“It has become appallingly obvious that our technology has exceeded our humanity.” – Said Scientist Albert Einstein

“It has become appallingly obvious that our technology has exceeded our humanity.” – Said Scientist Albert Einstein

Mad Hedge Technology Letter

February 26, 2021

Fiat Lux

Featured Trade:

(EV INDUSTRY GOES FROM HOT TO HOTTER)

(TSLA), (GM), (EV), (SAIC), (PLTR), (ROKU)

The electric vehicle market is blossoming into a mega tech growth industry and we are just entering the sweet spot of it.

Just take a look at the variety of options now on the market.

China has been doing its best to catch up to the standard bearer Tesla (TSLA) with generous government subsidies spawning a tidal wave of new investment.

A Chinese company partnering with GM has been able to introduce an electric vehicle (EV) selling in China for $4,500 and is now miraculously outselling Tesla's posher cars.

The compact car is proving a home run for state-owned SAIC Motor, China's top automaker.

The Hong Guang Mini EV is being built as part of a joint venture with US car giant General Motors (GM) and yes, this is the same joint venture where Chinese companies “borrow” the proprietary intellectual property.

This is just another example of the breadth of options out there and the insatiable popularity of the mode of transport in a world of climate change and the broad-based pivot to sustainable ecological business.

According to Fortune Business Insights, the global electric vehicle market will be worth $985.72 billion by 2027, growing at a compound annual growth rate (CAGR) of 17.4% over the next six years.

Electric vehicle sales are poised to surpass the highest level on record in 2021.

Edmunds data shows that EV sales made up 1.9% of retail sales in the United States in 2020 and that number is expected to surge to 2.5% this year.

Edmunds analysts anticipate that 30 EVs from 21 brands will become available for sale this year, compared to 17 vehicles from 12 brands in 2020.

Notably, this will be the first year that these offerings represent all three major vehicle categories: Consumers will have the choice among 11 cars, 13 SUVs, and six trucks in 2021, whereas only 10 cars and seven SUVs were available last year.

As it is true that compact vehicles will rule the road in China, Americans have a love affair with trucks and SUVs, to the detriment of compact cars.

Each EV manufacturing decision will need to have localization in mind.

This isn’t to say that China can produce EVs at the quality of Tesla, but it shows that alternative models of EV battery capabilities, range, and performance also have a strong place in the consumer world.

This isn’t just a Tesla world with everyone living in it.

The Chinese government has bet the ranch on EVs as it reduces the smog-induced megacity pollution that has been public enemy one, two, and three.

Clean air is a sensitive topic among Chinese urban dwellers.

The Chinese communist party offers EV license plates for free and they are guaranteed. In many cities, it can take years to receive a license plate for a petrol engine through various lottery systems.

The Tesla Model 3 sells for about $39,000 in China factoring in price cuts due to its local production.

So what does this mean for the short-term future of EVs?

First, they are showing growth numbers that almost every cloud executive would love to put on the radar for many tech investors.

Second, Elon Musk’s Tesla and The Hong Guang Mini EV are primed to be flooded in all markets overseas creating an ironic situation where Europeans are buying a cheaper EV from China instead of the homegrown stalwarts of BMW, Audi, and Mercedes.

China has been adamant that they want to secure higher manufacturing ground and this phenomenon is coming hard and fast for the Europeans and everyone else who have continuously kowtowed to Chinese business.

Reports have linked these Chinese mini EVs to a Latvian automaker who could sell an iteration of the car in Europe. However, the price is likely to be twice as high due to European environmental requirements.

This also paves the way for Tesla to eventually roll out a compact car to sell in the German market and the entire European Union.

Tesla Gigafactory Berlin-Brandenburg is a European manufacturing plant under construction in Grünheide, Germany and the campus is 20 miles south-east of central Berlin on the Berlin–Wrocław railway.

Of course, at first, they will produce the American models of the Tesla, but my guess after that is they will start right-sizing their models for the local market in all shapes and sizes.

This would be the new contact point in terms of funneling Tesla products into Europe and instead of SUV/Pick-up trucks, they will create something more akin to a Fiat-sized car to suit the European market.

Although the EV market is still in its infancy, Tesla not only has first-mover advantage and the best of breed stamp of quality, but has the manufacturing prowess in terms of battery and knowhow that others don’t.

That being said, beneath the robustness of Tesla, a lot of movement is taking place as we speak and we still do not have the 2nd or 3rd Teslas emerging from the pack and we will gain more insight into who that is in the next few years.

For the next 10X bagger, potential start-ups that could take the EV market by storm is where readers should put their money, but this comes with great risk.

But I’ve been pretty good at guessing 10 baggers with recommendations such as Roku (ROKU) and Palantir (PLTR) on the way to achieve 10 bagger status.

As many understood from the first pandemic year of 2020, just throw money into Tesla and watch it explode higher.

Tesla is still an incredibly bullish tech story and I wouldn’t want to get in the way of its up moves.

The moment Tesla’s quality starts to erode and Chinese low-quality EVs catch up, that would be the cue to take profits on Tesla, but that day is long off.

“I discovered Buddha but did not set out to unearth a world religion.” – Said CEO of Microsoft Satya Nadella

Mad Hedge Technology Letter

February 24, 2021

Fiat Lux

Featured Trade:

(THE LARGEST RISK TO TECH GROWTH SHARES)

(PYPL), (SQ), (GOOGL), (BTC), (TSLA), (FOMO)

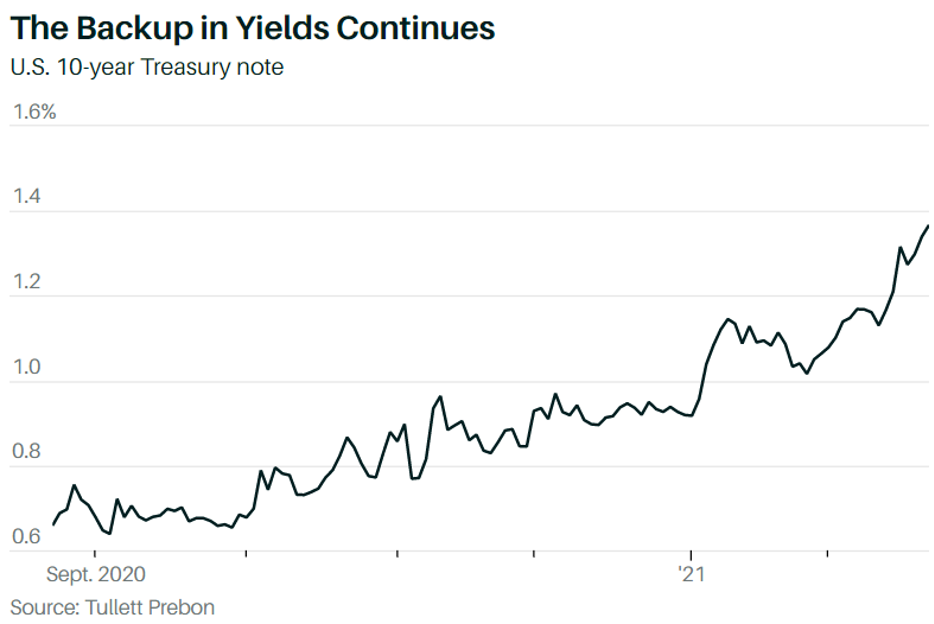

The U.S. Central Bank has chosen to be as accommodative as possible in order to put a floor under the stock market with near-zero interest rates and large-scale asset purchases.

This will have an inordinate effect on tech stocks moving forward because the rhetoric from the Fed is as close as one can get to admitting that tech stocks should be bought in droves.

Fed policy won’t kill the rally and talk up higher interest rates until “substantial further progress (to unemployment numbers) has been made,” and “is likely to take some time” to achieve said Fed Governor Jerome Powell.

Yes, it’s possible to attribute some of the bullishness to the “reopening” trade and the massive migration to digital, but the loose monetary policy is overwhelmingly the predominant catalyst to higher tech shares.

As Powell spoke, the Nasdaq did a wicked U-turn in real-time after being in the red almost 4% and sprinted higher to finish up the trading day only ½ of a percent down on the day.

What does this mean for the broader tech market and Nasdaq index?

We started seeing all sorts of wonky moves like Tesla (TSLA) making a $1.5 billion bitcoin (BTC) investment earlier this month.

Fintech player Square (SQ) bought Bitcoin on the dip pouring $170 million into it.

Yes, this isn’t a joke.

Corporations are becoming the dip buyers in bitcoin which would have never been fathomable a year ago from today.

The risk-taking has literally gone into hyper-acceleration in the tech world and is transforming into a fantasy world of corporations swimming knee-deep in capital trying to outdo one another with fresh bitcoin orders of millions upon billions.

That’s where we are at right now in the tech markets.

Treasury Secretary Janet Yellen has also gotten into the bitcoin story condemning the digital gold by saying that bitcoin is an “extremely inefficient” way to conduct monetary transactions.

But because of the extreme low-rate nature of debt, this just gives investors another entry point into the digital gold.

This sets the stage for a correction in tech stocks and the likely reason for it would possibly be higher interest rates or even negative lockdown news or some combination of both.

On the technical side of things, a result of this magnitude would be set off by first, cascading sell orders at one time, eerily similar to what got us the March 2020 low.

This could happen in either biotechnology stocks or Tesla shares and cause performance to deteriorate which could trigger net outflow and that would trigger a violent feedback loop.

Catherine D. Wood is the Founder, CEO, and CIO of ARK Invest and has been hyping up the super-growth tech assets like she was betting her life on it.

The only way she can get away with this chutzpah is in an anemic rate environment that pushes investors to search for yield.

Her reaction to yesterday’s market action wasn’t to buy bitcoin on the dip but go into a safer asset that actually produces something, and she bought another big chunk of Tesla.

Risk-taking and leverage in tech shares have gone up the wazoo which means that any incremental rising of rates is harder for the overall tech market to absorb.

Bitcoin is now being viewed as just one risk point higher on the risk curve than Tesla and that is a dangerous concept.

Technology often promises investors that they are paying for future cash flows of tomorrow and that story doesn’t work if the margins are turning against the management.

The low rates offer the impetus for characters like Wood to boast that she was surprised by how fast companies are adopting bitcoin and that her “confidence in Tesla has grown.”

It is just a sign of the times and even more money has been injected into zombie companies that have no hope of improving margins ala the retail sector.

Awash in liquidity has the ultimate effect of making tech growth stocks even more attractive than the rest of the crowd which is why we have been seeing sharp upward moves in second derivative plays to bitcoin like PayPal (PYPL), Square while the FANGs, aside from Google (GOOGL), have treaded sideways.

Markets tend to overshoot on the upside and downside and as the sell-off was met with shares that came roaring back in a speculative frenzy, we are now in a situation with many markets, even the foreign ones, hitting fresh records, even as the nations they were based in suffered their sharpest recessions since at least the Great Depression.

The overshooting tends to come from the fear of missing out (FOMO) amongst other reasons.

Ultimately, as the corporate list of characters and billionaire hedge fund community load up on tech growth stocks, just a small movement to higher yield could cause a Jenga-like toppling of their strategy and profits.

This could snowball into a massive unwind of positions to meet margin calls after margin calls.

If we can avoid this indiscriminate fire sale, then, like Bank of America recently just said, it’s hard to make a different analysis aside from being overly bullish as the treasury, Fed, and macroeconomic factors have made a major sell-off less likely.

I am bullish technology and would advise readers to go back into growth names as volatility subsides, but keep an eye out for rates creeping higher because, at the end of the day, it’s clearly the biggest risk to the tech sector.

“Our goal was never to create a better taxi.” – Said CEO of Lyft Logan Green

Mad Hedge Technology Letter

February 22, 2021

Fiat Lux

Featured Trade:

(AN ATTRACTIVE REAL ESTATE TECH PLAY)

(SPAC), (GHVI)

Special purpose acquisition company (SPAC) mania continues to bring a plethora of new tech names to the public market increasing the range of assets the Mad Hedge Technology Letter can look at.

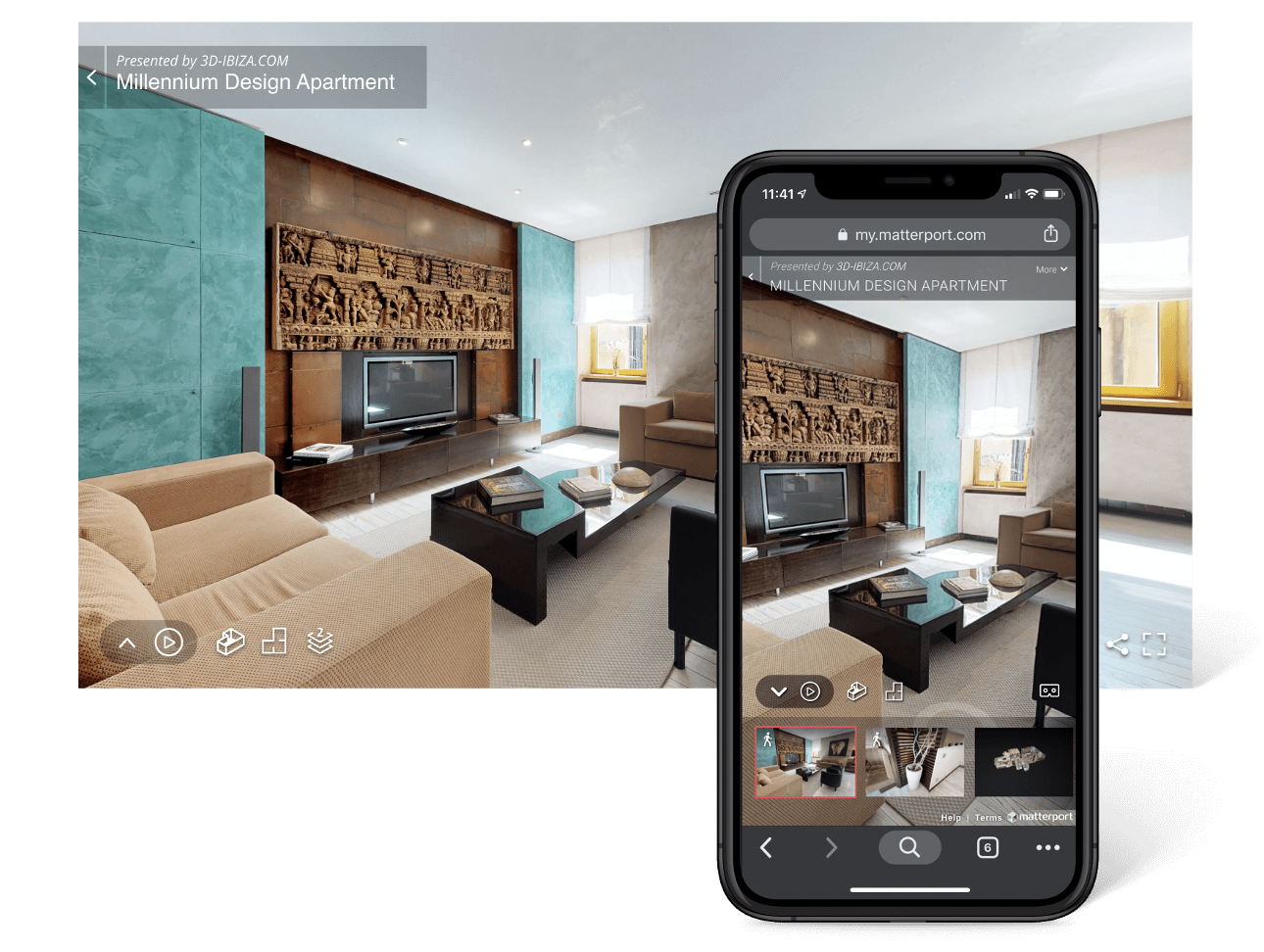

The latest is the VC-backed real estate tech company Matterport (GHVI).

Matterport has built the world’s most advanced platform for quickly and easily creating, modifying, and distributing 3D models of real-world spaces.

The company has amassed the largest repository of 3D space data in the world for industries including real estate, architecture, construction, insurance, hospitality, and more.

Matterport leverages this data to drive its AI and deep learning algorithms to create unparalleled digital reconstruction of physical spaces, with an understanding of the spaces themselves and the objects within them.

This firm went public with Gores Holding VI, a special-purpose acquisition company founded late last year by investment firm The Gores Group.

Virtual walkthroughs of properties have mushroomed during the pandemic, especially in regions of the U.S. where in-person showings were prohibited.

Matterport’s 3D technology is used in more than 130 countries by clients, which include Redfin and Marriott International.

Some prominent investors include DCM Ventures and the venture arms of Advanced Micro Devices and Qualcomm.

The SPAC popularity has now migrated to real estate, with several companies — including Opendoor and Porch.com — going public in 2020 via blank-check firms.

Matterport keeps improving its software with a major update this week, specifically for iPhone 12 Pro and iPad Pro 2020.

This update injects improved dimensional accuracy with LiDAR for those two devices.

This means that the 3D sensor at the back of the device will be deployed to capture and recreate a more life-like iteration than ever before.

Matterport has been around for a while and this app and the company behind it have been capturing 3D models.

But now the new application of LiDAR on these most advanced devices gives this software a better dimension.

This is really the first step to the real estate industry becoming more integrated with technology.

Matterport is also an expert in the handling and display of 3D-captured content from a variety of cameras, both standard flat and 3D / spherical.

Other fusion real estate technology companies are also getting in on the act hoping to go public via their own SPAC.

Recently, Compass, a New York-based real estate brokerage startup that heavily markets its technological prowess, filed paperwork to do an IPO of its own.

Alternative notables to keep an eye out for are Chattanooga, Tennessee-based tech-enabled moving company Bellhop and San Francisco-based residential real estate marketplace Sundae plan to raise more private capital before pursuing public listings.

Co-founder Gregor Watson said Oakland-based home rental marketplace RoofStock could eventually go public or sell a large strategic stake.

Carmel, Indiana-based Realync could also be an acquisition target after raising capital in 2020, according to co-founder and CEO Matt Weirich, who named RealPage and Santa Barbara, California-based Yardi Systems as logical buyers for its virtual leasing and engagement platform for multi-family residences.

I also have a good feeling about Matterport’s management.

Matterport’s CEO RJ Pittman also has a strong track record at his previous companies like having most recently served as Chief Product Officer for eBay following leadership positions at Google, Apple, and Groxis.

Pittman’s appointment coincides with a period of significant growth for Matterport, which has built a library of 1.4 million 3D models, with 600 million model views since the company’s inception.

We are barreling towards a tipping point in market adoption of 3D models to transform how building environments are designed, developed, experienced, and managed.

The commercial applications are quickly unfolding, and Matterport’s industry-leading technology is well-positioned to drive rapid market expansion.

I am convinced that management at Matterport will unlock the full potential of the breakthrough technology and unparalleled 3D media and data.

This company is on the verge of driving transformation and creating high-performance teams that will then attract world-class industry talent and accelerate the next phase of growth.

Matterport’s underlying shares have been the recipient of unbridled optimism in the accruing of future revenue and shares have already appreciated by around 100% since going public around a month ago.

“Culture eats strategy for breakfast.” – Said CEO of Microsoft Satya Nadella