“It's not about working harder; it's about working the system.” – Said Co-founder and CEO of the American social media company Snap Evan Spiegel

“It's not about working harder; it's about working the system.” – Said Co-founder and CEO of the American social media company Snap Evan Spiegel

Mad Hedge Technology Letter

September 27, 2021

Fiat Lux

Featured Trade:

(A SHORTENED RUNWAY FOR SILICON VALLEY)

(AAPL), (FB), (WIC), (SME)

I’m not going to go so far as to claim the Silicon Valley tech story is over — that’s too premature.

But—and a very big but—I will say that the runway has been significantly shortened for the aircraft taking off.

In an everchanging zig-zagging tech climate — it’s my job to take the pulse of it and correspond it to the reader.

I would characterize myself as concerned with the latest developments in technology, and I specifically mean for those business models that many of you have poured your hard earned cash into.

I have gone on record saying that Silicon Valley suffers from a lack of imagination and the gravitas shortage in which to sort this out is starting to stick out like a sore thumb.

What we have is what we have.

Dynastic, hegemonic tech companies who, instead of taking the reins and helping the industry develop in terms of paradigm shifts, have chosen the way of incremental development to suck the marrow dry via the capitalistic model of short-term profits that manifest themselves in higher stock prices.

I have no problem with that at any level—higher stock prices have given my readers a chance to enrich themselves with generational wealth.

And yes, I agree with you, investing for paradigm shifts isn’t cheap, and who wants to be on the hook for this bill anyway when this gravy train isn’t over yet?

Recent signals are emblematic of the narrowing paths to profits for tech companies; they are increasingly required to pull off 4th quarter heroics to get ahead, and we are starting to rub up against the extreme limits.

Exhibit A — Facebook.

The company has confronted sharp criticism from lawmakers and users for its plan to develop an Instagram for kids and said it was pausing work on the project.

Facebook said it will re-evaluate the project at a later date as a damning expose by the Wall Street Journal.

This latest app was intended for children aged 10 to 12.

One internal Facebook presentation said that among teens who reported suicidal thoughts, 13% of British users and 6% of American users traced the issue to Instagram.

Remember that Facebook bought Instagram because Facebook, its flagship platform, was dropping users left and right.

Instagram was the savior.

I would argue that Facebook would be a $200 stock without this asset.

The next question investors should ask is, if Facebook “kids” was going to be the next growth sub-sector for Facebook, what does it do now?

It’s an uncomfortable question for Facebook shareholders and rightly so.

Again, this screams lack of innovation to me—shareholders cannot just tolerate Instagram for 8–10-year-olds, then Instagram for 6–8-year-olds, only to be followed up by the Instagram for 4-6-year-olds.

Crazy as it sounds, that was the path Facebook intended to go down.

Now, it’s time for a reset while their metaverse project isn’t ready.

Silicon Valley's Exhibit B — Apple.

Apple's earnings for Greater China in Q2 2021 were up 87.5% from this time last year, to $17.7 billion.

During its latest earnings call, Apple has announced dramatically increased revenues from Greater China for the three months ending March 2021. At 87.5% year-on-year, the percentage rise exceeds all other territories bar the rest of Asia Pacific.

On a standalone basis, higher revenue is great for the stock, and here at the Mad Hedge Tech Letter, we love higher tech shares.

The problem is that Apple’s biggest growth driver is China revenue.

I am sure that many readers have started to notice the calm before the storm in China.

If it wasn’t the real estate problems there, then sure, that’s a different industry but worrying.

However, Chairman of China Xi Ji Ping has gone on an aggressive defanging of the Chinese tech sector.

From imprisoning executives to massive fines — he is really stirring up the pot.

Apple readers also must ask themselves — how long will Apple be immune to the whims of Chairman Xi?

The answer is that it’s increasingly starting to seem like not long.

Just this last weekend, some of the biggest names in China’s tech industry made an appearance at the World Internet Conference (WIC) in Wuzhen to pledge support for the country’s “common prosperity” and small and medium-sized enterprises (SMEs) nearly a year after the government began an extensive crackdown on the sector.

There’s a legitimate risk that Apple’s immunity pass won’t be valid for much longer.

Remind yourself that Apple just came out with iPhone 13 and is on the path to make iPhone 14, 15, 16, and up to 100 because they make good money doing it.

Also remind yourself that Android phones are now just as good for half the price so in terms of relative competition, if they didn’t have a loyal base, people might not buy iPhones anymore.

Reality sucks, doesn’t it?

The defanging of Silicon Valley is a when and not if proposition; they will be forced to bet on the next paradigm shift and if they choose correctly, they will also be the winner of it so they might as well enlarge the budget for it.

“When I was first getting started, I told myself that there's two people in the world when it came to technology: There's the people who created it and there's everybody else.” – Said Tech Investor and Owner of an NBA Franchise Mark Cuban

Mad Hedge Technology Letter

September 24, 2021

Fiat Lux

Featured Trade:

(NOT THE SEXIEST TECH STOCK — BUT HIGHLY RELIABLE)

(EBAY)

Readers of this tech letter know that I have been wildly bullish on ecommerce company eBay (EBAY) precisely when vulture hedge fund Elliot Management acquired it in January 2019.

Alongside fellow activist fund Starboard Value LP, Elliott pressured eBay to revamp its operations. At their urging, the company pledged to sell off its Stubhub ticketing and its internationally-focused classifieds businesses, and replace its CEO.

My recommendation was spot on, and shares are up 220% since Elliot forced massive changes to first, the crappy management, and second, to the business model.

Luckily, those changes have staying power as Elliot exited their investment at the end of last year at then — all-time highs.

Elliot’s legacy will inherently be one of turning around eBay into what it is now, and I write to you today to say that eBay is coming into its own even after Elliot’s exit.

It’s not only about discontinued legacy tactics that led to low value, infrequent or one-and-done buyers.

Such an unsustainable strategy makes you want to tear your hair out.

But now, a fledgling buyer base is starting to evolve based on a re-optimized strategy.

These high-volume buyers are growing compared to a year ago and their spend on eBay is growing even faster.

This higher-quality mix of buyers increases value for sellers and will lead to improved health of eBay’s ecosystem over the long term.

Payments and Advertising initiatives continue to deliver a simpler product experience and meaningful benefits for sellers, buyers, and shareholders.

Managed Payments is now live in every market globally, and the transition is progressing faster than expected.

eBay management is now driven via a multiyear journey to become the best global marketplace for sellers and buyers, through a tech-led reimagination.

Their priorities are to grow the core, become the platform of choice for sellers, and cultivate life-long trusted relationships with buyers, by turning them into enthusiasts.

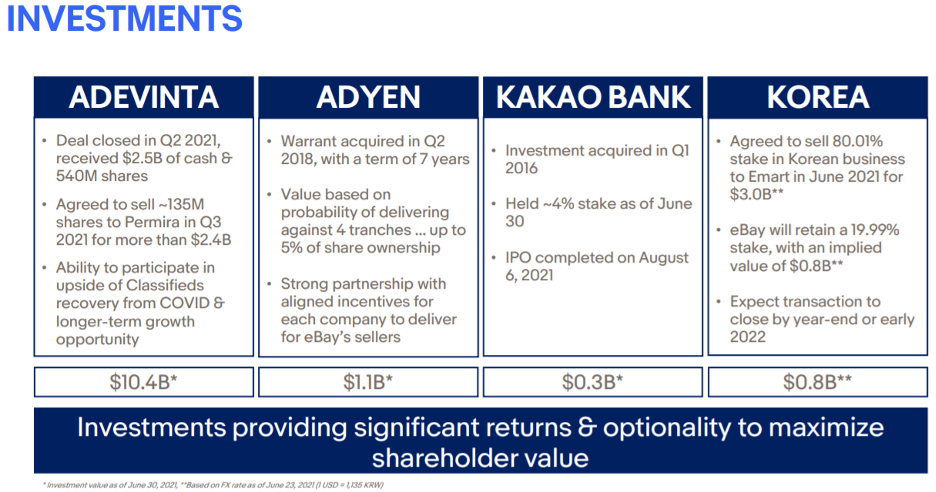

They finally completed the transition of eBay's Classified business, which was initiated by Elliot, to Adevinta.

This deal was originally valued at approximately $9.2 billion, but a closing in June had appreciated to $13.3 billion.

In June, eBay announced the sale of over 80% of their Korean business to Emart for approximately $3 billion, bringing together two leading e-commerce and retail companies that can unlock significant potential in Korea.

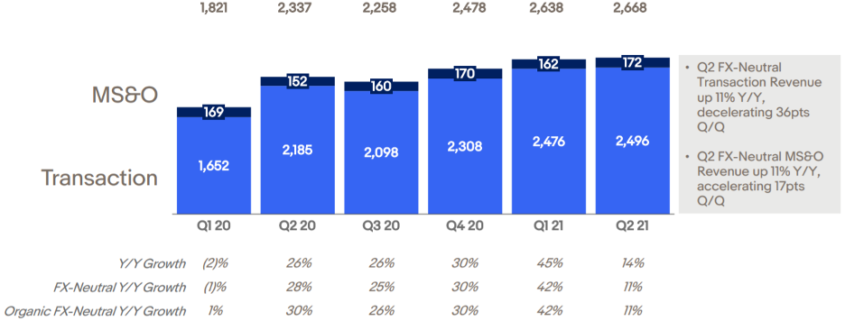

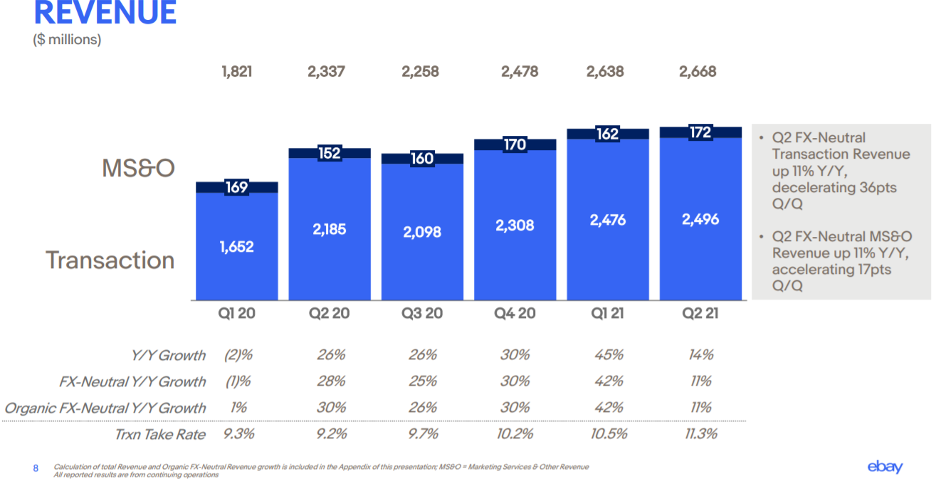

Revenue grew 11% driven by the acceleration in the Payments migration and advertising growth.

Luxury watches are also sustaining double-digit growth. Improved buyer trust is leading to strong cross-category shopping behavior similar to what eBay has experienced in sneakers. The next luxury category eBay is focused on is handbags.

They also expanded the My Garage feature to Canada, Italy, France, and Spain, which allows buyers to store their vehicle data, leading to a more tailored shopping experience. eBay plans to launch more technology-driven innovations in this category later this year to further build on their success.

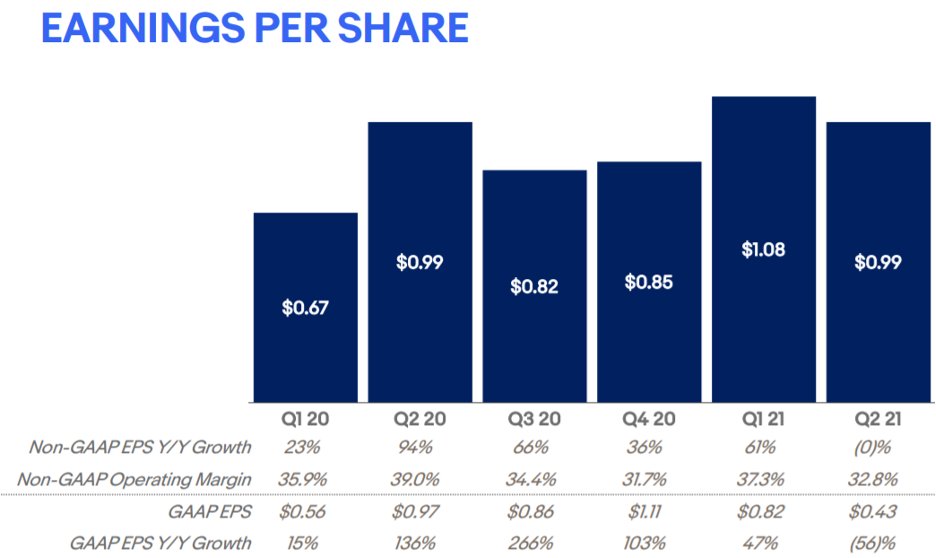

To sum it up, eBay delivered strong short-term results, ahead of expectations, while transforming the company for the longer term.

Obviously, the moves they are making at the top level to create over $20 billion of shareholder value give the company capital to intensely focus on growing the core.

Now the focus is laser-like to grow that central engine of ecommerce and the Covid bump forced a realization to the executive level here that it’s a no-brainer to double down at the core when the revenue runway is there.

To migrate into something else while the green, lush vegetation is right there for them to harvest would be nothing more than lunacy.

Management even felt confident enough to spin the cash from the Korean, Classified, and StubHub deals into an increased 2021 share buyback program to $5 billion for an initial $2 billion.

Granted that eBay isn’t a YOLO growth company to throw money at and its implied Q2 guidance between $2.58 billion and $2.63 billion of revenue growing 8% to 10% isn’t going to make you do cartwheels in the street, nor is the 11% Q2 revenue expansion, but this is a solid tech bet whose stock will grind up.

Management is also on a run of profitable deals that are meaningfully segueing into higher share buybacks.

Sometimes readers don’t need to focus on the sexiest tech stock, and just go with old reliable.

“The technology keeps moving forward, which makes it easier for the artists to tell their stories and paint the pictures they want.” – Said American Filmmaker George Lucas

Mad Hedge Technology Letter

September 22, 2021

Fiat Lux

Featured Trade:

(SHOP UNTIL YOU DROP)

(SHOP), (ZM), (TDOC), (TIKTOK)

E-commerce is now happening absolutely everywhere except the pipes in your house, and Shopify’s (SHOP) plan is to ensure that merchants using Shopify can sell pretty much everywhere.

That’s just how it is these days.

The internet town squares of modern day are social media and that corresponds to everywhere as people take social media to the streets in droves.

And so, it's important that wherever consumers could be potentially looking to purchase that Shopify merchants continue to show up there.

And from a merchant perspective, that it all neatly feeds back into a centralized back office where they can run their business.

So whether it's Google Search or it's on Instagram or it's on all the other channel integrations Spotify has, that is essential.

Now, again, over time, you are going to see more of these surfaces show up where commerce is happening, and Shopify is also integrating there to make sure that merchants can access those customers.

It’s SHOP’s job to stay one step ahead and that’s what they are exactly doing.

And of course, as more of those services come to life, that increases the complexity of commerce and running a business, a modern-day business, and that also increased the value Shopify provides to their customers.

Shopify and its platform do internet selling at a world-class level.

And yes, there are sometimes where it's faster, better, and more effective for them to partner with another technology company. They’ve developed a solid reputation for being a company that builds incredible software and particularly are renowned for having trustful partners.

But there are other times where SPOT needs to build it themselves because it's just mission-critical, and I have full confidence in them that they can actually deliver the best product on the planet.

This story and numbers are backed up by the latest short-term performance showing that SHOP is turning into an e-commerce juggernaut.

The latest earnings showed that year-over-year GMV growth in the rest of the world actually outpaced North America in Q2 2021.

We are seeing more international merchants that are joining and are succeeding on Shopify.

And fortunately, SHOP is stepping up its growth marketing, sales, and support efforts in places like Brazil and all over the world.

It isn't necessarily any particular focus on Brazil per se, but there are merchants around the world who are looking for a retail operating system and Shopify certainly is the priority.

Revenue in the second quarter was up 57% year over year to $1.1 billion, marking the first time Shopify exceeded $1 billion in a single quarter.

This was driven by strong performance from subscription solutions and merchant solutions segments.

The combined strength in revenue, improved margin profile, and lower overall opex spend as a percent of revenue contributed to strong adjusted operating earnings in Q2 compared to the same period last year.

Adjusted operating income was $236.8 million in the second quarter compared with adjusted operating income of $113.7 million in the second quarter of 2020, as revenue growth outpaced growth in spend.

Echoing the bit I said about social media being the townhall of ecommerce — this is something management takes personally, which is why they announced a partnership with TikTok to launch new in-app shopping features.

The deal will allow a select group of Shopify merchants to add a shopping tab to TikTok profiles and link directly to their online stores for checkout.

The understanding of buying things is now transforming shopping into an experience that's rooted in discovery, connection, and entertainment, creating unparalleled opportunities for brands to capture consumers' attention.

TikTok is uniquely placed at the center of content and commerce, and these new solutions make it even easier for businesses of all sizes to create engaging content that drives consumers directly to the digital point of purchase.

Social commerce is a rapidly booming market.

Sales on social media apps will surge 34.8% to more than $36 billion in 2021, according to eMarketer.

Partnering with the wildly popular short form video platform TikTok is a brilliant move for Shopify — one that’s likely to pay off quite quickly.

Back to the stock market — the stock today sits at $1,450 and has gone through a time correction shifting sideways for the past 3 months.

These levels still mean that SHOP is trading at PE levels around 75, but they are a growth stock so who cares about PE levels!

The past quarter’s sensational performance translated into expanding revenue by 57%.

No doubt that beating the comparable data from a covid year is turning out to be arduous with almost the effect of turning 2021 into a consolidation year.

That has certainly been the case for Zoom Video (ZM) and Teledoc (TDOC).

Management indicated that revenue won’t be growing at the same pace as last year, but readers shouldn’t stress because this lack of pace doesn’t suggest anything is wrong with the business model.

As long as Shopify sustains a growth rate of over 40% for the next few years which is easily attainable for a company accruing only $3 billion of revenue per year, the stock will go up.

That will surely happen, and I am guessing they can maintain a 50% growth rate.

Once the lower growth rates are digested, I envision this stock turning the corner and will rise to $1,800 by the middle of 2022.

“Creativity is just connecting things. When you ask creative people how they did something, they feel a little guilty because they didn’t really do it, they just saw something.” — Said Co-Founder of Apple Steve Jobs