"The greatest enemy of knowledge is not ignorance, it is the illusion of knowledge," said the late Professor Stephen Hawking.

"The greatest enemy of knowledge is not ignorance, it is the illusion of knowledge," said the late Professor Stephen Hawking.

Mad Hedge Technology Letter

October 21, 2019

Fiat Lux

Featured Trade:

(THE CLOUD BASICS)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry and still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley, you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at anytime from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies regardless of their size prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

"Life is not fair; get used to it," said the founder of Microsoft Bill Gates.

Mad Hedge Technology Letter

October 18, 2019

Fiat Lux

Featured Trade:

(THE ROAD OUT OF SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

In a new study, 44% of Millennials plan to move out of the Bay Area in the “next few years.”

In the same study, 8% of Millennials will move out of the Californian tech peninsula within the next 365 days.

Tech companies are in serious danger of stagnating because they won’t be able to hire the talent needed to keep their companies afloat while the number of foreign HB-1 visas has dried up.

All of this could come home to roost and early cracks can be found in the local housing migratory trends.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money has made living with a roof over your head a tall order.

The area has also become squalid like some third world countries due to the homeless problem that is growing faster than any software company.

Salesforce Founder and CEO Marc Benioff has lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing forever.

He has also urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as government policy stiffens.

I have walked around the streets of San Francisco myself.

Places around Powell Bart station close to the Tenderloin district are eyesores littered with used syringes that lay in the gutter.

South of Market Street (SoMa) isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there anymore.

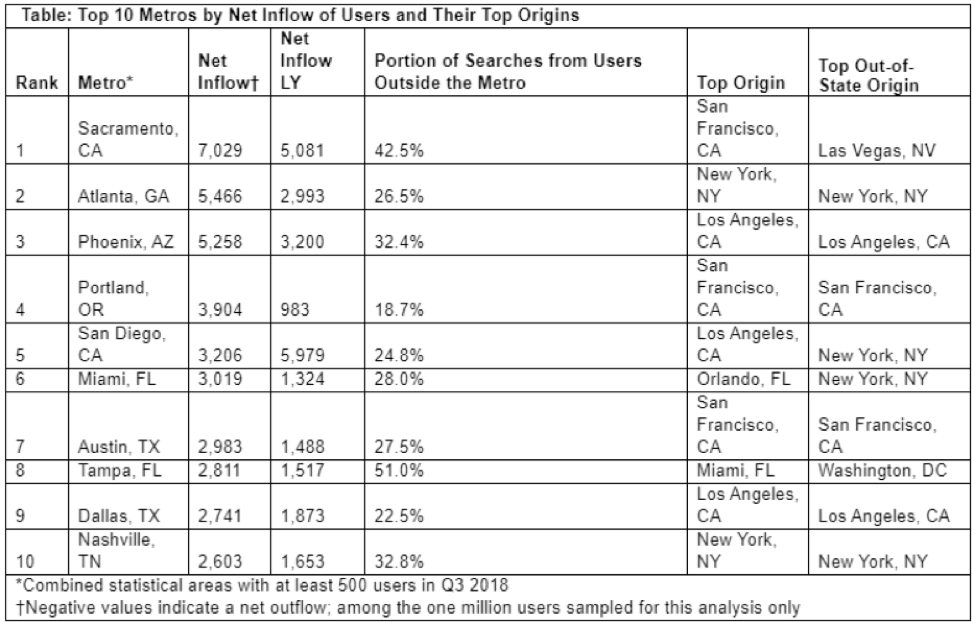

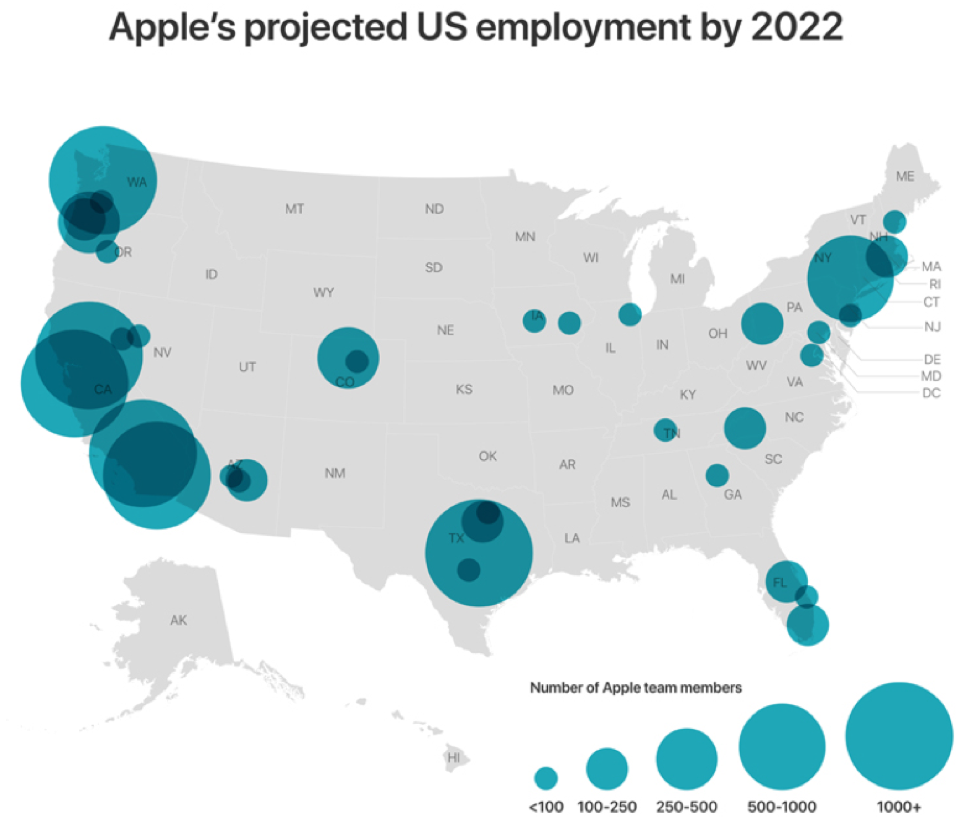

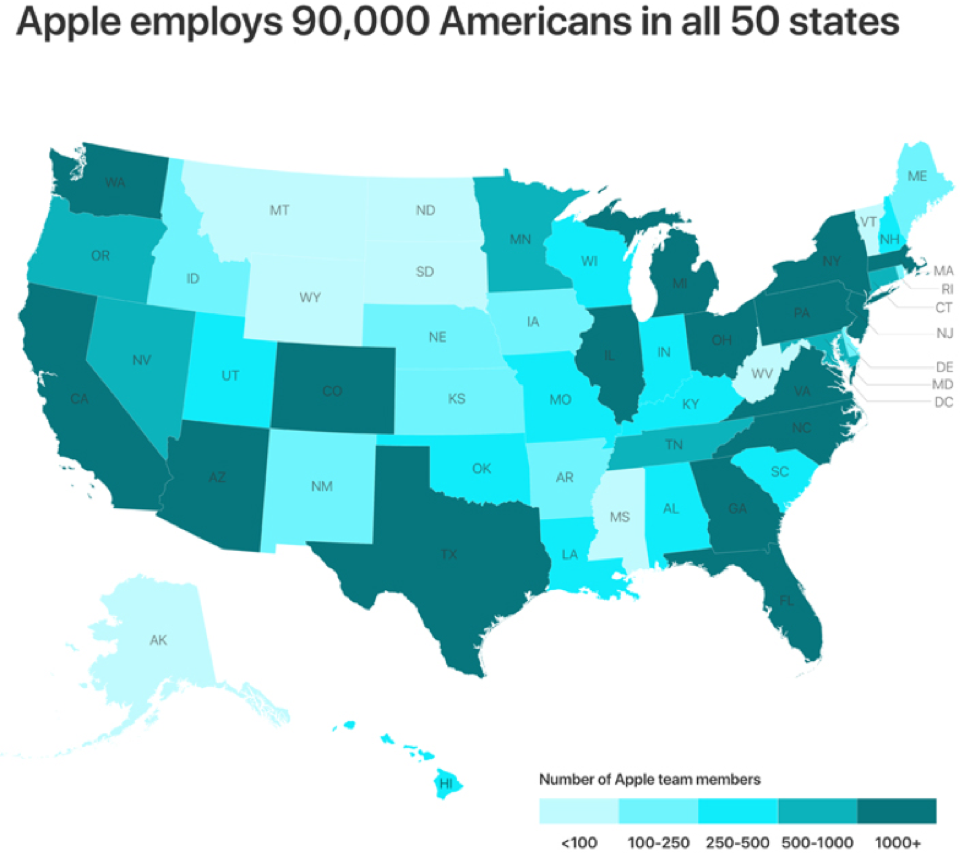

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas, and Amazon adding 500 employees in Nashville, Tennessee are all about.

Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Jobs simply flock to where the talent is.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area escaping the sky-high housing.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to take the first step onto the property ladder.

These are some of the practical issues that tech has failed to address, and part of the problem with unfettered capitalism which doesn’t consider quality of life.

No wonder why Silicon Valley real estate has dropped in the past year, people and their paychecks are on the way out.

Mad Hedge Technology Letter

October 16, 2019

Fiat Lux

Featured Trade:

(IS 3D PRINTING A WASTE OF SPACE?)

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

If you need a new investment theme – here’s one.

3D printing.

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

Believe me, I’ve been there and done that.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology like e-commerce company Etsy (ETSY) who focuses on personalized handcrafts.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was tedious.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can be Super Bowl quarterback Tom Brady.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is heaps better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand, but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are percolating together at the perfect time.

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in its infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in perfect in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus - 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could potentially consist up to 25% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins close to 60%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a multi-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 is applying a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE has already started mass production of the 3D printed brackets at its Auburn, Alabama facility.

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

As it stands, Stratasys is the industry leader in this field and if you believe in this long term then this stock would be for you.

It’s nonetheless still a speculative punt but a compelling pocket of the tech industry.

“Capitalism has worked very well. Anyone who wants to move to North Korea is welcome.” – Said Founder and Former CEO of Microsoft Bill Gates

Mad Hedge Technology Letter

October 14, 2019

Fiat Lux

Featured Trade:

(WHAT IS AUTONOMOUS DRIVING REALLY WORTH?)

(WAYMO), (UBER)