“Invention is by its very nature disruptive. If you want to be understood at all times, then don’t do anything new.” – Said Founder and CEO of Amazon Jeff Bezos

“Invention is by its very nature disruptive. If you want to be understood at all times, then don’t do anything new.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

November 15, 2021

Fiat Lux

Featured Trade:

(THE GEM OF TRAVEL TECH ACCELERATES)

(ABNB)

Airlines are bracing for a tsunami of travelers for the upcoming Christmas season and it’s no surprise — people are itching to get out of their homes for good reason.

What the news reports don’t tell you is that many of these travelers are on their way to an Airbnb (ABNB), where they will not only stay a weekend to sample the local zeitgeist, but will make their Airbnb a work-from-home office for 4 weeks or perhaps more.

The side effects from the pandemic have indicated to companies that technologies like Zoom and DocuSign make it possible to work from home.

Airbnb makes it possible to work from any home.

And this newfound flexibility is triggering a revolution in how we travel because for the first time ever, millions of people can now travel anytime, anywhere for any length, and even live anywhere on Airbnb.

I firmly believe that this trend toward more flexibility will only accelerate.

The pandemic has suddenly untethered tens of millions of people from the need to go into an office.

In recent months, some of the world's largest companies —Procter & Gamble, Amazon, Ford, PricewaterhouseCoopers — have announced increased flexibility for employees to work remotely.

This is just the beginning as I fully expect more companies to follow their lead.

I am witnessing several trends as a result of this travel revolution.

Can you believe now that Mondays and Tuesdays are currently Airbnb’s highest growing days of the week to travel?

This is a paradigm shift in the way we think about movement and cross-border living.

Second, now people are traveling everywhere, literally everywhere. During the pandemic, over 100,000 cities have had at least one booking on Airbnb. And that includes 6,000 towns and cities that received their first booking ever on Airbnb. The third trend is people aren't just traveling on Airbnb, they're now living full time on Airbnb.

Long-term stays on Airbnb, classified as a stay up to 28 days or more, remain Airbnb’s fastest-growing category by trip length.

People are traveling with Airbnb for extended vacations, relocation, temporary housing, student housing, and many other reasons.

I’ve illustrated how there has been a massive boost in inherent demand for Airbnb units with the merging of travel and work, but the thing that gets me excited is the supply side of the equation.

Now finally, more people than ever are interested in hosting.

Airbnb ended Q3 with the most active listings ever.

Demand is driving more supply. In fact, Airbnb’s highest supply growth is in their highest-demand destinations, particularly in North America and Europe.

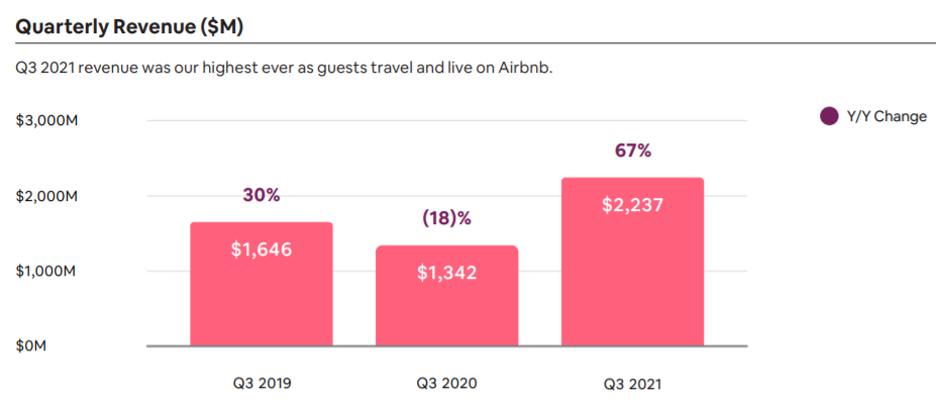

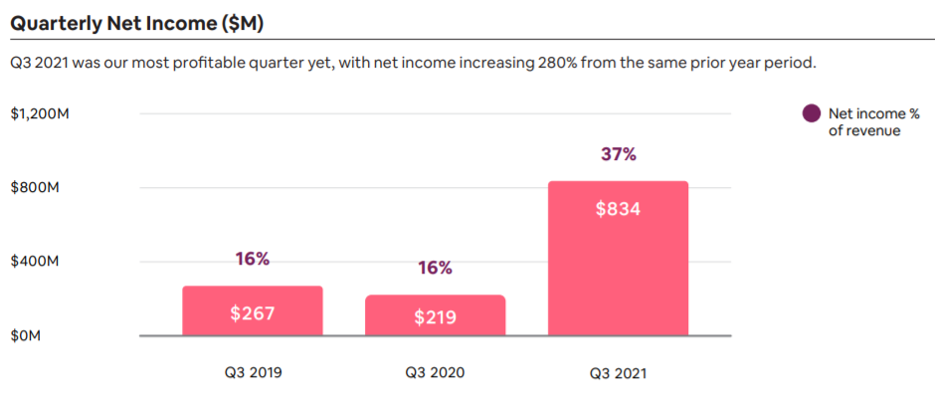

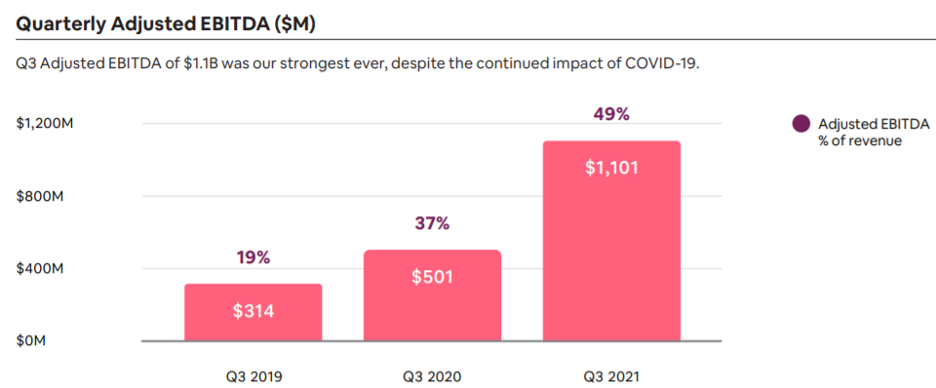

The travel rebound that began earlier this year accelerated in the third quarter resulting in Airbnb's best quarter yet recording revenue of $2.2 billion surpassing 2019 by 36%.

Net income of $834 million was the highest ever, nearly four times larger than a year ago.

Gross booking value of $11.9 billion slingshots above 2019's levels by 23%

Airbnb now has 4 million hosts, and 90% of hosts are individual meaning they specifically latched onto Airbnb’s platform to become a first-time host.

These units are only listed on Airbnb translating into Airbnb possessing the best quality of rental units and in high volume.

No other platform can lay claim to the depth of Airbnb’s business and companies like Tripadvisor.com, Expedia.com are miles behind the curve and still over-reliant on Google’s search engine to manufacture leads that translate into costly customer acquisition fees.

Airbnb now has a simple 10-step process to become a host where they’ve radically reduced the number of steps.

They’ve made it easier to host and the conversion rate for people starting to lease their space flow is up.

On no night, are Airbnb supply-constrained globally.

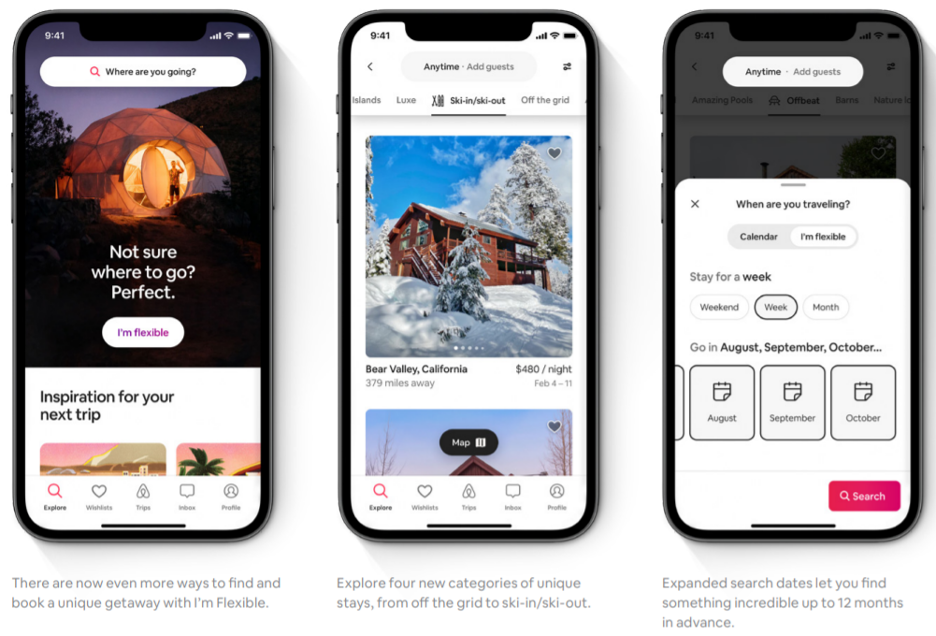

Before the pandemic, most people were narrowly stuck in their search parameters.

However, now, over 500 million searches have used flexible searches. More than 40% of searches, guests are flexible on where or when they're traveling, and as Airbnb management has become brilliant at predicting the onslaught of demand before it comes to fruition, they have also been stellar at adding the corresponding supply at the right moment in a preemptive fashion.

Airbnb has really moved the profitability needle and future quarters will see a hockey stick-shaped effect on revenue and EPS.

Any pullback should be bought and, to be honest, Airbnb really has hit the sweet spot as the world’s digital housing agent.

I am highly bullish on Airbnb for the year 2022 and beyond.

“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” – Said Harvard economist John Kenneth Galbraith

Mad Hedge Technology Letter

November 12, 2021

Fiat Lux

Featured Trade:

(PEAK STREAMING GROWTH ISN’T THE END OF STREAMING)

(DIS), (NFLX), (AMZN)

Peak streaming — that’s what the indicators are telling us.

It’s been a good run — lots of money made so far.

The streaming industry is resting after the pandemic pulled revenue forward a few years.

It won’t be as easy now, as the maturity of the industry means that it becomes a war inside the war, instead of the tide-lifts-all-boats type of growth.

The latter is what everyone hopes, but doesn’t always get.

The world’s largest entertainment company, Disney, posted a significant slowdown in subscriber sign-ups at its flagship streaming service in the most recent quarter.

Disney+ added only two million subscribers last quarter bringing its total to 118.1 million.

Analysts had expected this quarter’s total to come to 125.3 million. During the previous quarter, Disney+ had added more than 12 million new subscribers.

First, the follow-through from consumers just wanting to experience outside and the services attached to them ring true.

The price hikes are also another net negative, as it makes consumers less enthused about signing up.

This had to be expected and many of these streaming companies would honestly admit that they couldn’t continue the pandemic era performance.

A reversion to the mean is not the end of streaming and Disney’s streaming services.

It is still on track to reach previous guidance of between 230 million and 260 million paid Disney+ subscribers globally by the end of fiscal 2024.

Dig deeper into the streaming data and it shows that customers in India didn’t sign up because of a delay of Indian Premier League cricket games that were to air on the service.

Another indicator of the pivot to outside business is the Disney theme park revenue climbing 99%.

The trend towards outdoor activities means a slew of cancellations of the monthly subscriptions.

Netflix was the rare streaming company that bucked the trend.

Netflix streaming service added 4.4 million subscribers—or about a million more than it had forecast—on the strength of new popular shows like “Squid Game.”

Moving forward, the bar rises quite a bit for the quality of content.

Viewers are demanding more or they are riding Space Mountain in Anaheim.

Streaming companies won’t be able to pedal out mediocre shows and movies, and secondly, there is no patience for customers as the number of streaming options has multiplied.

The deeper underbelly shows us that the general trend of linear TV cancellations and streaming signups appears to be continuing even if the rate of signups is slowing.

Disney, WarnerMedia, and AMC Networks all reaffirmed previous full-year and future year forecasts. And while pandemic gains may have slowed, production slowdowns and shutdowns have also ended, which will lead to a surge of new content for all of the streaming services.

Disney investors will be zeroed in to see if the company can pump out some blockbusters, but a glut of content might mean not enough eyeballs to digest these blockbusters.

Coronavirus-related production delays continue to disrupt its pipeline of content delivery.

Disney subscriber growth could ramp back up in the latter half of 2022 when they have better titles coming to market.

Another issue for Disney is if they are willing to produce more adult content and veer away from the younger cohort they are used to entertaining.

I don’t mean X rated, but the 25-44 aged bunch, everyone is sick of the superhero movies.

When it comes to attracting subscribers to Disney+, the company in November and December will be relying on a Beatles documentary, “The Beatles: Get Back,” additional Marvel Studios and Lucasfilm Ltd. shows and films that include a new “Home Alone” feature.

In April, Jeff Bezos said more than 175 million Amazon Prime members had streamed shows and movies in the past year.

Beyond the big three — Netflix, Disney+, and Amazon Prime — things get cloudier.

In July, NBCUniversal’s Peacock reported 54 million net new subscribers and more than 20 million monthly active accounts.

Other players with potentially strong platforms include WarnerMedia’s HBO Max, with a reported 69.4 million global subscribers, and Apple TV+, which is rumored to have about 20 million U.S. subscribers.

The major streaming competitors are also actively expanding their footprint abroad to acquire more growth, but the issue I have there is that the average revenue per user (ARPU) is nothing close to what it is in North America.

Although oversees revenue could provide a little bump to earnings, it won’t recreate their earnings composition.

Which leads me to a broader take on tech, it’s slowing down because we have been in the same cycle which was essentially initiated by the smartphone, the cloud, 3G super apps, and high-speed internet.

Those super levers are showing exhaustion.

It’s not a coincidence that Facebook’s Mark Zuckerberg was desperately trotting out his vision for the Metaverse and Apple removing personal data tracking from its ecosystem.

These are late cycle signs that shouldn’t be missed.

Big tech has become a great deal more mercantilist during the latter half of this bull market, yet we aren’t at the point of cannibalization, but I do envision that moment 5-7 years out from now.

Until then, high quality tech will grind higher while slowly raising their monthly prices, and the low-quality tech products will fall by the wayside because they lack the killer content.

“I know that you must be passionate, unreasonable, and a little bit crazy to follow your own ideas and do things differently.” – Said CEO and Founder of Salesforce Marc Benioff

Mad Hedge Technology Letter

November 10, 2021

Fiat Lux

Featured Trade:

(DATA ANALYTICS AT ITS FINEST)

(PLTR)

Investors shouldn’t stress too much about the drop in Palantir stock.

It’s still a great company that is on pace to do what it promised — achieve annual revenue growth of 30% or more through 2025.

In fact, they will easily surpass those projections, and any of these mini pullbacks that we are seeing now is just a matter of not fulfilling sky-high expectations and coming in a tad below that.

I can accept that and so should you.

Why is this data analytics company so great?

It is the connective tissue that connects analytics to operational systems which leads to winner business decisions.

Such architecture offers enterprises with action APIs that allow first model and simulate, and second, orchestrate and execute complex cross-functional transactions.

As the health crisis limited visibility and indicators, many started to trust the power of Palantir’s platforms and installed the technical infrastructure, to translate that into coordinated, orchestrated actions in the operations of their business.

Credit should go to Palantir’s developers who created a secret sauce to supercharge earlier-stage companies, enabling them to deliver a central operating system for their data and to scale rapidly from day zero.

These companies, they're not just managing their data and their operations, they are wielding them to blitz, scale, and conquer at a devastating rate.

Palantir’s clients originate from a diverse set of industries and continue to partner with innovative companies across industries such as automotive, biotech, healthcare, media, and the government.

Now, they are generating major product innovation that extends the openness and flexibility of their infrastructure for developers calling it Operational APIs or OPIs for short.

This liberates the ontology to serve as a nervous system, the cardiovascular system of the enterprise as a unified action and orchestration layer.

This manifests itself in a way that inventory can be allocated, production can be scheduled, orders can be fulfilled. To accomplish these deceptively simple actions requires communication with potentially tens of source systems transactionally.

Palantir allows you to orchestrate complex cross-system decisions to win and turn market disruption into competitive glory.

For example, a large industry company is unlocking value by integrating Microsoft Power apps with the Palantir Foundry platform. This powers workflows and writing data back to external operational and transactional systems

State defense contracts have been hyper-lucrative to PLTR.

PLTR has demonstrated its usefulness in the production of the A320 of RAM pickup trucks, auto parts, PPE, and tractors. PLTR can leverage its technology so customers can do it better, faster, and cheaper.

It’s a win-win for everyone.

And the defense industrial base is seeing that it can have the same impact on the production of fighter jets, naval ships, and land vehicles.

Lastly, their dealing in healthcare is shooting through the roof with cornerstone partnerships with the NHS, MD Anderson Cancer Center, 70 academic medical centers through the NIH's N3C, the Department of Veteran Affairs, and even more regional US providers means that PLTR is helping to manage over 300 million patient lives and growing.

Complex clinical care continues to be the recipient of cutting-edge products and continued innovation.

It’s not surprising that PLTR’s US commercial revenue growth accelerated once again to 103% year over year and this flavor of business offers the longest runway for PLTR to grow.

They more than doubled their commercial customer count.

Palantir management guided us to 34% growth in government revenue during the third quarter, while this segment was up 66% in the second quarter, but I believe this is highly misunderstood.

Just the nature of working with the government, the bureaucracy, and the single entity nature of it, deals aren’t going to be flying in left and right.

There is a processional nature to working with the US government because its such a monolith.

The more salient story here is the in-roads of the commercial business which will turn into its core identity.

The commercial business will be the x-factor driving PLTR into surpassing its revenue promises, and investors will acknowledge that as commercial revenue begins to overpower the defense contracts.

Revenue for the full year is expected to be about $1.53 billion or 40% year-over-year growth which conspicuously gets over any bar that tech growth companies are expected to jump over.

“Stock market bubbles don't grow out of thin air. They have a solid basis in reality, but reality as distorted by a misconception.” – Said Hungarian American billionaire investor George Soros