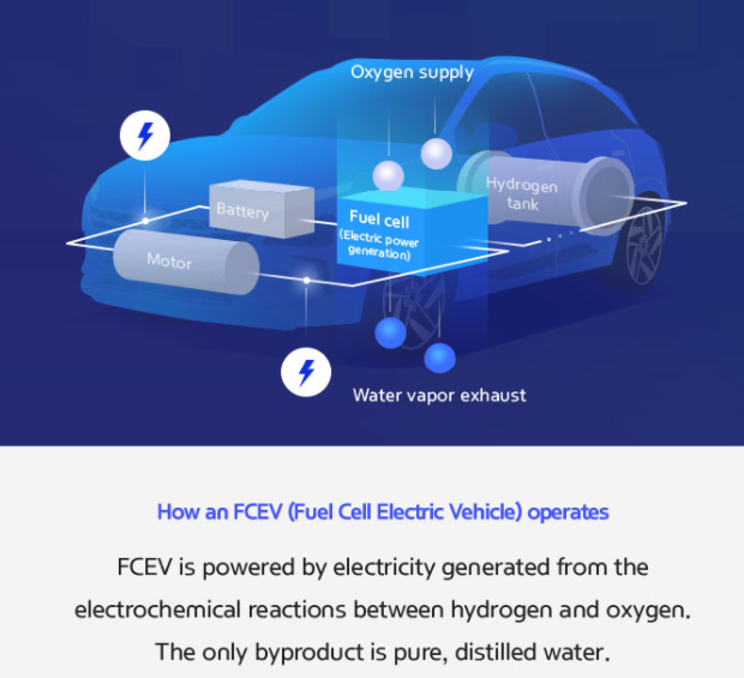

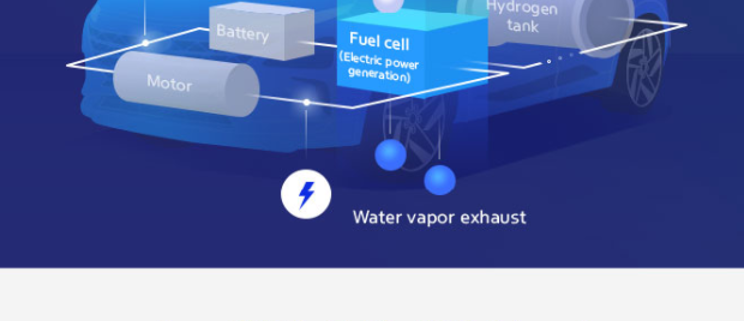

Hydrogen fuel cell technology goes like this: electricity is generated from an onboard supply of hydrogen.

That electricity powers the electric motor.

When hydrogen gas is converted into electricity, water and heat are released.

A FCEV (Fuel Cell Electric Vehicle) stores the hydrogen in high-pressure tanks.

Non-toxic, compressed hydrogen gas then flows into the tank when refueling.

Did you get all that?

This is an industry that Goldman Sachs’ (GS) says is a $10 trillion industry just waiting to happen and that is one of the plethora of reasons to look at Plug Power (PLUG.)

And when you consider that 20% of European recovery stimulus will be spent on hydrogen fuel cell technology, it seems like a no-brainer.

French automaker Groupe Renault and U.S.-based Plug Power just told us that they signed a memorandum of understanding to establish a joint venture that will develop, build and market electric fuel cell light commercial vehicles (LCVs).

The progress is real, even with German automaker BMW saying it would produce an X5 SUV with its second-generation hydrogen fuel cell powertrain by 2022.

This move pushes the narrative along for technology automakers who once hoped would replace batteries as the power source for electric vehicles, only to be thwarted by a lack of refueling infrastructure and safety surrounding the use of flammable hydrogen.

“Hydrogen fuel cell vehicles are superior driving machines compared to traditional vehicles” said Jackie Birdsall, senior engineer on Toyota's fuel cell team.

Plug Power, headquartered in Latham, N.Y., outside Albany, has emerged as the leader in developing fuel cell systems, the proverbial “best in show” having deployed more than 40,000 such systems, and has built 110 hydrogen refueling stations.

That’s essentially why Renault has made the executive decision to partner with Plug Power as it looks to create fuel cell-powered light commercial vehicles for business-to-business customers in Europe based on its Master and Trafic truck platforms.

The more practical reason to go with hydrogen fuel cells is because in electric vehicles, batteries simply cannot carry payloads of more than four tons with 20 cubic meter volumes.

There is no solution for light commercial trucks because you would need a lot of battery on board, a lot of energy, more than 100 or 120-kilowatt hours and that doesn’t make any sense in terms of cost or in terms of weight.

The attractiveness in this asset consists of perpetual operation, fast charging, fuel cells that can fill up in 5-6 minutes, can get twice the range and you also have greater density for packaging.

The target is to capture more than 30% of the fuel cell-powered European light commercial vehicle market.

The initiative goes a long way to commercializing fuel cell LCVs in Europe with a pilot fleet.

The deal with Renault is a boon for Plug Power and comes a few days after announcing a $1.5 billion investment from SK Group, a South Korean conglomerate.

It all amounts to new energy for fuel cells—not as competitor to batteries, but as an additional and supplementary source of electric power more suitable for certain applications.

The venture will start commercializing fuel-cell light commercial vehicles in Europe starting in 2021 with pilot fleet deployments and the partnership will also create a hydrogen vehicle ecosystem solution company that offers vehicles, hydrogen fueling stations, and hydrogen fuel.

The project will finish by mid-2021.

Indeed, while sentiment has grown fairly sour for using fuel cells in passenger vehicles, Plug Power CEO Andy Marsh says the technology is a perfect fit when it’s not feasible to wait around for a battery to recharge, which is why the B2B market is embracing it.

The commercial market sits entirely adjacent to the private vehicle market and traction has been slow to pick up for that segment.

Hydrogen fuel-cell cars remain low in volume, expensive to produce, and restricted to sales in a few niche regions that have built hydrogen fueling stations.

Passenger cars won’t scale up on this technology unless policies change.

I am not a believer of FCEVs for passenger cars. It costs tens of billions of dollars to set up a hydrogen fueling network that requires industrial-strength compression equipment.

However, Plug Power is the best of breed and its technology is well suited for a specific application and I do believe other countries will be interested in partnering with them to introduce it into their business-to-business segment.

Wait for a pullback to purchase shares.