Mad Hedge Technology Letter

June 22, 2020

Fiat Lux

Featured Trade:

(IS ROKU BREAKING OUT?)

(ROKU)

Mad Hedge Technology Letter

June 22, 2020

Fiat Lux

Featured Trade:

(IS ROKU BREAKING OUT?)

(ROKU)

Roku (ROKU) is another tech growth stock that is a conviction buy in my eyes.

Never sell this company if you plan to be in this long term.

The only way a sell would make sense is if digital ads stopped existing or Roku’s platform somehow managed to blackball itself out of the digital ad landscape.

Both scenarios are highly unlikely.

What does Roku actually do?

This is the company that is single-handedly destroying linear television and is laughing all the way to the bank – or at least the shareholders are.

Roku is a leader in advertising-supported video-on-demand streaming services.

In layman’s terms, they basically run commercials on its own Roku Channel and other third-party channels.

A minor part of their business is involved in making set-top boxes and streaming sticks to plug into internet video services such as Netflix and Hulu.

Plus, it sells licenses to an operating system that is thrown up smart TVs.

To beef up its products and move up in the quality food chain, the streaming platform outperformer Roku (ROKU) has agreed to a data exchange agreement with supermarket giant Kroger (KR).

Roku will apply data from the supermarket chain in its recently launched shopper data program.

The tech firm will finally get a peek deep inside the psyche of the American consumer.

I also believe this is the beginning of a massive wave of data-sharing partnerships as companies desire to understand their consumers deeper at a time when the coronavirus shut their consumers inside their house with nowhere to go.

So, how will Roku parlay this partnership into more revenue?

As people cord cut, the main goal is to seduce advertisers away from linear TV.

Juicing up its targeting abilities by using Kroger’s leading data science KPM (Kroger Precision Marketing) program, Roku will be able to move closer to the customer’s digital wallet enabling them to anticipate what they buy and how much of it they want.

The ads will be pricier because Roku will be able to hyper-target specific audiences due to a higher quality set of data they will have to work with.

From the CPG marketers’ perspective, supermarket brands will apply the data from Kroger’s KPM platform to better target the approximately 40 million and growing households using Roku, thus enabling them to better gauge which ads viewers are more likely to respond to.

Kroger will be able to understand more about their audience by assessing what commercials they consume and how they can adjust and expand their supply of goods to better capture the demand of their shoppers.

Getting more bang for their buck is a winning strategy for Roku as they delve deep into the mystical art of artificial intelligence to offer a better ad funnel.

Kroger Precision Marketing (KPM) spans 60 million US households which is not shabby itself. Marrying the 60 million with the 40 million to create a 100 million data analytics treasury trove means that Roku has just become 20% more valuable in a blink of an eye.

Roku's international growth could experience the same type of meteoric rise as what Netflix had.

If Roku can accumulate 82 million active accounts by 2025, it should have $4.5 billion in annual platform revenue.

This would mean that Roku's market cap would be around $40 billion to $50 billion in 2025. Its current market value is about $16.5 billion.

Roku still has its share of headwinds and are still loss-making.

The company reported a 45-cent loss per share for the first quarter, in-line with analyst expectations and revenue of $321 million beating the estimates by $13 million.

Since the company is still a “growth” company, investors still look through the losses to glorify growth, and Roku reporting 39.8 million active accounts, up 37% from a year ago, means they are on track.

Another concern is the higher-than-normal number of cancellations in the short-term even though its long-term runway is still solid.

However, I would say the biggest problem Roku faces is that the stock is just too hot pricing around many investors looking to put new money to work in shares.

The stock has doubled since the March lows.

In short, unless the government bans digital ads, Roku is poised to harvest the lion’s share of the spoils of the streaming revolution.

I am highly bullish on Roku shares.

Mad Hedge Technology Letter

June 19, 2020

Fiat Lux

Featured Trade:

(BET THE RANCH ON SQUARE),

(SQ), (XRT)

Square (SQ) is one of those fintech companies that you buy and never sell.

The company’s recent stock performance has eclipsed many of the other cloud stocks that have done almost as well.

Shares of Square are up from the March lows of $36 and now trading a smidgeon below $100.

It is just a matter of time before the stock breaks $100 and this company is easily a $200 stock in the future.

Let us look at the reasons why shares have rebounded with extra zeal from the nadir.

First, they are an overwhelming recipient of the “re-opening” trade which is in full effect even with a reboot of coronavirus cases in the U.S.

The government has been adamant that there is only a way forward and not backwards - shutting down the economy again is not an option.

With people out of their houses, data points are up from zero like May’s retail sales numbers showing a sharp rise of 18% month on month. The SPDR S&P Retail ETF (XRT) is up 2.4%.

Square is a fintech payment service provider among other things and their addressable market worth $160 billion is expanding and they are perfectly positioned for sustained expansion in the years ahead.

The digitization of the economy has played into Square's hands and the pandemic has acted like a supercharger to a trend: the steady migration of most everyday banking activities to mobile apps and online portals.

Why is Square a legitimate long-term threat to the traditional banking system?

Square has siphoned accounts from banks and add up to 14 million in total including customers who direct deposited their stimulus checks and/or tax refunds and not necessarily their paychecks.

Square Capital’s 75,000 PPP borrowers give Square real skin in the game and combined with a growing base of larger merchants, intimate knowledge of their revenue flows, Square will win a good amount of new small business loan activity.

Its small business loan portfolio is already approximately 75,000 loans and were facilitated during the quarter with a total value of $548 million - an increase of 8% year-over-year.

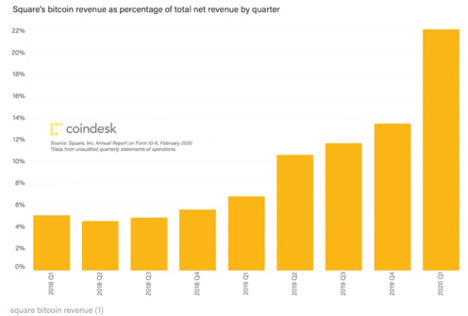

One of Square’s massive growth drivers is its accessibility to buying bitcoin and the commission of payments on the Cash app.

Square’s bitcoin revenue now accounts for 22% of total quarterly revenue.

In Q1, Cash App gross profit grew 115% year over year and gross profit on Cash App is dominated by Square’s $222 million in non-bitcoin revenue, $178 million of that was profit.

The bad news is already behind the fintech companies with the post-pandemic which saw Square’s payment volume crater 39% last month.

Even with such terrible data, Square still posted a positive earnings report with revenue for the quarter up 44% year-over-year. Gross Payment Value (GPV) was up 14% year-over-year. Gross profit was up 36% year-over-year.

Square also offers an online retail capability with Square Online Store, which competes with Shopify.

The company is a hotbed of new fintech innovation rolling out new products every quarter.

If a new product fails, management is quick to put out the flames and try something new.

They are not just a one-trick pony like Facebook and are one of Silicon Valley’s true innovation firms.

It is refreshing to see a company led with a bold CEO in Jack Dorsey who isn’t 99% marketing and 1% substance like many who make the decisions at these ultra-powerful firms.

Volatility in this stock makes this a terrible stock to trade – 6% down days are common.

Buy this stock and it will no doubt cross $200 in the next 3 years.

“Things don't have to change the world to be important.” – Said Co-Founder of Apple Steve Jobs

Mad Hedge Technology Letter

June 17, 2020

Fiat Lux

Featured Trade:

(WHY VEEVA HAS MORE TO RUN),

(VEEV), (CRM)

I am going to revisit a call I made last October 2019 on a tech stock that has outperformed mightily this year, and for good reasons.

There isn’t a tech stock more relevant today than Veeva Systems (VEEVA) because of the wave of health spending transcending the world.

Find me a country that is spending less on healthcare today!

I recommended this stock last October and the shares keep climbing over itself to reach all-time highs over and over again.

The one-sentence answer to why buy this stock is that Veeva’s latest earnings showed quarterly total revenue growing 37.7% year-over-year and EPS surging 32% year-over-year.

If I stopped here, that would most likely be enough to convince readers about this spectacular company.

Read on to understand more about this health cloud upstart positioned at the intersection of healthcare and cloud technology.

Veeva provides cloud-based CRM, data storage, and analytics services for life science and pharmaceutical companies.

It was co-founded by the former senior VP of technology at Salesforce, and its services are seamlessly integrated into Salesforce's platforms.

Veeva's tools help companies keep track of customer relationships, clinical trials, government regulations, prescribing habits, and other data in real-time.

I guess you could call it the Salesforce of cloud healthcare.

It enjoys a first-mover's advantage in the space and services an all-star lineup of top pharmaceutical companies like GSK and Novartis.

The first-mover advantage is critical because Microsoft announced a copycat version of Veeva’s services just a month ago.

To read about Microsoft heading into the health cloud business, click here.

Demand for Veeva's services has surged over the past few years, thanks to vicious competition between drugmakers and the need for real-time data.

The health crisis will also generate tailwinds for Veeva as leading drugmakers scramble to develop treatments and vaccines.

The company hasn’t been quiet, rolling out new products this year.

In May 2020, the company announced MyVeeva for clinical trials.

It is software built to enable clinical research sites to interact remotely with their patients easing the burden on in-clinic visits.

In March 2020, the company commercially launched Veeva Data Cloud, a robust technology platform constructed for the development and delivery of large-scale patient data and analytics.

The coronavirus is the catalyst that is forcing our healthcare industry to digitize rapidly and modernize.

The data backs up this trend.

The healthcare IT Market is forecasted to be valued at $511.06 Billion by 2027, growing at a CAGR of 13.8%.

To read more about this trend, click here.

Veeva analytics showed us that monthly doctor visits were halved in February compared to April before the widespread lockdown.

Teleconference doctor calls have skyrocketed increasing 30% year-over-year in April, compared with less than 1% in February.

Remote meetings between pharmaceutical companies and doctors increased more than 30 times and email communications doubled from February to April.

Veeva's management wholeheartedly believes it will reach its goal of generating $3 billion in revenue by 2025.

Their goals are impressive with an expectation of year-over-year growth rate of 26% at the midpoint.

Veeva loves to overdeliver, and if one thing is clear from the Q1 scorecard, health cloud computing services are more critical than ever to the life sciences and healthcare industries.

The company also has a pristine balance sheet with $1.38 billion in cash and short-term investments (nearly three years of cash operating expenses at the Q1 run rate) and zero debt.

Moving forward, I firmly believe that Veeva Systems will fetch a growing premium to the overall market.

The stock has zoomed from the March lows of $133 and is now trading at a robust $223 and the path of least resistance is up.

“Study hard so that you can master technology, which allows us to master nature.” – Said Argentine Revolutionary Che Guevara

Mad Hedge Technology Letter

June 15, 2020

Fiat Lux

Featured Trade:

(DON’T TAKE YOUR EYES OFF BIG TECH SHARES),

(GOOGL), (AAPL), (MSFT), (NFLX), (FB), (AMZN), (IBM), (CSCO)

There is literally no possible scenario in a post-second-wave lockdown where the 7 tech stocks of Facebook, Google, Apple, Microsoft, Netflix, Facebook, and Amazon don’t shoot the lights out unless the world ceases to exist.

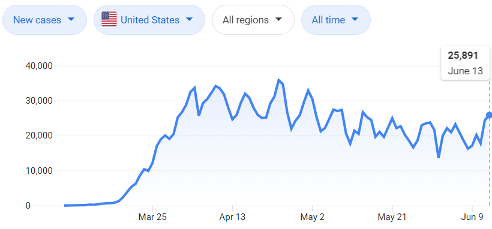

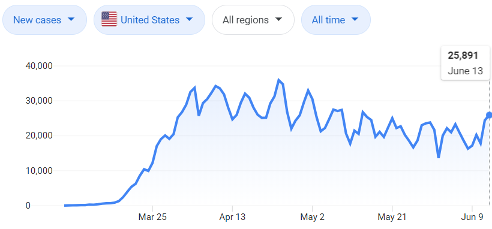

25,891 – that is the number of new coronavirus cases registered in the U.S. on June 13th, 2020 which is about in line with the recent near-term peaks of total daily U.S. coronavirus cases.

Why is this important?

Traders are calculating whether a “second wave” will possibly rear its ugly head to crush the frothy momentum in tech stocks.

That is where we are at now in the tech market.

Tech stocks could possibly ride another magnificent ride up in share appreciation if the reopening of the economy can kick into second gear.

Skeptics are sounding the alarms that this is not even the “second wave” and we still in the latter half of the first wave.

Consensus has it that this could be just a head fake.

The jitters are real with recent dive in tech shares.

The five biggest tech companies burned more than $269 billion in value last Thursday - the worst day for U.S. stocks since March and the 25th worst day in stock market history.

Nasdaq stocks ended the day largely 5% in the red with Microsoft shedding $80 billion in market cap in just one day.

Larger drops were led by IBM who lost 9% and Cisco who lost 8%.

It was a dreadful day at the office, to say the least.

We are teetering on a knife's edge and the tension is running high in the White House with Treasury Secretary Steven Mnuchin already announcing that the U.S. can’t afford another lockdown.

It’s not up to him in the end, it’s about how consumers will assess the confronted health risks.

Tech will undoubtedly be dragged down with the rest on the next lockdown sparing few survivors.

The housing market might actually go down as well as the initial push to the suburbs will dissipate and fresh forbearances will explode higher.

Consumers might not even have the cash to pay for their monthly Apple phone service or internet bill if the worst-case scenario manifests itself.

The health scare has already dented new software purchases by small and medium businesses (SMBs) and tech companies in industries such as travel, retail, and hospitality; online ad spending by the likes of automakers and online travel agencies; and smartphone, automotive and industrial chip purchases.

Small business has held off on reducing their tech software spending too much on the expectation that macro conditions will perform a V-shaped recovery.

Numerous tech firms have cited “demand stabilization,” but it’s not guaranteed to last if we revert to another lockdown.

If a lockdown happens again, it will be another referendum on Fed’s enormous liquidity impulses versus the drop in real earnings or flat out losses to tech business models.

Even with the media’s onslaught of vicious fearmongering campaigns, I do believe this is the time for long-term investors to scale into the best of tech such as Amazon, Apple, Google, Microsoft, Facebook, Netflix.

If you thought these 7 companies had anti-trust issues before, then look away.

We could gradually head into an economy where up to 40% of the public markets comprise of only 7 tech stocks which is at a mind-boggling 25% now.

Never waste a good crisis – tech is following through like no other sector!

Bonds don’t make money anymore and hiding out now means putting your life savings into these 7 premium tech stocks.

In the short-term, this is a good opportunity for a tactical bullish tech trade.