Mad Hedge Technology Letter

December 23, 2020

Fiat Lux

Featured Trade:

(HOW SILICON VALLEY STAYS AHEAD)

(MSFT), (ORCL), (FB), (SNAP), (QCOM), (TWTR)

Mad Hedge Technology Letter

December 23, 2020

Fiat Lux

Featured Trade:

(HOW SILICON VALLEY STAYS AHEAD)

(MSFT), (ORCL), (FB), (SNAP), (QCOM), (TWTR)

Northern Californian tech companies stopped innovating because of the monopolistic nature of their current business models.

They keep one principle close to their vest – to crush anything that remotely resembles competition.

This has been going on in Silicon Valley for years and the government still hasn’t taken their finger out to do much about it.

The end result is an ever-growing impoverished U.S. middle class and bleak prospects for their children.

Why does the U.S. government largely sit on the sidelines and turn a blind eye?

If I deploy the concept of Occam's razor to this situation, a philosophical rule that entities should not be multiplied unnecessarily which is interpreted as requiring that the simplest of competing theories be preferred, my bet is that most of U.S. Congress own stock portfolios and these portfolios are spearheaded by the likes of Apple (AAPL), Facebook (FB), Amazon (AMZN), Google (GOOGL), Netflix (NFLX), and of course Tesla (TSLA).

This has come into the open frequently with members of Congress even front-running the March sell-off with their own portfolios like U.S. senator Kelly Loeffler from Georgia selling $20 million in stock after attending special intelligence briefings in the weeks building up to the coronavirus pandemic.

It’s a direct conflict of interest, but that's not surprising for politics in 2020, is it?

It’s also why Congress hasn’t acted on Silicon Valley’s excessive abuse of power.

The government likes to jawbone to the public saying they will make competition a level playing field, but actions show they are doing the opposite.

The Silicon Valley oligarchs are whispering in the ear of Congress and they listen.

Well, what now?

Fast forward to the future – and it was only in mid-September, TikTok — the Chinese-owned, video-sharing phenomenon — was being forced to sell its U.S. operations.

The situation is still pending, and TikTok has asked for extensions hoping to arrive at the next administration.

Given the app’s 100 million U.S. users, this forced divestment by President Trump triggered a delirious auction pitting tech giants Microsoft (MSFT), Oracle (ORCL), and Twitter (TWTR) against one another.

The White House and Big Tech are boiling the free for all down to a combined story of national security and opportunistic capitalism amid unfortunate geopolitical tension between the U.S. and China.

But the ultimatum for ByteDance, TikTok’s Chinese Mainland owner, is more accurately understood as a dark window into Silicon Valley’s utter failure to innovate, and a warning signal of its transformation into a mere protector of long-established turf.

If you don’t have it, claim national security threats, and steal it.

Silicon Valley has long adhered to the motto, “Move fast and break things” – but that was long ago when Steve Jobs was busy making the first iPod and iPhone.

That was a time when Silicon Valley headed by luminaries like Jobs was actually innovating.

Tech has now turned mostly into a digital marketing lovefest with cheap shortcuts and big swaths of the internet corrupted.

The truth is Silicon Valley couldn’t be more corporate and monolithic than it is now, and they use the corporate machine to serve the ends they desire for their shareholders to the devastation of the majority of U.S. society.

Big Tech is just in love with buybacks like the rest of corporate America and the only reason they avoid it now is to appear as if they are in tune with public discourse and not tone-deaf.

I believe that once 2021 rolls around, a floor will be set with U.S. tech because they will initiate a new wave of buybacks.

Huawei, another punching bag of the Trump administration’s tech war with China, is just an externality to Silicon Valley’s inability to innovate.

In remarks to reporters in March 2019, Chinese politician Guo Ping said, “The U.S. government has a loser’s attitude. They want to smear Huawei because they can’t compete with us.”

It’s sadly true that the U.S. has fallen so far behind the Chinese in 5G development that they have opted to scratch and claw back their position through geopolitics.

Huawei not only possesses more 5G-related patents than any other company (some 13,474). It also holds a larger share of standard-essential patents (or SEPs) – about 19% of them to be precise versus 15% for Samsung, 14% for LG, 12% for each of Nokia and Qualcomm, and just 9% for Ericsson.

The writing is on the wall that Silicon Valley is falling behind and that gap is accelerating.

ByteDance produced the hottest new social media platform on a global scale, and Facebook, in typical fashion, responded by brazenly copying TikTok, adding a feature called Reels to Instagram.

Facebook has also tapped the political back channels to encourage the U.S. government to ban TikTok not because it threatens Facebook’s model but because Facebook is concerned about national security.

What a joke.

Don’t forget that Mark Zuckerberg has been attempting to destroy Snapchat (SNAP) for years after CEO Evan Spiegel refused to sell it to Zuckerberg.

The rest of the tech ecosphere has given a free pass to the anti-trust violations because they don’t want to be the next takeout target.

Make no bones about it, Silicon Valley, aided by the Trump administration, is about to do a smash and grab job on China’s best tech growth asset then do the same thing to Huawei’s 5G apparatus.

This cunning maneuver alone has the knock-on effect of not only extending the tech rally in U.S. public markets but increasing the scarcity value and emboldening the Silicon Valley oligarchs.

The de-facto robbing of Chinese tech in broad daylight is overwhelmingly bullish for the U.S. tech sector and that is why no foreign tech player will be able to compete again in the U.S.

So why innovate? Why deploy capital into research and development when you can just nick a foreign company's crown jewel?

Exactly, so innovation does not happen and will not happen.

We, as consumers, have been thrust into the cluster of ever-degrading smartphone apps that offer less and less utility.

But ultimately, even if you hate Silicon Valley at a personal level, it is literally impossible to short them, and now they are resorting to adding foreign companies on the cheap, what other passes will government, society, and corporate America give American tech?

In either case, it’s not for me to judge, and as a technology analyst - I am bullish U.S. tech because love it or hate it, revenue is still growing and relative to the rest of the U.S. economy, they are still growth dominators.

However, one must ponder when these actions will come back to bite, if it ever does. Even though integrity has been sacrificed for profits, 2021 is poised to be the most exciting tech year with the sector usurping an even bigger portion of the broader U.S. economy.

“A good boss is better than a good company.” – Said Founder of Alibaba Jack Ma

Mad Hedge Technology Letter

December 21, 2020

Fiat Lux

Featured Trade:

(THE BEST WAY TO SUPERCHARGE YOUR TECH PORTFOLIO)

(NVDA), (PLTR), (AMD), (APPL), (OTC:SFTBF), (INTC), (QCOM)

Superiority is mainly about taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

Well, if you thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

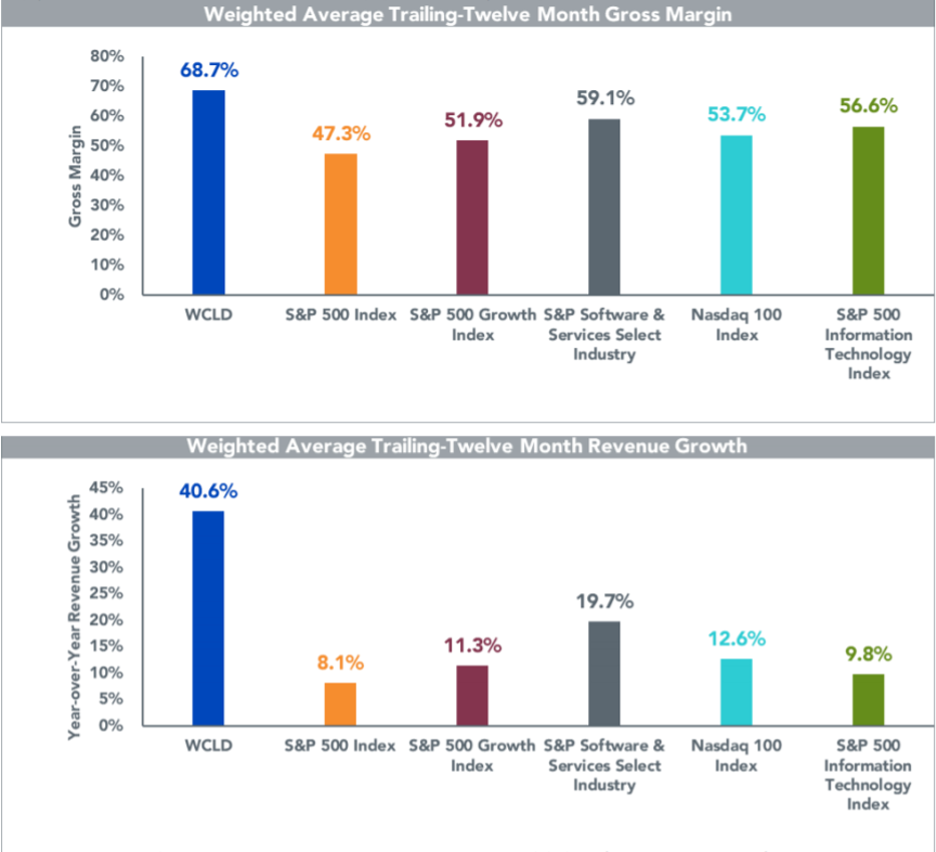

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot in 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deploying via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can more easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue streams making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to better margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD stock are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a direct play on cloud computing, but the elements of its cloud business are nothing short of brilliant.

But ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more risk because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger.

One stock that has the chance of a 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations, and my call was to buy them at $10 after it’s IPO, it's up to $26 and has an easy pathway to $50.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations even though its CEO Alex Karp has been caught on video making fun of the current administration’s leaders.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner and don’t forget about PLTR while you’re at it.

“When we launch a product, we're already working on the next one. And possibly even the next, next one.” – Said Current CEO of Apple Tim Cook

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

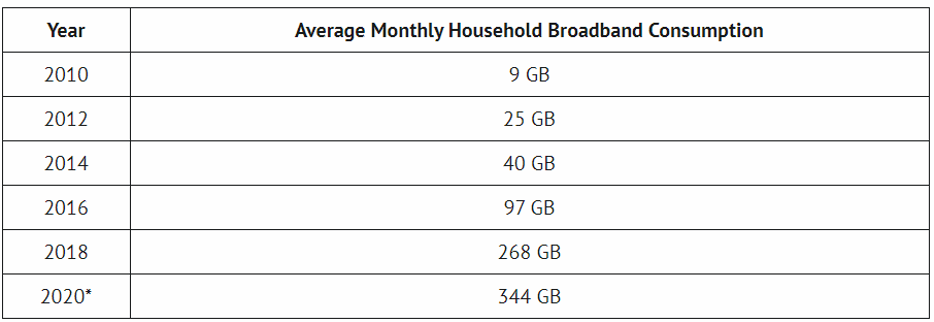

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

“I see little commercial potential for the Internet for at least 10 years.” – Said Co-Founder of Microsoft Bill Gates in 1993

Mad Hedge Technology Letter

December 16, 2020

Fiat Lux

Featured Trade:

(THE NEW SALESFORCE)

(NOW), (CRM), (SAP), (ORCL), (IBM), (MSFT)