Mad Hedge Technology Letter

January 24, 2020

Fiat Lux

Featured Trade:

(THE NETFLIX EARNINGS SHOCKER)

(NFLX)

Mad Hedge Technology Letter

January 24, 2020

Fiat Lux

Featured Trade:

(THE NETFLIX EARNINGS SHOCKER)

(NFLX)

Netflix is saying no to over $2 billion in extra digital ad revenue – that is the critical takeaway from Netflix’s earnings call that fell in line with exactly what I thought would transpire.

As Netflix’s domestic subscriptions continue to soften, this is the first of many earnings calls where management will be put to the sword on why they still haven’t swiveled to digital ads.

As you guessed right, Founder and CEO Reed Hastings pulled out all the usual excuses explaining why Netflix is leaving a massive chunk of revenue on the table.

Some of his evasive rhetoric came in the form of explaining there’s no “easy money” in an online advertising business that has to compete with the likes of Google, Amazon, and Facebook.

He continued to spruce up his excuses by saying, “Google and Facebook and Amazon are tremendously powerful at online advertising because they’re integrating so much data from so many sources. There’s a business cost to that, but that makes the advertising more targeted and effective. So I think those three are going to get most of the online advertising business.”

Even most peons would understand that Netflix’s network effect is so robust that they could turn on the digital ad revenue spigots with a flick of a wrist.

It doesn’t matter that there are also three other tech firms in the digital ad sphere.

Netflix certainly has the infrastructure in place and manpower laid out to harness the power lines of the digital ad game.

Hastings weirdly lamented that revenue would need to be “ripped away” from the existing providers, he continued. And stealing online advertising business from Amazon, Google and Facebook is “quite challenging.”

I don’t believe that is entirely accurate.

Dipping into that digital ad revenue would be quite challenging if you are a 2-man start-up, but the power centrifuge that has become to be known as Netflix is stark crazy for taking the high road on data privacy when the US government still allows tech companies to profit off of digital ads.

The musical chairs might stop in less than 3 years, but not now.

It’s hard to understand why Netflix isn’t approaching this as a short-term smash and grab type of business.

If they really wanted to, they could have layered each service into ads and non-ad subscriptions just like Spotify does.

If muddying their premium service is taboo, then there are alternative solutions.

I understand and agree with Hastings that delivering “customer pleasure” is the ultimate goal, but that doesn’t mean there can’t be an ad-based model as one of the options.

I believe this is a substantial letdown to the shareholder and the stock price would be closer to $500 if there was a realistic ad revenue option.

Even worse, Hasting’s argument for not delving into digital ads is flawed by saying, “We don’t collect anything. We’re really focused on just making our members happy.”

That is materially false.

Netflix already tracks loads of data and it doesn’t take a Ph.D. data analyst to ignore that when you are busy perusing the Netflix platform, Netflix’s are tracked non-stop.

Netflix uses algorithms to track user’s behavior through tracking viewership data in order to make critical decisions about which of its original programs should be renewed and which should be booted.

It also looks at overall viewing trends to make decisions about which new programs to pursue.

It then also tracks user's own engagement with Netflix’s content in order to personalize the Netflix home screen to user’s preference.

Netflix is already “exploiting users” and they are doing shareholders a massive disservice by not maximizing revenue to the full amount they can.

And yes, I do agree Netflix is not as good as Facebook, Google, and Amazon at tracking users, but the roadmap is certainly out there for Netflix to indulge in digital ads.

It would take less than 18 months for Netflix to be running on full cylinders if they poached a few experts.

Aside from the lack of digital ads, Netflix finally is starting to acknowledge the new competition from two major streaming services, Disney+ and Apple+ — both of which have subsidized their launch with free promotions in order to gain viewership.

Then it gets worse with streaming service Quibi, WarnerMedia’s HBO Max and NBCU’s Peacock rolling out.

The latter features a multi-tiered business model, including a free service for pay-TV subscribers, an ad-free premium tier and one that’s ad-supported.

Other TV streaming services also rely on ads for revenue, including Hulu and CBS All Access. Meanwhile, a number of ad-supported services are also emerging, like Roku’s The Roku Channel, Amazon’s IMDb TV, TUBI, Viacom’s Pluto TV, and others.

Considering much of Netflix’s rise is fueled on debt, it’s bonkers they aren’t going after every little bit of revenue that is there for the taking.

Netflix could lose 4 million subscribers this year, and sooner or later, Hastings will run out of places to hide.

Slowing domestic subscriber growth and bad guidance don’t sound like a roaring growth tech stock to me.

“If the Starbucks secret is a smile when you get your latte... ours is that the Web site adapts to the individual's taste.” – Said Founder of Netflix Reed Hastings

Mad Hedge Technology Letter

January 22, 2020

Fiat Lux

Featured Trade:

(THE HOLLOW VICTORY FOR TECH IN THE CHINA TRADE DEAL)

(MSFT), (AMZN), (HUAWEI)

The Davos World Economic Forum is the optimal place to get a snapshot of the state of the American technology sector and apply its underpinnings to an overall trading strategy for 2020.

Stepping back, one clear theme is the lasting effects of the trade war and how that will manifest itself in the broader tech sector.

We got some serious sound bites from CEO of Microsoft Satya Nadella at Davos who is convinced that mutual economic saber-rattling between the US and China will show up in higher costs because of the misallocation of resources.

The most critical point of contention is the development in the semiconductor space as we move into the 5G world and this $470 billion industry which realizes cost savings from scaling by global supply is splintering off as we speak into two separate industries.

This just translates into higher costs to source components for your Microsoft Surface laptop or your Apple Ear Buds.

The follow-through effect is ultimately bludgeoning global growth rates and tech intermediaries will be forced to pick up the extra tab or face the looming decision to pass costs on to the consumer.

As we move forward, the administration is considering more limits to US semiconductor companies’ access to the Chinese consumer market.

The scaremongering fueled by the rise and threat of Huawei has reached fever pitch.

Remember that even with the aggression of the American administration hoping to cap Huawei’s revenue explosion, Huawei still managed to grow sales 18% last year to $122 billion.

I can tell you that if the U.S. administration came after the Mad Hedge Technology Letter guns blazing, we wouldn’t be sitting here growing 18% annually!

The U.S. administration hasn’t stopped at Huawei and is putting in shifts attempting to convince other nations to avoid using Chinese infrastructure equipment for the 5G revolution.

The “Phase One” of the trade agreement is largely seen as a moot point in the technology community and in some cases can be argued as a net negative to component makers whose access to the local Chinese market has narrowed.

The agreement signed also delivered no meaningful protection to intellectual property for US technology companies working with China which was largely viewed as the main catalyst provoking a geopolitical fight.

The trade war has sped up the bifurcation of internets, better known as “splinternet,” and I believe that sometime in the near future, you will need to download Chinese software and platforms to function inside of China.

Much of these misunderstandings stem from the lack of trust that has accumulated between the two parties.

The American tech sector and Wall Street have indirectly subsidized China’s technological rise to this point and now they must go head-to-head in every future technology such as artificial intelligence, 5G, fintech, augmented reality, and virtual reality.

This appears to be the new normal - a frosty and adversarial tech relationship.

There is now zero good will between each other.

The trust of tech on American shores could almost be ironically argued that it is worse than the trust level with China.

Edelman’s 20th annual trust barometer surveyed more than 34,000 adult respondents in 38 markets around the world.

It found that 61% of participants said the pace of change in technology is too fast and government does not fully understand emerging technologies enough to regulate them efficiently.

Trust in tech from 2019 to 2020 declined the most significantly in France, Canada, Italy, Russia, Singapore, the U.S. and Australia.

Much of the narrative has been about the domination of American tech by a handful of actors that has seen American companies go up against foreign governments.

France and America recently announced a temporary truce after the French President Emmanuel Macron reached out by phone to President Trump hoping to end the threat of tariffs while they work out a broader accord on digital taxation.

The French leader agreed to postpone until the end of 2020 a tax that France levied on big tech companies last year and in turn, the U.S. will delay the counter-tariffs that were in the works set to be levied on the French.

And it’s not just the French.

India has taken heed from the brooding trouble between the encroachment on sovereignty and American tech giants by adopting an aggressive stance towards Amazon.

Amazon CEO Jeff Bezos' lowlight of a recent India work trip came in the form of being snubbed by the Indian government.

India’s commerce minister Piyush Goyal said, “It’s not as if they (Amazon) are doing a great favor to India when they invest a billion dollars.”

He called Amazon a capital guzzler equating its mounting losses up to “predatory pricing or some unfair trade practices.”

India is on the verge of turning protectionist on foreign tech and this flies in the face of the tech atmosphere even just a few years ago.

Governments have come to realize that America’s FANGs are too dominant and entrenched often resulting in a net negative to the local populace.

More often than not, American tech found ways of rerouting local revenue to coffers of a few billionaires while paying zero local tax.

The easy money has been made and now the Tim Cooks and Sundar Pichais of the world will have to fight tooth and nail with not only the U.S. antitrust regulators, but foreign governments.

This is why a handful of tech companies this dominant has been the outsized winners over the past generation as their share prices have gone from the lower left to the upper right but now command minimal consumer trust.

The ultimate Davos message is that big tech continues to grind higher, but alarm bells have started to ring.

There’s only so much friction they can handle before investors pull the rug.

“We also welcome any regulation that helps the marketplace not be a race to the bottom.” – Said CEO of Microsoft Satya Nadella

Mad Hedge Technology Letter

January 17, 2020

Fiat Lux

Featured Trade:

(WHY ZOOM IS ZOOMING)

(ZM)

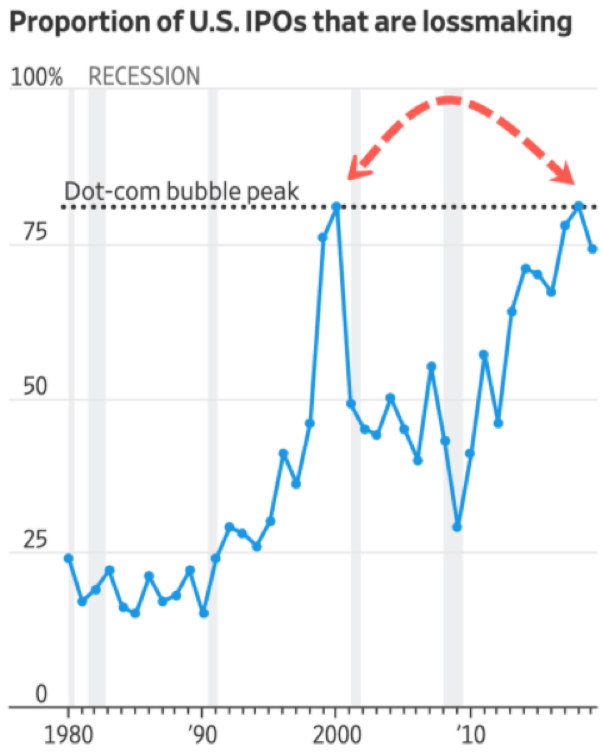

A report from a prominent new source reveals that in the past 12 months, 40% of all US-listed companies were losing money and of these, 17% were tech firms, the highest level since the Dot Com bubble.

That is why software gems like Zoom Video Communications, Inc. (ZM) should be bought and held, never to see the light of day ever again.

The company makes money at such an early stage of their development that it's hard not to get excited about the future.

Readers can indulge themselves in this high caliber tech growth stock, especially after they demonstrated that they are hitting on all cylinders after a high-flying earnings report.

Another prominent new source recently said that this company’s products are “changing the entire landscape” of U.S. business.

Just one instance they have infiltrated deep into real American business is the U.S. Postal Service.

They are starting to deploy Zoom Meetings more broadly across the organization after an extensive proof-of-concept.

The USPS is Zoom’s first major agency and major business win since they received FedRAMP approval in May.

Why did they pick Zoom?

Easy! Simply for Zoom’s high-quality video and audio.

Zoom’s share price cratered 40% since hitting the heights of $102 in July 2019 which was coincidentally the high for most post-IPO tech stocks of 2019.

It was an elevator straight down to no man’s land – but investors would be foolish to paint all hyper-growth companies with the same brush.

Filtering out the wheat from the chaff is critical and Zoom is the stock that still has the gloss on its outside package buttressed by its best-in-show video conferencing software.

There are no other proper alternatives in this sub-sector of software.

The volatility can be extreme making this name difficult to trade and constantly has dips of 7% even though the company crushes expectations.

I called for readers to scoop up shares in the low $60s and the stock is now healthily trading in the upper $70s as we hit the back half of January.

Remember that this company grew 96% just 3 quarters ago and it would be illogical to believe that the stock is being penalized from faltering to 85% today.

The report on January 6th showed a strong quarter as evidenced by a combination of high revenue growth of 85%, with increased profitability and free cash flow of $54.7 million.

They continue to have success with customers of all sizes and one metric that has continued to stick out is customers with more than $100,000 of trailing 12 months revenue – that metric grew 97% from Q3 last year.

Any tech company would give a left thigh for 85% growth in this climate which is why many have resorted to inorganic growth.

Buying growth is not necessarily a bad strategy now but buying growth at this point in the economic cycle naturally means that companies will need to overpay for growth because of expensive valuations.

Zoom is perfectly positioned to outperform in the next 1-3 years.

The advancing runway is wide open with no competition in sight and a generous growth trajectory is firmly on their side.

At some point, this software company could become a takeover target for a larger corporate.

I am impressed with Zoom's superior products, growth prospects, and scalable business model, and the stock’s near-term risk/reward trade-off is mildly bullish after the jump from $62.

There is an actionable and manageable clear path to a $2 billion revenue run rate with strong margin expansion potential and with its flagship product growing around 80-90%, its next growth driver in Zoom Phone could translate well into a meaningful revenue stream.

Zoom Phone is the next springboard to further success for this company, meaning there won’t be any cliff edge with future revenue streams.

Anyone that has used Zoom as a product can confirm the veracity of its superior performance standards.

This isn’t the type of stock to trade short-term - the volatility undermines any potential entry points.

If the broader market holds up in 2020, Zoom’s value extraction potential is substantially robust, and shares should reach $90.

Growth stocks can only be pinned down for so long before the beast is unleashed.

Buy this stock on any short-term dip.

“Success is a lousy teacher. It seduces smart people into thinking they can't lose.” – Said Founder of Microsoft Bill Gates

Mad Hedge Technology Letter

January 15, 2020

Fiat Lux

Featured Trade:

(THE TRADE ALERT DROUGHT EXPLAINED)

(GOOGL), (AMZN), (MSFT), (FB), (JPM)