Mad Hedge Technology Letter

January 12, 2022

Fiat Lux

Featured Trade:

(JUMP OFF THE ROKU BANDWAGON)

(ROKU), (GOOGL), (AMZN)

Mad Hedge Technology Letter

January 12, 2022

Fiat Lux

Featured Trade:

(JUMP OFF THE ROKU BANDWAGON)

(ROKU), (GOOGL), (AMZN)

Many “experts” have been advising investors to buy the dip in Roku (ROKU) since it dropped to $370 from the peak of $480 it reached in July 2020.

These experts kept banging the drum to buy the dip on Roku as it slid to $350 then $320.

The calls for dip-buying continue as Roku nosedived to $280 then most recently on a downgrade, Roku fell all the way to $177.

Painful as it feels to be an investor in Roku, this is not the time to double down on high-tech growth stocks.

Growth tends to usually overshoot to the upside as investors give a pass to growth for losing money and selectively put a premium on high growth rates.

But that deal is only valid in a low-interest rate environment and what we are witnessing is the reverse happen as investors are bolting from Roku like stallions out the back of a stable.

At a micro level, there is somewhat distaste at the ever-increasing competition Roku is facing and the lack of growth prospects overseas.

Overseas is usually the growth engine for many of these streaming cohorts, but the dilemma here is that margins are lower because of a poor purchasing power profiles for the median consumer overseas.

That’s not to say it’s easy to succeed in the U.S. — hardly so.

However, Roku’s business in the United States has been highly successful, but the issue here is that the market is getting somewhat saturated and since the stock market is priced based on future cash flow, where does the incremental buying come from to save Roku’s stock?

Roku faces a perilous uphill challenge to convince the incremental platform user to install its Roku stick at a time when Amazon (AMZN) and Google (GOOGL) are using their greater clout and sharper elbows to get rid of the tech peons.

Amazon reported sales of over 150 million Fire TV devices recently. Roku has over 56 million active accounts, although it’s not a direct comparison because Amazon’s figure counts sold devices and includes Fire TV devices that are not being used.

There is no possible way that Roku can secure 50% of the market here and 40% would be a stretch capping its ceiling.

Another leery signal came when smart television maker TCL who have partnered to make the Roku smart TV decided to jump ship to Google.

This could represent a red flag as these bigger companies have the capacity to poach talent, know-how, and convince suppliers to jump ship with a more lucrative contract for a larger install base.

This could be the first point of contact that could eventually lead to Google buying out TCL and cutting off Roku from a source of a hardware supplier.

TCL has now claimed to be one of the biggest sellers of sets featuring Google’s connected TV operating system and the partnership will take precedence over anything Roku is involved with.

In the short term, readers need to stay away from Roku as we need more commentary on how it plans to shake off Google and Amazon and how it plans to navigate a perceived saturation in its domestic business while underperforming overseas.

Granted, it’s intimidating to go up against Google and Amazon because there are less tools available in the tool kit in terms of stacking resources and convincing consumers that they are indeed a higher quality product.

Long term, I don’t see it for Roku.

Short term, it’s dicey at best.

This stock promises to be volatile in the next three months and actively trading this stock will probably mean selling sharp rallies and avoiding dips.

The first-mover advantage was stellar for a while and Roku rode that donkey up the mountain of success, but now as reality sets in and the first-mover advantage dissipates, they need a miracle or should just negotiate to sell itself while the stock price is still near $200.

It’s sink-or-swim at this point.

“I have a secret project which adds four hours every day to the 24 hours we have. There's a bit of time travel involved.” – Said CEO of Google Sundar Pichai

Mad Hedge Technology Letter

January 10, 2022

Fiat Lux

Featured Trade:

(THE EV DARKHORSE)

(LCID), (TSLA), (NKLA)

2022 could be the year that Lucid Motors (LCID) put a dent in the universe as one of the many EV upstarts hoping to eventually challenge Tesla (TSLA) one day on top of their lofty perch.

Realistically, many EV companies never get to the point of delivering cars, like fraudulent company Nikola (NKLA), but Lucid has started to roll out new cars to US customers.

Things move fast in the EV industry and Lucid has announced they are planning to start shipping cars in Europe sometime this year.

The stock exploded to the upside on the announcement.

Conceptually, the idea that Lucid is expanding fast, creating and looking to take advantage of the total addressable market in Europe only signals to investors they are doing all the right things in all the right places.

I believe there is loads of momentum in EV cars today, and their trajectory this year is impressive as we are seeing it in our news feeds.

I am not just talking about Tesla, but the mainstreaming of the product will help the next in line to build something competitive to Tesla and Tesla blazing an early trail has helped really legitimize the industry.

Sure, at the micro level, there are still teething pains with EVs, like waiting an hour for your Tesla X to charge at a supercharger.

The science behind it still needs to catch up to the point where someone can just get behind a wheel and drive coast to coast without crunching the logistics designed for the trip.

Germany will probably be the most important European market for Lucid, being a car-first society while the citizens harness high purchasing power.

Lucid also wants an expansive taste of Europe by expanding all over and that means places like Sweden and Switzerland.

The company is currently building its only model, the Air sedan, at its Arizona plant, yet the volume of cars is kept from the public view.

The firm pumped out a few hundred cars in 2021 but wants to ramp up to 20,000 by the end of 2022.

The vehicles it has delivered so far don’t have a full variety of active safety aids online, but they will be enabled via an over-the-air updated by the end of January.

Just like Tesla, Lucid will probably try to push its direct sales model in Europe as well. The manufacturer has already announced plans to set up nine Lucid Studios in the United States and major European cities are in the mix as well.

Lucid CEO Peter Rawlinson has already stated that the company also plans to roll out in the Middle East in 2022, with China following in 2023 so there’s a lot in the pipeline here, but it could be biting off more than they can chew.

If the “EV trade” catches fire this year which is certainly in the realm of possibilities, I see the stock doubling from $42 to over $80 per share.

Let’s not forget that the used car market is so hot that it costs almost as much as buying a new car.

Energy is higher across the board, so why not slap on some solar panels on the roof and drive an EV for free instead of indulging in expensive fossil fuels?

The Saudi Arabia's Public Investment Fund has previously stated that they will not be selling any of their Lucid Motors shares until beyond 2030, which is why they are planning to sell these EVs in the Middle East.

When the PIF gave Lucid Motors an investment of $1 billion in 2018, that deal was contingent on Lucid Motors building a plant in Saudi Arabia.

Lucid is projecting themselves to be a leader in solar, and by 2026 they estimate that they will make over $22 billion a year from their Renewable Energy division.

This EV company has a solid foundation, and if the cars stack up nicely against the Teslas of the world, then they really have the potential to uplift the stock price in 2022.

Reviews of its car have been generally good, with highlights like world-class efficiency, miraculous packaging, and amazing performance and comfort.

This could be the dark horse of EV’s in 2022 and I am looking out for a splashier Lucid EV model in the years ahead. I am bullish on Lucid Motors.

Mad Hedge Technology Letter

January 7, 2022

Fiat Lux

Featured Trade:

(THE DEATH OF VISA AND MASTERCARD)

(MA), (V), (SQ), (PYPL), (AFTPY), (AFRM), (AMZN)

Visa and Mastercard’s card networks are a relic of the past, not in terms of reach or footprint, but the technology of it.

This will cost their stock price and we are already seeing it play out in the market.

The canary in the coal mine was fintech players Square (SQ) and PayPal (PYPL) whose share prices were pummeled at the back end of last year.

PYPL is down 40% from its 2021 peak and SQ experienced a similar 42% drop.

This fierce competition and the crowded marketplace have investors paying less of a premium than ever before.

In a tightening rate environment, it’s clear the wolves are out for more flesh and the contagion will spread to those further up the food chain.

Fintech business models aren’t as robust or foundational as the bulwarks of MA and V, but questions must be asked if small businesses aren’t willing to pay an extra 2% on sales for outdated technology.

The fintech space has moved a long way in a short amount of time causing investors to be concerned about secular growth sustainability.

Among them are concerns that consumers are shifting to debit, away from higher-margin credit cards.

Consumers are also using more alternative payment methods that may bypass the card networks, including “buy now pay later” services offered by companies like Klarna, Afterpay (AFTPY), and Affirm (AFRM).

Visa has also come under pressure from a recent announcement by Amazon.com (AMZN) that next year it will stop accepting Visa-branded credit cards issued in the United Kingdom and this could be the beginning of a narrowing of Visas’ moat that could trigger a domino effect in other rich western countries.

The bulls would say that the stocks could undergo a reversal if the Omicron variant is not as bad as initially thought creating a tsunami of consumer spending massaging the bottom line for Visa and Mastercard.

But it’s looking more like V and MA are the victims of tightening travel restrictions around the globe and elevated positive cases that are immobilizing consumers.

The big card networks rely heavily on revenues related to cross-border travel as consumers and businesses use their cards for airfare, Airbnb’s, and Ubers, as well as duty-free gifts in foreign countries.

Multiples may need to come down if the Omicron variant puts the shackles on travel as countries reimpose bans or quarantine rules.

Investors had been counting on a recovery in cross-border travel to boost revenues for the card networks. This is definitely a kick in the nuts after initially seeing momentum as countries in general trended to loosening restrictions.

International transactions brought in $1.9 billion, or 21%, of Visa’s $8.9 billion in revenues for the 2021 fourth quarter.

The segment is highly profitable due to steep transaction and foreign-exchange fees. Cross-border margins come in around 69%, contributing significantly to Visa’s overall earnings per share.

The Christmas season has been confronted by a bevy of new restrictions as many places consider other measures to curb the spread of the Omicron variant.

Ultimately, even if MA and V can get positive reinforcement from increased short-term travel which seems unlikely, alternative business models are breathing down their neck as the technology of money has advanced.

The “buy now, pay later” phenomenon, although risky, is a rapid gut punch to the incumbents.

Then consider there is speculative technology like Bitcoin out there that bypasses these dinosaur networks altogether.

I believe 2022 is the year that MA and V get exposed as a luxury in a frugal world where small businesses can’t afford to give away 2% of revenue.

There’s too much money being invested into the technology of money for small businesses to reach for MA and V’s network.

Even open banking and digital networks can really dent the traditional payment networks.

Basically, I believe these companies have hit the high-water mark, and the likes of Zelle and Venmo will start to put pressure on these high fees.

Places like China don’t even use them by bypassing them through digital wallets like Wechat pay and Alipay.

Pie shrinkage and revenue decelerate — I believe this is one of the seminal trends we will see in fintech in 2022.

“Study hard so that you can master technology, which allows us to master nature.” – Said Argentine Revolutionary Che Guevara

Mad Hedge Technology Letter

January 5, 2022

Fiat Lux

Featured Trade:

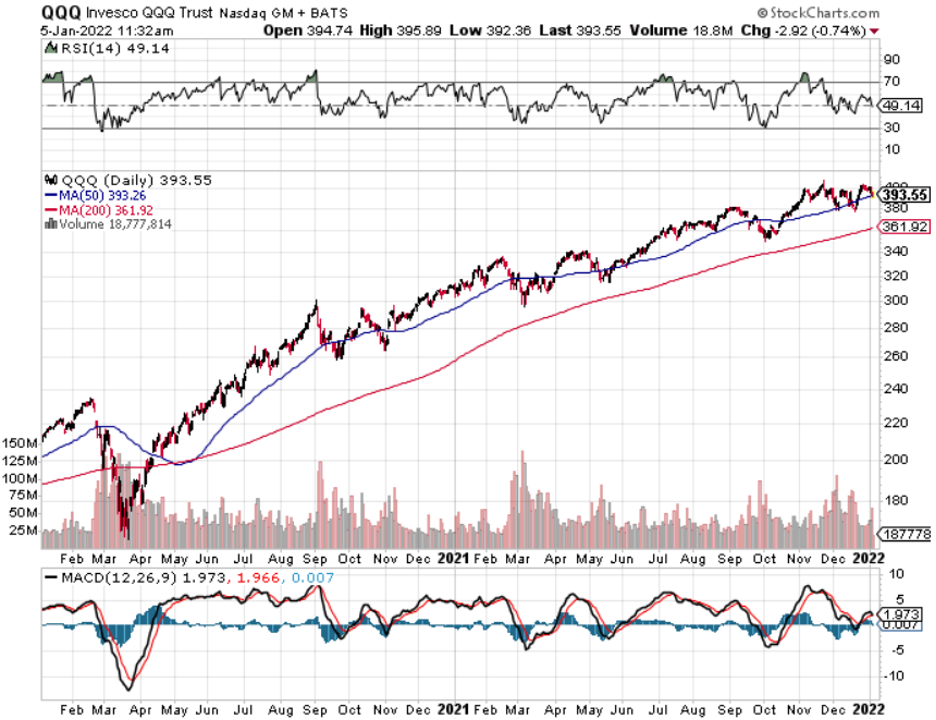

(10 REASONS WHY THE DIGITAL ECONOMY IS THRIVING)

(QQQ)

The outlier out there is inexorably linked with technology because, since early 2020, we have experienced a renaissance in efficiency and productivity, largely driven by our weaponization of technology that strongly feeds into the overall economy.

This drove the United States economy to higher growth rates in 2021, and the market isn’t expecting close to 6% of US economic growth in 2022 after the Build Back Better bill was thrown in the dustbin by the Senate.

The truth is that America has never been better at creating quality growth, and that largely flies in the face of mercantilist economies who build inefficient ghost cities or spew out pollution to register growth.

There has never been a better time to be employed in the United States, and the pandemic brought on a revelation of newly formed companies offering highly specialized services in droves.

If you travel abroad, many countries have in fact lost services in aggregate and have largely not replaced because many emerging cities don’t have the spirit of entrepreneurship, access to robust digital infrastructure, or access to cheap capital like in the US.

Although working remotely is not entirely unique to the United States, the U.S. has integrated this phenomenon into the social fabric of daily work life better than almost any other country.

Japanese workers are still required for in-person office time to use the office fax machine and Europe has made inroads to working remotely but workers often don’t push back on their bosses because of the nominal lack of jobs on the European continent.

Here is a list and explanation of the new type of economy we are thriving in in 2022 and the present synergies that could lead the US economy to surprise to the upside for the foreseeable future.

Technology has always been a catalyst for efficiency.

Adopting modern technology like the cloud, mobile devices, big data, and analytics help businesses achieve higher levels of efficiency and productivity.

Supplementing these platforms is the ability to sprinkle in AI to supercharge the performance by harnessing data to make predictive decisions in real-time.

Firms need to maximize their resources for optimal growth, from capital and labor to suppliers and inventory.

Cloud computing has been adopted widely to support resource sharing across different departments within organizations from an IT standpoint.

The internet of things (IoT) is helping businesses track their resources in near real-time, offering greater visibility into how they are being used and where improvement is needed.

Technology is an enabler for business agility. Companies can leverage new technologies like IoT and blockchain to develop highly resilient business ecosystems.

Every company is turning into a digital company if they like it or not. This means having a well-designed website and being easy to navigate, active on social media platforms, and engaging with customers online. The end game here is being able to bypass retail and communicate directly with customers.

To overperform, businesses need to engage with their customers meaningfully.

Technology can help businesses do this by providing tools to understand their customer’s needs and wants. Data analytics and AI, for example, can be used to create customer profiles, which can then be used to provide personalized customer experiences.

Top companies today deploy IT systems with built-in flexibility and scalability, which deliver instantaneous service when need be.

These AI-based technologies can perform repeatable tasks, freeing employees to focus on more valuable work requiring human intelligence. Also, robotic chatbots can assist human employees in providing high-quality customer service.

Today’s employees are technologically savvy, and they expect to use technology in their work.

New technologies like IoT and AI can help harness hidden knowledge within data and transform it into actionable business insights. Such insight-driven companies can make smarter decisions and identify new revenue streams.

Today’s market is full of innovative startups who are able to harness technology so well that they can deliver new products in days if not hours. Businesses need to be able to sense emerging threats and opportunities early on, and being able to bring products to market faster than the competition is crucial to staying ahead.

Businesses can use big data analytics to identify new market opportunities and potential customer segments. They can also use data-driven marketing techniques like predictive analytics to create targeted marketing campaigns.

To make informed and timely decisions, businesses need accurate and up-to-date information.

Digital technologies can offer a better understanding of the current realities of the industry and how that translates onto a balance sheet. This allows for better decision-making, more effective business processes, and a more robust overall company culture.

In a Yahoo Finance interview with hedge fund manager Jeffrey Gundlach, Gundlach espouses that he has benefited big by betting the ranch on the American economy up until now, and he pauses to say that emerging economies’ equities are cheap, and he likes to buy assets that are cheap.

But he fails to realize that these economies are cheap for a reason, and even if the quality of life has improved drastically in places like Central Europe and Southeast Asia in the past 30 years, it does not mean the foundations are there for a catch-up trade, let alone a tech catch up trade, that relies on momentum investing.

In fact, America has extended its lead as the place everyone wants to invest in, which is why sovereign wealth funds of all sorts have been looking to get into American single-family homes since the pandemic started.

I believe there is a nice surprise to the upside when it comes to tech stocks because companies are using the 10 different ways listed above to supercharge their business models.

Of course, this also depends on the Fed pulling back from its aggressiveness which isn’t guaranteed.