Mad Hedge Technology Letter

February 25, 2019

Fiat Lux

Featured Trade:

(THE CLEANEST INTERNET PLAY OUT THERE),

(GDDY), (WIX), (CSCO),

Mad Hedge Technology Letter

February 25, 2019

Fiat Lux

Featured Trade:

(THE CLEANEST INTERNET PLAY OUT THERE),

(GDDY), (WIX), (CSCO),

Check out GoDaddy (GDDY).

It’s a general bet on more people using the internet.

This trade dovetails nicely with my broader thesis of the dramatic migration to digital.

Brick and mortar stores will have no choice but to create a unique website and one of the most prominent web hosting services is GoDaddy.

The Mad Hedge Technology Letter is even powered by its services.

Lately, I’ve been all about this digital migration mantra and we are in the early innings of this seminal trend.

I gave you Cisco (CSCO) as a hot pick which is a bet on an increase in enterprise software business.

This is more of a question of how fast than if or when.

Are you ready for 5G?

The technology is on the verge of rolling-out to select cities around the US, and it will juice of web usage simply because users can navigate around more in a smaller time window.

GoDaddy was established by fellow Marine Bob Parsons in Baltimore 22 years ago and before GoDaddy, Parsons sold off his financial software services company, Parsons Technology to Intuit for $65 million.

He then launched Jomax Technologies which later morphed into GoDaddy in 1999 when employees were collaborating to change the company name and someone jokingly shouted out, "How about Big Daddy?"

Sadly, when the company found out that domain name had already been registered, Parsons replied, "How about Go Daddy?" and that was that.

What do I like about GoDaddy’s financials?

Better than expected profitability.

EPS forecasts were beaten handily with the company posting 24 cents, almost a double of the forecasted 13 cents.

Estimates of $693.5 million for the top line were marginally beaten by $2.3 million.

The company gave positive all-important guidance indicating robust momentum.

The firm is expecting $3 billion in 2019 sales and that is after doing $2.23 billion of sales in 2017.

Management has kept sales growth strong with a 3-year sales growth rate of 19%.

Customer renewal strength and higher average revenue per user (ARPU) growth is resonating with investors, and fused with higher operating margin could propel this firm’s shares higher.

ARPU mushroomed to $148.00 up 7% YOY while total customers rose 7% bringing the total customer base to over 18.5 million.

In 2018, over 1 million new customers were lured into the ecosystem.

The reason for this successful rise in domestic ARPU is enhanced site and product experiences, interactions focused on details and conversational marketing.

In a tech climate where a good portion of company outlooks are tepid at best, GoDaddy didn’t mince its words offering a better than expected positive outlook.

The financials look solid but allow me to explain a little more about its core products.

Almost 35% of websites on the internet is already constructed using WordPress’s platform and GoDaddy is the biggest host of paid WordPress at the end of last year.

GoDaddy’s supported WordPress offering automates the entire process of operating a secure WordPress website making it easy to use and highly popular to its customer base.

The role GoCentral's, GoDaddy’s flagship DIY website building product, plays is expanding as its numerous features increase and efficient performance is a consistent highlight for the firm.

The journey started in 2017 when GoDaddy established this service as a simple website building tool.

Concrete foundations were set and this service was integrated across a myriad of relevant third-party platforms while boosting product functions that are seeing outsized growth.

Daily entrepreneurs can now produce robust websites and carry out syndicate marketing across the e-commerce landscape.

The tandem of WordPress and GoCentral are growing subscriptions more than 40% YOY.

North America and Canada are the main revenue drivers, but international business is a wide-open opportunity waiting for management to pick off whether that's Latin America, Asia, or even in the Middle East.

The strategy for Europe is extracting the capability and product portfolio of North America, whether it be conversational marketing or features like security, backup, malware scans, plug-ins, and proactively migrate it to Europe because the model in America is obviously working and using that model will be a great development point.

Mexico and Brazil possess great growth potential and Asia continues to be about customer adds because the willingness to pay is different.

Competitor Wix (WIX) lately announced a shift in strategy, removing Domain Connect, and some of the low-end products and saying that they're going to come after WordPress.

But Chief Executive Officer of GoDaddy Scott Wagner is not worried about this nascent threat and is sure that this is the case of GoDaddy is in control of its own destiny than Wix being a viable threat.

As long as the company reinvests in its offerings and maximizes the user experience, Wix has a long way to go to compete with WordPress and are substantially smaller than GoDaddy.

And as GoDaddy keeps working on offering great value propositions and expanding the ecosphere with integrated and high-quality software, the stock is bound to jump further.

The momentum is palpable with this website hosting service a top player in its industry.

Wait for a pullback to buy some shares.

“You got to go down a lot of wrong roads to find the right one.” – Said Founder of GoDaddy Bob Parsons

Mad Hedge Technology Letter

February 21, 2019

Fiat Lux

Featured Trade:

(BUY AMD ON THE DIP),

(AMD), (NVDA), (INTC),

I am bullish Advanced Micro Devices (AMD).

The company is doing backflips and edging around other fertile pastures to the dismay of competitors.

They jumped all over Intel’s (INTC) CPU lead promising more cores and adding on more features to lure in a new audience.

In terms of computer graphics, Nvidia (NVDA) still wields more clout in the higher-grade GPU space and AMD has been playing second fiddle with cheaper, value-oriented GPU cards that can be best described as mid-range.

That is about to change.

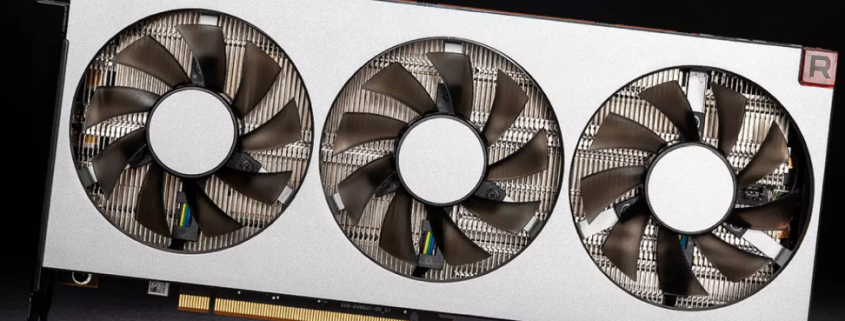

AMD is at it again acing its attempt to pull down Goliath with its new Radeon VII.

This $700 GPU card is the first 7 nanometer (nm) GPU on the market and is a warning shot to Nvidia who they plan to surgically invade in order to snatch market share.

This new AMD GPU is a direct threat to Nvidia’s set of RTX 2080 graphics cards and is set at the same price point with comparable performance.

The Radeon VII is the next iteration to AMD’s Vega 64 and possesses similar architecture with specific enhancements in clock speeds and VRAM.

Gamers are still on the fence to whether this new product can eclipse the heavily entrenched Nvidia graphics cards that are time-honored, tested and stamped with the industries seal of approval.

It is still uncertain whether AMD can introduce the necessary supply and if you still remember when the prior iteration Vega 64 debuted in 2017, it was a threat to Nvidia’s top-tier GTX 1080, but ran out of inventory quickly.

The new Radeon VII card is one of the best on the market for professional work and still does well in the gaming realm, albeit with a lack of ray tracing.

Few video games support ray tracing currently but new game studios plan to adopt this cutting edge technology later this year.

I commend AMD’s first foray into this part of the niche market and when AMD upgrades its architecture and improves on the next iteration, Nvidia will be squarely in their crosshairs.

The number of new products that drive top-line growth is another reason to be positive on this stock.

Looking at the CPU market – momentum would be the key word to describe AMD’s current trajectory.

For generations, Intel has had a secure stranglehold on this rapidly expanding market, but the fringes of the industry have been hijacked by AMD and they seek to spread its tentacles deeper into foreign CPU waters.

By the end of the year, I believe that AMD will carve out a nice high single digit market share of global CPU sales.

Intel has been bogged down by production setbacks in the deployment of the 10-nm server chip giving AMD a chance to take advantage of this gaping pothole to jack up sales with its EPYC chip.

Not only that, AMD is motoring ahead with a superior 7-nm chip which is a faster processor and is more energy-friendly than Intel’s 10-nm version.

I can conclude that AMD is blowing past Intel in chip technology, and has its third generation of CPUs earmarked for the market in the summer ready to stretch the lead.

CEO of AMD Dr. Lisa Su is compounding the misery for Intel, offering a physical glimpse of plans to roll out its third generation Ryzen CPUs for PCs by the middle of the year at the Consumer Electronics Show in January.

Another catalyst that could drive the stock higher is a favorable earnings outlook in 2019.

After meeting expectations last quarter, expansion is expected in the high single digits in a tough chip environment that has wrought its fair share of carnage.

I wouldn’t pigeonhole the new product line as mere hype, it’s clear they are meaningfully enhanced and improved with each successive iteration.

I estimate that these new products will give AMD solid traction to close in on the competition in the CPU and GPU markets.

Clearly, this isn’t a 1-quarter venture, but visibly aware that AMD is making inroads into other markets are a demonstrably net negative to weight on Intel and Nvidia shares.

This part of tech is not without its headaches and is fraught with China risk.

Chinese gaming regulators have put the kibosh on new gaming licenses and AMD’s scaling back of forecasts should reflect this development.

Intel cited falling spend on server chips and Nvidia came out with a dreadful earnings report to forget lately.

However, when there is blood in the streets, the status quo is ripe for some change and I am confident that AMD can execute this aggressive ramp up after digesting some of the excessive inventory in the first quarter.

As AMD trades at $24, I can’t help but believe this name will end the year higher.

Investors must remember that in the near term, the Fed has hit the pause button aiding the equity market, and China has reportedly been keen on some massive chip purchases to help soothe the nerves of the administration.

If the market can marry this up with favorable reviews of AMD’s latest products, I don’t see why AMD can’t be trading at $30 by the end of the year.

At the Mad Hedge Lake Tahoe Conference, I proclaimed that AMD was one of my favorites going into 2019 and exploded upwards from $17 in October 2018.

AMD truly has not disappointed.

“If you don't have a mobile strategy, you're in deep turd.” – Said CEO of Nvidia Jensen Huang

Mad Hedge Technology Letter

February 20, 2019

Fiat Lux

Featured Trade:

(WALMART’S DRAMATIC SAVE),

(WMT), (AMZN)

This is not your father’s Walmart (WMT).

Peel back a layer or two of that thin veneer and in Walmart, you have nothing closely resembling the Walmart you grew up with.

This would have been a coup de grâce for many companies facing the tsunami of tech strength crushing business models left and right.

Yet, Walmart has found a way to turn the tables and flourish when many industry experts thought this once legacy shopping business was careening towards extinction.

Walmart’s outstanding performance of growing e-commerce sales 43% YOY in the winter quarter of 2018 is a proclamation that they are here to stay through hell or high water and it’s the e-commerce segment leading the charge.

Betting the ranch on e-commerce has them inevitably on a collision course heading directly towards competitor Amazon (AMZN).

Instead of shriveling up and waving the white flag, Walmart’s President and CEO Doug McMillon is acutely aware that the overall pie is growing and there is room for more than just Amazon.

His company’s recent success echoes this trend of the overall marketing growing, and I believe passing the acid test of the 2018 winter shopping season is concrete evidence that Walmart has a prosperous future if they can navigate around four objectives.

First, triple-down on the e-commerce strategy which could translate into being a tad cavalier to operating margins.

This would take a machete to short-term profitability, but I believe Walmart investors are starting to believe in this tech pivot and further margin erosion can be stomached because they are currently conditioned for it.

To capture a larger footprint in the e-commerce market, data analytics specialists will need to be recruited in heavy numbers and convinced of the future vision of Walmart.

The turn of the calendar year means that end of the year bonuses are out and now is the time to capture the horde of tech talent sitting on the open market waiting to be put on Walmart’s books.

Walmart could potentially leap into position to nab some of these tech high flyers who specialize in Python and SQL programming languages. The demand for these wizards is insatiable and the key to any corporate digital migration strategy.

Second, being able to penetrate the target audience a notch above than what Walmart is traditionally accustomed to.

This would correlate into higher average spend per Walmart transaction which would become a feedback loop into Walmart carving out higher-grade product line-ups to compensate increasingly pressured margins.

Third, enhance the logistics and fulfillment strategy by automating more of the business process through robotics and a streamlined IT department.

Walmart has been in the process of scaling out this portion of the business process and they are probably the only one that can pull this off because of the gigantic addressable market and flowing access to capital.

Fourth, originate an educational program coaching up spendthrift customers on how to access its products digitally.

Investors must remember that a large swath of Walmart’s customers aren’t at the top of the socioeconomic ladder and seamlessly culling them into the digital orbit is a responsibility shouldered on upper management.

The goal is to gradually migrate every type of order variant online or through self-checkout means, and self-navigating through these payment and service barriers could be a hindrance as Walmart’s customer base is less tech-savvy than Amazon’s prime subscription customer base.

However, the smaller digital native customer base on a percentage basis is offset by the 4,700 physical stores allowing these partially digital-savvy customers to click and collect.

I view the click and collect distribution channel as a bridge towards becoming fully digital and if Walmart can provide superior customers service, this cohort will likely stick with Walmart’s full-service digital offerings in the future once they upgrade.

In the distant future, it’s almost guaranteed these physical stores end up as fulfillment centers with robotic automation or some type of mix of the two.

Walmart is starting to get serious looks as an e-commerce powerhouse, and I have consistently described Walmart as the next FANG. This latest earnings report reinforces this thesis.

I champion some of the moves to add to product lines such as online brands Art.com and female garment retailer Bare Necessities.

If Walmart could whip up an in-house brand similar to Amazon Basics, that would also be a gamechanger. That step is down the road and Walmart would need to accumulate higher expertise to convert certain products from the 3rd party variety.

Another growth inducer would be establishing a subscription-based service similar to Amazon Prime. Software as a subscription (SaaS) is all the rage in technology and for all the right reasons as this recurring revenue is a boon for the CFO and stabilizes finances.

The Arkansas-based firm forecasted e-commerce annual sales growth of 35% and indicated that huge sums of capital would be allocated into remodeling store units, reinforcing the e-commerce platform, and juicing up its supply chain operations.

Walmart is only scratching the surface and it would take a debacle of epic proportions or a massive recession crimping product demand to knock off Walmart from this high-speed train of positive momentum.

Yes, I agree this company isn’t even close to Amazon now, but the catch-up potential and that path to catch up is clear as daylight.

There is no need to chase shares at this price, but I can say that Walmart is on the verge of locking itself up at the $100 price point as an eternal support level moving forward.

If shares sell off to $90 because of the recent buying from oversold conditions, it could be one of the last times ever to secure a price that cheaply for a precious FANG company.

The company is also famous for continuously raising its dividend.

Walmart is an intriguing stock for the rest of 2019, particularly if the momentum snowballs from here.

“There are seven billion people in the world. And I think phones are the first time most people will have access to a modern computing device. With Android, we want to enable that for people.” – Said CEO of Google Sundar Pichai

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)