Mad Hedge Technology Letter

September 20, 2021

Fiat Lux

Featured Trade:

(CHECK OUT THE SCARCITY VALUE OF THIS TECH STOCK)

(MP)

Mad Hedge Technology Letter

September 20, 2021

Fiat Lux

Featured Trade:

(CHECK OUT THE SCARCITY VALUE OF THIS TECH STOCK)

(MP)

Rare earth elements shaped modern society into what it is today — just take a look at the silky-smooth touch screens on our Android phones to the Air Force’s newest fighter jets — rare earths are the building blocks of these products.

America's only rare earth mine, Mountain Pass is owned and operated by MP Materials (MP).

This open-pit mine of rare-earth elements on the south flank of the Clark Mountain Range, southwest of Las Vegas, Nevada supplied 15.8% of the world's rare-earth production last year.

It is the only rare-earth mining and processing facility in the United States, and it should be the bulwark of any long-term technology portfolio.

This is not a stock one should day-trade or even trade with a 4-week time horizon — put it deep inside your portfolio and watch it appreciate over the long haul.

One of the first things to know about rare earths is that their name is a bit of a misnomer. While their importance to consumer electronics, renewable energy, and national defense makes these materials very costly, rare earths are actually plentiful in the Earth’s crust.

The problem is that much like oil or gas, these metals can only be found in select locations around the world, hidden away inside mineral deposits that did not form with country borders or trade wars in mind.

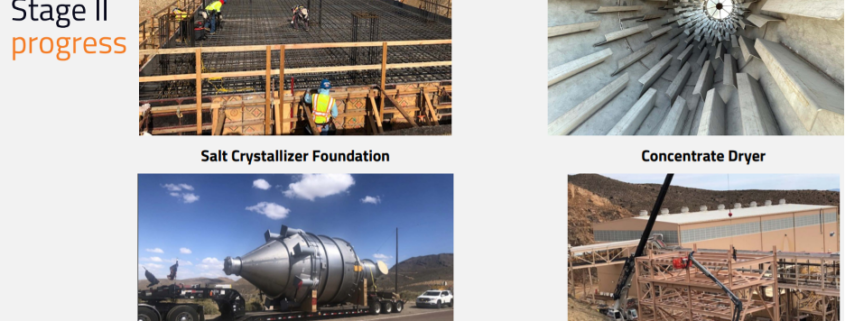

MP has a mission to achieve restoring the full rare earth supply chain in the United States.

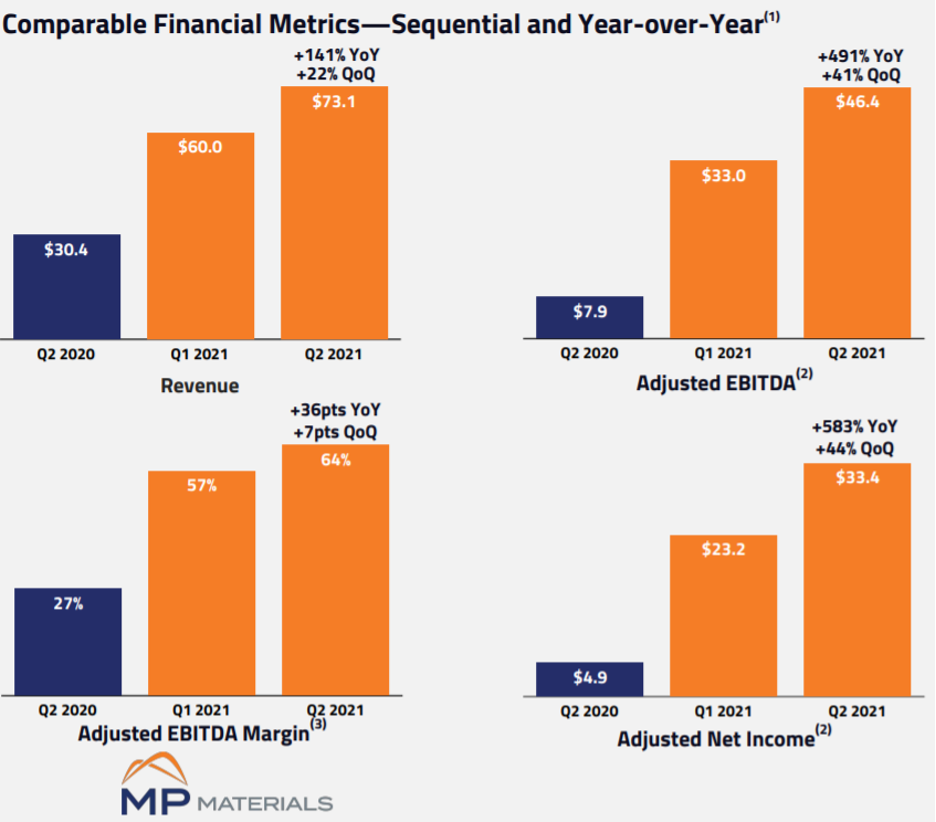

We are at the point where the Stage II project, the optimization of the Mountain Pass site, is moving beyond today's profitable concentrate production to separating rare earth oxide.

The success is critical to the global industry and supply chain security since today nearly 90% of all rare earth separation is done in China.

To contribute additional layering on why the global backdrop makes me highly bullish, I would like to analogize today's pandemic shock with the 1973 oil shock.

The ultimate takeaway is that an unexpected and significant global economic supply shock can end up reverberating for decades, not months.

In fact, the misunderstanding of transitory or short-lived events downplays the effects to the long-term cost structures.

Rare earths have experienced a rapid shift in psychology around prices in the supply chain meaning substantially higher and that’s here to stay.

Rising prices and fear of oversupply have become a further self-fulfilling prophecy across the economy.

The pandemic shock has happened under the backdrop of an already weary geopolitical environment with respect to supply chain security.

This industry has been crushed by demand backlogs for some things that stretch into next year and of course that assumes limited incremental demand in the coming months and no acceleration from an infrastructure bill.

I believe that if you do the math on some of the quantities implied by these projected investments, shortages and shocks are here to stay for quite some time despite the hundreds of billions of dollars of projected investment across new and legacy OEMs on EVs alone in the next few years.

Truthfully, I can say with audacity that at some point in the next five years, we will see at least one major global household name auto original equipment manufacturer (OEM) as well as many other small ones, fail or need a bailout due to failure to gain access to a critical material.

The last scaled and vertically integrated domestic magnet producer ceased operations and relocated to China in 2003.

Needless to say, MP is taking a concrete step towards representing a full rare earth supply chain in the United States.

Long term, are there other incremental potential customers aside from the EV supply chain expressing more interest in supply agreements?

It's broad based — not just EVs — I can tell you this with conviction.

Other spots of demand include wind turbines, drones, and many types of IoT (industry of thing) products.

I would highlight the industrial customers as chomping at the bit to get a solid pipeline of rare earths into their workshops — to get their engineers testing it in real time — it’s just not happening with this dearth of supply.

Then when you step back further and understand the semiconductor shortage — it’s a major headache — created chaos in terms of many tech companies not able to meet production deadlines simply because they have to stop production.

Investors should double down in terms of supply chain security, the first mover advantage is nothing to diminish for MP, and they are partnering with the U.S. Department of Defense due to rare earths being a national security issue.

They often host the DoD to discuss these critical issues and for the potential of future funding.

Therefore, for investors, the idea of investing in MP should be more about can I buy this whole company rather than just buying a few shares because their strategic position, tech knowhow, and revenue pipeline has a sort of unrelenting stranglehold that isn’t mirrored anywhere else in the U.S. tech ecosphere.

Then after one considers that the Chinese dilemma of protecting U.S. tech interests isn’t going anywhere anytime soon, investors must feel that any major dip in MP shares can be considered a premium buying opportunity into one of the building blocks of U.S. tech and pretty much the entire world at this point.

“I’d rather be seen as evil than incompetent.” — Said German-American billionaire entrepreneur and venture capitalist Peter Thiel

Mad Hedge Technology Letter

September 17, 2021

Fiat Lux

Featured Trade:

(AVOID THE SOFTBANK VISION FUND OF EUROPE)

(PRX.AS), (NPNJn.J), (9984.T), (LSE:MAIL), (CTRP),

(GOOGL), (APPL), (MSFT), (FB), (AMZN)

Readers should stay away from investing in Prosus NV (PRX.AS).

Who is Prosus NV?

They are Europe's answer to Japan’s SoftBank (9984.T) and its Vision Fund, and they invest in tech startups all over the world including India, Latin America, and Europe.

To get more technical, they are essentially a registered Dutch company trading in Amsterdam as the international Internet assets division of South African multinational, Naspers.

Naspers (NPNJn.J) spun out this division from South Africa in 2019 and owns stakes in consumer internet companies in online marketplaces, educational software, food delivery, and fintech.

They were once heralded for their 28.9% stake in China’s Tencent (0700.HK) but that investment has backfired as Chairman Xi has cracked down on local tech practices including data handling and youth video gaming.

Much like the Softbank Fund, which has seen its share of shocking investments, they are playing the long game through themes of accelerating artificial intelligence and achieving stakes before many companies ever go public.

Prosus has other meaningful investments in Russian tech services Mail.ru (LSE:MAIL), China’s Ctrip.com International Limited (CTRP), and Germany’s DeliveryHero.

I can’t say I scratched my head when I heard that Prosus NV has agreed to acquire Indian online payments service BillDesk for $4.7 billion, making its largest global acquisition to date in the South Asian nation.

It’s typical behavior from Prosus.

The rapid growth of the payments industry worldwide has been helped by rising demand during the pandemic.

PayU processed $55 billion in payments in the year ended March 31, 2021, a 51% increase on the previous year.

BillDesk processed $92 billion of payments in the same period suggesting an acquisition price of more than 100 times earnings.

Prosus plans to combine BillDesk with PayU, its existing global fintech and payments business, which already has a strong presence in India.

The issue I have with this is the price that was paid, and the lack of value received; and Softbank has been guilty of the same cocktail of crimes.

Overpaying for Indian fintech — at about 20 times revenues.

I just don’t get it, to be frank.

But there should be significant synergies in combining the two businesses, as well as relatively high growth to come, given the attractiveness of the Indian payment market.

The deal to buy BillDesk, which was founded in 2000, is subject to regulatory approvals, including by the Competition Commission of India.

And that’s the thing; Indian regulators have almost adopted a hostile attitude towards foreign tech acquisitions, and rightly so.

India, aside from China, boasts the biggest army of tech workers in the world and regulators are increasingly viewing foreign takeovers as foreigners hijacking a domestic growth story before Indians can harness tech they built themselves.

Deals that have been pulled off run into red flags right away just from the owners not being locals, and this risk is real.

Prosus said Tuesday's acquisition brings the total it had invested in the Indian market to more than $10 billion.

Doubling down right here I feel is a little tone-deaf as to what’s happening in the broader balkanization of the global internet.

But I am not surprised that it’s Prosus, because their most notable investment is Tencent Holdings Ltd., and getting in on an Indian payments arena on the cusp of taking off looks good from far, but is it really when the Chinese tech industry has been crushed short-term?

More than 200 million more people will adopt digital payments there over the next three years, fueling a 10-fold increase in annual transactions per person to 220, Prosus said, citing Indian central bank estimates.

Investor interest in India is accelerating as Beijing pursues a campaign to rein in tech sectors from online commerce and fintech to gaming.

Opportunities in online shopping are particularly attractive, as e-commerce accounts for less than 3% of retail transactions. Tech startups in India are still paying to build a supply chain and delivery networks.

India had a record $6.3 billion of funding and deals for technology startups in the second quarter, while funding to China-based companies dropped 18% from a peak of $27.7 billion in the fourth quarter of 2020, according to data from research firm CB Insights.

The 2020 U.S. market sell-off was met with a double for U.S. tech stocks and from that moment in time, Prosus went from a peak of €109 to €67, which is a drop of around 40%.

Even on news of this Indian takeover, there was a 5% pop met with a 5% sell the news reaction that took the stock back to 2-year lows.

Investors are not convinced of this tech start-up story and the stock has become a sell-the-rallies type of stock which is tough to shake off in the short term.

Overpaying for emerging tech while Prosus’ largest investment Tencent is down 35% from its February 2021 peak smacks of desperation and seems like they are grasping for straws.

Let me remind readers that the stock is only up 9% from its 2019 public listing and certainly when we cross-examine and compare this to U.S. tech, the only conclusion I can come up with is that performance is pitiful.

I would rather moderately overpay for Alphabet (GOOGL), Apple (AAPL), Microsoft (MSFT), and Facebook (FB), and Amazon (AMZN) than grossly overpay for Prosus.

The U.S. simply takes better care of its tech companies from a regulatory point of view, as well as stock market, business models, capital markets, desirability to be employed here, tax benefits, etc. And there’s a synergistic effect where the sum of the parts is times more.

The deal murderer is that we are inching towards a rising rate environment which couldn’t be a worse backdrop for these exotic tech investments in a murky regulatory environment.

Conversely, big tech will be able to stomach any rate rise on the backs of their robust balance sheets.

Avoid Prosus unless it drops to €50 — that’s another 19% from current prices — that would be only for a quick trade because I’m not sold on this company long term.

“The car business is hell,” said founder Elon Musk, when announcing he would sleep in the Fremont Tesla factory until Model S production reached 2,500 units a week.

Mad Hedge Technology Letter

September 15, 2021

Fiat Lux

Featured Trade:

(TRY THIS RELIABLE DATA CENTER STOCK)

(EQIX)

One of the seismic outcomes from the current rollout of 5G is the plethora of generated data and data storage that will be needed from it.

In the land of tech stocks — more data means more money.

If one fashions themselves as a cloud purist and wants to bet the ranch on data being the new oil (and one would be daft not to realize it is) then look no further than Equinix (EQIX).

This is a tech firm that connects the world's leading businesses to their customers, employees, and partners inside the most interconnected data centers.

We are really talking about the backbone of the internet.

This is what the company represents and without this spine, the internet would be way more primitive and not as robust.

On this global platform for digital business, companies fuse together worldwide on five continents to reach everywhere, interconnect everyone and integrate everything they need to reap a digital windfall.

And whether we like it or not, the future will be more interconnected than ever because of the explosion of data and the 5G that harnesses the data.

This is precisely why the data will motivate businesses to extend their reach across the globe and expand their addressable audience.

It’s not me just talking up these bunch of overachievers; the numbers back me up fully.

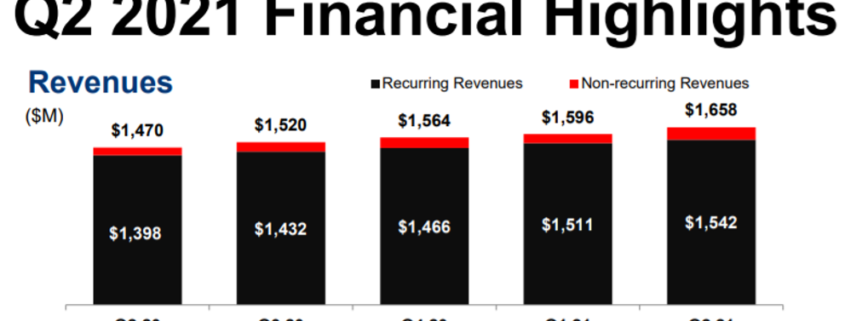

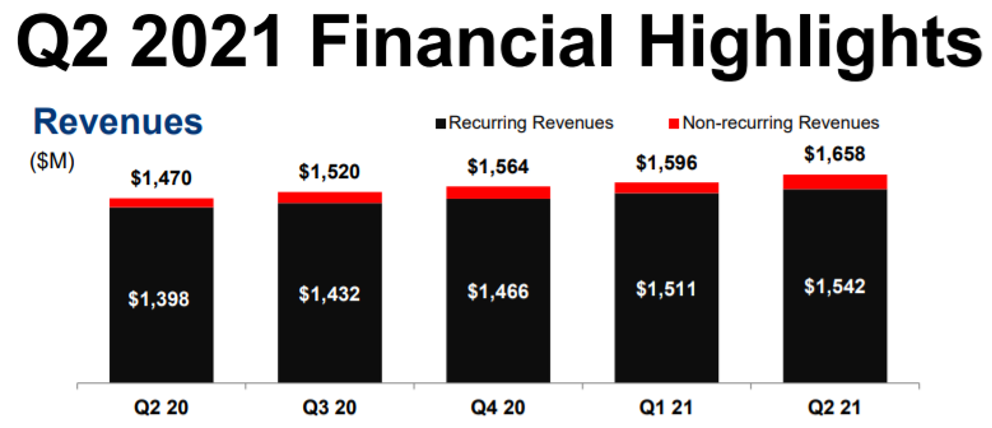

This past quarter Q2 revenues were $1.658 billion, up 8% over the same quarter last year due to strong business performance across EQIXs platform, led by the Americas region.

And as expected, nonrecurring revenues increased quarter-over-quarter to 7% of revenues due to a meaningful step-up in joint venture fees in Asia and Europe and custom installation work across all three regions.

As we must grapple with, nonrecurring revenues are inherently lumpy and therefore, as a result, EQIX expects Q3 nonrecurring revenues to decrease by $8 million compared to Q2. Cloud and IT verticals also captured strong bookings led by SaaS as the cloud diversifies towards a hybrid multi-cloud architecture.

High single digits might not look so glossy at first, but this is not a $1 billion per year in revenue company.

It’s probably one of the most stable businesses around since, unlike software, they can go out of fashion quite quickly if the next version bombs, yet storage space is more about economies of scale.

Other won deals lately include a leading SaaS provider expanding to support growth in new markets and with the Federal Government as well as an AI-powered commerce platform upgrading to enhance user experience support a rapidly growing customer base.

As digital transformation accelerates, the enterprise vertical continues to be Equinix’s sweet spot led by healthcare, legal, and travel sub-segments this quarter and the main catalysts to why I keep recommending readers this data storage company.

Other expansions this quarter included Zoom, a leading video communications platform, expanding coverage and scale to support market demand, and a cloud-delivered enterprise network security provider deploying infrastructure to support offerings in new locations.

EQIX’s enterprise vertical achieved record bookings, with broad global strength punctuated by an exceptionally strong quarter in the Americas across several subsegments, including healthcare, consumer services, business and professional services, and retail. New wins and expansions included Red Bull, a major sports energy drink manufacturer, deploying infrastructure across all three regions to take advantage of EQIX's cloud ecosystem.

EQIX can boast 65 consecutive quarters of increasing revenues, which eclipses every other company in the S&P 500, and it anticipates 8%-10% in annual revenue growth through 2022.

But now they are rolling out upgraded 2021 guidance by $15 million, forecasting to grow 10% to 12% year over year.

This represents a company that cuts across every nook and cranny of the tech sector by taking advantage of the unifying demand and storage requirements of big data.

This company will only become more vital once 5G goes blooms and being the global wizards of the data center will mean the stock goes higher in the long-term.

The momentum behind digital transformation is as robust as ever and shows no signs of letting up.

As a world digital infrastructure company, Equinix plays a unique role in this evolving story and is positioned to be both a catalyst and a key beneficiary as they partner with customers to unlock the enormous promise of digital.

They will continue to scale, doubling down on the strength of their core business, investing to further scale a go-to-market machine to win new customers, putting capital to work to add capacity in existing markets, and executing on targeted operational improvements to standardize, simplify and automate, driving expanded operating margins and providing a better experience for customers and partners.

Delivering advanced features to sustain momentum in EQIXs market-leading interconnection franchise and driving adoption of digital infrastructure services to deepen our relevance to customers is still paramount for the firms’ prospects.

I recommended this stock at $491 and now it sits nicely at $840.

My premise of buying and holding long term still holds true and any dip should be bought to take advantage of dollar-cost averaging.

I expect Equinix to be a slow and steady climb because let’s face it, it’s not a 40% per year growth story, but the stock does the job and rarely declines while providing a stable dividend.

“Capitalism has worked very well. Anyone who wants to move to North Korea is welcome.” – Said Founder and Former CEO of Microsoft Bill Gates

Mad Hedge Technology Letter

September 13, 2021

Fiat Lux

Featured Trade:

(THE DATABASE MOST WANTED BY DEVELOPERS 4 YEARS RUNNING)

(MDB), (MSFT), (IBM), (SAP), (ORCL), (CLDR)