“The next major explosion is going to be when genetics and computers come together. I'm talking about an organic computer - about biological substances that can function like a semiconductor.” – Said American writer, futurist, and businessman Alvin Toffler

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/toffler.png614510Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-05 14:00:172021-04-05 14:31:31April 5, 2021 - Quote of the Day

The incredible secular trend toward digital is something a lot of CEOs talk about; and essentially, what happened last year might have taken a decade to happen in terms of the adoption of digital technology. Just take the Service Cloud at Salesforce (CRM) for an example.

Their digital service capability has grown at just unprecedented rates with the adoption of tools like chatbots powered by artificial intelligence software Einstein, they experienced a 91% quarter-over-quarter growth in chatbots alone.

Take data coming from Cyber Week this past quarter, mobile push notifications were up 131% year over year.

SMS was up 171% year over year.

The unprecedented adoption of digital really opens the playbook up for cloud companies and especially Salesforce.

Delivering success from anywhere has become their de facto motto.

Their revenue rose to more than $5.8 billion, up 20% year over year, which is expected but difficult for a company of their size.

And for the full fiscal year 2021, revenue was $21.25 billion which was up 24% year over year.

Salesforce even raised their fiscal year 2022 guidance to $25.75 billion which is now at the high end of their range, representing 21% projected growth year over year.

Salesforce’s long-term revenue target for the fiscal year 2026 is now $50 billion or basically, they plan to double the company from where we are right now.

Doubling revenue in five years would make Salesforce the second largest independent software company in the world which is breathtaking.

And a big part of Salesforce’s thesis as a company is, they’re not going back, I mean, not going back to business pre-Covid.

It’s really everyone who has experienced all these digital trends, whether it's bought online, curbside pickup, that direct-to-consumer trend in the consumer packaged goods industry, the move to telemedicine.

Salesforce is accelerating at such a rapid speed because the new world is here already, this work-from-anywhere world.

The great news for cloud companies is that they can achieve success from anywhere, but unfortunately, Salesforce is currently grappling with expensive M&A acquisitions that have penalized the recent price action in shares.

This includes costs like $190 million from Acumen, and $600 million from Slack.

For fiscal 2022, Salesforce expects an operating margin of 17.7% or flat year over year because of an expected 160 basis points headwind from Slack and Acumen.

Also, other heightened costs include investments in the core business and the anticipated gradual increase of travel in the second half of fiscal 2022.

The decrease in profitability will translate into much lower earnings per share (EPS).

As a result, this puts CRM stock on a high price-earnings (P/E) multiple of 48 which definitely isn’t cheap.

Last year, EPS was $4.92, up 64.6% from last year’s $2.99. But going forward, Salesforce forecasts that its EPS will be between just $3.39-$3.41 for 2022.

Real estate consolidation would also hurt their earnings in the year.

If you remember correctly, the company has splashed out on building Salesforce Tower in the middle of downtown San Francisco which gave them 1.4 million square feet of workspace.

Now, it sits unused because of remote work policies.

Salesforce is paying $27.7 billion in cash for the Slack acquisition which was considered way too much at the time and the all-cash transaction will mean the company will have to borrow at least $15 billion, since it has just $11.96 billion in cash and securities at the end of January 2021.

The consolidation in shares from $270 to $210 reflects the time needed to absorb these higher costs, lower profitability, and M&A transitions at a time when many cloud stocks doubled in 2020.

I do believe that when Salesforce turns around its profitability with higher trending EPS growth, stocks will gain sense of it and the direction will turn for the better.

That being said, most of the bad news is already in the stock, and we are getting close to the inflection point when Salesforce would be a favorable reversal trade.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-31 14:02:122021-04-04 21:34:00Time to Look at Salesforce

“Automation is going to cause unemployment, and we need to prepare for it.”

– Said Tech Investor Mark Cuban

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/tech-mark-cuban-033121-3.jpg489373Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-31 14:00:162021-03-31 17:05:01March 31, 2021 - Quote of the Day

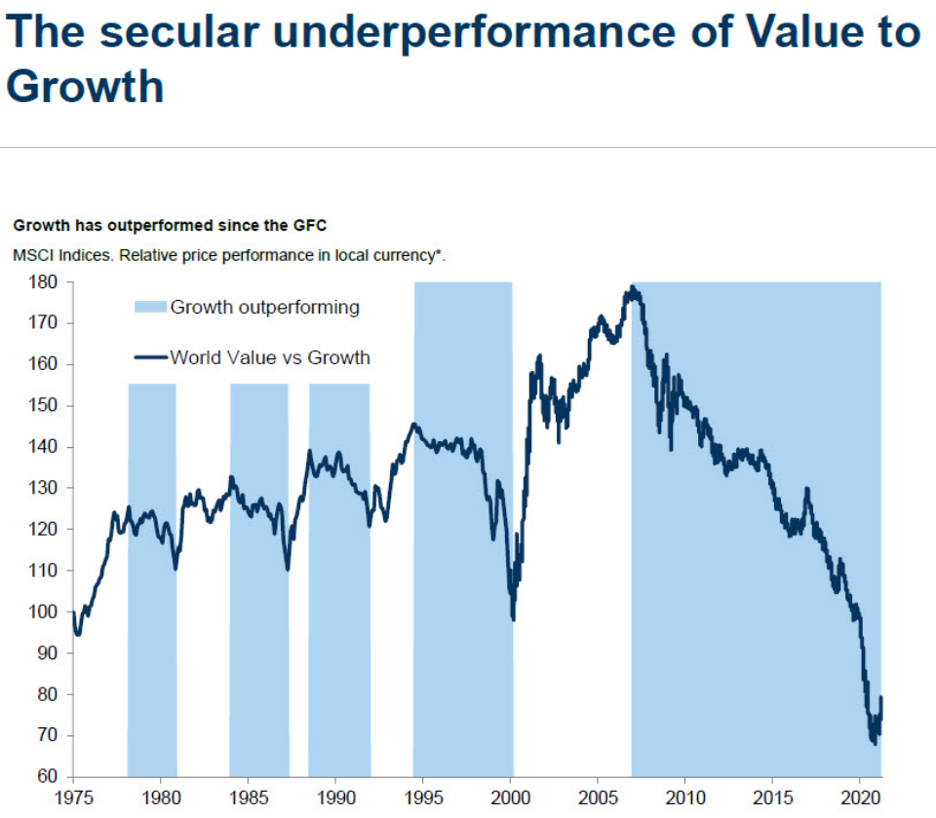

As we zoom out from tech, energy and industrials stocks have muddled through lately relatively well, while growth tech has been lethargic.

I cannot argue that we are in the middle of a rotation away from growth with capital migrating into value stocks.

Issuing low-interest rate corporate debt and spinning around to unload it to the debt market is advantageous because growth projects can be initiated without worrying about a crushing amount of future interest payments.

There is an expectation of three rate hikes by the end of 2023 which the market must absorb.

Then a mid-term expectation that the domestic economy will come roaring back is now penalizing expensive cloud services and digital communications stocks.

So now, here we are at a rock and hard place with growth with the broader market attempting to digest these roadblocks before the Nasdaq turns higher.

Just take a look at the ultimate growth stock Amazon (AMZN) or even Facebook (FB) to see a frustrating sideways consolidation from last September.

As much of this is quite disheartening for the tech investor, the tech sector remains one of the best places to look for companies creating innovative products and services that transcend industries.

I view this more as a buy the dip opportunity with the dip being elongated with numerous external events working against tech stocks.

So what are tech’s secular drivers?

According to IDC, investments in digital transformation will nearly double by 2023 to $2.3 trillion, representing more than 50% of total IT spending worldwide.

Deloitte recently released a report revealing that during the next 18 months, they expect to witness global companies embrace the bespoke-for-billions trend by exploring ways to use human-centered design and digital technology to create personalized, digitally enriched interactions at scale.

The study found that digital engagement was essential in 2020, with 96% of business leaders reporting companies who did not digitize customer engagement would experience severe negative repercussions.

These problems include a reduction in competitiveness and an inability to meet customer demands.

The companies who chose to embrace software agility meant empowering their developers to prepare tech firms for the unknown and meeting these customer expectations.

Whether it's a meteor hitting the earth, or anything else that is threatening to disrupt an industry or a business, the companies who do best can change on a dime to suit themselves for conditions in the current marketplace.

The health crisis accelerated transformation overnight.

Healthcare had to accelerate the adoption of telemedicine, and commerce companies accelerated their e-commerce plans.

The funnel that led to the consumer wallet has forever changed and in 2021, we will see further strength and momentum where we left off from last year.

Given the increased importance of digital engagement to the company's success moving forward, nearly all business leaders surveyed, 95%, expect to increase investment in digital tools after the pandemic.

Firms are now hyper-targeting a model revolving around customer engagement platforms that truly serve the end-to-end life cycle of all customer engagement in the enterprise.

Why? Because companies need to understand who their customers are, what products they're looking for, what products they bought, and where customers are interacting with their brand across multiple touchpoints.

Platforms allow the developers of the world to build, to take all of those bits of data that are siloed throughout the company to build a cohesive picture of the customer, build a world-class customer service experience and deliver the right communication over the right channel at the right time.

The endgame is to meaningfully improve every interaction every business has with every customer.

That's incredibly valuable to enterprises because it allows them to create differentiated customer experiences and all of the successful tech companies have participated in this trend.

I think that the infrastructure to build great digital products and great digital experiences spans many categories.

This rich area of opportunity will unlock developer influence and developers' ability in tech companies to build the future of these companies.

Now that every other company and industry needs tech to reach the end-user and to even initiate the selling cycle, tech is entrenched as the long-term winner.

Global business will cease to exist without software and no company will reach full potential without being powered by the best tech tools in the world, period.

And as the digital transformation is suppressed momentarily by external factors out of the control of the tech companies themselves, tech investors wait for signals for when the consolidation is over.

Tech already comprises 40% of the S&P, and by 2030, that number will be close to 75%.

This is still an industry that nobody should bet against in the long term.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/growth.png818936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-29 12:02:482021-03-29 17:31:59The Secular Tailwinds are Intact

“A founder is not a job, it's a role, an attitude.” – Said Founder and CEO of Twitter and Square Jack Dorsey

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/jack-dorsey.png510450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-29 12:00:462021-03-29 12:48:31March 29, 2021 - Quote of the Day

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

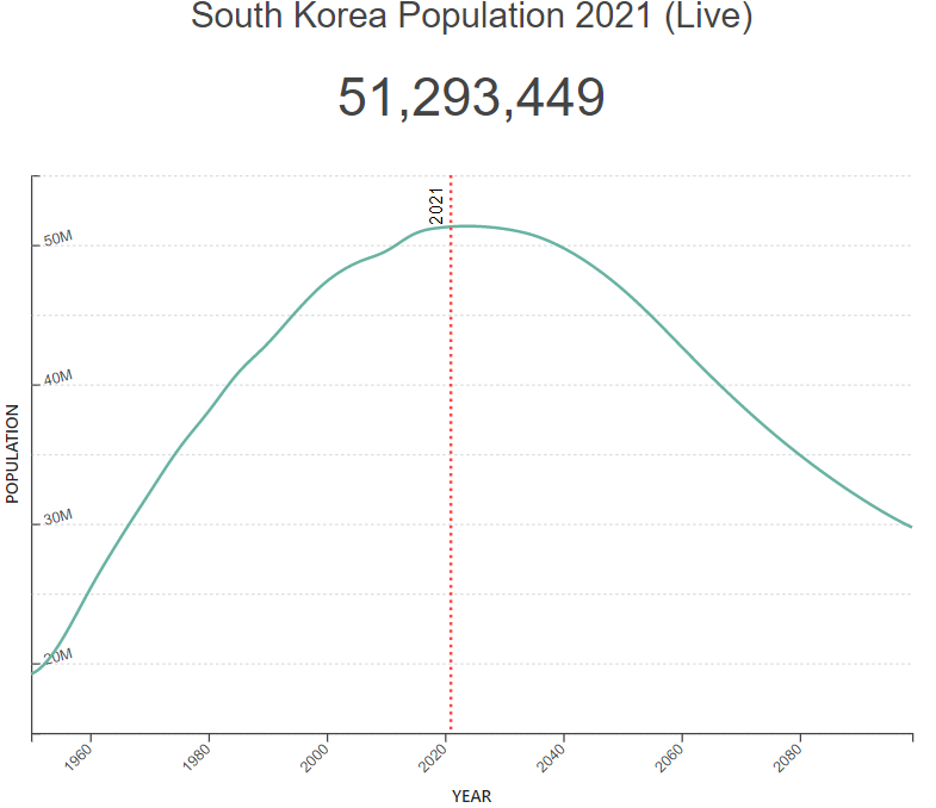

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

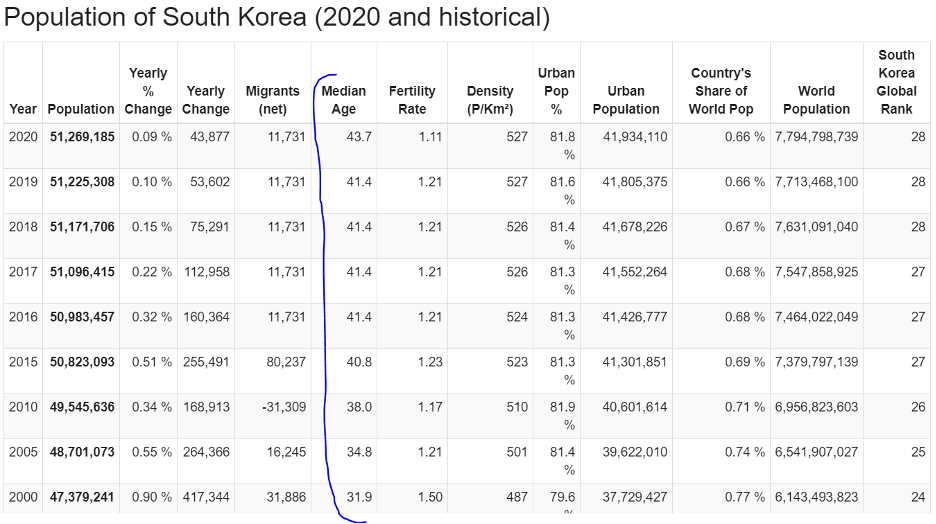

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-26 13:02:552021-04-02 23:27:35Avoid This Korean eCommerce Company

“If you're gonna make connections which are innovative... you have to not have the same bag of experiences as everyone else does.” – Said Co-Founder of Apple Steve Jobs

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/steve-jobs-e1631634374388.png328350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-26 13:00:092021-03-26 14:52:14March 26, 2021 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.