“When something is important enough, you do it even if the odds are not in your favor.” – Said Founder and CEO of Tesla and Neuralink Elon Musk

“When something is important enough, you do it even if the odds are not in your favor.” – Said Founder and CEO of Tesla and Neuralink Elon Musk

Mad Hedge Technology Letter

December 20, 2021

Fiat Lux

Featured Trade:

(GETTING AHEAD WITH THE CLOUD)

(AMZN), (ZS), (CRM), (GOOGL)

Dealing with the Cloud works and for every relevant tech company, this division serves as the pipeline to the CEO position.

If this isn’t the case for a tech company, then there’s something egregiously wrong with them!

Take Andy Jassy, the mastermind behind Amazon’s (AMZN) lucrative cloud computing division and is the man who succeeded company founder Jeff Bezos.

He’s been rewarded this important position based on his performance in the cloud and faces a daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon almost 30 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Cloud 101

If you've been living under a rock the past few years, the cloud phenomenon hasn't yet passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them work remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the recent ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there, your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

The cloud is where you want to be.

Mad Hedge Technology Letter

December 17, 2021

Fiat Lux

Featured Trade:

(LOOKING FORWARD TO TECH IN 2022)

(FB), (NVDA), (AAPL), (MSFT), (AR), (VR)

Another pandemic year is on the verge of being in the books and we need to look yonder to 2022 and what it can offer.

Now that billions are being poured into the project, it’s not weird to say that advanced technology and the arteries and ventricles surrounding it, will all lead to developing this new world called the Metaverse.

The metaverse is a hypothesized iteration of the Internet, supporting persistent online 3-D virtual environments through conventional personal computing, as well as virtual and augmented reality headsets.

And I am not saying this is a new thing just to be cool, analyzing thousands of earnings reports, it’s clear that companies are deploying human capital around gaining a slice of this future Metaverse.

This idea is so prominent that Facebook (FB) changed its name to Meta to signal its commitment to this new technology.

Next year will be the year that we get closer to the real deal — a fully functioning Metaverse even if it might just be a beta version.

And it’s not just Facebook, Apple (AAPL), and Microsoft (MSFT) and the rest are in it too with Nvidia’s (NVDA) chips serving as a building block of the Metaverse.

Naturally, related technologies will be of great importance, and I can easily see a greater surge in augmented reality (AR) interest.

People should also keep a close eye on the introduction of Meta's internet-of-VR.

The idea of the metaverse and an advanced VR world must be seen through the prism of the pandemic which has forced us to become digital first even if many of us aren’t native digital users.

Many of us have had to learn on the go, for instance, download that Zoom video conferencing software or upgrade our home office.

This torrent of internet usage has its pitfalls like explosive growth in cyberattacks, making cybersecurity more important than ever.

Cybersecurity will no longer be seen as an “added extra” by organizations and will be built into the DNA of any and every IT system, from supply chains to infrastructure and devices.

Our reliance on internet leads nicely into 2022 becoming the year when 5G became mainstream.

We are edging towards that point where we need that extra speed to harness our work devices and to wield them in the most efficient and optimal way.

Many of you have had to upgrade data packages, build robust infrastructure into your home office and I don’t mean just buying a better office chair.

This could see the rise of “digital cities” along with new smart mobility services such as autonomous vehicles and 5G connected bicycles. We could also see a rise in private 5G networks for businesses in manufacturing and logistic sectors.

A new era of private connection for businesses will be launched, enabling greater data-driven insights and real-time business decisions.

2022 will see businesses continue to neglect the traditional office and many companies will be at best — hybrid.

We might start seeing companies go bankrupt because they can’t convince any workers to show up in physical form.

It’s already happening to the workers I talk to where limited remote working opportunities when interviewing for new jobs is a deal-breaker.

Next year is also when we finally see artificial intelligence on steroids.

The explosion of AI-powered gadgets, apps, websites, and tools is here for 2022.

It'll become harder to differentiate chatbots from human customer support agents. Other products such as future content recommendations on social media and streaming websites are likely to come from an AI rather than traditional data analysis.

The Internet of Things, AI, and automation will aid businesses to fill gaps created by the labor shortage while optimizing staff. In retail and hospitality, this will take the form of self-serve kiosks, autonomous order fulfillment, and AI-enabled drive-thrus, all freeing people up for higher-skilled roles.

Ultimately, an explosion of data requirements will offer complex challenges to firms that must manage large amounts of data.

This goes triple for many companies still struggling to fully digitize.

Although it’s hard to visualize, our reliance on technology will keep growing and the winners will be the ones who can harness these new technologies to supercharge their financial profiles.

It’s not that I am boring, but the companies leading the new stage of digital technologies are the biggest and richest of Silicon Valley, and I would rather ride the bandwagon with them than try the sexy contrarian play, especially with higher interest rates hurting start-up culture.

“We want Google to be the third half of your brain.” – Said Co-Founder of Google Sergey Brin

Mad Hedge Technology Letter

December 15, 2021

Fiat Lux

Featured Trade:

(BUY THE DIP IS BEING CHALLENGED)

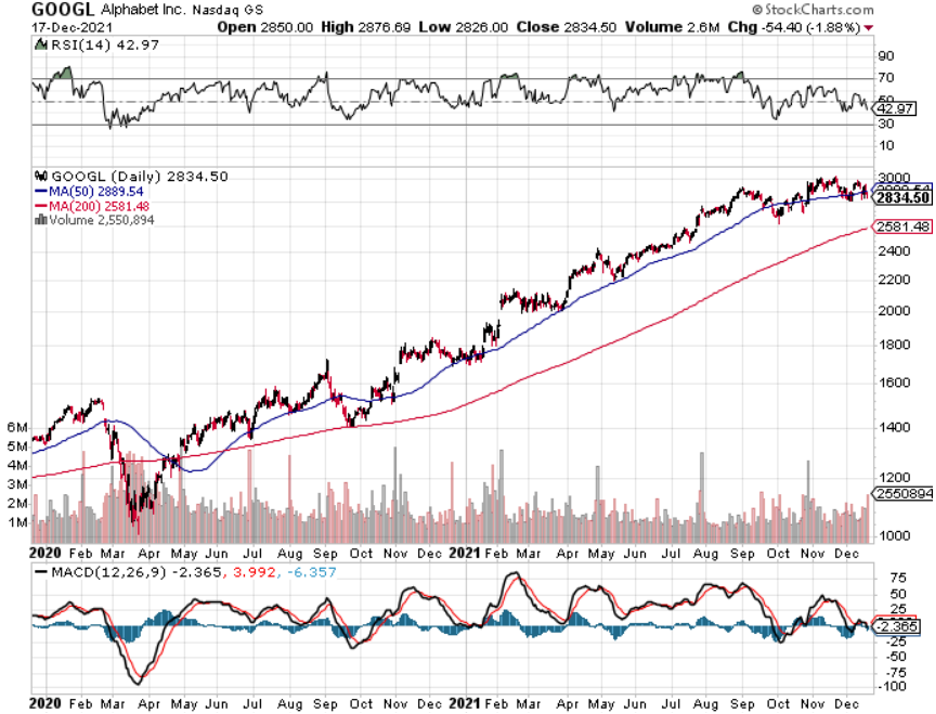

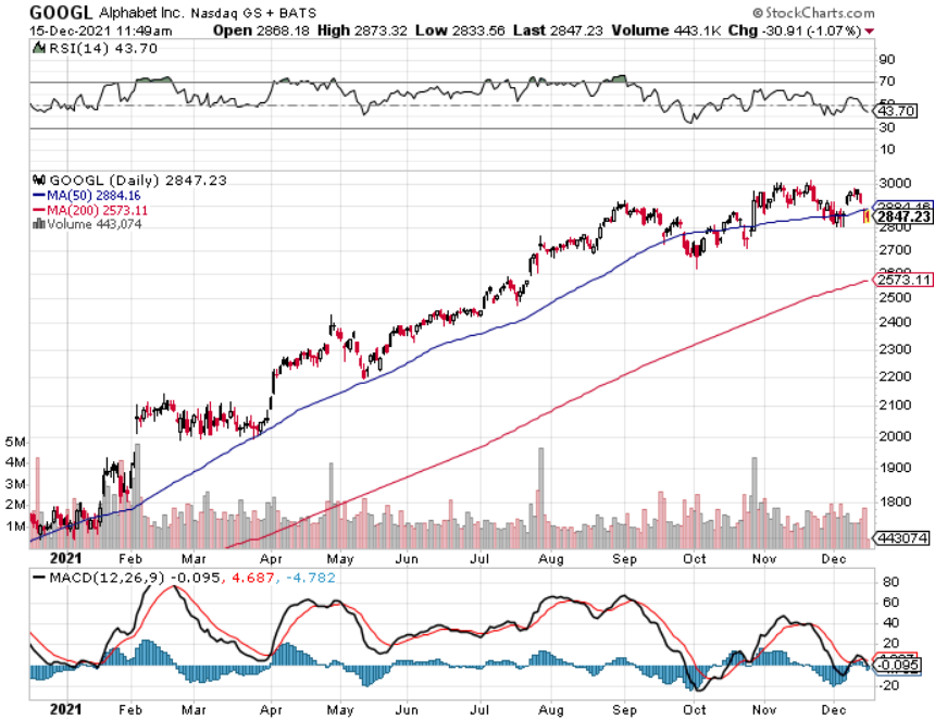

(PTON), (ROKU), (TSLA), (GOOGL), (FB), (DOCU), (TDOC)

Ominous signals have started to emerge in the short-term patterns of tech stocks over the past few weeks.

We have essentially traded a Santa Claus rally to sell the spiked peaks as inflation numbers have come in way too hot for anyone to handle.

The poor inflation numbers have triggered a cascade of algorithmic selling.

Why is this important?

These stock patterns will offer us clues to how tech stocks will react in a quickly changing backdrop where the Fed is backing away from the cheap money cauldron as fast as it can.

For over ten years now, as tech stocks have bulldozed their way to higher highs and as Apple inches closer to $2.9 trillion in market cap and on its way to $3 trillion, investors have been systematically conditioned to buy the dip.

The Fed is doing its best to recreate a new type of conditioning where the dip is not bought and that is awful for tech stock prognosticators.

This effectively means a large layer of buyers on down days will be stripped away from the tech markets.

Any idiot would understand this means that tech stocks will not go as high as they could if dip buying is conditioned.

The tech market is trying to figure out the new rules of the game and that is resulting in choppy patterns almost in whipsawing fashion.

March 2022 is the new consensus for an interest rate rise which is bad news for tech stocks because pulling forward interest rate rises coincides with higher volatility in the short term.

The Fed could make another interest rate move in the second half of 2022.

This means that anyone dallying in the speculative area of the tech market needs to pull the reigns in immediately.

Stocks like Peloton (PTON), essentially a stationary bike with a tablet pasted on the dashboard, will historically underperform in the new environment.

Another tech stock I love to bully is Pinterest (PINS), by far the worst social media platform I have ever seen, will need to face reality without the Fed punchbowl that was most likely their biggest tailwind.

Tech stocks must now stand on their two feet and that’s scary news for all tech stocks not named Tesla, Facebook, Apple, Amazon, Microsoft, and Google.

After these top 5, the quality dwindles fast and expect a slew of rapid downgrades that will throttle the non-elite software stocks.

Adobe’s stock had its second-worst day of the year on Tuesday, as analysts jumped on the higher rates bandwagon and cited high valuations.

Valuations are now “high” even if these business models are the same as they were a few days ago.

Expect poor guidance from management with earnings growth, free cash flow, and annual revenue downgrades in the pipeline.

Other notable sell-offs this week include shares of cybersecurity companies Zscaler and Cloudflare, which crumbled 7.8% and 9%, respectively.

Zscaler had been up 55% for the year, prior to Tuesday, and has an enterprise value to revenue multiple for 2022 of 39. Cloudflare was up 91% and trades at a multiple of 61.

Tech growth works both ways in which they get the benefit of the doubt in a low-rate environment and vice versa in a tightening environment.

Case in point is a company I really like Roku (ROKU) whose shares are down a hideous 230% since mid-July.

The weakness in the secondary names has been biggest secret untold in tech for quite a while and the confirmation of a tough 2022 was what happened in the first two weeks of December.

And it gets worse when looking at the shelter-at-home darlings of 2020 Teledoc (TDOC) and DocuSign (DOCU) who have been totally neglected this year.

This goes to show that every year is different and as the stock market is levered to the skies, the slightest nudge by the Fed does a lot to wobble the trajectory of tech.

Luckily, tech still has the 6 big tech stocks to rally around and even if the best of the rest must go into hibernation in 2022, we still got guys like Mark Zuckerberg, Tim Cook, Elon Musk powering us through the sludge.

“The business model of social media companies, of pure advertising, is problematic. It turns out the huge winner is low-quality content.”– Said Founder of Wikipedia Jimmy Wales

Mad Hedge Technology Letter

December 13, 2021

Fiat Lux

Featured Trade:

(THE POTENTIAL NORMALIZATION OF 2022)

(ABNB), (BKNG), (ZM)