Mad Hedge Technology Letter

May 11, 2020

Fiat Lux

Featured Trade:

(HOW ALGORITHMS ARE TAKING OVER THE WORLD)

($COMPQ), (TSLA)

Mad Hedge Technology Letter

May 11, 2020

Fiat Lux

Featured Trade:

(HOW ALGORITHMS ARE TAKING OVER THE WORLD)

($COMPQ), (TSLA)

Let me explain how China has created a sudden U.S. tech ($COMPQ) renaissance that will most likely change the face of business and society in the U.S. to a degree we cannot even fathom yet.

To decompress the catalysts and the mechanisms at play in this confusing time in history, it is important to understand how the Middle Kingdom has supercharged American tech being one of the main protagonists.

Part of it is healthcare's role in the events, and part of it is tech’s strategic position waiting for a broad-based pivot in how humans internalize and execute business.

The supercharger has been the algorithms.

To explain in the best way I can, I will reference the Founder and CEO of Tesla (TSLA) and Space X Elon Musk who had a wide-ranging and insightful interview with popular podcast personality Joe Rogan.

The much-viewed interview preceded Musk’s threats to leave Fremont, California for greener pastures and transfer operations to the Gigafactory near Reno, Nevada and Texas.

To check out an article about Musk’s dare this weekend to migrate Tesla’s operations to the “Battle Born State” of Nevada, please click here.

In the interview, he delves into the U.S. healthcare system’s conflicting incentive to label anything remotely close to Covid-19 as symptoms associated with Covid-19 (which there is a long list of) that doesn’t differentiate between deaths attributed to Covid-19.

This line of thought is to widen the Covid-19 healthcare footprint to the point where each hospital can request more government funding based on the high volume of Covid-19 activity and required help to fight it.

We all love extra funding, right?

Musk also disagreed on every procedure not related to Covid-19 labeled as “elective” because it equates a pulled hamstring to a triple bypass heart surgery which can truly be life-threatening.

The point that I would like to expand on is that the attempts at widening the net of Covid-19 cases in order to curry favor for more government aid are effectively widening the digital footprint of Covid-19 internet content that is feeding back into the algorithms that are responsible for the majority of stock trades.

What we have here are vicious feedback loops that can’t be broken out of because of the misallocated tagging of Covid-19 that filters into algorithmic trading.

That is why we open up the newspaper, social media platforms, and any content provider and we are swamped by Covid-19 content and everything “associated” with Covid-19 content meaning all content has become Covid-19 content!

The net has been cast wide with homelessness caused by Covid-19, tax revenue shortfalls associated to Covid-19, professional sports seasons cancelled by Covid-19, and even a story about the King of Thailand King Maha Vajiralongkorn holed up in Switzerland with his wife and a harem of 20 other women to “quarantine” because of, yes – Covid-19. To read this story, click here.

Basically, all content is Covid-19 content until it isn’t.

This indelible influence on global governance has been deep with every politician feeling the pressure of continuing the lockdown because of a massive dislocation between the real footprint of Covid-19 and the digital footprint of Covid-19.

Healthcare pros as well have been duped by the wrong data and supporting lockdown policies because of the risk of looking bad due to perceived optics not meshing well with the current digital content being published.

The truth is that the real data is probably 1.5 standard deviations from what is believed to be consensus – a far cry from the gross data politicians and healthcare experts are using to make important decisions with.

Naturally, protecting a tenure as a politician is human nature and the unintended consequences to guarding one’s political career are causing longer lockdown periods.

Nobody wants to put their neck out and appear out of line.

Musk argued the case that the virus’s fatality rate is in fact “5-10X” lower than it actually is because of the concept of too many deaths being falsely attributed to Covid-19 symptoms and the lack of tests meaning many people are living with it but have not been accounted for in the data.

The tech market has taken wind of the discrepancy and the fierce rally calling the data’s bluff working with another set of data.

Then add to the casserole that tech companies successfully missed the “big one.”

The “big one” is defined by a virus that actually kills healthy bodies between 20 and 30 years old with no pre-existing conditions at a high rate.

And in economic terms, the “big one” means not being a hospitality, retail, or transport business.

The strength of the tech V-shaped recovery stems from the notion that this pandemic is not nearly as bad as we think it is.

There is definitely a level of truth in this.

Another unavoidable unintended consequence is the hastening of decoupling between the Chinese and U.S. economy as the blame game accelerates.

As a result, corporate manufacturing will be shipped back to the U.S. and this isn’t your father’s manufacturing either.

We are talking about manufacturing in the vein of Tesla, that will sprout up across the U.S. as artificial intelligence is finally good enough to make manufacturing profitable stateside as more automation takes hold.

Many of these new industrial A.I. manufacturing headquarters, factories, and complexes will be set up in tax-friendly states like Nevada and Texas taking a cue from Tesla.

There have been many analysts in the China camp prophesizing that the Chinese Communist Party (CCP) will apply the virus as a vehicle to push their narrow agenda.

However, Liu Chenjie, chief economist at fund manager Upright Asset has estimated job losses in China resulting from the pandemic of up to 205 million workers.

Click here to read about the devastating job losses in China.

The CCP is more worried about cleaning up the mess at home.

I would argue that the post-virus tech economy is setting up for a quicker than expected recovery.

As fast as the virus hit, the algorithms pushing this pandemic into the arteries of all digital channels will disappear in days, almost as if Covid-19 never happened.

Covid-19 has been the direct catalyst to a myriad of firings at digital newspapers all over the U.S., for example, Vice Media cut 10% of company’s employees — resulting in the elimination of 250 jobs.

As one door shuts - another one opens.

As tech companies have withstood semi-apocalyptical conditions, imagine how well they will do on the other side when consumers finally get their incomes flowing again.

U.S. tech is a shining example of the future being limitless, and complicit or not – China, algorithms, and healthcare experts gave a great assist.

“Artificial Intelligence is a fundamental risk to the existence of human civilization.” – Said Founder and CEO of Tesla and Space X Elon Musk

Mad Hedge Technology Letter

May 8, 2020

Fiat Lux

Featured Trade:

(WHY TECH IS THE BIG BAILOUT WINNER)

(EA), (ATVI), (TWLO), (UBER), (LYFT)

Today, we got a convincing signal that trillions of stimulus dollars are being diverted into one asset class – tech shares.

That’s right, even though main street has not participated in the V-shaped recovery that tech shares have basked in, tech’s profit engines have gotten through largely unscathed.

The earnings that have streamed out this week validate the big buying into tech shares and today’s price action was mouthwatering.

We had names like cloud communications platform Twilio (TWLO) rise 40% in one day, ride-sharing platform Lyft (LYFT) was up 21%, and Uber (UBER) another 11%.

Outperformance of 5% seemed pitiful today in an asset class that has gone truly parabolic.

Another sub-sector that can’t be held down is video games.

The rampant usage of video games dovetails nicely with the theme of tech companies who have triumphed the coronavirus.

There is nothing more like a stay-at-home stock than video game maker Electronic Arts (EA) who beat expectations during its March quarter.

The company reported adjusted earnings of $1.31 per share during its fiscal fourth quarter, topping consensus estimates at 97 cents a share.

Revenue also beat totaling $1.21 billion surpassing estimates by $.03 billion.

EA Sports has identified Apex Legends as their new growth asset and this free game is having a Fortnite-like growth effect.

Apex Legends was the most downloaded free-to-play game in 2019 on the PlayStation 4 system.

The full ramifications of Covid-19’s impact on EA’s business, operations, and financial results is hard to quantify for the long term and this has been a broad trend with many tech companies pulling annual guidance.

I can definitely say that the year 2020 is experiencing a video games renaissance.

On the downside, EA is heavy into sports video games, and cancellations of sports seasons and sporting events could impact results, given its popular sport simulation titles like FIFA and Madden NFL.

EA Sport’s competitor Activision Blizzard (ATVI) is positioned to reap the benefits by reimagining mainstay title Call of Duty Warzone and users have already hit 60 million players in just 2 months.

The result is accelerating momentum entering the second quarter from the dual tailwinds of strong execution and premium franchises following last year's increased investment.

With physical entertainment venues like movie theaters, live sports, and music venues closed, home entertainment services have pocketed the increased engagement.

Nintendo is another gaming company whose fourth-quarter profit soared 200% due to surging demand for its Switch game console, and that title Animal Crossing: New Horizons shifted a record 13.4 million units in its first six weeks.

Activision is riding other hit game franchises like World of Warcraft, Overwatch, and Candy Crush – to visit their roster of blockbuster games, please click here.

These blockbuster titles are carrying this subsector at a time when the magnifying glass is on them to provide the entertainment people crave at home.

Shares of EA and Activision Blizzard are overextended after huge run-ups and another gap up from better than expected earnings reports.

If there is a dip, then that would serve as an optimal entry point.

The lack of vaccine means that gaming will see elevated attention until there is a real health solution.

If there is a second wave that hits this fall, then pull the trigger on these video game stocks.

To visit Electronic Art’s website, please click here.

“My goal wasn't to make a ton of money. It was to build good computers.” – Said Co-Founder of Apple Steve Wozniak

Mad Hedge Technology Letter

May 6, 2020

Fiat Lux

Featured Trade:

(THE GOLDEN AGE OF BIG TECH HAS ONLY JUST BEGUN)

(AMZN), (MSFT), (AAPL), (FB), (GOOGL), (ZM)

The tech market is telling us that the effects of coronavirus on the U.S. economy have accelerated the Golden Age of Big Tech pulling it forward to 2021.

You know, Big Tech is having their time in the sun when unscrupulous personal data seller Facebook is experiencing 10 times growth with its live camera product Portal video during the health crisis.

That is the type of clout big tech has accumulated in the era of Covid-19 and investors will need to focus on these companies first when putting together a high-quality tech portfolio.

Every investor needs upside exposure to a group of assets that is locked into the smartphone ecosphere.

There are no excuses.

Smartphones, although not a new technology, is now a utility, and the further away from the smartphone revenue stream you get, business is nothing short of catastrophic minus healthcare.

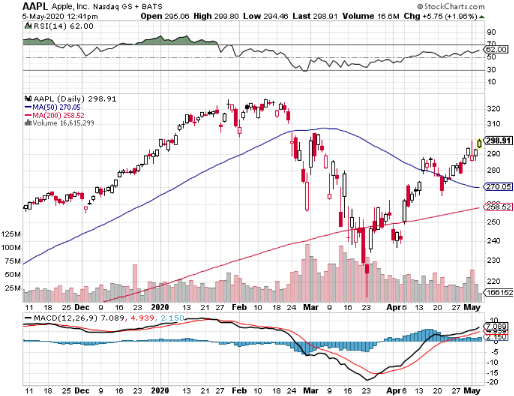

The health scare has ultimately justified the mammoth valuations of over $1 trillion that Apple, Microsoft, and Amazon command.

The next stop is easily $2 trillion and then some.

Consumers are so much more digitized in this day and age weaving in a tapestry of assets such as the iPhone at Apple, advertising at Facebook, and search ads at Google.

Can the coronavirus keep the digital economy down?

Green shoots are certainly popping up with regular consistency.

Facebook and Google have said that digital advertising has “stabilized.”

Apple, Amazon, Netflix, Facebook, and Google each reported financial results in the past week with profits and revenue that, while hit by the closure of the economy, still outperformed relative to the broader market.

Investors already priced in that Apple's iPhone sales temporarily disappeared, that Google's and Facebook's advertising revenue dropped and that Amazon is spending big to keep warehouse workers safe.

Forward expectations can only go north at this point reflecting a giant bull wave of buying that has benefited tech stocks.

Other top tier companies not in the FANG bracket have also gone gangbusters.

Zoom has turned into an overnight sensation now replacing all face-to-face meetings, sparking competition with Microsoft's Teams video chat and Google Meet.

The market grab that big tech has partaken in will position them as the major revenue accumulators for the next 25 years.

Unsurprisingly, Apple was the canary in the coal mine by calling out a dip in iPhone sales and manufacturing in China earlier in the year.

While iPhone's sales did fall, down nearly 7%, to $28.9 billion, its revenues from services and wearables, two categories that have been rising steadily for years, jumped 16.5% and 22.5% respectively.

Chip giant Qualcomm said phone shipments will likely drop about 30% around the globe in the June quarter while Apple rival Samsung, said phone and TV sales will "decline significantly" because of the coronavirus.

Google’s YouTube has grown 33% while the video giant keeps us entertained and Microsoft’s Xbox Game Pass subscription service notched more than 10 million subscribers.

Facebook said nearly 3 billion people use its collection of chat apps representing an 11% jump from a year ago.

Everywhere we turn, relative outperformance is evident which in turn minimizes the absolute underperformance in year to year growth.

The market is looking through and putting a premium on the relative outperformance.

Many are coming to the realization that the economy and population will live with the virus until there is a proper vaccine, meaning an elongated period of time where consumers are overloading big tech with higher than average usage.

President Trump’s chief economic adviser Larry Kudlow is projecting that the U.S. economy next year could see “one of the greatest economic growth rates.”

I would adjust that comment to say that big tech is tipped to be the largest winner of this monster rebound in 2021 putting the rest of the broader market on its back.

This is quickly turning into two economies – tech and everybody else.

The eyeballs won’t necessarily translate into a waterfall of revenue right away because of the nature of all the free services that they provide.

But at the beginning of 2021, a higher incremental portion of consumer’s salaries will be directed towards big tech and the fabulous paid services they offer.

Actions speak louder than words and Berkshire Hathaway’s Warren Buffett unloading billions in airline stocks is an ominous sign indicating that parts of the U.S. economy won’t come back to pre-virus levels.

The biggest takeaway in Buffet’s commentary is that he elected to not sell tech stocks like his big position in Apple validating my thesis that any investor not already in big tech will flood big tech with even more capital after being burnt in retail, energy, hotels, and airlines.

Then, when you consider the ironclad nature of tech’s balance sheets, even in the apocalyptical conditions, they will profit and rip away even market share from the weak.

It’s to the point where any financial advisor who doesn’t recommend big tech as the nucleus of their portfolios is most likely underperforming the wider market.

As the U.S. economy triggers the reopening mechanisms and we enter into the real meat and bones of the reopening, data will recover significantly signaling yet another leg up in tech shares.

Hold onto your hat!

“I want to put a ding in the universe.” – Said Co-Founder of Apple Steve Jobs

Mad Hedge Technology Letter

May 4, 2020

Fiat Lux

Featured Trade:

(AMAZON’S BIG DISAPPOINTMENT)

(AMZN), (MSFT)