Mad Hedge Technology Letter

November 8, 2021

Fiat Lux

Featured Trade:

(HOW SOFTBANK GOT GLOBALIZATION ALL WRONG)

(SFTBY), (DIDI), (BABA), (CPANG)

Mad Hedge Technology Letter

November 8, 2021

Fiat Lux

Featured Trade:

(HOW SOFTBANK GOT GLOBALIZATION ALL WRONG)

(SFTBY), (DIDI), (BABA), (CPANG)

Softbank’s Vision Fund, a technology-biased venture capitalist fund, is basically a leveraged massive bet on synchronized bullish behavior on the future earnings of global tech companies.

It assumes that technology is one of the critical underpinnings to global business and it's more or less a wager on an increased rate of harmonic globalization.

I get what they are trying to do, but in 2021, globalization is far from harmonic, and there are many in the camp that the world is wrought by a current phase of deglobalization.

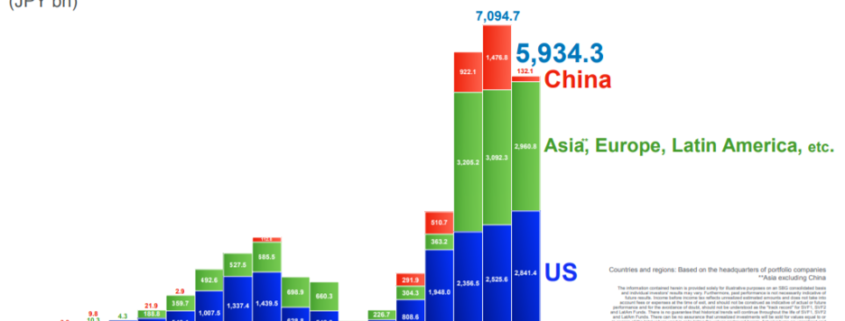

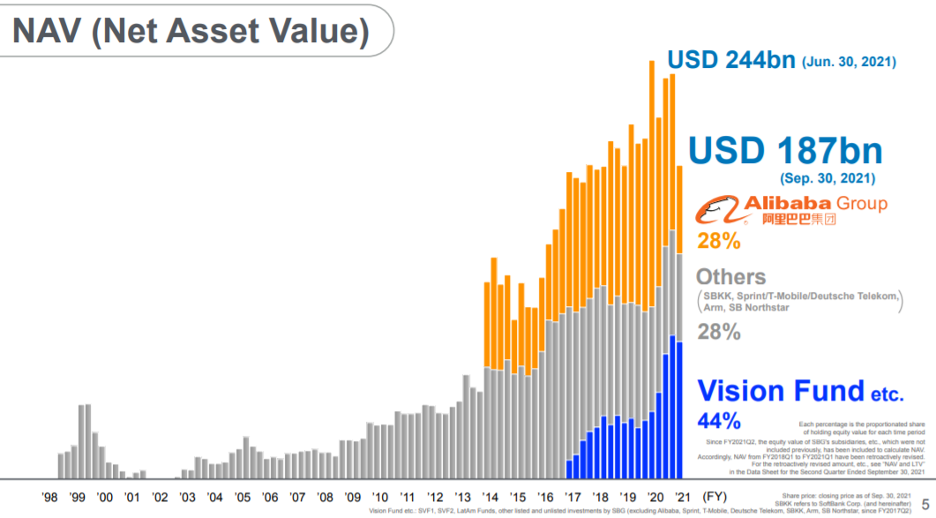

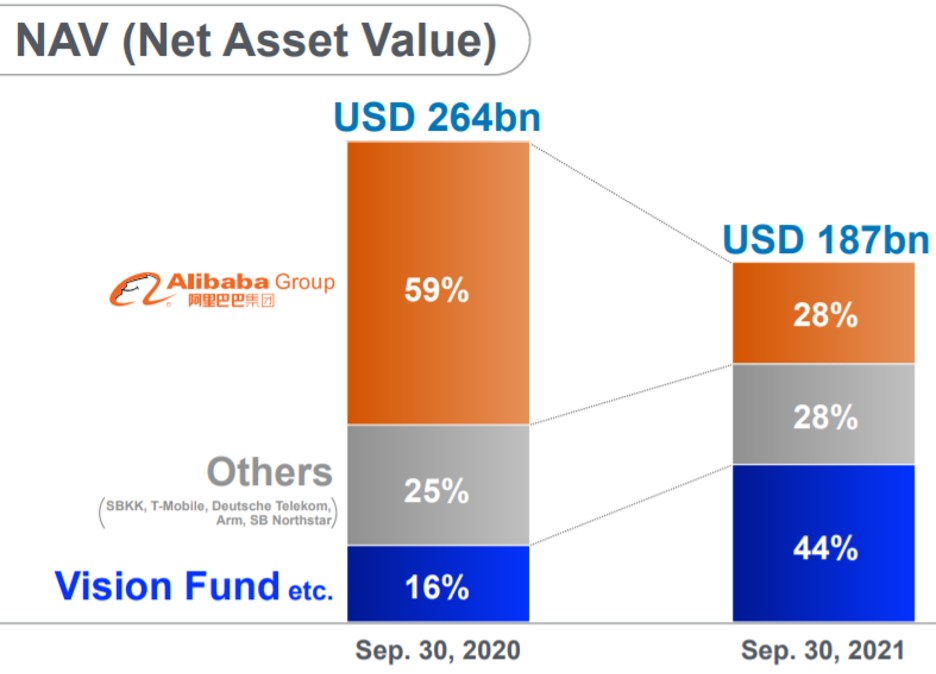

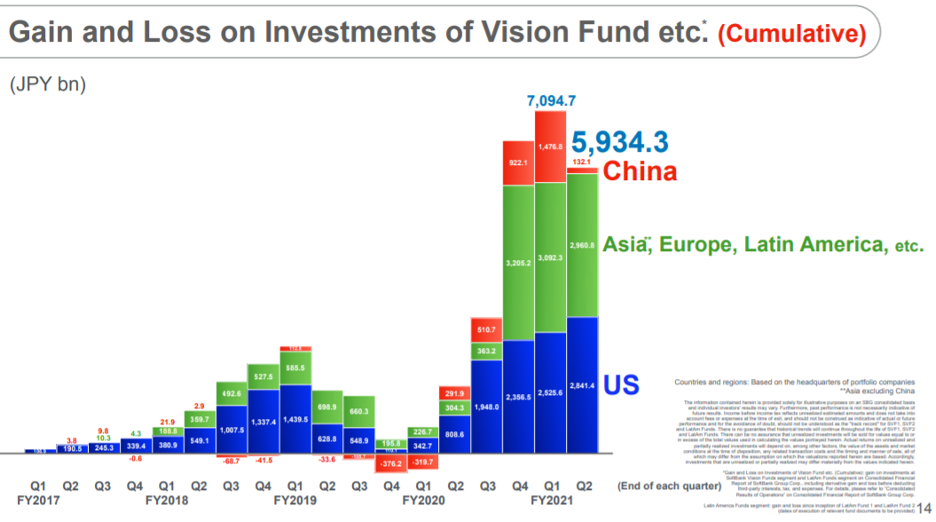

This past quarter, Softbank presided over a precipitous drop in the Net Asset Value of their technology investments from $244 billion to $187 billion.

The -24.6% return and the pain from it were mainly induced from Softbank’s vast array of Chinese investments specifically dreadful performance from its bellwether leader Alibaba (BABA) whose stock has halved since the crackdown started.

CEO of Softbank Masayoshi Son, an ethnic Korean with a Japanese passport, described its current predicament as being “right in the middle of a storm.”

The problem with that is not being in a storm per se, but the timeline into transitioning into sunnier climate because just 1-2 quarters out from now, prospects appear bleak.

If one might remember, DiDi Global Inc. (DIDI), the Chinese ride-sharing platform, was the big shebang going public at a valuation that pegged the company at $68 billion.

Since then, not much has gone right as it was later found out that (DIDI) went public without the tacit approval of the Chinese Communist Party.

Falling out with the good graces of their overlords has meant a halving of the stock and Softbank has taken a loss of $6.1 billion on DiDi.

Even worse for the firm, there appears to be no savior or “next DiDi” IPO to save their Net Asset Value in the upcoming quarters.

That means we could be staring at the high-water mark which occurred 2 quarters ago.

Thank God for the outperformance in Europe and the United States that, in effect, accomplished some damage control for the bottom line.

And their recent short-term track record has been overwhelmingly poor.

Let’s take a glimpse into the other investments that have been chop blocked at the knees.

The losses keep rolling off the tongue with Uber-like trucking startup Full Truck Alliance Co. down $1.2 billion.

KE Holdings Inc., which runs the Beike online property service, lost $2.2 billion of value — the stock is down more than 70% from its peak and is trading below the IPO price.

And the failings weren’t just in China, take a stock that I have extensively bashed on — the biggest ecommerce company in South Kora — Coupang (CPANG).

Their poor past quarter’s performance meant that Softbank booked a quarter performance of a horrific -$6.7 billion.

I told readers to stay away from this one not because it is a bad company.

It was crystal clear in the underlying data that its business was saturated in Seoul, and there are no other big cities in South Korea, and I couldn’t see where the next phase of incremental growth would come from.

The idea was to grow abroad but everywhere else in Asia has been monopolized by local or brand-named ecommerce companies.

That was the bad news, and the silver lining is that ex-China, particularly the United States, they have been doing well and are highly profitable.

Slippage from this Vision Fund is quite notorious, from its misallocation of funds of shared office space company WeWork to overpaying for many other companies with a vanilla idea that technology will overcome any obstacle.

I would say that at a management level, not a lot is well thought out at Softbank.

I would like to remind readers that many of these new China investments by Softbank have just plain out ignored the geopolitical tensions.

They have nobody to blame but themselves because they certainly had time to divest from China and take profits which would have been the right move to do at that time.

Softbank’s parent company’s stock is basically half of what it was in March 2020 thanks to China and the Vision Fund will need to rely on its ex-China investments to pull itself out of this “storm.”

Another big plus is that the China losses are unrealized, but China has offered zero indication that their monumental crackdown on private business is over, and no amount of kowtowing will sway them from their lofty perch.

This could just be the start of their reign of terror over private business and that’s a scary thought right there.

Honestly, I opt for the more conservative stance of never buying Chinese stocks.

Why invest in Chinese tech when United States tech is so much better?

Not enough growth for you?

Then use options.

Softbank should and could have just poured all their investments into Silicon Valley, or just one company like Google, or even the digital gold of Bitcoin.

Good thing there is no ETF that tracks the performance of Softbank!

Invest at your own peril.

“Almost everything is like a machine.” – Said Hedge fund Manager Ray Dalio

Mad Hedge Technology Letter

November 5, 2021

Fiat Lux

Featured Trade:

(LET THE DUST SETTLE FOR THIS CHIP STOCK)

(QRVO)

This is not an uncertainty at the end of the tunnel turning out to be a train-like situation with chip company Qorvo, Inc. (QRVO).

Hardly so.

The 17% sequential decline QRVO is guiding for their mobile business in December isn’t something investors will dance in the streets about.

The chip sector is an anomaly because of the boom-bust nature of the semiconductor cycle.

Here at the Mad Hedge Technology Letter, we find it more conducive to trade in annuity-like software revenue where CFOs have a better handle on predicted cash flow and state of the balance sheet.

Qorvo, Inc. (QRVO) decreased its December revenue forecast by about $150 million, and about $135 million of that was in mobile chips.

The balance of the decrease was also in Infrastructure and Defense Products (IDP).

Of the $135 million roughly in mobile, QRVO has been wrought by supply constraints, specifically meaning their suppliers not delivering supply for them.

Sucks, right?

The result is QRVOs customers not receiving their allotment of chipsets, thus not able to build their product and use QRVOs products, a type of vicious cycle of being empty pocketed for everyone.

The earnings’ quarter for Qorvo epitomizes the 2021 economy and that’s not only for semiconductor chips — the master word being supply constraints.

The demand part of the equation has also been affected particularly in parts of Asia but is secondary to the supply headwinds.

I am disappointed with the December guide, but it’s not the death of QRVO as I see it.

They need to reinforce a commitment to keep the product channel healthy and give a guide that most accurately describes the supply/demand fronts.

It’s never just cut and dry, but admittedly, visibility is cloudy now and that must be reflected in the management rhetoric and prognosis.

Generally speaking, Qorvo has a great business with best-of-breed products, and we shouldn’t lose sight of that.

Regarding the supply environment, it’s been tough sledding for 1.5 years, almost two years now so it’s not just a 1-day hangover.

The supply environment deteriorated, but inventories are still healthy.

Trying to sort out the internal calculus, I have full faith in QRVO to get their shop in order and meaningfully cast a better light in the March quarter.

I feel that is right around the corner.

The silver lining is that QRVO’s gross margin outlook is intact around 52%.

Opex is in control, and they’re investing in the future of the business.

These investments entail both the traditional parts of the business and newer parts of the business.

And in the end, EPS continuity is hardly affected so we can still count on the same type of elevated profitability which is a hallmark of a good company.

Most chip companies aren’t like crappy loss-making Uber and firms of that ilk.

Absorbing a bit of a correction is nothing to freak out about, but I would say it's the right thing for them to do and will curry investment trust over the long haul.

I can confidently say that I feel great about QRVO’s strategic position as we creep closer to 2022.

They wield premium technology and products, serving attractive end markets growing double-digits, and I fully expect them to outperform next year.

Operations are like a well-oiled machine with sustained margins over 52%, expanding operating margins, and the underlying strength of the company is nothing to diminish.

Considering the concrete evidence, this will be a great semiconductor firm to buy on the dip once the stock settles down from its cringeworthy sell-off.

Granted, the 22% drop from its peak is precipitous, but these smaller chip companies have heightened embedded volatility because of their diminutive size.

That’s not to say they are bad.

The stock has still more than doubled since early 2020 and once the stock levels off, there will be a massive tranche of buyers bidding this chip company back up which should see the stock blast past $200 and beyond.

This could happen by the back half of 2022 and by that time you’ll be glad you bought at discount levels.

“The American dream, what we were taught was, grow up, own a car, own a house. I think that dream's completely changing. We were taught to keep up with the Joneses. Now we're sharing with the Joneses.” – Said CEO of Airbnb Brian Chesky

Mad Hedge Technology Letter

November 3, 2021

Fiat Lux

Featured Trade:

(AVOID THIS TECH STOCK)

(Z)

Zillow iBuying division, Zillow Offers, registered a meager average gross loss per home sold of $80,771.

This division did so bad that they are closing it down translating into a culling of 25% of the workforce.

Zillow's co-founder and CEO Rich Barton is to blame for this disastrous attempt at going from a digital ad company on a real estate platform to a full-blown house flipping company.

This idea probably looked good on paper at first (though I'm not sure how) but executing it was hell.

It seemed that nobody even considered the carrying costs, such as HOA fees, local property taxes, utilities, home insurance, appraisal costs that added up to most of the gross loss per house.

And the fact that competition to buy housing lately has resulted in buyers offering well above the listed price should have sent a warning signal to stay out of this.

It is hard to understand how they would ever make a profit while employing 2,000 full-time iBuying employees to carry this out.

Even if profit could be possible, it would be minimal at best.

Zillow partially blamed the algorithms for the lack of success, but I would lean towards saying this was a hopeless endeavor from the start.

The failure has led to a total write-down of more than $540 million and the company said it was halting new purchases of homes, so at least they got that right.

In the earnings report, Zillow Offers purchased homes during the last quarter for prices higher than it believes it can sell them.

It also could be a sign for a short-term post-pandemic market top in housing.

Flipping houses doesn’t work when buying at the market peak and Zillow, who possesses the most real estate data out of anyone, should have known that.

Yes, housing prices are unpredictable, but this is not a type of business that can scale.

Flipping houses also has to do with finding anomalies, bargains, or renovating fixer-uppers which are hard to do now because supply chain disruptions and the labor shortage are causing a backlog in home repairment services.

Instead of going so far off the path from their core business, they should have just bought Bitcoin in 2018 or even big tech and sat on the couch and watched it appreciate.

We all try to minimize our cost of doing business and Zillow chose to shoulder outsized risk in an unscalable business.

Zillow Offers tried to offer homeowners a fair market cash offer; or at least that was the plan.

The idea was to grow that service and offer it to a wider audience. But because of the price forecasting volatility, the company had to reconsider and management probably realized they needed a lot more capital which would create massive problems in the quarter-to-quarter balance sheet.

Remember selling ads is a remarkably predictable revenue stream for these platforms.

Much of their revenue are annuity-like.

The competition in the market amid other iBuyers meant that most proposals Zillow Offers made to homeowners were rejected.

Only 10% of offers from Zillow were accepted because the housing market has largely been irrational the past 18 months.

I commend Zillow for cutting their losses, and they still need to work through their backlog of already purchased homes which will surely result in a higher than $80,000 per unit loss.

Zillow ended the quarter with 9,790 homes in inventory and 8,172 homes under contract that it will still purchase, which it will sell over the next six months or at least try to.

The company should do what it does best — sell ads.

Consequently, Zillow’s stock has been battered peaking at $200 this February and now at $70.

I personally wouldn’t touch Zillow stock with a 10-foot pole, and would be suspicious of management if they announce some grand plan to regain momentum.

Management needs wholesale changes to get back to its core competencies.

It’s a crime that it took 3 years for Zillow to figure out this was a cruddy direction.

"Life is not fair; get used to it." said the Co-Founder of Microsoft Bill Gates.

Mad Hedge Technology Letter

November 1, 2021

Fiat Lux

Featured Trade:

(A FINE-TUNED MACHINE)

(MSFT)