Nvidia (NVDA) was right to pull the trigger – that was my first reaction when I first learned that they had aggressively acquired Israeli chip company Mellanox for $6.9 billion.

The fight to seize these assets were fierce triggering a bidding war -American heavyweights Intel and Microsoft were also in the mix but lost out.

CEO of Nvidia Jensen Huang touted the importance of the deal by explaining that “the emergence of AI and data science as well as billions of simultaneous computer users, is fueling skyrocketing demand on the world's data centers."

Therefore, satisfying this demand will require holistic architectures that connect massive numbers of fast computing nodes over intelligent networking fabrics to form a giant datacenter-scale compute engine.

Mellanox and its capabilities cover all the bases for Nvidia and will nicely slot into its portfolio offering, an added bonus of cross-selling and upselling opportunities to existing clients.

The strategic motives behind the deal are plentiful with increased importance of connectivity and bandwidth enhancing Nvidia's ability to provide datacenter-scale computing across the full stack for next-generation high-performance computing and AI workloads.

The agreement is the result of the company's shift toward next-gen technology as adoption of cloud, AI, and robotics ramps up and Nvidia will be at the forefront of this massive migration.

As the fourth industrial revolution advances, Nvidia is best of breed of semiconductor companies and the imminent adoption of 5G will aid the likes of Microchip Technology (MCHP) and Xilinx (XLNX).

Technology is rapidly changing, and the data center is the segment that is accelerating at a faster clip than in previous years translating into de-emphasizing current revenues of gaming and autonomous on a relative growth basis.

These segments will be secondary to the addressable opportunity in data center and signing up Mellanox is a key strategic initiative to exploit this growth opportunity.

Missing the boat on this compelling opportunity could have dragged Nvidia into an existential crisis down the road as the missed opportunity costs of lucrative data center revenues would begin to bite, and with no quick fix on the horizon, Nvidia’s growth drivers would be potentially disarmed.

Investors need to remember that Nvidia derives half of its revenue from China and up until this point, gaming had been a huge tailwind to its total revenue, however, the Chinese communist party has identified gaming addiction in young adults as a national crisis and have been refusing to deliver new gaming licenses to gaming creators.

As the data center via the cloud begins its next ramp-up of insatiable demand, Nvidia was acutely aware they could not miss the boat and to grab a foot hole against larger player Intel.

Almost overpaying to have more skin in the game does not do justice to what the ramifications would have been if Intel or even Microsoft were able to hijack this deal.

The two-fold victory will in turn boost sales of Nvidia's data center products long term while depriving Intel of extending the lead in data center.

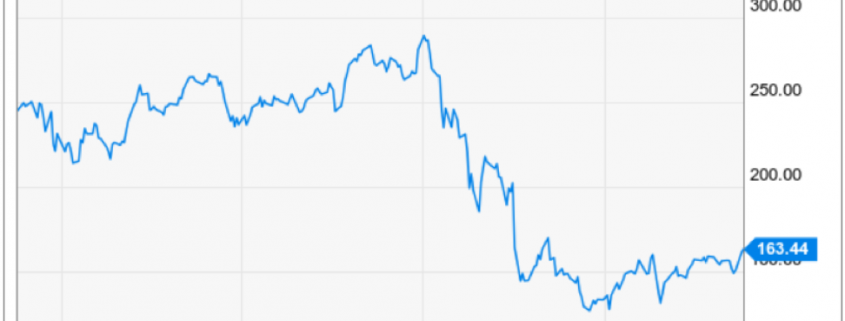

And after the lack of recent underperformance in the prior quarter, Nvidia needed a gamechanger to cauterize the blood flow.

Nvidia's total revenue plunged more than 24% YOY in Q4 of 2018, and shareholders have been looking for remedies, especially after the once mythical cryptocurrency business blew up and the company was stuck with a glut of inventory.

The purchase of Mellanox will help Nvidia start competing with other dominant players like Cisco Systems (CSCO) and Arista Networks (ANET).

Mellanox is one of a handful of firms selling hardware that connects devices in the data center through network cards, switches, and cables.

The deal still needs regulatory approval and could be a stumbling block if Chinese authorities drag this into the orbit of the trade war and make it a bullet point in negotiations.

The net result is positive to the overall business model, and this move will breathe oxygen into Nvidia’s long-term narrative with a flow of revenue set to come online once the 5,000 Mellanox employees are integrated into Nvidia’s levers of operation.

Shares should be the recipient of short-term strength and after getting smushed by a poor last quarter, there is substantial room to the upside.

A dip back to $150 would serve as a good entry point to strap on a short-term bullish trade in Nvidia shares.