Mad Hedge Technology Letter

April 1, 2019

Fiat Lux

Featured Trade:

(THE NEXT TECH BUBBLE TOP HAS STARTED)

(LYFT), (PIN), (UBER), (AAPL), (JPM), (FB)

Mad Hedge Technology Letter

April 1, 2019

Fiat Lux

Featured Trade:

(THE NEXT TECH BUBBLE TOP HAS STARTED)

(LYFT), (PIN), (UBER), (AAPL), (JPM), (FB)

Don't go chasing rainbows.

That is what the current tech IPO environment is hinting.

Even though market conditions are frothy, that doesn't mean I'm calling a market top today, hardly so.

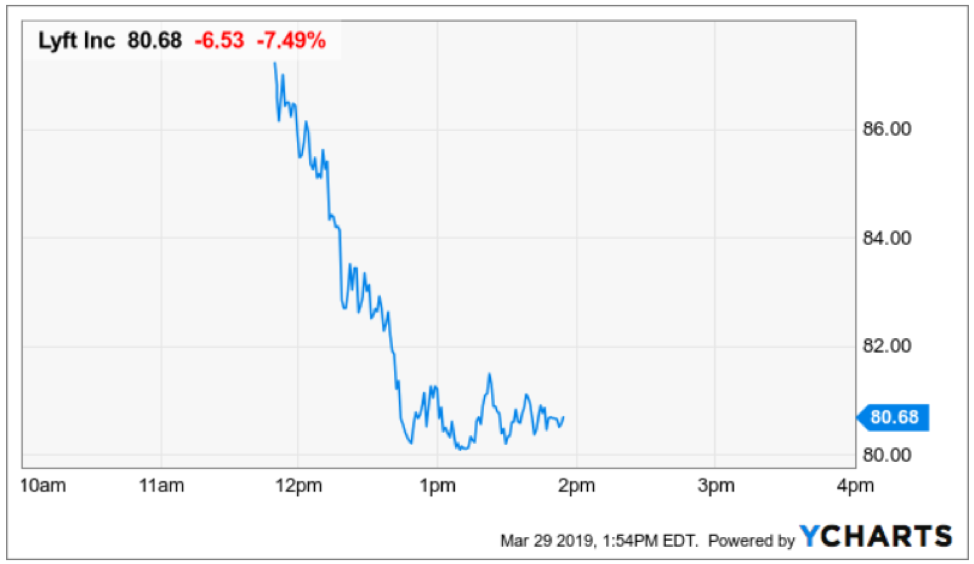

I predicted that Lyft (LYFT) would storm out of the gate like a bull on ecstasy, and I was vindicated when the stock flirted intraday with the $87 mark.

The scarcity value of these gig economy companies is hard to quantify.

Examples Uber unduly promise ambition and innovation leading to hopes of a possible air transport service and sharing network that I would need to see to believe.

The built-up expectations smell of over-promising and under-delivering, the majority won’t be able to deliver merely half of what their manifestos promulgate

As I put my analyst hat on, the 2019 IPO frenzy coming online has some of the same fingerprints of the infamous dot com bust of 2001.

The two main trends symbolic of the last time the tech industry disentangled were overly generous valuation, pricing in revenue expansion of 80% for the next five years when the leader of the pack Microsoft (MSFT) only grew at 50%.

A tantalizing clue was the utterly deficient cash flow generated back then.

The underlying premise revolved around putting the network effect on a pedestal irrespective of understanding that the network effect should have caused cash flow to accelerate which was conspicuously absent.

Losing money and losing a lot of it does lead to paralysis, examples were rife, for instance, priceline.com losing $30 on each air ticket sold.

Even more hard to fathom was that Priceline was stretching itself to the limits on the open market filling ticket orders because of a dearth of inventory steepening losses.

Priceline gushed about a unique business model of collecting excess ticket inventory that airlines couldn't sell at low cost and reskinning them to a digital audience hoping to take advantage of this price dispersion.

But in reality, this wasn’t always the case.

Priceline was on a suicide mission and expanding from 50 employees to 300 employees based upon misleading growth was madness.

In a nutshell, investors bypassed pragmatic arithmetic and were lifted by the fumes of exuberance that had manifested around the euphoria of the tech bubble.

Lyft is not revolutionary, they are a broker which occupy a low position in the spectrum of tech intellectual property.

Exploiting drivers, compensating them per hour, and letting them figure out their own cost structures for car insurance, fuel costs, and opportunity cost while offering zero benefits is a court battle waiting to happen in California.

And if your response was the way they craft value is by way of a proprietary app, well, Google, Apple, or even Netflix can produce the same type of app and quality of app in a few weeks with their legendary phalanx of top-tier engineering talent.

To Lyft’s credit, they have at least collected the treasure trove of data the app has compiled which is extraordinarily valuable.

The top of the tech bubble means that big tech is overreaching into any revenue they can get their hands on like a heroin addict yearning for the next syringe.

The environment has transformed into an eerily zero-sum game, such as Apple (AAPL) cooperating with JPMorgan Chase (JPM) to create Apple pay, and then instantly flipping around to compete with JPMorgan Chase in the credit card space with Apple Pay being an accomplice.

Big tech has sown the seeds of discord by quietly attempting to trample on any analog business they can get near.

Leveraging the network effect of billions of users in a proprietary walled garden to extract the incremental dollar for a new service is impossible to compete with for analog companies without a similar embedded on-demand audience.

Lyft co-founder and CEO Logan Green mentioned in an interview that in the next five year, he plans to deploy a subscription service coined as transportation-as-a-service like a software-as-a-service option which cloud platforms sell.

A fight to the bottom with Uber will cause major disruption in the pricing mechanisms of the subscription service and could force Lyft to earn less revenue per ride than the current pricing system.

Investors need to remember that Uber is bigger than Lyft and possessed more ammunition.

At the end of the day, the race to the bottom is never good for profitability or sustainability, and Lyft has yet to provide any substantial clues on how they will navigate through this quagmire.

My guess is that Lyft will have to do a deal with the devil of sorts to slang its branded broker app onto the cresting wave of Waymo as Waymo motors ahead and starts to materially monetize its self-driving program.

Remember that Alphabet already has a small stake in Lyft and these two could partner up with Alphabet dictating terms.

Lyft cannot compete with the holy grail of tech - self-driving technology – they are way down the tech value chain.

If we look at the bigger picture, the broader market has been riding the coattails of Federal Reserve Chairman Jerome Powell’s 180-degree turn from winter’s statement that interest rate tightening was on “autopilot.”

Now, there is only a 27% chance given by the market that the Fed will raise rates at all in 2019.

The market responded with strength begetting strength allowing the bull run to continue and even whispers of a possible rate cut later this year.

Sentiment will not change until we get to the point when earnings can’t surpass the expectation which have been lowered substantially.

I bet this won’t happen until late this year or next year.

This is inning 8 or 9 of the bull crusade, the closer is warming up in the bullpen.

Lyft’s opening day gallop is just one of the side effects from a market that is toppy.

“Our goal was to completely change transportation. Change traffic. And make it possible to get anywhere you want to go without owning a car.” – Said Lyft Co-Founder and CEO Logan Green

Mad Hedge Technology Letter

March 28, 2019

Fiat Lux

Featured Trade:

(MACDONALD’S GOES HIGH TECH)

(MCD)

If McDonald's is using more technology, then maybe your company should be using more too.

In its most dynamic deal since divesting from Chipotle (CMG) in 2006, McDonald’s acquired artificial intelligence software company Dynamic Yield.

The company is an Israeli startup specializing in software that customizes content to the user.

The result of this ramp up in technology means that your McDonald's experience is about to improve, become easier and faster.

This is not your father’s McDonald’s.

At handpicked locations in America last year, McDonald's tested the artificial intelligence software which provides functions such as cross-selling different items on a sidebar and taking into consideration the current weather and time of day.

For example, on hot summer days the machine learning software will most likely recommend colder items such as desserts and soft drinks, and on colder days lean towards a hotter, more filling option.

Another likely consequence is after choosing a full meal of some sort, the software will further prompt the customer of the choice of popular à la carte items via the sidebar.

The theme of digital transformation is upon us and following the lead of other fast food companies such as Domino's Pizza (DPZ) will make operations more efficient and appeal to different segments of society.

The decision to gentrify and digitize the customer experience could be a result from a stagnating fast food industry that is in a price war down to the bottom.

Did you know you that you can buy 10 chicken nuggets for $1 at Burger King now?

Or even a simple cocktail at Applebee's for just $1?

QSRs (quick service restaurants) have lagged posher establishments caused by the cutting down of immigration and the struggling of the low-income class that is squeezing out fast food restaurants’ go-to clientele base.

And as construction rates have crashed because of the surging material costs induced by tariffs and a lack of foreign workers, McDonald's has been forced to look to replace demand.

Construction workers are a healthy portion of McDonald’s domestic lunch demand.

Not only is foot traffic being affected, but the fast food industry in America is saturated and funnily enough, when I travel to Europe every summer, this is one of the first comments I get from the Europeans.

The drive-thru menu will be one of the primary beneficiaries of this new software, and the projected enhancement of customer satisfaction should drive higher retention rates.

McDonald's plans to roll out kiosks that self-serve customers which is one stop on the way to a fully automated experience.

In the next 5 or 10 years, there might be only one or two McDonald's employees running a franchise.

McDonald's is clearly trending towards reducing employee headcount evident in their strategy of deciding to halt lobbying efforts to bring down the minimum wage.

Genna Gent, McDonald’s Vice President of U.S. government relations, went on record sharing that “outlets owned by the company have an average starting wage that exceeds $10 per hour.”

Most fast-food companies would be frightened to discover the House Committee on Education and Labor advanced a bill earlier this month to increase the minimum wage from $7.25 to $15 per hour by 2024 thus incentivizing McDonald’s to pick up the pace of their digital transformation.

McDonald's is not only one of the biggest employers in America, but they are one of the largest in the world.

The company had 210,000 employees in 2018 and I believe they will be able to quickly get down to 150,000 with the new software streamlining employees’ tasks allowing franchises to reduce headcount.

Getting on top of the mobile app and optimizing delivery is another step to McDonald’s digital growth strategy.

The adoption of machine learning will at some point allow customers to reorder their favorite meals on demand or before they enter the establishment, and even possibly personalizing parts of a meal that can mix and match to create alternative meals.

And the beauty of all of this, the same software rolled out to the self-serving kiosks, drive-thru platform, and mobile app can be universally adopted and managed from the cloud causing massive savings from tech efficiencies.

McDonald’s is not without its share of difficulties, sales have been plunging since 2014 and part of the response to this was to start the digital transformation.

This is just the second step of a long drawn own process that will automate the production process and customer experience.

On the flip side, the 3-year EPS growth rate is 16% demonstrating that even with falling sales, the efficiencies are falling down to the bottom line with the company profiting over $5 billion in 2018.

Ironically enough, McDonald’s profits were substantially lower with higher sales, indicating to management that a leaner version of itself has been justified.

I believe McDonald’s will continue to gentrify its menu, digitize its customer experience and production process, and sale deceleration will slow down while profit acceleration and EPS will increase.

This is a good omen for the stock’s trajectory and the company continues to be a good buy on the dip candidate because its upward share movement is entirely correlated to the increasing profitability which it continues to deliver on.

As we inch closer to a recession, deterioration of economic conditions could push an unintended growing number of customers through McDonald’s arched doors as they usually attract customers who earn less than $45,000 per year, looking to save some extra cash.

This could set the stage for a reawakening of increased sales.

“Ultimately, what any company does when it is successful is merely a lagging indicator of its existing culture.” – Said CEO of Microsoft Satya Nadella

Mad Hedge Technology Letter

March 27, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF ANOTHER STARTUP)

(WINE.L)

In a story that starts across the pond in Watford, England, BevMo! look-alike wine retailer Majestic Wine (WINE.L) has landed itself on the endangered species list.

If you don’t know, Majestic Wine is the largest specialty wine retailer in Britain.

The company revealed it would shutter most domestic locations and change its name to the internet wine distributor it bought in 2015 called Naked Wines.

The news is another glaring reminder that niche retailers have been muscled out of the picture and don't possess the business model to compete in the most dynamic and innovative sector in the world – groceries and the ecommerce surrounding it.

America isn’t the only country grappling with the dreaded Amazon effect.

In a drastic readjustment of strategy, Majestic Wine has given up on its physical presence choosing to up their investment in the online space before the window of opportunity closes.

The decision to bet the ranch on its Naked Wines online division and the subsequent news of the restructuring hit shares hard dropping 10%.

As of today, Naked Wines loses money as it attempts to lure in new online customers, and the higher costs have hit the bottom line.

The downfall of companies such as Majestic Wine directly correlates with the success of deep discount German supermarkets Aldi and Lidl that take a refreshing surgical approach to cost and convenience.

They use data analytics to make bold decisions, but they aren’t online retailers.

Hybrid strategies are being increasingly effective at solving complicated transnational problems.

The rise of the duo has outsized ramifications for the US supermarket industry, just only a few years after coming to America, they have penetrated with success.

If I had to sum up their model, I would describe it as Whole Foods quality meets Walmart prices with a truncated catalog of items and a superstar German management team.

In 2018, Aldi had already captured over 3% of market share in six of eight American markets, while Lidl had seized 3% of market share in five and seven markets.

This might not seem impressive in the world of supermarkets, but this is a resounding victory, it usually takes more time to convince new shoppers to switch their allegiance.

Not only have they made inroads in the US market, but they are the fastest-growing supermarkets by market share in Britain.

Much of the blame of Majestic Wine’s demise can be levied on these deep discount upstarts that act in real time allowing management to seamlessly shift products, alter floor designs, and capitalize on operational efficiencies on the ground.

Aldi plans to ramp up its British operations by remodeling the current 1,800 stores and open another 400 stores by 2022.

Up to 20% of products are continuously changing, giving another nod to the efficient management team in place.

They plan to offer 40% more prepared foods and wholesale changes in the business model are a hallmark of the company.

Covertly, they have single-handedly crushed the competitive advantage for Majestic Wine by offering medium-tiered wines for as little as $2.

And the $2 price point is not just a teaser rate, their wine selection is stocked full of options of $2 to $4 making it strenuous to compete on price.

You don’t need a full-blown online operation if management systemically executes and these two are proof.

Consumers are voting with their feet for Aldi and Lidl with British market share doubling since 2012 while every other supermarket has flatlined or decreased.

Some of the tactics spearheading the new jolt of positivity are minimizing staff while implementing a cozy design layout making it possible to conclude shopping in a streamlined fashion.

They are pedantically selective in what products they sell by offering only 1,750 products compared to big-box supermarkets that routinely sell up to 40,000 products.

Why sell 10 versions of ketchup or 50 types of flavored soda?

Being able to truncate the floor space by not wasting it with unlimited choices allows the company to deliver cost savings back to the customers.

They have also gone the Amazon route by producing an in-house brand by sourcing local ingredients and again, seeking to deliver back savings to the consumer.

The smaller space of the stores means shelves are less deep and items leave quickly, a specialized team is in place to refill products as quickly as possible.

The employees are also benefiting from this scheme by becoming the highest paid grocery staff in England surpassing the average industry wage by more than $2 more per hour.

Effectively, Lidl and Aldi are cherry-picking the industries' best practices then marrying it up with big tech’s best practices, and executing on a superior level to rave reviews from the consumer from America, Britain, and continental Europe.

Applying data analytics to reformulate strategy can be used for a recipe for success instead of copying Amazon.com.

The waters are treacherous for Majestic Wine as reverse globalization cast a dark cloud over consumer sentiment with Brexit causing the British pound to materially weaken stripping Brits of discretionary income.

The currency weakness has increased import costs of wine and an immediate threat of a hard Brexit forced the firm to import an extra 5 million to 8 million pounds of stock guaranteeing it is hedged against any delivery bottlenecks in the case of a calamitous “no deal.”

If Brexit does leave the European Union without a deal, tariffs will be slapped on imports the next day amongst other headaches.

Just as heinous, a “no deal” will force wine companies to fill out more than 600,000 additional forms that will cost the wine industry £70 million, and the need to carry out thousands of individual laboratory tests on all wine imports.

UK wine inspectors will face an immediate uptick in workloads with every handwritten VI-1 form needing to be analyzed and stamped before wine can enter from Europe.

If you visit Britain this summer, expect pricier spirits, expect more Lidls and Aldis in the area, and short the new e-commerce firm Naked Wines on every rally on the London Stock Exchange.

“We're running the most dangerous experiment in history right now, which is to see how much carbon dioxide the atmosphere... can handle before there is an environmental catastrophe.” – Said Founder and CEO of Tesla Elon Musk

Mad Hedge Technology Letter

March 26, 2019

Fiat Lux

Featured Trade:

(PINTEREST COMES OUT)

(PINS), (FB), (AAPL), (GOOGL), (AMZN)