Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(WHY YOU CANNOT NEGLECT THE CLOUD)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(WHY YOU CANNOT NEGLECT THE CLOUD)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Cloud stocks should be at the vanguard of your tech portfolio, no ifs, ands, or buts.

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 15% and is rapidly zeroing in on Amazon Web Services (AWS).

Amazon leads the cloud industry it created which is partly why the first-mover advantage is so effective.

It still maintains more than 30% of the cloud market and Microsoft still needs to gain a lot of ground to even come close.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes the lion’s share of Amazon's total operating income.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products, most notably the iPhone and iPad.

The future is about the cloud.

These days, the average venture capitalist probably hears about the cloud 100 times a day.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to dramatic investment opportunities.

And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside imposing data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even collaborate in real-time, making it the perfect force multiplier in our globalized world.

Once you start using the cloud to store a company's data, the benefits are countless.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can divert resources on the core aspects of their business where they can increase value without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved through telecommuting. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I shoot off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees while boosting performance.

According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way, a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document, so they can stay on top of real-time changes which can help businesses to better manage workflow regardless of geographical location.

Another important reason to move to the cloud is superior data security, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down operations for days.

The cloud simply routes traffic around disaster zones as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud to avoid such disruptions.

Even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can slash expenses fast.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, resources that in turn can be used to expand the business. Setting up an in-house data center requires millions, and that's not to mention perpetual maintenance costs.

Creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

“Life is not fair; get used to it.” Said founder of Microsoft Bill Gates.

Mad Hedge Technology Letter

December 23, 2019

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND WALL STREET JOBS)

Automation is taking place at warp speed displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the direct capital of $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. bank jobs getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

Mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificial engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

Front-office staff have already felt the brunt of downsizing with purges carried out in 2018 representing a fifth year of decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 20% and the accumulation of hordes of data will advance the marketing effort into a smart, hybrid cloud-based and hyper-targeted strategy.

Historically, a strong labor market and low unemployment boost wage growth, but national income allocated to workers has dipped from about 63% in 2000 to 56% in 2018.

Causes stem from the deceleration in union membership and outsourcing has snatched away negotiating power amongst workers and the implemented mass automation has poured fat on the fire.

I was recently in Budapest, Hungary on a business trip and on a main thoroughfare, a J.P. Morgan and Blackrock office stood a stone’s throw away from each other employing an army of local English-proficient Hungarians for 30% of the cost of American bankers.

Banks simply possess wider optionality to outsource to an emerging nation or to automate hard-to-fill positions now.

In this race to zero, companies can easily rebuff requests for higher salaries and if they threaten to walk off the job, a robot can just pick up the slack.

Automation is getting that good now!

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies are chomping at the bit and even tech companies like Amazon and Apple have started tinkering with new financial products.

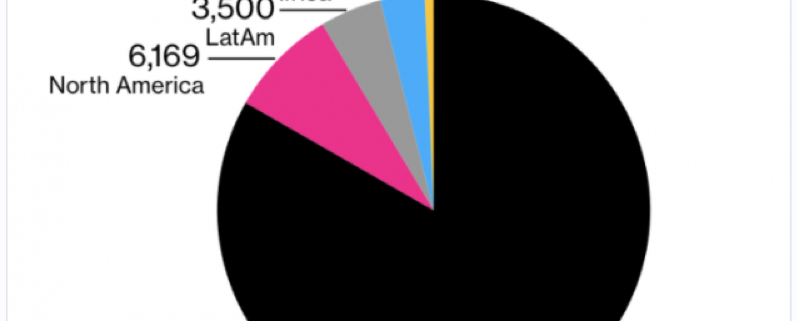

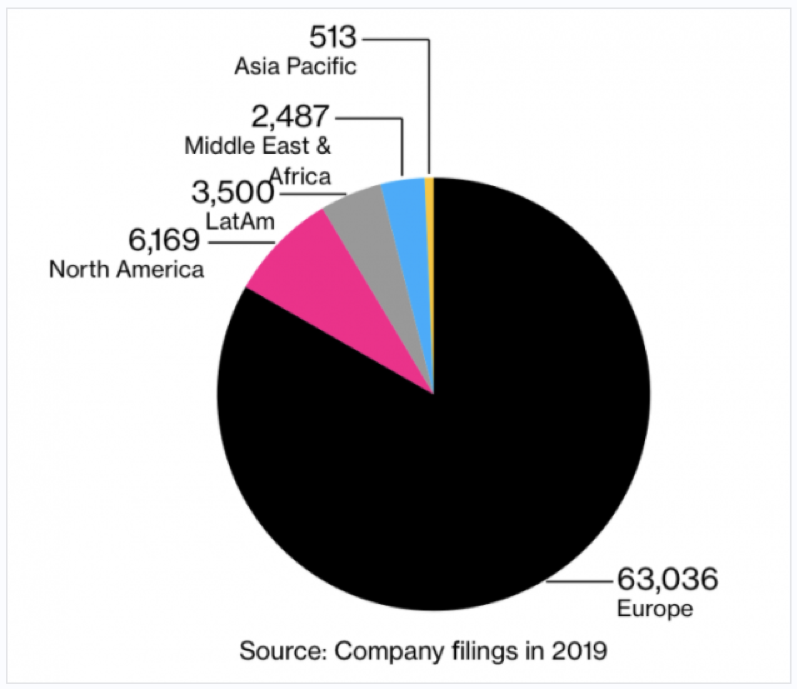

And if you thought this phenomenon was limited to the U.S., think again. Europe is by far the biggest culprit by already laying off 63,036 employees in 2019, more than 10x higher the number of U.S. financial job losses.

In a sign of the times, the European outlook has turned demonstrably negative with Deutsche Bank announcing layoffs of 18,000 employees through 2022 as it scales down its investment banking business.

Germany banks are also passing on the burden of negative interest rates to their clients.

A recent survey by Deutsche Bundesbank shows that 58% of banks are charging all savers negative interest rates while others only target wealthy and corporate clients.

If the U.S. dips into negative rates in the future, expect the same nasty effect on job force cuts that Europe has experienced.

Either way, don’t tell your kid to get into banking because they will most likely be feeding on scraps in the future.

Mad Hedge Technology Letter

December 20, 2019

Fiat Lux

Featured Trade:

(THE BIG TECH TRENDS OF 2020)

(AAPL), (GOOGL), (FB), (AMZN), (NFLX)

The year is almost in the rear-view mirror – I’ll make a few meaningful predictions for technology in 2020.

Although iPhones won’t go obsolete in 2020, next year is shaping up as another force multiplier in the world of technology.

Or is it?

A trope that I would like to tap on is the severe shortage of innovation going on in most corners of Silicon Valley.

Many of the incumbents are busy milking the current status quo for what it’s worth instead of targeting the next big development.

Your home screen will still look the same and you will still use the 25 most popular apps

This almost definitely means the interface that we access as a point of contact will most likely be unchanged from 2019.

It will be almost impossible for outside apps to break into the top 25 app rankings and this is why the notorious “first-mover advantage” has legs.

The likes of Google search, Gmail, Instagram, Uber, Amazon, Netflix and the original list of tech disruptors will become even more entrenched, barring the single inclusion of Chinese short-form video app TikTok.

The FANGs are just too good at acquiring, cloning or bludgeoning upstart competitors.

It’s the worst time to be a consumer software company that hasn’t made it yet.

Advertising will find itself migrating to smart speakers

Amazon and Google have blazed a trail in the smart speaker market but ultimately, what’s the point of these devices in homes?

Exaggerated discounting means hardware profits have been sacrificed, and the lack of paid services means that they aren’t pocketing a juicy 30% cut of revenue either.

These companies might come to the conclusion that the only way to move the needle on smart speaker revenue is to infuse a major dose of audio ads to the user.

So if you are sick to your stomach of digital ads like I am, you might consider dumping your smart speaker before you are forced to sit through boring ads.

Amazon’s Alexa will lose momentum

In a way to triple down on Alexa, Amazon has installed it into everything, and this is alienating a broad swath of customers.

Not everyone is on the Amazon Alexa bandwagon, and some would like Amazon’s best in class products and services without involving a voice assistant.

Privacy suspicion has gone through the roof and smart speakers like Alexa could get caught up in the personal data malaise dampening demand to buy one.

Your voice is yours and 2020 could be the first stage of a full onslaught of cyber-attacks on audio data.

Don’t let hackers steal your oral secrets!

Cyber Warfare and AI

Hackers have long been experimenting with automatic tools for breaking into and exploiting corporate and government networks, and AI is about to supercharge this trend.

If you don’t know about deep fakes, then that is another thorny issue that could turn into an existential threat to the internet.

Not only could 2020 be the year of the cloud, but it could turn into the year of cloud security.

That is how bad things could get.

A survey conducted by Cyber Security Hub showed 85% of executives view the weaponization of AI as the largest cybersecurity threat.

On the other side of the coin, these same companies will need to use AI to defend themselves as fears of data breaches grow.

AI tools can be used to detect fraud such as business email compromise, in which companies are sent multiple invoices for the same work or workers duped into releasing financial information.

As AI defenses protect themselves, the sophistication of AI attacks grows.

It really is an arms race at this point with governments and private business having skin in the game.

Facebook gets out of the hardware game because consumers don’t trust them

Remember Facebook Portal – it’s a copy of the Amazon Echo Show.

The only motive to build this was to bring it to market and expect Facebook users to adopt it which backfired.

Facebook will find it difficult convincing users to use more than Facebook and Instagram software apps.

Don’t wait on Facebook to roll out some other ridiculous contraption aimed at stealing more of your data because there probably won’t be another one.

This again goes back to the lack of innovation permeating around Silicon Valley, Facebook’s only new ideas is to copy other products or try to financially destroy them.

China continues to out-innovate Silicon Valley.

The rise of short-form video app TikTok is cementing a perception of China as the home of modern tech innovation, partly because Silicon Valley has become stale and stagnated.

China has also bolted ahead in 5G technology, fintech payment technology, unmanned aerial vehicle (UAV) and is giving America a run for their money in AI.

China’s semiconductor industry is rapidly catching up to the US after billions of government subsidies pouring into the sector.

Silicon Valley needs to decide whether they want to live in a tech world dominated by Chinese rules or not.

Augmented Reality: Is this finally the real deal?

Augmented reality (AR) is still mainly used for games but could develop some meaningful applications in 2020.

Virtual Reality (VR) and AR will play a big role in sectors such as education, navigation systems, advertising and communication, but the hype hasn’t caught up with reality.

One use case is training programs that companies use to prepare new workers.

However, AR applications aren't universally easy or cheap to deploy and lack sophistication.

AR adoption will see a slight uptick, but I doubt it will captivate the public in 2020 and it will most likely be another year on the backburner.

Apple’s New Projects

Apple has two audacious experimental projects: a pair of augmented-reality glasses and a self-driving car.

The car, for now, has no existence outside of a few offices in California and some hires from companies like Tesla.

And, at the earliest, the glasses won’t hit shelves until 2021,

The car is likely to fizzle out and Apple will be forced to double down on digital content and services to keep shareholders happy which is typical Tim Cook.

The 5G Puzzle

Semiconductor stocks have been on fire as investors front-run the revenue windfall of 5G and the applications that will result in profits.

Select American cities will onboard 5G throughout 2020, but we won’t see widespread adoption until later in the year.

5G promises speeds that are five times faster than peak-performance 4G capabilities, allowing users to download movies in five seconds.

With pitiful penetration rates at the start, the technology will need to grow into what it could become.

The force multiplier that is 5G and the high speeds it will grace us with probably won’t materialize in full effect until 2021.

Each of the nine tech developments in 2020 I listed above negatively affects US tech margins and that will follow through to management’s commentary in next year’s earnings and guidance.

Tech shares are closer to the peak and the bull market in tech is closer to the end.

Innovation has ground to a halt or is at best incremental; companies need to stop cloning each other to death to grab the extra penny in front of the steamroller.

Profit margins will be crushed because of heightened regulation, transparency issues, monitoring costs, and the unfortunate weaponizing of tech has been a brutal social cost to society.

Tech is saturated and waiting for a fresh catalyst to take it to the next level, but that being said, tech earnings will still be in better shape than most other industries and have revenue growth that many companies would cherish.

“History rarely yields to one person, but think and never forget what happens when it does.” – Said CEO of Apple Tim Cook

Mad Hedge Technology Letter

December 18, 2019

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL A BUY)

(SYMC), (PANW), (CSCO), (FTNT), (AAPL), (MSFT)

What does the technology sector’s “last gasp up” mean for tech stocks?

At the Mad Hedge Lake Tahoe Conference in late October, I correctly identified that the tech sector would experience a last leg to the price appreciation that has been part of a broader 10-year bull market in American equities.

The past 7 weeks have been nothing short of spectacular for tech shares as not only have the heavy hitters delivered in spades, like Apple (AAPL) and Microsoft (MSFT), but tech growth shares have been released from the penalty box after a short-dated growth scare and joined the rally with zeal.

How long will the “last gasp up” last?

The bar was set exceptionally low in 2019 because senior management spun the trade war acrimony into the accounting calculus effectively offering CFOs a chance to lower expectations to the point of getting away with murder.

Even with earnings’ expectations reset at nadir data points, performance was a mixed bag.

Superior tech companies were able to jump over the pitiful expectations, then if that wasn’t enough, they pushed backwards any inklings of earnings growth by guiding as low as they possibly could.

An archetypal example is Palo Alto Networks (PANW) whose shares dipped more than 8.5% in pre-market trading after issuing their quarterly earnings report.

The company announced sales of $771.9 million with an adjusted EPS of $1.05 topping analysts' estimates.

Why did shares sully?

Palo Alto Networks tanked guidance by telling investors they expect sales between $838 million and $848 million in the second quarter.

The expectation represented a midpoint sales forecast of $843 million, which is lower than the consensus estimates of $845.12 million.

The adjusted EPS in the second quarter is estimated to be $1.11–$1.13, below the consensus earnings forecast of $1.30.

Palo Alto Networks is forecasting sales between $3.44 billion and $3.46 billion with an EPS between $4.9 and $5.0 for next year, compared to analyst projections of $3.46 billion in revenue and an EPS of $5.07 in 2020.

PANW accounts for a big piece of the pie in the cybersecurity trade comprising 16.2% in 2019.

Overall industry growth is strong at 10.4%, and PANW managed to increase its sales by 22.3% to $633.7 million.

This cybersecurity company is one of my favorite tech stalwarts and is as rock-solid as they come for a second-tier tech growth company.

Another trend that dovetails closely with the last gasp up thesis is buying growth.

At this stage in the tech cycle, the low hanging fruit has been plucked and tech companies are increasingly finding it hard to generate organic growth.

Companies are now resorting to inorganic growth with Palo Alto Networks announcing that it will acquire Aporeto for $150 million in an all-cash transaction.

This isn’t just a one-off for PANW, they have acquired four other companies in 2019 to plug into their growth puzzle.

They have also completed the acquisition of an IoT cybersecurity firm Zingbox.

Palo Alto Networks acquired two cloud security startups in July as well - Demisto to gain traction in the AI security segment and Twistlock, the leader in container security.

The other top players in this field are Cisco (CSCO), Fortinet (FTNT) and Symantec (SYMC).

The bullish secular trend in cybersecurity is watertight and comments from Nikesh Arora, CEO of Palo Alto Networks, only reconfirmed the strength in cybersecurity when he said, “As a growing number of organizations move their business to the cloud, developers increasingly rely on cloud-native technologies such as containers and serverless infrastructure to accelerate the development, testing, and deployment of modern applications and services.”

What’s next for investors?

Barring any exogenous shocks, the last gasp up continues and recent macro policy developments have supported this hypothesis as well as the tailwinds of an improving economy.

Palo Alto Networks is part of a high growth segment and many corporates are on record contemplating lower enterprise tech spending heading into 2020.

This sets up another incredibly low bar for cybersecurity companies to hop over next year and I believe the best in show such as PANW, Fortinet, Cisco, and Symantec will pass with flying colors.

The interesting acid test will occur at the end of 2020 when tech firms and sub-segments of tech such, as cybersecurity, release commentary on whether 2021 guidance could signal ensuing risk of being dragged into recessionary turbulence.

A 2021 tech sector recession is certainly not priced into current tech share valuations in this frothy period of asset appreciation.