Mad Hedge Technology Letter

July 12, 2021

Fiat Lux

Featured Trade:

(RIDE THE MOMENTUM)

(SHOP), (NFLX), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

Mad Hedge Technology Letter

July 12, 2021

Fiat Lux

Featured Trade:

(RIDE THE MOMENTUM)

(SHOP), (NFLX), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

Just as millions of people in the United States are sensing that life has returned to something that resembles normalcy, the Coronavirus’ delta variant has emerged as American technology stocks biggest upcoming inflection point.

This certainly ups the ante in the struggle to grapple with the pandemic and has wide-reaching consequences for your technology portfolio.

Fresh data from the U.S. Centers for Disease Control and Prevention shows that more than half of all new cases in the U.S. were attributed to the delta variant, which is believed to be easily transmissible.

About 50% of Americans are fully unvaccinated meaning 50% are not, which could lead to hellacious autumn for the 175 million who are not.

The tech market has sniffed this out.

Data suggesting this variant is three times as infectious as the original coronavirus strain is the catalyst for a massive rotation into premium big tech who boast glamorous balance sheets.

It is still unclear if this virus is actually deadlier or leads to more severe illness, but the health of Facebook, Google, Apple, Microsoft, and Amazon aren’t reliant on the outcome of the delta variant or at least relative to companies that have physical storefronts.

I believe the momentum in these names will continue in the short term as more countries prepare to carve up new movement restrictions and quasi lockdowns to combat the new variant.

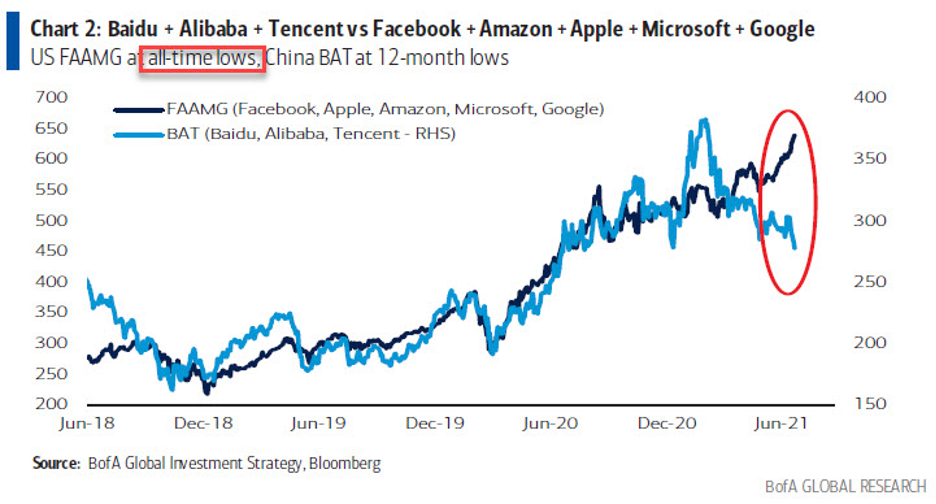

The recent tech rotation has been inconspicuous but powerful and the who’s who of big tech are enjoying a stellar run in the past month with FB up 6%, GOOGL up 4.5%, AAPL up 13%, MSFT up 8%, and AMZN up 11%.

These premium tech stocks are acting almost like U.S. treasuries and are increasingly defined as a perceived flight to safety because of

the net high quality of the assets.

Whether there is another virus that kills another 4 million globally again, investors are confident that these prioritized tech stocks are immune to any meaningful weaknesses.

On a granular level, pullbacks are becoming highly rare and mini pullbacks are becoming the only practical entry points into these stocks.

Readers waiting for a 5% drop are still waiting.

Reading waiting for 10% drops risk never getting in when the going is good.

Fresh news of Japan banning spectators for the upcoming and badly organized Tokyo Olympics took down GOOGL and FB 2% intraday only for shares to make up half the losses in one afternoon.

The delta variant has strengthened the “buy the dip” philosophy that is deeply entrenched in these 5 tech names.

The strength of tech can be seen further down the totem pole in inferior names.

Shopify (SHOP), Canada’s ecommerce crown jewel, is another winner with shares up 19% in the past 30 days.

If this rotation continues, I can realistically expect dips or sideways price action in Uber (UBER), Lyft (LYFT), and Airbnb (ABNB) because their investment case weakens relative to the big 5 in a delta variant world.

Netflix (NFLX) is another one that will harvest the low-hanging fruit with strong near-term action resulting in a 9% gain in the past 30 days.

It’s highly likely that in more than several regions around the world, the delta variant will re-silo consumers and hamstring businesses.

Crushing any green shoots that the reopening is supposed to deliver isn’t an ideal runway to growth.

Epidemiologists are starting to come out of the woodwork with Hungarian virologist Ferenc Jakab saying Hungary will be lucky to “get away with August” when referring to a possible 4th wave.

This hasn’t been fully priced into the U.S. tech market and tech will enjoy a full-scale rotation if the 4th wave arrives in full force.

However, I don’t believe we are on the cusp of another $12+ trillion bailout for the delta like last time go around, which does cap momentum to the upside.

There will also be a lack of meme stock profit-taking and bitcoin profit-taking that can be rolled into the big tech safety trade.

Sensibly, this could be a short-term boost for emerging growth tech as well with the likes of DocuSign (DOCU), Zoom Video (ZM), and Teladoc (TDOC) benefiting from investors dusting off the 2020 playbook again.

I forgot to mention that U.S. treasuries falling to $1.36% is the primary reason why at the balance sheet level, growth tech will also get the benefit of the doubt in the short term.

This won’t just be a big 5 momentum encore, others will enjoy the fruits of labor.

Loss-making tech is inordinately reliant on rates being low to subsidize losses and as the 10-year rate has gone from 1.72% to 1.36%, it’s no surprise that growth tech looks like eye candy now too.

Big tech is certainly more durable and has the capacity to navigate around rising rates which is the deal-clincher for me.

I am inclined to get back into the market with any delta scare that cheapens tech before the next leg up.

The embarrassing loss in the judicial system against FB by the Feds is the cherry on top.

I am bullish tech in the short term.

“Technology helped end communism by bringing in information from the outside.” - Said Former President of the Republic of Poland Lech Wałęsa

Mad Hedge Technology Letter

July 9, 2021

Fiat Lux

Featured Trade:

(BUYER BEWARE)

(DIDI), (PGJ), (FB), (AMZN), (GOOGL), (NFLX), (AAPL)

Chinese regulators announced on our Independence Day that they were banning downloads of Uber’s China DiDi in the app stores in the country because it poses cybersecurity risks and broke privacy laws.

This was after DiDi raised $4.4 billion by listing its shares in New York.

However, unnamed sources leaked that China's cybersecurity watchdog suggested to DiDi that it delay its IPO before it happened.

Delaying a wealth generating event like the IPO is controversial.

At this point, DIDI, the Uber of China, is worth a speculative trade at $1 and that’s if the Chinese tech firm doesn’t delist before that.

No — scratch that — it’s not even worth your time at $1 if you hold currency denominated in USD or anything even half as credible.

But if you’re from somewhere like Venezuela wielding infamous bolivars then take a wild stab around $1 or double up at $0.50 for a trade.

There is a reason that I have never in the history of the Mad Hedge Technology Letter recommended buying a Chinese technology stock.

The astronomical risk isn’t justified.

The evidence is now out in public with Chinese big tech and the Chinese Communist Party (CCP) airing their dirty laundry.

Most sensitive business dealings are usually dealt with in-house in the land of pan-fried dumplings and Beijing roasted duck, so things must be spiraling out of control on the inside.

No doubt that inflation spikes are causing chaos everywhere, but China is particularly vulnerable because of the high volume of Chinese living in poverty.

It’s unrelated to this IPO, but another valid reason why Chinese “growth” is weakening fast.

Stateside, cashing out is normal for tech growth companies who want to reward earlier seed investors, their own management teams, and in this case the early-stage investors were Japanese Softbank (21.5%), Silicon Valley’s Uber (12.8%), and China’s Tencent (6.8%).

This was pretty much a big middle finger to these three along with the other Chinese investors which were about to profit big.

This is on the heels of the CCP nixing the Jack Ma Alipay IPO.

Chinese big tech has gone from darlings to pariahs in a short time proving that in the U.S., you get too big to fail, but in China, you get too big to exist.

Silicon Valley tech princelings are also validated for leaving China such as Facebook (FB), Google (GOOGL), Amazon (AMZN) and Netflix (NFLX).

If local Chinese tech can’t flourish in China, then forget about foreign tech in China.

It’s a non-starter.

Apple (AAPL) is the only exception because they are grandfathered in when China had no smartphone and now they provide too many local jobs to be kicked out.

There is definitely a plausible case that U.S. retail investors who were part of that $4.4 billion holdings should be refunded their capital because DiDi didn’t truthfully disclose the risk of potential Chinese regulations properly.

There is also the logic that Chinese companies should never be able to list in New York in the first place which would be sensible.

As it stands, Chinese companies don’t need to follow U.S. GAAP accounting standards and cannot be prosecuted by the U.S. legal system if they commit fraud, embezzlement, or any other financial crime and decline to leave Chinese soil.

This incentivizes Chinese companies listed in the U.S. to cheat U.S. investors with fraudulent accounting and deceitful behavior because they aren’t accountable at the end of the day.

The Invesco Golden Dragon China ETF (PGJ), which tracks the performance of US-listed Chinese stocks, has lost more than one-third of its value since February.

I can tell you from close friends who call themselves frontier investors that investing in China is not worth your time and the fear of missing out (FOMO) rationale is all marketing chutzpah and nothing much else.

China’s economy hasn’t had any positive growth in the past 10 years according to Chinese insiders off record.

This FOMO narrative is often peddled by Wall Street “professionals” who are making exorbitant fees for selling retail investors Chinese junk stocks masquerading as real companies.

Out of many financial pros I have talked to, China leads in terms of horror stories from foreign investors.

The Chinese financial system is a hoax created to lure foreign capital in and for it to never leave often viewed as a free lunch for the local recipients.

And I am not only talking about Chinese tech, but this phenomenon also extends to every reach of the financial system there.

At the end of the day, China’s tech aristocracy wished they originated in the United States which is why they went public here because our markets work and theirs don’t.

They got to New York in the first place by marketing false numbers to U.S. investors and concealing regulatory issues, and U.S. investors must not fall for this trap.

If you look at the Shanghai Stock Exchange Composite Index ($SSEC), it’s gone nowhere in the past year and rightly so.

Even Chinese investors don’t buy Chinese stocks because there is no trust in their financial system. They buy property instead or buy U.S. tech stocks.

Don’t be the next sucker.

“A good boss is better than a good company.” – Said Founder of Alibaba Jack Ma

Mad Hedge Technology Letter

July 7, 2021

Fiat Lux

Featured Trade:

(SHOULD YOU BUY THE ROBINHOOD IPO?)

(HOOD), (COIN), (PLTR)

Robinhood (HOOD) is an American financial services company headquartered in Menlo Park, California, known for offering commission-free trades of stocks, exchange-traded, and cryptocurrencies via a mobile app introduced in March 2015.

After perusing their S-1, I can’t help but offer the same recommendation I gave readers for the Coinbase (COIN) listing, which proved to be spot on.

Although this is a real company with real revenues, the growth rates are particularly high because of a one-off phenomenon in alternative asset classes.

I would urge readers to not buy shares of HOOD directly after they are public but instead wait for an entry point sometime after the lock-up period expiration which usually coincides with the insiders and long-time employees unloading shares or a partial trove of them.

The same happened to Palantir (PLTR) which saw a meaningful sell-off upon the lock-up expiration and although PLTR shares are higher today than they were the day of lock-up expiration, it’s better to avoid that dip if you can. PLTR had a big dip when the lock-up expired presenting a great entry point into shares.

Lock-up periods are usually 180 days and I firmly believe this company that will be trading under the ticker symbol HOOD, is not worth paying a premium before that 180-day lock-up period is over.

Don’t be that sucker.

To dovetail with my thesis of not buying HOOD too early is the analysis of their inherent high stakes/ high rewards nature of the business.

Let’s not fudge the details, this is a high-risk business and as of now, they have been handsomely rewarded for it, but that might not always be the case.

They pioneered commission-free trading when the likes of Fidelity and Charles Schwab were still charging $15 to execute one side of a trade.

Why can they offer free trading?

Order history is paid for by third-party high-frequency traders, namely Citadel.

Citadel accounts for 27% of payments for Robinhood retail order flow, and Payment for order flow is 81% of total Robinhood revenue.

The thinking behind buying order flow is to then apply the data through machine learning to even front-run orders of normal retail traders and profit off the spread or micromovements in shares.

They even make markets with their liquidity and trade their own proprietary books.

And yes, this is legal in the United States and companies have gone gangbusters in high-frequency trading (HFT) like Virtu Financial founded by Vincent Viola who owns the NHL franchise Florida Panthers and is big into competing for his horses at the Kentucky Derby.

It obviously pays to do HFT, and if done properly, are great businesses and these are the companies propping up HOOD today.

Robinhood has taken advantage of the Millennial lust to go crypto or go home.

The numbers back me up — $11.6 billion of crypto under custody by the end of Q1.

Bitcoin was the HOOD’s most traded asset in 2020 and the first quarter of 2021 and 17% of total revenue came from crypto in Q1, (compared to 4% in Q420)

In the S-1, it said that HOOD’s business “may be adversely affected, and growth in our net revenue earned from cryptocurrency transactions may slow or decline, if the markets for Dogecoin deteriorate or if the price of Dogecoin declines.”

HOOD and its future success are now uniquely levered towards alternative coin Dogecoin which is now 34% of their total crypto revenue in Q1.

This is the altcoin that Elon Musk joked about, and it explains the 54% growth of 2020 revenue in the first 3 months of 2021.

This is an incredibly high-risk growth strategy that won’t work out every quarter.

HOOD now has 18 million cumulative funded accounts showing the popularity of the business and did $522M in 1Q21 revenue vs. $127.6M in 1Q20 and did $958.8M in revenue in '20 reporting $7.5M in net income.

The median age of customers on HOOD’s platform is 31 and over 50% are first-time investors so if they nurture this customer base, this could be a sticky business moving forward.

If they lead them down this treacherous Dogecoin cliff, it could be trouble and result in terrible quarterly earnings.

A few other risks I felt notable was that Robinhood users went from holding/trading $400M of crypto to $11.5B of crypto from March 2020 to 2021, but HOOD intends to potentially never offer delivery of customer crypto purchases.

This means they are exposed to derivative contracts which just layers on high risk on top of high risk.

Robinhood said there is tremendous regulatory risk for its stock with the company fined $70 million by the securities industry's self-regulator, FINRA, for misleading customers and system outages that the agency said hurt Robinhood's customers.

They said they will likely incur similar fines in the future and investors will need to stomach its predisposition to skirt the law.

There is nothing low-risk about HOOD, and I would wait for a big sell-off after the lock-up expiration to get in at a certain discounted price. Readers shouldn’t blindly pay a premium for HOOD, the risk isn’t worth it.

“I see technology as being an extension of the human body.” – Said Canadian Film Director David Cronenberg

Mad Hedge Technology Letter

July 2, 2021

Fiat Lux

Featured Trade:

(WHAT’S UP WITH MICRON?)