in 2022’s as the demand for EV soars.

To satisfy the industry's insatiable appetite for lithium, global supply will have to quadruple to 2 million metric tons by 2030.

Current and expected projects should be able to meet demand until 2025, but after that, the world will need to explore more supply.

Over the longer term, high prices will fix themselves by spurring miners to increase production. Higher prices will also encourage more lithium recycling, further boosting supply. Meanwhile, companies that buy lithium will look for cheaper alternatives.

Lithium companies that need to be looked at:

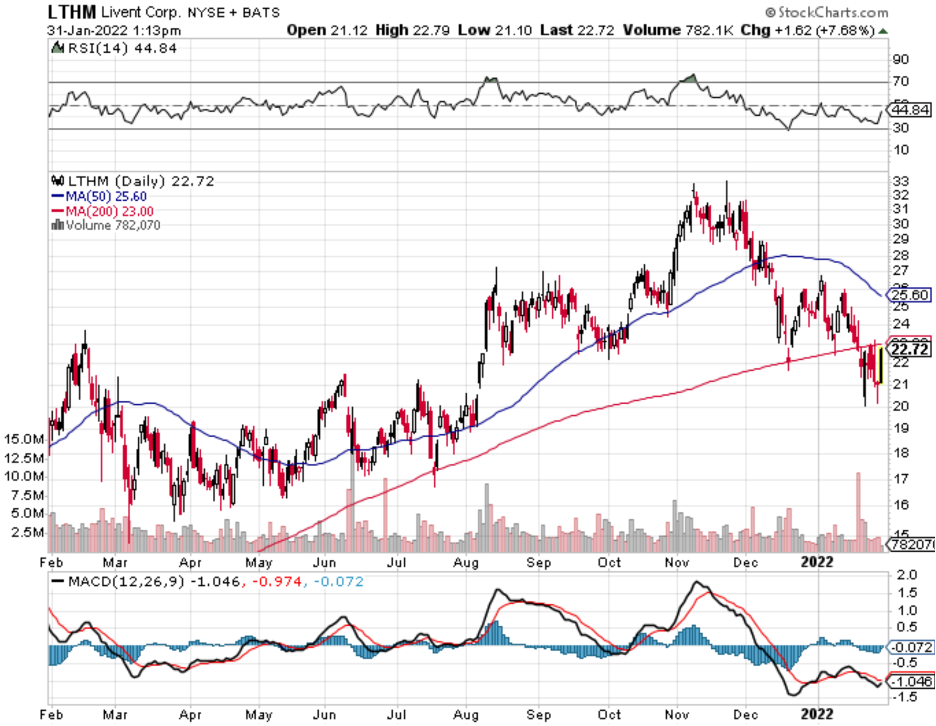

There are more native plays involved in more of the lithium supply chain than simply mining. Livent Corp. (LTHM), which is on track with its own near-term lithium expansion plans and has a decent cash-to-debt ratio, adds value to the lithium it mines by turning it into compounds for the electric vehicle market and other industries.

ALB stock is also among the best lithium stocks to consider for the medium to long term.

For Q3 2021, the company reported lithium sales of $354 million, which was higher by 33% year over year.

Remember that some of these companies have never extracted any lithium and are trading on the prospect of mining lithium so it’s important to differentiate who actually has meaningful sales.

Overall, ALB’s lithium, bromine and catalyst business segments reported $863 million for the third quarter. The key point to note is that Albemarle expects earnings to increase three-fold by 2026. A large part of this growth is likely to come from lithium expansion.

Lithium Americas (LAC) got a boost right as 2021 kicked off when its Thacker Pass project in Nevada, which had been delayed for years because of the inability to receive a federal permit.

Thacker Pass is said to have the largest lithium resource in the U.S. and holds the key to the company's growth.

Finally obtaining the Thacker Pass permit was a big deal, but the $400 million in issued debt means it will cost a pretty penny to extract.

Lithium Americas continue to make inroads on its other project, the Cauchari-Olaroz mine in Argentina, which it owns alongside China's Ganfeng Lithium.

The two companies announced second-stage expansion to add additional annual capacity of at least 20,000 tons of battery-grade lithium carbonate equivalent (LCE) by 2025.

Investors also have the choice to reduce risk by buying into a Lithium ETF.

The Global X Lithium & Battery Tech ETF (LIT) and Amplify Lithium & Battery Technology ETF (BATT) are some that readers should look at.

“I even went to KFC when it came to my city. Twenty-four people went for the job. Twenty-three were accepted.” – Founder and Former CEO of Alibaba Jack Ma when asked about applying for jobs after university

Mad Hedge Technology Letter

January 28, 2022

Fiat Lux

Featured Trade:

(APPLE PUSHES THE ENVELOPE)

(MSFT), (AAPL), (GOOGL), (FB)

We can flip through the thesaurus to look for superlatives that would describe how Apple (AAPL) is performing versus the rest of the market or tech sector, yet it really doesn’t matter who we compare them to, because no matter what we do, somebody would need to be clinically insane to bet against this well-oiled machine.

To give credit where credit is due, Apple CEO Tim Cook parlayed his friendship with co-founder Steve Jobs into the top job at Apple precisely because he was and still very much is an operational specialist.

In times of pandemic, climate change, supply chain problems, hyperinflation, and geopolitical volatility, this is the man you want at the helm to make those operational decisions that benefit shareholders.

Cook even pulled off China and is the only person in Silicon Valley that can claim that level of tech success in the Middle Kingdom.

Not many US tech companies can outdo the Chinese in China, but that is what Cook has managed to achieve and that sometimes gets overlooked.

I have undeniably been a major skeptic about China, but he has managed to penetrate so deeply into Chinese culture that the Chinese can’t root him and his products out without massive disruption and possible social unrest.

Cook, being the operations guy that he is, told the media that he expects supply bottlenecks to ease, which is a major bullish signal to the rest of tech and the semiconductor industry.

That comment alone will mean that the Nasdaq will finish the year at least 7-10% higher than if he didn’t make that comment and to nobody’s surprise, Apple is trending higher by over 6% today and rightly so.

The market trusts Tim Cook and what he says, and I can’t say the same for Tesla’s Elon Musk who loves to overpromise and underdeliver.

This is also good news for the EV sector such as Lucid (LCID) and Rivian (RIVN) which I highlight as two stocks with massive potential even if they can’t ramp up to Tesla levels right away.

Optimizing the supply chain has never been more important today because of the de-globalized elements that have filtered through to corporate America.

Part of streamlining the operations helps when you are Apple and you are Tim Cook and you can negotiate contracts down to the fractional cent.

Other companies simply don’t have that negotiating leverage.

They have curried together that type of goodwill that Apple has with their brand name and footprint.

Moving forward, the best way to decode the content of Apple’s earnings report is by viewing it as an equivalent to an implicit guarantee that margins and operations will be running smoothly for the rest of the year.

That in itself carries more weight than the Fed supplying capital for zombie companies.

I keep mentioning that this is the era in which the balance sheet matters; and wow, Apple has a crystal clean sheet that almost doesn’t need balancing.

Apple’s optionality is just mind-boggling from unlimited buybacks, to possibly raising their dividend from 22 cents, to hiring and expanding their workforce, adding more data centers, and so on.

They literally have any tool in the tool kit to respond to any possible headwind.

That is a luxury that most tech companies cannot claim to possess aside from a handful.

As Microsoft reported stellar earnings, this is just another feather in the cap for big tech.

Big tech is protected from the carnage that smaller tech companies must face, and who have less options to remediate possible devastating internal or external threats.

Not only is Apple riding high on their horse at the vanguard, but they possess products and software that simply can’t be substituted out, which easily creates an overwhelming strong hand when it comes to pricing power.

Next in the queue with earnings is Alphabet (GOOGL), where I fully expect them to reveal record earnings. Facebook (FB) too should do well, but not as good as GOOGL.

Don’t bet against Goliath.

Mad Hedge Technology Letter

January 26, 2022

Fiat Lux

Featured Trade:

(MSFT DIGS US OUT OF A HOLE)

(MSFT), (AMZN), (GOOGL), (AAPL)

The 14% selloff year to date in tech shares finally met its match when Microsoft (MSFT) soothed us with its most recent quarterly performance.

It’s starting to feel like a broken record, but this world belongs to 5 large Silicon Valley tech companies and for the rest of the other few hundred publicly listed companies, we are just living in their world.

And it just so happens that if anybody or anyone is anointed as the savior to save this market from capitulating, it has to be the heavy lifters and we are getting validation from the strongest of cloud/enterprise companies.

Just as resonating, MSFTs positive quarter draws yet one more line in the sand for Mr. Market, offering us support and offering us evidence this could morph into a short-term bottom.

Even more salient, this is even deeper evidence that the software sector is the cream of the crop in tech and their strategic position is only getting stronger.

The thing that these guys have that is critical in today’s economic environment is tinged with inflation headwinds — pricing power.

Starting in March, Microsoft is pushing through an MSFT 365 price hike and consumers and businesses will see their monthly bill go up a few bucks.

According to Microsoft, those increases will apply globally with local market adjustments for certain regions.

And it’s not that 365 is MSFT's cutting edge division, it’s just another example of how MSFT can raise prices and consumers have no other choice but to comply because, at this point, 365 is a utility.

Sure, you can find a substitute, but it wouldn’t be as good of a product.

It was a record quarter, driven by the continued strength of the Microsoft Cloud, which surpassed $22 billion in revenue, up 32% year over year. We are living through a generational shift in our economy and society. Digital technology is the most malleable resource at the world's disposal to overcome constraints and reimagine everyday work and life.

Anyone who bet the ranch on the cloud and enterprise is happy they bet the ranch on it.

MSFT's earnings were just a giant confirmation of how tech won’t be knocked off its perch as the apex warrior, not only in the Nasdaq index but the broader market.

The stock market has been a tech market for quite a few years and that can’t be ignored or discounted.

Fundamentally, the foundations of profitable tech stocks have never been healthier, and they are extracting more of the pie than ever.

Then as we hear nonstop about the upcoming metaverse project and its entryways through gaming, MSFT is so on top of that new development that they will put all other companies to shame.

Granted, there are other heavyweights like Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL) that MSFT must take measures of to see if they are pushing ahead with something they are unaware of, but all is good is Redmond, Washington.

As data volumes and transactions increased over 100% year over year, MSFT has a grip on what’s going on and can quickly pivot to anything that’s worth it with its army of high-quality developers.

MSFT’s ubiquitous fingerprints are everywhere with even over 90% of Fortune 500 companies using Teams Phone this past quarter highlighting the deep penetration into the richest corners of corporate America.

My overarching point is that MSFTs products aren’t just a one-trick pony ala Facebook.

More than half of customers have four or more MSFT workloads, up 75% year over year, underscoring MSFTs end-to-end differentiation.

On a short-term trading basis, traders must adopt tech winners with robust balance sheets, and this must be looked at as a dealbreaker or deal winner of sorts.

In a world that is clamoring for quality tech names, it’s no time to allocate your hard-earned savings into Podunk technology.

Once the macro washout fades, pile into MSFT!

What I am saying is that there is a great deal of the market to plain out avoid, and don’t get caught up in those lemons.

“Culture eats strategy for breakfast.” – Said Microsoft CEO Satya Nadella

Mad Hedge Technology Letter

January 24, 2022

Fiat Lux

Featured Trade:

(BEST OF THE REST GETS SLAUGHTERED)

(MSFT), (SNAP), (GOOGL), (AAPL), (AMZN), (FB), (TIKTOK)