Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

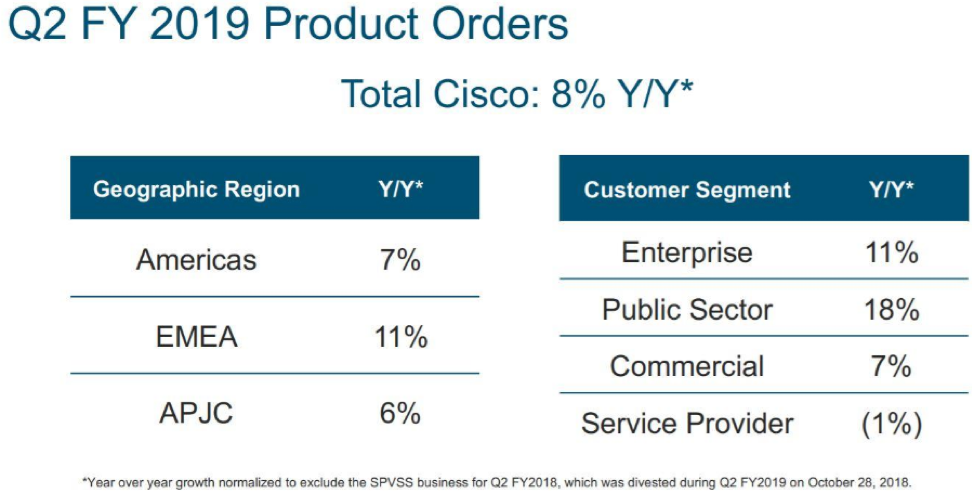

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.