“I want to put a ding in the universe.” – Said Co-Founder of Apple Steve Jobs

“I want to put a ding in the universe.” – Said Co-Founder of Apple Steve Jobs

Mad Hedge Technology Letter

January 3, 2022

Fiat Lux

Featured Trade:

(TESLA SETS THE TONE)

(TSLA), (F)

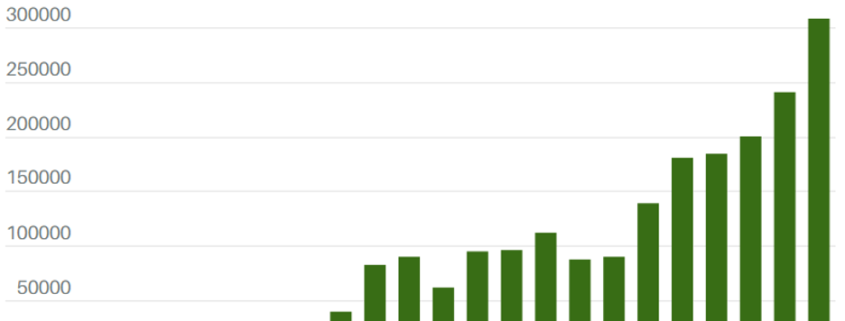

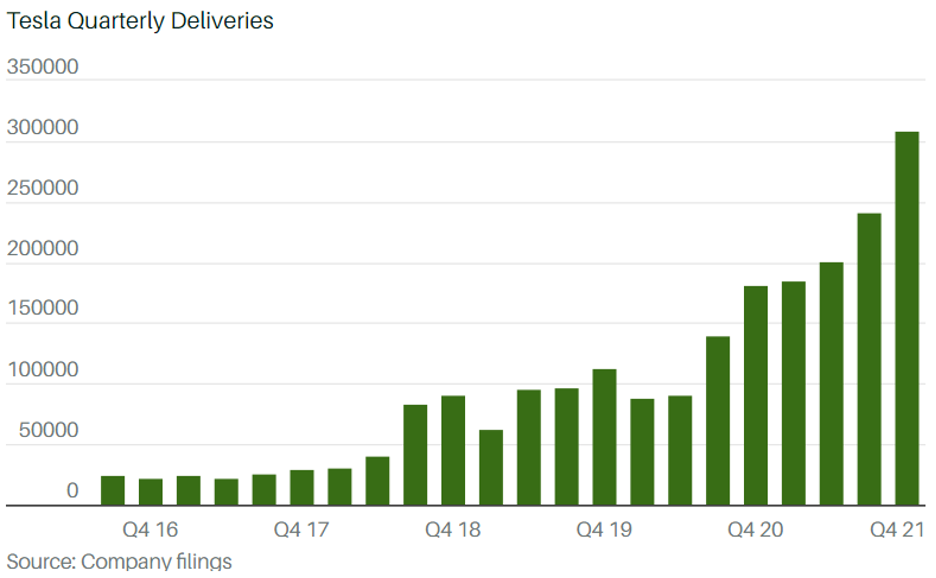

The 87% year-over-year increase in Tesla deliveries this past quarter really sets the tone for Tesla for rest of 2022.

They are picking up where they left off last year and Tesla’s stock price at the end of the year could be substantially higher than it is now.

It’s been a while since I’ve heard from the Tesla haters — and if you remember correctly, there were angry flocks of them up until just recently.

But that’s what overperformance will do to the naysayers, ironically. They’ve never been this quiet, and rightly so, after crushing delivery expectations by 12%

In the same quarter last year, they registered 180,000 deliveries, and the math is stunning with the company adding an extra nominal 128,000 this past quarter to 308,000 units at a time where supply chain shocks and semiconductor shortages are rocking the EV industry.

This leads me to believe that if Tesla can carve out stellar performance at the height of snarled supply chains, imagine what they can do when the world isn’t clogged up.

We must take it seriously when management predicts 50% gains in deliveries year over year for the foreseeable future and what I mean by that is — multiyear.

Ultimately, there is a strong correlation between accelerating Tesla deliveries and an appreciating Tesla stock price and readers shouldn’t overcomplicate things.

The rest is just fluff and readers need to zone it out.

Readers also get the added bonus that Tesla easily outperforms the S&P benched against any standard metric and they are in online brokerage Robinhood’s top stocks to buy based on the data from their own traders.

The delivery beats against consensus are also widening for Tesla who just in 2020 was only able to overdeliver unit deliveries by 3%, which is no small feat, but the under-promising and over-delivering is getting more impressive by the quarter which is the hallmark of a great company with over 10% beats versus consensus the norm today.

The average consensus for gross 2022 deliveries of about 1.4 million looks highly attainable if Tesla can keep up at this clip, which I have faith they can.

Fortifying their already enviable position is the success of the Shanghai Gigafactory, and the potential to sell 60,000 Tesla’s to Chinese customers this year.

Gazing into our 2022 crystal ball, the EV story and the narrative underpinning it look healthy and, more importantly, sustainable.

Over the past decade, the EV market has gone from a drip of EV choices to a full-out avalanche of options on the US market these days.

Recent surveys back up the concept of insatiable thirst for new EV buyers, and higher oil prices have added an extra turbocharger to EV demand.

A private survey showed that the percentage of U.S. adults who say they would consider purchasing an EV in the next 10 years has seen active growth over the course of 2021, as announcements of new models and new charging infrastructure add gloss to the already emerging industry.

One might surmise that this could be the year of an EV inflection point when it comes to getting bums in EV seats.

This could be the year where the numbers gap up and put gas-powered engines in the rear-view mirror.

The number of options in 2022 starts from roughly 62 models currently available to at least 100 later this year.

But U.S. consumers love to buy pickup trucks, crossovers, and SUVs, and their dramatic arrival on the EV market is one of the main reasons 2022 could be unprecedented for adoption.

The next big blockbuster launch — Ford (F) is beginning production on its F-150 Lightning pickup truck in Spring 2022, giving consumers the option of purchasing an electric version of the best-selling car in the country.

58% of Gen Z and 60% of Millennials have shown a willingness to dip into the future EV market, and by that purchase time, options will be everywhere.

The one true knock against Tesla is the lack of developing a Tesla pick-up truck. Their much-hyped “Cybertruck” has been delayed now over a year to the end of 2022 because of continuous bumps in the supply chain.

This could turn out to be another cash cow for Tesla, with potential Cybertruck revenues topping $400 million in 2023, potentially rising to about $7 billion by 2026.

The takeaway from the Cybertruck project is that Tesla is still in the early stages of its growth cycle, and will be expanding at a 50% rate while ingratiating its diehard audience with more products than they can handle.

Tesla products are backlogged to the hills, try inputting a new Tesla X for online purchase, and their official website spits out an estimated delivery date of January 2023.

That’s how great this product is, so don’t diminish it or its ever-higher stock price.

It’s high for a reason and will be higher in the future.

“AI doesn’t have to be evil to destroy humanity – if AI has a goal and humanity just happens to come in the way, it will destroy humanity as a matter of course without even thinking about it, no hard feelings.” – Said Founder and CEO of Tesla Elon Musk

Mad Hedge Technology Letter

December 29, 2021

Fiat Lux

Featured Trade:

(AUTOMATION AND BANKING)

(SQ), (PYPL), (APPL), (AMZN)

Automation is taking place at warp speed displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the direct capital of $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. bank jobs getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificially engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

Front-office staff has already felt the brunt of downsizing with purges carried out from 2018 representing an eighth year of continuous decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30% and the accumulation of hordes of data will advance the marketing effort into a smart, multi-pronged, hybrid cloud-based and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies like PayPal and Square are chomping at the bit and even tech companies like Amazon and Apple have started tinkering with new financial products.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 63,036 employees in 2019, more than 10x higher the number of U.S. financial job losses and that has continued in 2020 and 2021.

In a sign of the times, the European outlook has turned demonstrably negative with Deutsche Bank announcing layoffs of 40,000 employees through 2023 as it scales down its investment banking business.

Germany banks are also passing on the burden of negative interest rates to their clients.

A recent survey by Deutsche Bundesbank shows that 58% of banks are charging all savers negative interest rates while others only target wealthy and corporate clients.

If the U.S. dips into negatives rates in the future, expect the same nasty effect on job force cuts that Europe has experienced.

Either way, don’t tell your kid to get into banking, because they will most likely be feeding on scraps at that point.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

Mad Hedge Technology Letter

December 27, 2021

Fiat Lux

Featured Trade:

(SWITCHING CAMPUSES FOR FULFILLMENT CENTERS)

(AMZN), (TGT), (WMT)

Moving on to tomorrow’s tech and the decisive trends that will power your tech portfolio, you can’t help but think about what will happen to the American university system if we are slammed with another delta dropkick.

A bachelor’s degree has already been massively devalued with each subsequent “wave” knocking off an extra 20% from a 4-year achievement.

Another unstoppable trend that shows no signs of abating is the “winner take all” mentality of the tech industry.

The virus was a great catalyst for U.S. tech companies and U.S. asset holders in stocks and real estate to cash in with a smash and grab of the century effectively leaving the rest of the uncompetitive global economy in its wake.

Remember this is all while China is destroying their own tech companies with zeal because they perceive them as too powerful at this point and a legitimate threat to the interest of the communist party.

Now, tech giants will apply their huge relative gains to gut different industries and have set their sights on academics and the buildings they operate from as their next exercise in destroy and conquer.

Recently, we got clarity on big-box malls becoming the new tech fulfillment centers with the largest mall operator in the United States, Simon Property Group (SPG), signaling they are willing to convert space leftover in malls from Sears and J.C. Penny.

The next bombshell would hit sooner rather than later.

College campuses will become the newest of the new Amazon (AMZN), Walmart (WMT), or Target (TGT) eCommerce fulfillment centers, and let me explain to you why.

When the California state college system shut down its campuses and moved classes online due to the coronavirus in March, rising sophomore Jose Antonio returned home to Vallejo, California where he expected to finish his classes and “chill” with friends and family.

Then Amazon announced plans to fill 100,000 positions across the U.S at fulfillment and distribution centers to handle the surge of online orders. A month later, the company said it needed another 75,000 positions just to keep up with demand. More than 1,000 of those jobs were added at the five local fulfillment centers. Amazon also announced it would raise the minimum wage from $15 to $17 per hour through the end of April.

Antonio, a marketing and communications major, jumped at the chance and was hired right away to work in the fulfillment center near Vacaville that mostly services the greater Bay Area. He was thrilled to earn extra spending money while he was home and doing his schoolwork online.

This was just the first wave of hiring for these fulfillment center jobs, and there will be a second, third, and fourth wave as eCommerce volumes spike.

Even college students desperate for the cash might quit academics all together to focus on starting from the bottom at Amazon or launching an e-store.

Even though many of these jobs at Amazon fulfillment centers aren’t the plush office job that Ivy League graduates covet, any job will do for the bottom 40% of hardworking Americans.

The rise of ecommerce has happened at a time when the cost of a college education has risen by 250% and more often than not, the price rises don’t live up to the value accretion.

Many fresh graduates are mired in $100,000 or even $200,000 plus debt burdens that prevent them from getting a foothold on the property ladder and delay household formation and there’s been no indication President Biden is about to cancel this colossal debt.

Then consider that many of the 1000s of colleges that dot America have borrowed capital to the hills building glitzy business schools, $200 million football locker rooms, and rewarding the entrenched bureaucrats at the school management level outrageous compensation packages.

America will be saddled with scores of colleges and universities shuttering because they can’t meet their debt obligations.

The financial profiles of prospective students have dipped by 50% or more in the short-term with their parents unable to find the money to send their kids back to college, not to mention the health risks.

Then there is the international element here with the lucrative Chinese student that added up to 500,000 total students attending American universities in the past.

They won’t come back as well.

The college campuses will be carcasses with juicy meat on the bones allowing Jeff Bezos to choose the prime cuts.

The coronavirus has exposed the American college system for what it is, and not every college has a $40 billion endowment fund like Harvard to withstand today’s financial apocalypse.

The only two industries now big enough to quench big tech’s insatiable appetite for devouring revenue are healthcare and education.

We are seeing this play out quickly, and once tech gets a foothold literally and physically on campus, the rest of the colleges will be thrust into an existential crisis of epic proportions with the only survivors being the ones with large endowment funds and a global brand name.

It’s scary, isn’t it?

This is how tech has evolved and certain parts of society are now diminished while others supercharged.

This is also part of how the world is changing so rapidly now because of a combustible mix of geopolitics, health scares, and accelerating technology that average people can’t recognize the world we live in anymore.

When this happens, close your eyes and buy tech stocks since most of us don’t run pharma companies or can’t extract largesse from dollar or euro-denominated governments.

YOUR NEW DELIVERY CENTER

“Life is not fair; get used to it.” Said the founder of Microsoft Bill Gates.

Neuralink Corporation is an American neurotechnology company developing implantable brain-machine interfaces.

You would think this is straight out of science fiction, but mark my word that in our lifetime, we could all be operating digital devices from our heads if Musk gets his way.

And he often does get his way.

Scary as it seems now, this will probably be the first of many artificial intelligence procedures to infuse humans with layers of artificial intelligence.

Musk believes humans will go the way of robot hybrid in the future because the natural development of competition is trending in that way and sadly, this direction in humanity is ultimately existential for every one of us.

Improvements in technology will periodically be announced and iterations will need to be adopted because software is upgraded.

As for today and now, testing on pigs has segued into testing on monkeys.

Musk has told us the monkey testing has gone “well.”

Pending FDA approval, Musk hopes to start testing humans with severe spinal-cord injuries like tetraplegics, quadriplegics in 2022 which would represent a monumental step in this technology.

Earlier this year, a 20-person biotech firm called Synchron secured approval from the FDA to start human testing, so the stakes are high and imminent.

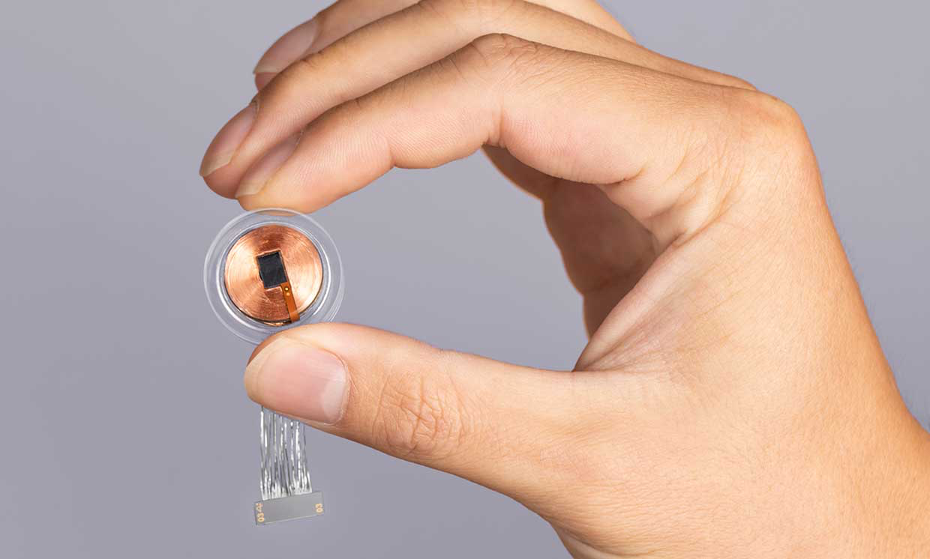

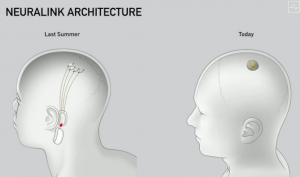

Neuralink’s dramatically simplified design for an implant that hopes to create brain-to-machine interfaces is a big deal and partly because of the star power backing the project that can literally move mountains.

The previous design consisted of a bean-shaped device that would sit behind the ear, but now it is the size of a large coin, and it goes in your skull.

I expect the final iteration to be a millimeter wide.

The in-brain device could enable humans with neurological conditions to control technology, such as phones or computers, with mere thoughts.

The other use case is solving neurological disorders from memory, hearing loss, and blindness to paralysis, depression, and brain damage which is a tad more altruistic.

The current prototype – referred to as version 0.9 – measures 23 millimeters by eight millimeters and has 1024 electrode "threads" attached to it that are implanted into the brain.

It is designed to replace a coin-sized portion of the skull and sit flush so it would be physically unnoticeable. It would be inductively charged the same way you would wirelessly charge a smartwatch or a phone.

The surgical robot, which is programmed to insert the neural threads safely into the brain, was done by US design company Woke Studios.

Woke Studio’s robot would be able to insert the link in under an hour without general anesthesia, with the patient able to leave the hospital right away.

The robot will eventually do the entire surgery – so everything from the incision, removing the skull, inserting electrodes, placing the device, and then closing things up.

It will be completely automated.

If this technology is green-lighted by the U.S. Federal Government, I envision a free for all into this technology from the likes of Facebook, Google, Apple, and Microsoft, and so on.

If you thought website “cookie tracking” is bad now, then once tech firms are granted access to consumers’ brains, it could open up a pandora's box of moral conflicts of interest, an avalanche of revenue opportunities, and lawsuits galore.

Look at the hesitation and disgruntlement of the health industry hoping to convince Americans to take two jabs of an mRNA vaccine in the arm and now think about trying to convince humans to implant a chip in their head for the sake of competing.

Will American society really get to the point where Facebook is selling your “thoughts” to neural advertisers?

It’s scary to think about but that is the direction we are headed down for better or worse.

If you view this through the lens of big tech, battering down the hatches to get access to consumers’ “thoughts” is the holy grail of access points and revenue flow.

In 2021, humans still need to digest thoughts and carry out functions through actionable fingers into a phone interface.

We have also allowed big tech into our home feeding them data through smart devices and virtual assistants like Amazon Alexa.

Getting rid of all that “fluff” and extracting data and behavioral results from the original source is potentially worth over 20 trillion dollars along with a recurring revenue source to infinity.

Not only will physical devices be useless at that point, but they will also spawn a mega cloud storage business that is hooked straight to the mind.

An economic analyst can digest how cloud companies like Amazon and Google would rake in the trillions by storing libraries of data that a mind can tap in at any time.

It really is a gigantic step that will digitize, even if marginally ethical, and computerize humans - big tech is first in line to reap the profits and literally control our brains.

This is the future – a future where we coexist with artificial intelligence and brain chips.