“You don't have to start from scratch to do something interesting.” – Said CEO of Twitter and Square Jack Dorsey

“You don't have to start from scratch to do something interesting.” – Said CEO of Twitter and Square Jack Dorsey

Mad Hedge Technology Letter

September 23, 2020

Fiat Lux

Featured Trade:

(THE HOT CLOUD IPO OF FALL 2020)

(SNOW), (ZM), (ORCL)

The good news is that investors are thirsting for new cloud IPOs boding well for tech firms like Airbnb who plans to go public later this year.

The long-term health of the U.S. tech sector is on solid footing.

Most recently we had Snowflake (SNOW) who is a cloud provider and has an impressive enterprise business.

The public cloud is the data storage unit which literally everyone stores their operations on that has benefited from a massive wave of digital migration.

Many of the cloud-targeted tech firms of recent years have been 10-baggers and have dominated the overall market's returns.

Typically, these companies trade at high premiums, and rightly so, because of the corresponding growth trajectories and Snowflake is no different.

The stock has doubled after less than half a month as a tradable market-moving instrument.

Even by the standards of the most expensive software companies on the Nasdaq index, Snowflake is not cheap, although it’s a growth monster.

Snowflake was valued at $12.4 billion in February and even has investor Warren Buffett, the Oracle of Omaha, among its investors.

Buffett dove headfirst into tech investments in Apple and even some Indian fintech firms as well.

Snowflake is the largest software IPO on record and the largest since Uber's $8.1 billion IPO in May 2019.

The firm was striving for a valuation of $20 billion. In total, Snowflake has raised $1.4 billion from investors including Sequoia and Iconiq Capital.

Snowflake even makes the high-flying Zoom (ZM) Video Communications look cheap which is hard to do.

Zoom is growing three times faster than Snowflake, but trades at roughly half of Snowflake's price-to-sales ratio.

Zoom is also profitable, whereas Snowflake is a huge loss maker and that is a staple of many tech startups. This is an economic environment that is more conducive to profit drive companies instead of the tech model of promising future growth.

Snowflake is over four times more expensive than cloud company Datadog.

Snowflake's market is thought to be bigger than most other niche software applications, and therefore it may have a longer runway. In the regulatory filing, Snowflake claimed its total addressable market was around $81 billion.

Along with many other growth companies, Snowflake's ultimate margin potential is still hard to fathom and more passengers are starting to arrive in the sector than drivers.

Even worse, Snowflake not only competes with legacy data warehouse companies such as Oracle (ORCL) and Dell but also with products from the cloud infrastructure company it collaborates with.

Since shares have already doubled, I do believe that investors will need to wait for a pullback to put money to work in Snowflake.

The company said it had about 3,100 customers, including 56 clients that contributed about $1 million in a 12-month period.

Even with the pricey valuations, Snowflake is the pre-eminent cloud listing of the second half of 2020 and its enterprise business is sustainable.

If a broader sell-off drags this name down into the $180s, pull the trigger and start wading into this one.

The stock is currently priced as such that it represents flawless execution quarter after quarter for many years, and they would have to live up to lofty expectations to grow into its valuation.

While the management is stellar and is known for its execution, the odds of Snowflake's stock faltering are high because of the high bar.

Keep this one on your hot list because with all the variables waiting to pull down the market, there will be a time when the price is right in Snowflake.

“If someone asks me what cloud computing is, I try not to get bogged down with definitions. I tell them that, simply put, cloud computing is a better way to run your business.” – Said Founder and CEO of Salesforce Marc Benioff

Mad Hedge Technology Letter

September 21, 2020

Fiat Lux

Featured Trade:

(WHAT’S NEXT FOR THE TECH MARKET)

($COMPQ)

The tech market appears to be stalling out confronting uncertainty on a host of fronts, but investors betting on one theme—the unfolding economic recovery—appear positive.

What is certainly uncertain is that elections, brazen geopolitics, healthcare bills, inflation, forbearance, natural disasters are piling up like a dirty laundry basket of heightened risk.

Cyclical outperformance has been the catchphrase since the start of September, and the establishment on Wall Street has been barking for a rotation in market leadership from mega-cap tech.

As much as I love the business models of Apple, Google, Amazon, Microsoft, and Netflix, they have come too far — too fast.

We are currently smack dab in an economic phase where growth stocks won’t perform like they did when the broader economy was humming along just before March and the shelter-at-home trade has faded away from its initial boost.

There are knock-on effects and big tech doesn’t just live in a silo which is why investors are searching for reasons to take tech higher.

That being said, big tech did harvest the lions’ share of the gains from March until the end of August and in relative terms, they have emerged the ultimate winners during this health crisis.

Many upper-middle-class families are beginning to feel the economic pinch as well, as the damage is starting to be felt further up the economic food chain.

But these families will still need their tech software and services when they do a cost-benefit analysis and items such as car loans, entertainment, and food delivery will be more likely on the cutting block.

The overextended S&P 500 technology sector has lost 8% in September, while value-oriented materials and industrials have added 6% and 2%, respectively. The overall S&P 500 has declined 4%.

The valuation of the market is arguing for a rotation, not a continued leg up.

In the short term, tech stocks could lose out to U.S. small-caps and specifically small companies with high returns on equity, or ROE.

Low-ROE and nonearning stocks have dominated the Russell 2000’s rebound since late March, as investors focused on revenue growth above all else. That has benefited a lot of software, biotech, and other stocks, but forced investors to pay a high premium.

When the economy is in free fall, many companies have negative sales growth, and the market will favor those who aren’t overvalued.

By my estimation, tech is overvalued in the short-term but still a great long term bet.

Now that the fiscal morphine shot is wearing off, tech appears to be resting while it consolidates while waiting for an “event” to give it more juice.

Some fiscal tools just don’t work now like share buybacks. Management would be tone-deaf to the economic carnage going on in the U.S. — not to mention that tech stocks just visited all-time highs.

The Federal Reserve now sees 4% gross domestic product growth in the U.S. next year, followed by 3% in 2022.

This small-cap rotation will come and go, and once tech gets a little cheaper, the dip will be bought.

As the retracement goes from 20 days to one month, some positive news comes in the form of Walmart and Oracle acquiring parts of TikTok even in a highly diluted form.

Fortunately, the tech portfolio has been in 100% cash as I sensed the consolidation in time.

We will search for better entry points and will need to be patient.

“Strip malls are history.” – Said CEO and Founder of Amazon Jeff Bezos

Mad Hedge Technology Letter

September 18, 2020

Fiat Lux

Featured Trade:

(HOW WILL ARTIFICIAL INTELLIGENCE AFFECT YOUR LIFE)

(AI)

Artificial Intelligence is something we as a society, economy, and individual simply don’t talk enough about.

The point we find ourselves at today is disappointing.

Artificial intelligence is mainly controlled by the big corporations and big governments.

How is it being applied?

Largely through spying, surveillance, and digital marketing.

Digital marketing is the only one that really hits home because we are constantly bombarded with predatory ads that manipulate consumers into buying goods we don’t need.

As artificial intelligence becomes more widespread and cheaper to apply to everyday microeconomic situations, our workforce will transform into something that we could have never fathomed.

What does that mean?

Job losses and a tidal wave of automated jobs will come to the fore.

With the pandemic ravaging job prospects, white-collar professionals have lucked out being able to loaf around the office, stroke a few keys, and get paid.

Well, massive job displacement won’t come for these professionals yet, but once artificial intelligence improves by a factor of 10X,100X, 1000X, 10000X than the average human, then job losses will reach higher up the job chain and arrive like an avalanche.

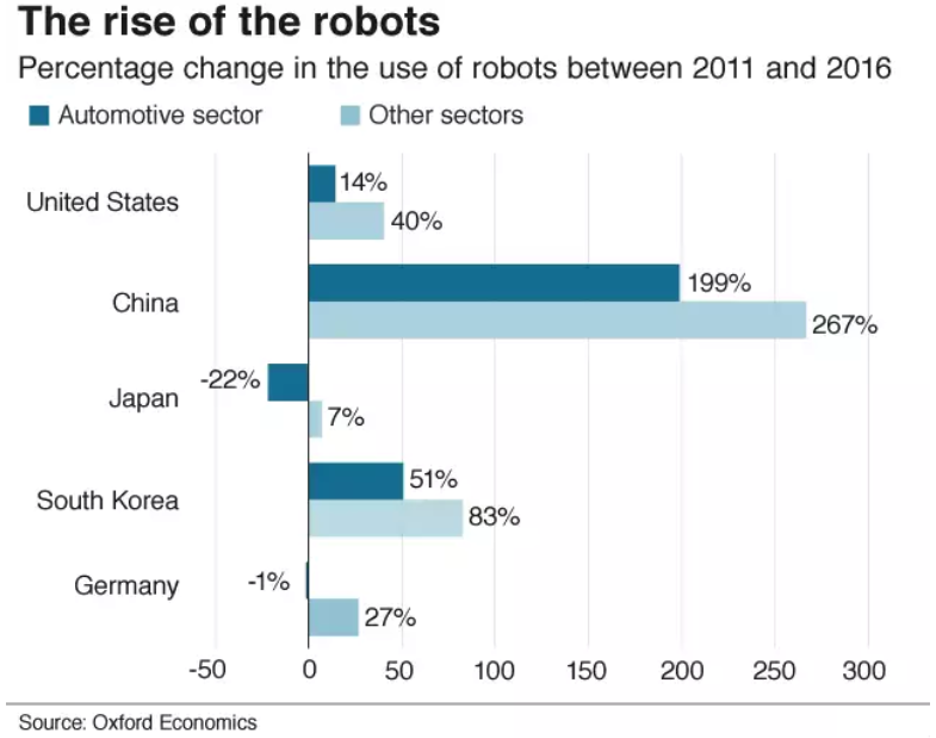

There are few hideouts from the robots, examples can be found everywhere such as accountants have a 95% chance of losing jobs in 20 years and 35% of legal sector jobs could be automated in 10 years.

Intelligent agents and robots could replace 30% of the world’s current human labor.

AI systems are already replacing human stock pickers, turning banks into human-less cloud centers running on algorithms that can analyze information from markets, social media, corporate filings, and economic conditions to quickly decipher trades. These systems can trade better than any human.

A London School of Economics study showed that 40 million manufacturing jobs around the world could be replaced with robots by 2030. Each robot impacts 1.6 jobs, with lower-skilled regions seeing a higher impact.

The only way humans will be able to get a foothold in the future job market is to merge with robots and become a super worker being able to tap into the deep reservoir of knowledge that artificial intelligence pools together.

“Augmenting humans” is a scary thought in 2020 but in 10 or 20 years, it could become the only means to survive or the only way to be competitive.

Enhanced productivity leads to economic growth, which in turn can fund new job creation opportunities and this enhanced productivity will be led and influenced by AI.

A University of Tokyo study involving 1,500 companies shows that significant performance improvement is experienced by firms which combine the forces of human and robot.

Man and AI can collaborate to enhance each other’s complementary strengths: leadership, team spirit, creativity, and social skills of the former, and speed, scalability, and data crunching techniques.

Also, technological advancements are propping up new areas which did not exist before like big data analysis, data security, decision support analysis, predictive analysis.

Data scientist was a job that didn’t exist 10 years ago, but today almost every business, from consumer brands to online pharmacies, needs data scientists to interpret customer data to design product and marketing strategies.

Around 50% of surgeons will be replaced in 20 years substituted by robots who are precise to the millimeter removing any remnants of human error.

Technology is being increasingly used to support doctors – whether it is retrieving digital records or using data analysis for diagnosis.

The “human touch” could almost become completely erased in healthcare giving way to robots being the brains of the operation and humans as assistants to lend a face to the business.

Then as AI develops, it could fork into different types of AI.

At some point, AI might be able to think for themselves, achieve consciousness, conceptualize, and do complex strategic planning or make decisions based on emotional intelligence (EQ).

Robots will eventually deal with situations where there is an absence of data and feel or interact with empathy and compassion.

Granted, we are nowhere near this last developmental stage of AI but it's food for thought while humans battle the first wave of job losses with primitive AI robots who can’t understand how you feel.

The ultimate decision that humans will need to make is if they are willing to eventually become part robot to survive.

I believe young people will jump at the chance to forge ahead a new career and ride a wave of momentum to get a leg up on the competition because they have the rest of their lives ahead of them.

Pensioners might be averse to joining the youth because they rather enjoy their last years instead of hooking up to a network of infinite data.

Do not forget that when AI is finally fused with the human brains, these humans will be able to creatively think, problem-solve, collaborate on a level that the prior collection of humans together could not compete with.

In the short-term, job losses will deepen as the world becomes overpopulated and AI isn’t mature enough to offer legitimate meaningful solutions yet.

Sometimes the economy has to go 1 step backward to go 2 steps forward.

In the next few years, we will experience the full force of digital marketing as the industry milks the last drops of what it can before that industry finally changes.

The same goes for devices like smartphones and iPads, they won’t exist in 10 years because they will be replaced.

Investors need to keep in touch with the developments of AI because seismic shifts could mean certain tech companies are deemed obsolete going forward.

In either case, software is the future, and AI and whatever framework replaces physical devices will need more software and better-quality software.

Therefore, I recommended finding the best software companies and just buying and holding because they will be part of any new tech revolution and most likely an oversized participant.

“Success in creating effective AI could be the biggest event in the history of our civilization. Or the worst. We just don't know.” – Said British theoretical physicist Stephen Hawking