“When something is important enough, you do it even if the odds are not in your favor.” – Said Founder and CEO of Tesla and Neuralink Elon Musk

“When something is important enough, you do it even if the odds are not in your favor.” – Said Founder and CEO of Tesla and Neuralink Elon Musk

Mad Hedge Technology Letter

July 21, 2021

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND WALL STREET JOBS)

(AAPL), (SQ), (AMZN), (PYPL)

Mad Hedge Technology Letter

July 19, 2021

Fiat Lux

Featured Trade:

(THE LARGEST SHADOW BANKER AND U.S. TECH)

(BLK), (AMZN), (MSFT), (AAPL)

In the top-heavy global media landscape, there seems to be this notion that the U.S. and its capital is the primary alpha male swaying asset prices.

The close to $6 trillion in recent stimulus chasing too few services demonstrably has an outsized vote on the matter of asset pricing.

But the dirty little secret about this stimulus is that U.S. private equity is spilling into Nordic and Western European markets effectively forcing a rapid Americanization of asset prices across the Atlantic.

Shadow banks finance financial transactions that are too risky for banks.

In the US, they already grant half of all loans.

In times of low or even negative interest rates for credit, fewer and fewer investors bring their money to a normal bank, but rather to a so-called shadow bank.

This is a term that has become established to describe a phenomenon for financial participants who are not a bank.

What a shadow bank is is not exactly defined, because there are no shadow banking licenses; but tech companies and the U.S. wielding of this critical function have changed the financial world.

In some cases, a few large private families who now have the means to invest in such funds are also focused on funding through these shadow banks and most of the time to buy American tech stocks.

And they deliberately invest not just in a single fund, but across all countries in the world, and shadow banks make up around a third of the financial sector.

In Germany, it is more than a third and on the EU average, it is almost exactly a third.

Pension funds and pension funds work like small insurance companies: employees of a company pay part of their gross wages directly, free of tax and social security contributions. At the end of their working life, they will then be paid a supplementary pension from the income generated.

The fact that “their” money is mandated to be invested in the global financial markets - at least if people hope to receive a pension after their active working life.

These European pension funds are also turning to U.S. branded shadow banking.

According to the Financial Stability Board, shadow banks had a total of $80 trillion in business in 2021.

Compared to the previous year, this was an increase of 8.5%. The FSB information is based on data from 29 countries. These in turn represent 80% of global economic output.

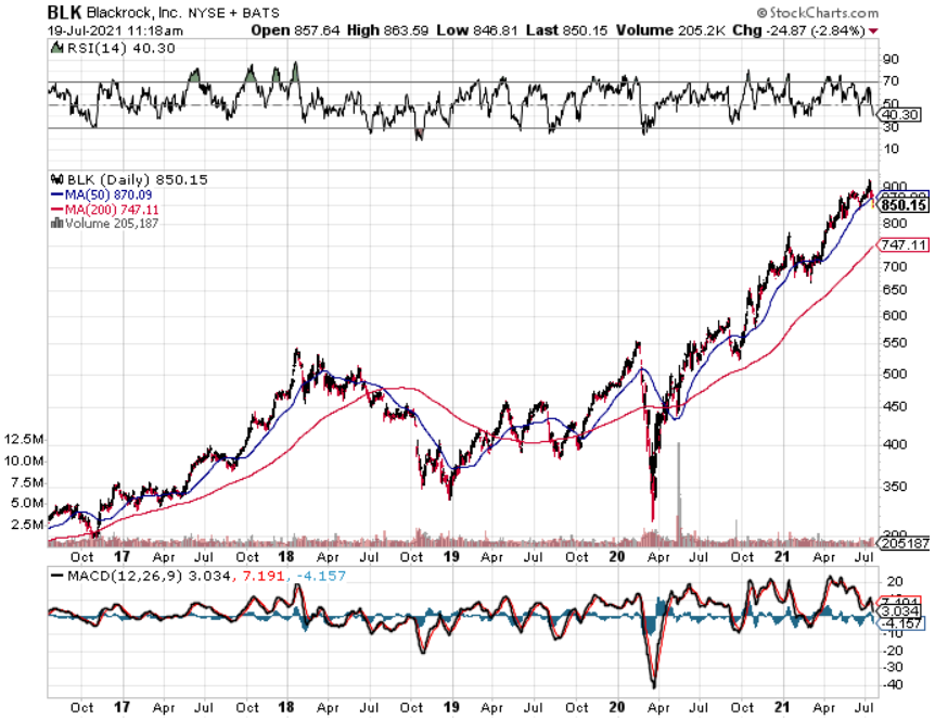

Many deals and transactions are outsourced from the banks now. That means: The financial business tries to circumvent the regulations and the largest shadow bank is BlackRock (BLK) - involved in 20,000 companies.

Many of these outsourced financial service providers are also nothing more than subsidiaries of BlackRock.

This outsourcing offers their customers the prospect of significantly higher interest rates.

BlackRock is an influential major shareholder in all listed global corporations from Europe and the USA.

Although it was founded in 1988, BlackRock was unknown to most people in Germany for decades.

That only changed in 2018, when the politician and lobbyist Friedrich Merz announced his candidacy for the CDU party chairmanship.

At this point in time, Friedrich Merz had been head of the supervisory board of the German offshoot of BlackRock for two years.

This is a company that currently manages a fortune of over nine trillion dollars which is far more than what is produced in Germany, every year, in terms of goods and services - considerably more.

At BlackRock, they harness the smorgasbord of mechanisms that define this new area of shadow banking: hedge funds, VC, real estate, index funds, and money market funds.

BlackRock holds considerable blocks of shares through various subsidiaries, including in normal commercial banks - such as Bank of America, Citigroup, and Deutsche Bank.

But that’s not all.

BlackRock is by far the largest owner in the German share index - with a share of 15 to 17%.

That means: every sixth share of the 30 largest German corporations is controlled by one of the BlackRock funds.

That BlackRock's ownership structure rotates in circles. The asset management companies control themselves, or are actually not subject to any control.

It’s an almost incestuous system where you pursue your own interests through a network of participation. While banks are systemically relevant, BlackRock is still uncontrolled, and they refuse to classify this company as systemically relevant.

But that is BlackRock and that is part of what made them highly successful.

It is extremely well connected. It has long-standing, important politicians in its ranks. Friedrich Merz is just one example in the big picture.

French President Emmanuel Macron recently said he wanted to see the creation of at least 10 tech companies in Europe worth over 100 billion euros each by 2030.

While Europe is now home to many unicorns — start-ups valued at over $1 billion — it is yet to produce a company with the scale of American and Chinese tech giants.

But I am ready to argue that Europeans no longer have control over their own narrative in their own financial system, it is now U.S. private equity.

Assuming that this holds true, even if President Macron’s wish bears fruit, the owners of these “European” tech companies will of course be Americans who are dressed up as European pension funds and maybe even perhaps somehow a company starting with a B and ending with ROCK?

The oversupply of capital from the U.S. that has overcharged U.S. tech shares will get any piece of the action that Europe creates if they are to create a tech renaissance, which I highly doubt.

And the real truth is that any unicorn created in Europe will most likely go public in New York anyway.

The pandemic has also supercharged the influence of Blackrock in Germany and Europe as a whole and that cannot be diminished.

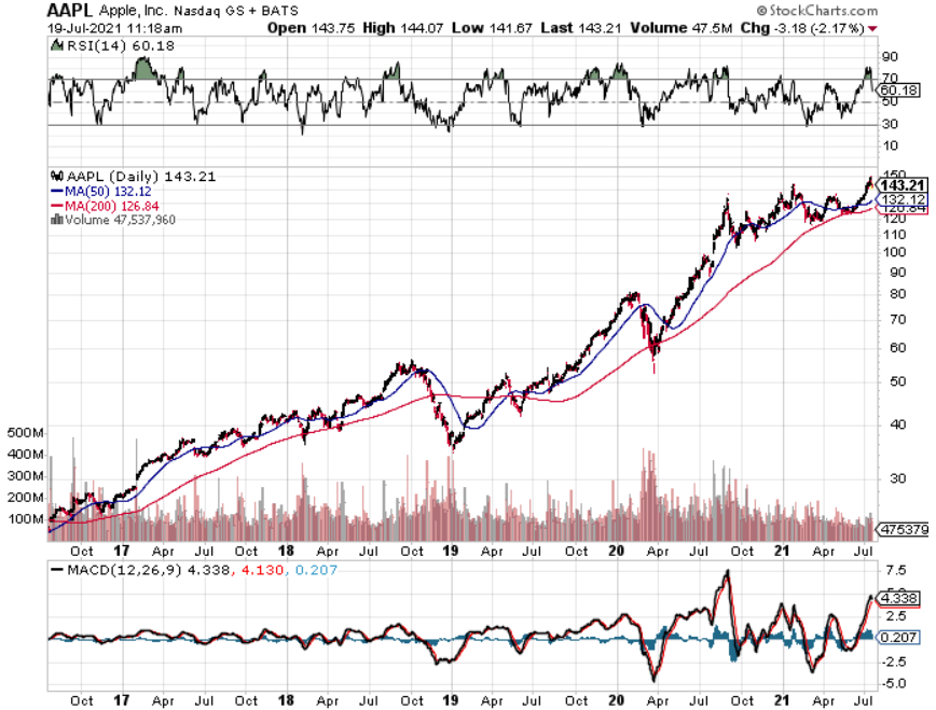

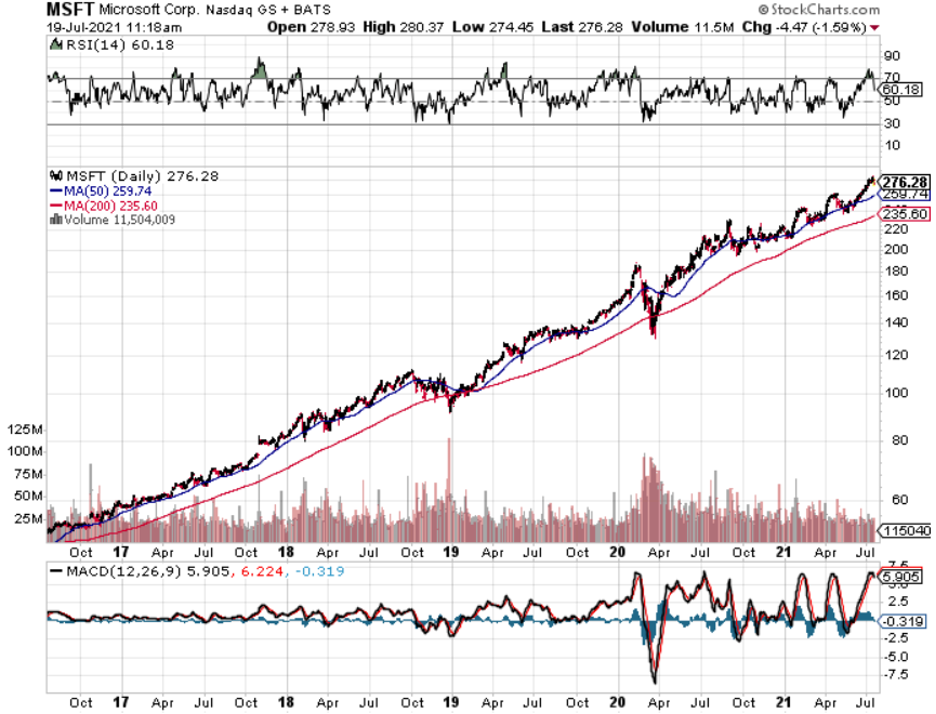

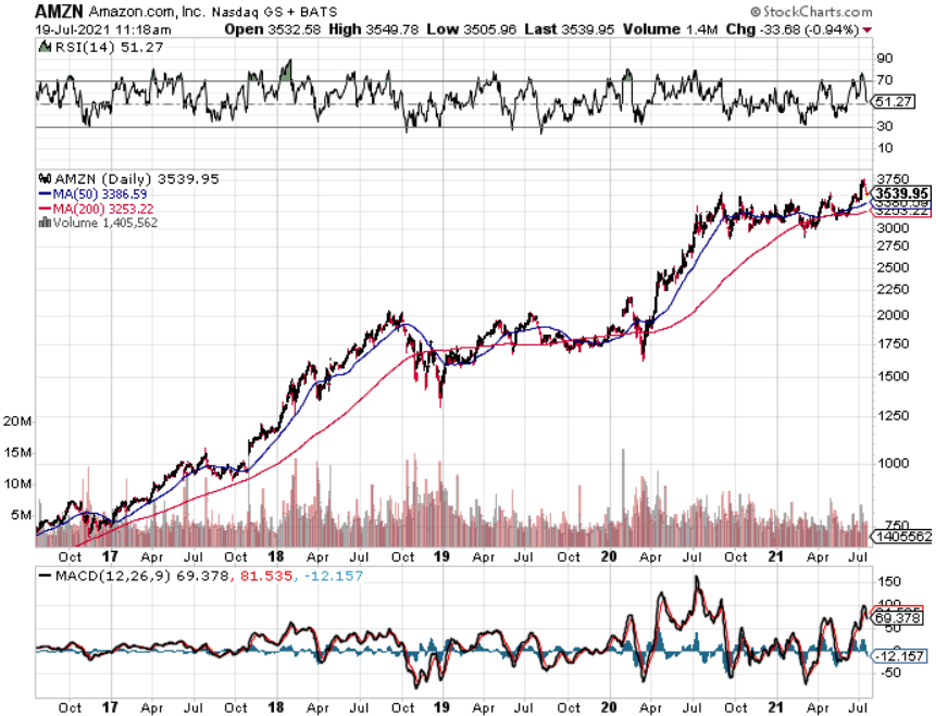

According to Blackrock’s 13F, 10% of their portfolio is Apple (AAPL), Microsoft (MSFT), and Amazon (AMZN) - holding $128 billion in AAPL, $123 billion in MSFT, and only $87 billion in AMZN.

Their largest 7 holdings are in U.S. tech stocks.

This is just a 13F in their main fund, and it wouldn’t be shocking to find out some of their European subsidiaries are also doing the same thing even if not with the same amount of capital.

The European financial system has effectively been gamed by Blackrock and its copycats, so next time you hear of a large Nordic or German equity fund making a big splash in U.S. tech shares, the eventual originator of that decision could be Blackrock.

This is the type of sophistication we are dealing with at this point in global markets and essentially nothing beats the eye test anymore because we have no idea what is happening unless we follow the trail of money.

“If GM had kept up with technology like the computer industry has, we would all be driving $25 cars that got 1,000 MPG.” – Said Co-Founder of Microsoft Bill Gates

Mad Hedge Technology Letter

July 16, 2021

Fiat Lux

Featured Trade:

(THE CLOUD)

(AMZN), (GOOGL), (CRM)

Dealing with the Cloud works and for every relevant tech company, this division serves as the pipeline to the CEO position.

If that’s not the case, then there’s something egregiously wrong!

Take Andy Jassy, the mastermind behind Amazon’s lucrative cloud computing division, and is the man who will succeed company founder Jeff Bezos.

He’s been rewarded this important business based on his performance in the cloud and faces a daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon exactly 27 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Can you believe that Amazon's stock started out at $1.50 per share when adjusting for future equity splits?

It now trades at more than $3,500 per share and is worth over $1.8 trillion, making it one of the most valuable companies in the world.

Amazon's annual profit almost doubled in 2020 to $21.3 billion stoked by the pandemic that forced people to stay home and use Amazon services.

Consumers had no choice but to shop online, helping the company grow revenue 38% to $386.1 billion.

What exactly is the cloud that Amazon created?

Cloud 101

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them working remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the recent ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

Now you might digest somewhat how Amazon built their share price from $1.50 in 1997 to over $3,500 today.

Thanks to the cloud.

“Life is not fair; get used to it.” - Said the Founder of Microsoft Bill Gates

Mad Hedge Technology Letter

July 14, 2021

Fiat Lux

Featured Trade:

(WHAT’S THE DEAL WITH MEME MANIA?)

(GME), (AMC), (WISH), (CLOV), (BB)

Although poor long-term investments, meme mania captured the imaginations of short-term traders with its wicked price action.

The counterculture drumbeat of taking down the institutions was then usurped by the meme management who issued shares after any sort of short squeeze.

Onlookers had to know the energy would not last and it is finally dying down.

Euphoric moments minted traders who benefited from unusual price spikes when institutions were caught off guard and had to buy the stock back at outrageous prices.

It appears as if this stage of meme mania is at the dying embers, and a sell the rally pattern has emerged in the past month just as big tech has accelerated its lead over everyone else.

For short-term traders, executing directional bearish bets is still on the table and for long-term buyers, you never should hold any of these following companies.

This type of smash and grab philosophy was just too risky for the Mad Hedge Technology portfolio and we avoided it like the plague.

I saw this more as a byproduct of too much liquidity in the system than anything else.

The stocks which skyrocketed were, in most cases, failed business models and only specific anomalies helped price action spin their way.

Since the volume has fallen off a cliff, the sell the rally would be the logical way to go for all the risk-takers who missed out on the meme mania phenomenon on the way up.

Here are the stocks involved.

Clover Health Investments, Corp. (CLOV) operates as a health insurer. It recently said it would be expanding insurance plans across nine states and more than 200 new counties in a bid to focus on underserved communities. The share price of the firm soared 8% after the announcement.

BlackBerry Limited (BB) provides intelligent security software and services to enterprises and governments worldwide. The company leverages artificial intelligence and machine learning to deliver solutions in the areas of cybersecurity, safety, and data privacy.

It is placed fourth a list of 10 Reddit’s WallStreetBets meme stocks hedge funds are piling into.

The company’s shares have returned 145% to investors in the past twelve months.

The company announced that the QNX software marketed by the firm was now installed in close to 200 million vehicles worldwide. This is an increase of 20 million compared to last year.

ContextLogic Inc. (WISH) is a California-based mobile ecommerce firm.

It is ranked third on a list of 10 Reddit’s WallStreetBets meme stocks hedge funds are piling into.

On July 6, the company announced that ContextLogic B.V, the Dutch arm of the business, had been granted a payment license for the European Union region. The share price of the firm jumped more than 5% after the announcement, which a company official said was the first step towards becoming a payment service provider in Europe.

GameStop (GME) rose from $4 to $325 and currently sits at $180.

The stock has continued to trend down from $320 after the latest short-squeeze and momentum is strongly biased towards the downside.

The retail company sells video games and has a terrible business model.

The last one is AMC Entertainment Holdings, Inc. (AMC) whose stock went from $2 to $60 and now is back down to $40.

AMC was a headliner disaster during the pandemic because movie theatres were closed and consumers were substituting their services for Netflix or other streaming services.

The Chinese property tycoon Wang Jianlian who bought into AMC before the pandemic was able to exit from his investment with a $675 million gain.

He acquired the company applying $1.9 billion of debt in 2012.

The Wanda Conglomerate was bailed out by the Reddit trading army after his vision of making AMC a “true global cinema operator” fizzled out big time.

The cinema chain reported a net loss of $4.6 billion for 2020, thus it’s stunning that Wang was able to spin such a disastrous investment for a tidy profit.

The AMC stake sale is the latest instance of Wanda offloading assets under pressure from Beijing, which wants Chinese to pare back its overseas holdings and debt.

The company was placed on a watch list by regulators in 2017 along with Anbang Group, Fosun Group, and HNA Group. These privately controlled Chinese conglomerates had accumulated some of the world’s largest debts after snapping up overseas trophy assets, often at premium prices, and were facing significant debt maturities.

Wang got lucky but the annual 2020 losses highlight the extent to how bad these business models are and how fortunate they were to have received a bailout from retail traders.

I believe these stocks are good for a short-term directional bearish bet with a controlled stop-loss strategy if things go sour fast.

None of these are worth owning, there are just too many other items on the menu that are tastier in a roaring U.S. economy.

From a wider-angle lens, the stock frenzy has fueled a record flow of money into the market from retail investors.

Only just last month, traders bought almost $28 billion of stocks and exchange-traded funds on a net basis, the largest amount in a single month since at least 2014.

This surely means that this new source of investment flows has gone into big tech with its huge surges higher.

At some point, capital will find itself in a different part of the equity market again and the Reddit army will be resuscitated basically because too many of them took profits and will be able to roll those profits into new positions.

Don’t get dragged into the mud looking for an easy buck.