Mad Hedge Technology Letter

August 26, 2024

Fiat Lux

Featured Trade:

(LET IT SNOW)

(SNOW), (NVDA)

Mad Hedge Technology Letter

August 26, 2024

Fiat Lux

Featured Trade:

(LET IT SNOW)

(SNOW), (NVDA)

Some might believe that there are no more growth companies out there in the tech sector.

Innovation has been dragging its heels for quite some time.

Shouldn’t we have put someone on Jupiter yet?

Tech is still very much in the software revolution.

Screens and iPads have been the devices that have allowed software companies to print money.

Then came the monopolistic stranglehold of big tech like Google and Amazon that has really crushed the small guy.

However, there is still room to flourish for smaller companies that are punching above its weight like Snowflake (SNOW), a software company, renowned for its data cloud platform which houses a global network designed to maximize its cloud potential.

This platform allows thousands of organizations to manage their data concurrently, providing both scale and performance.

Snowflake’s unique platform allows thousands of organizations to manage their data with extensive storage and computing power.

Key features of the platform include data storage, processing, and analytic solutions that run faster than traditional systems.

SNOW disappointed in its sales outlook which is why the stock cratered in the short-term, but I do believe this is a buy-the-dip opportunity for the objective investor.

It assured investors that results weren't affected by AT&T's recent data breach or the Crowdstrike outage.

Deceleration is never a term shareholders want to hear from a public company.

The reason for the slowdown is that other companies are beginning to pull back their budgets.

Snowflake’s data warehouse also competes with platforms operated by larger technology giants such as Amazon’s (AMZN) Redshift and Alphabet’s (GOOGL) BigQuery.

These companies could challenge Snowflake’s unique usage-based pricing model as compared to traditional subscription-based pricing.

Lastly, the company still has not turned profitable, leading investors to question the sustainability of the company’s business model.

The company is actively expanding its capabilities in new ways.

Snowflake has developed its own Large Language Model (LLM) called Arctic, which has outperformed other LLM models in various benchmarks, such as Meta Platforms’s (META) Llama.

Furthermore, the company is also enhancing its capabilities through a strategic partnership with Nvidia (NVDA) which aims to provide its customers with a platform designed to boost AI productivity, thereby enhancing business performance.

These 10 new features will provide new revenue streams and more users, re-accelerating Snowflake’s year-on-year revenue growth.

Snowflake’s focus on ramping up its AI offerings displays its commitment to maintaining its leadership in the data warehousing sector.

I do believe that SNOW is worth a look.

It’s true that competition will be a rough ride with the likes of big tech looking to outmuscle SNOW.

That is a serious risk to the long-term viability of the business model and I am not downplaying this risk.

At a $40 billion market cap, the stock definitely screams small company.

However, I do believe there is more room to run to the upside, but the growth is definitely limited.

I think at $115 per share, it is worth a trade and the next pop would be a great time to take profits.

Much of the rate hikes have been discounted into the price of shares so I do believe they will need to show us more than just give them the benefit of the doubt.

“Price is what you pay, value is what you get.” – Said Investor Warren Buffett

Mad Hedge Technology Letter

August 23, 2024

Fiat Lux

Featured Trade:

(TECH STOCKS LAUNCHED INTO ORBIT BY JEROME)

($COMPQ), ($TNX)

The job is done – The Fed won against inflation.

When is the parade?

That was largely the message that was delivered to us this morning by U.S. Federal Reserve Chairman Jerome Powell.

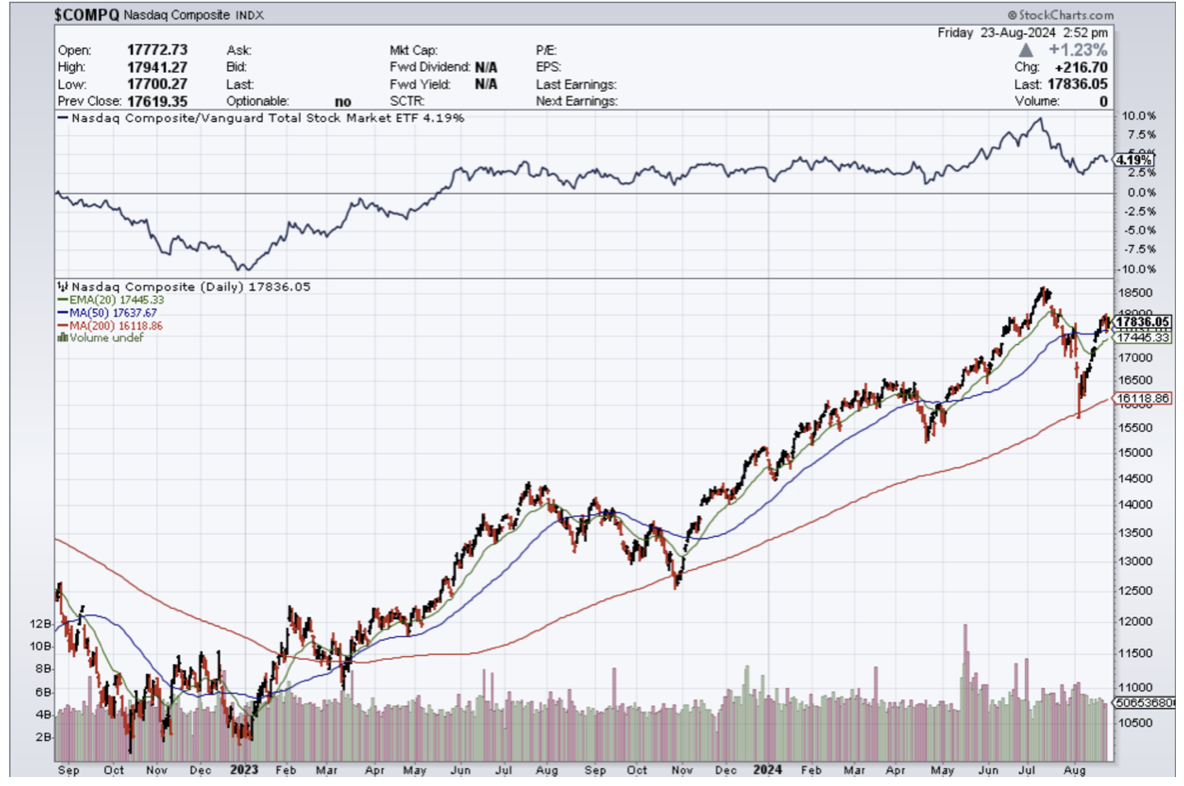

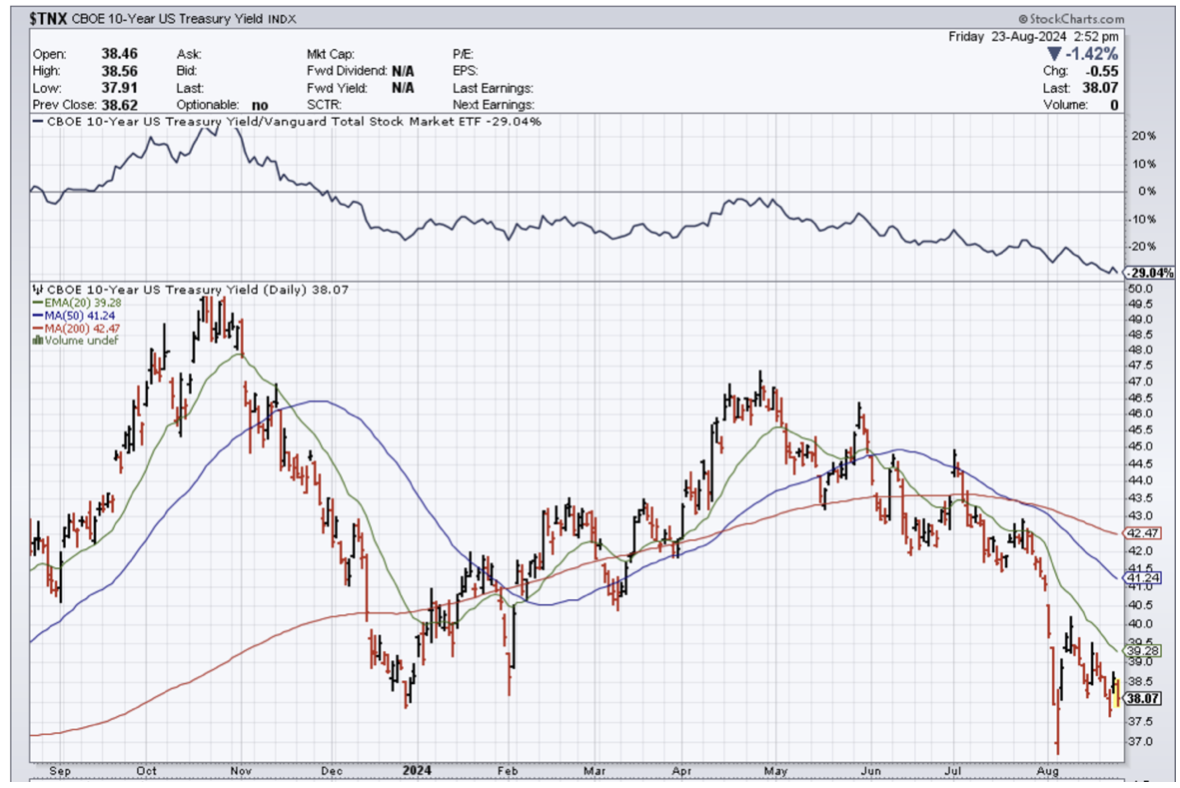

Migrating into rate-cutting mode means that tech stocks ($COMPQ) are about to explode into orbit.

We will only know how much higher tech stocks will go when we can understand how much Powell’s Fed will cut.

If he cuts the Fed Funds rate from 5.25% to 2% then tech stocks will be up at least another 50% from these levels.

What is bizarre is that Powell is cutting rates ($TNX) with housing prices, grocery costs, stock market, and a price for one ounce of gold at all-time highs.

Things are about to get more expensive – that is guaranteed.

Ironically, the Fed is planting the seeds for the next rip-roaring wave of inflation, because 3% inflation levels will be the new floor and not the ceiling.

Once the CPI hit 2.9% just a few days ago, the Fed went into the “the job is done” mode which is extremely dangerous.

Either way, tech stocks are in for a spectacular monster rally heading into the year's close and we just added a big position in chip stock Micron (MU).

There should be two to three .25% cuts by the end of the year which is highly bullish for equities.

"The direction of travel is clear," Powell added.

Powell acknowledged recent softness in the labor market in his speech and said the Fed does not "seek or welcome further cooling in labor market conditions."

The July jobs report rattled markets earlier this month, revealing that there were just 114,000 jobs added to the economy last month while the unemployment rate rose to 4.3%, the highest since October 2021.

Data earlier this week also showed that 818,000 fewer people were employed in the US economy as of March, suggesting reports have been overstating the strength of the job market over the last year.

Powell's remarks on Friday were reminiscent of those he delivered at Jackson Hole in 2022, in which the Fed chair offered a direct assessment of the economic outlook and, at the time, the need for additional rate increases.

The similar part of the speech was his call to action to change the direction of policy and he did just that.

We are about short-term trading and trade alerts here in what moves the market with tech trades.

I do believe long-term, what Fed chair Jerome Powell did, will turn out to be a policy mistake that will result in a lot higher bond yields.

The Fed's slow walking the rate hikes on the way up and then now slow walking the rate cuts on the way down is a recipe for disaster and the wrong way to approach this problem.

The ironic thing here is that tech stocks are the only equities, apart from energy and supermarket stocks, to do well in a higher inflation backdrop and part of that has to do with their monopolistic power which continues unabated.

Not that tech needed any help, but help is arriving in terms of lower rates and I do believe tech stocks will do well as we move closer to year-end.

Buckle up, put on your cowboy hat, and enjoy the tech rally!

“A brand for a company is like a reputation for a person. You earn reputation by trying to do hard things well.” – Said CEO and Founder of Amazon Jeff Bezos

Mad Hedge Technology Letter

August 21, 2024

Fiat Lux

Featured Trade:

(SPEND UNTIL REVENUE COMES)

(NVDA), (SMCI), (AVGO)

Spend, spend, and spend some more.

That is the current zeitgeist in the tech community about the direction of generative artificial intelligence.

Companies are trying to outdo each other to see how much cash they can splurge to build out the AI infrastructure.

This is no joke.

Remember that there have been no meaningful explanations about how much revenue will directly come from AI, but my belief is that we are still in the “honeymoon phase” of the AI movement.

Eventually, and gradually, real questions will be asked and results will need to be provided instead of “building” nonstop with no accountability.

We are still in the phase of giving AI a pass which is why many have suggested stocks like Nvidia are turning into a bubble similar to 2001.

How do I know that AI is back?

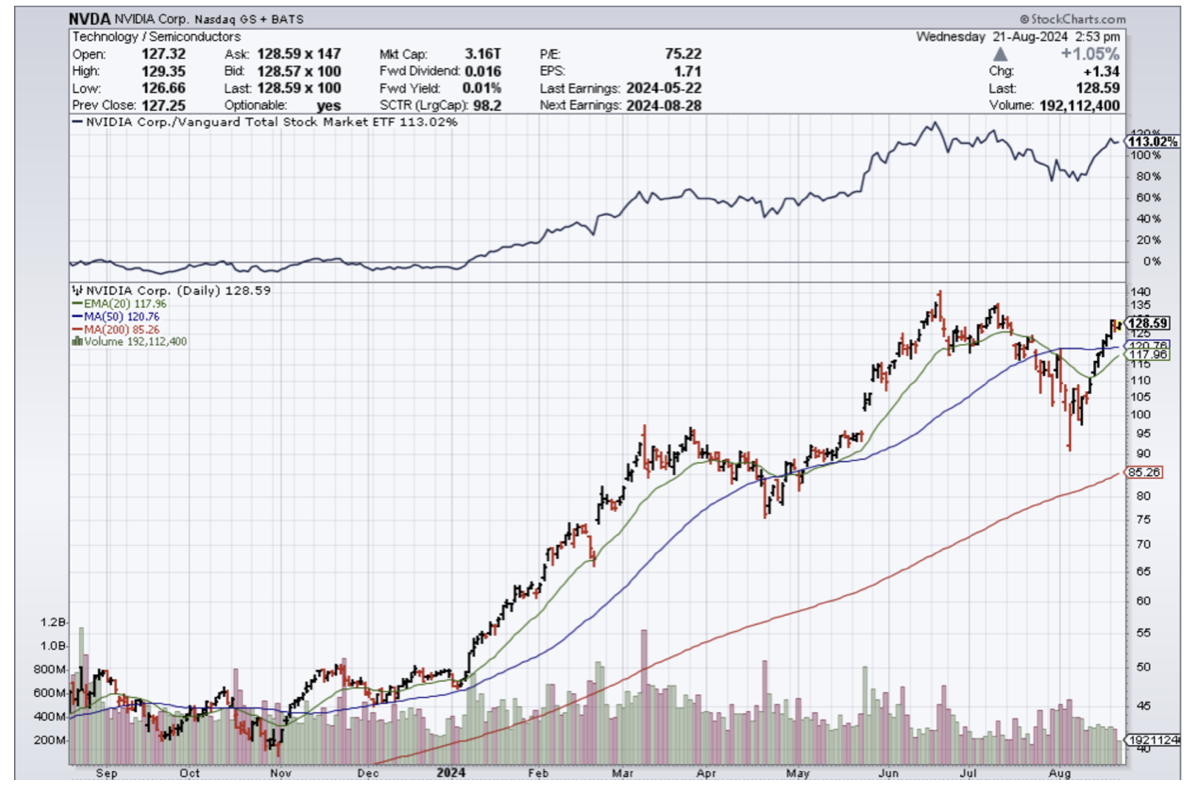

Look at the chips stocks who were leading the tech rally for most of the year.

They sold off violently because of the unwinding of the Japanese yen carry trade, but the dip was bought because the discounts were too good to pass up for investors and because the AI trade isn’t over yet.

The snapback in chip stocks was v-shaped and set the stage for the rest of the year to power into the close.

I do believe the tech sector will receive better-than-expected news from the wider economy that shows the consumer is in better shape than initially thought.

The bar is extremely low for tech stocks to jump over and I do believe the ones with great balance sheets will use shareholder returns to convince shareholders to stick with their stocks.

AI hardware and chip companies have led the bounce in the Nasdaq from its August low, with Nvidia the index’s top performer, up almost 30% and just 6.1% short of the all-time high, as of its last close. Similar stocks like Micron, Marvell Technology, Super Micro Computer, and Broadcom have all participated in the snapback.

Strong monthly sales from Taiwan Semiconductor Manufacturing similarly pointed to robust AI demand.

The build-out of AI infrastructure is expected to be both enormous and long-lasting and investment in data center infrastructure needed to support GenAI could reach $6 trillion.

Capex from big tech could potentially increase by as much as 25% in 2025, well above the consensus expectation for 10-15% growth. This is especially positive for AI enablers in the semiconductors field.

Nvidia’s expensive valuation is completely justified when you understand that they carry the entire tech sector which is carrying the entire market on their back.

Shorting NVDA has probably been one of the worst trades you could have made in the past few years.

Mad Hedge Technology Letter

August 19, 2024

Fiat Lux

Featured Trade:

(WHAT WILL PALANTIR STOCK DO FOR THE REST OF 2024?)

(PLTR)

Not all tech stocks are created equal.

Some have the power of connections from the beginning and that goes a long way to understand if a company can do what it takes to survive.

Very rarely do tech companies come out of nowhere and it is true that recognized venture capitalists help like rocket fuel.

Palantir (PLTR) was supported initially by tech insider billionaire Peter Thiel.

It’s not surprising that this is a company sitting deep at the intersection of strategic national intelligence and artificial intelligence.

The stock hit a low of $5 per share and now trades north of $32 per share.

Investors might easily understand this company as the war tech stock and co-founder and CEO Alex Karp is in no mood to apologize or be politically correct for its military, police, and U.S. Immigration and Customs Enforcement services despite facing massive backlash.

Karp acknowledged the company’s consistent pro-Western view despite polarizing views regarding the appeasement of Iran, Russia, and China.

Karp refused to apologize for defending the U.S. government on any issue and he has never wavered behind their principle of powering the U.S. government.

Karp stood out for his fierce criticism of Former US President Donald Trump, but he has said that he will work with both administrations.

Karp also maintained his pro-artificial intelligence stance, indispensable to preventing AI abuse.

In August, Palantir reported second-quarter revenue of $678.13 million, up 27% year-over-year, topping the analyst consensus of $652.1 million.

Palantir has been selling AI software for much longer than most of its competitors, which gives it a leg up on its competition. It started off as a software program intended for government use, with the simple concept of data in and insights out. This helped guide real-time decision-making by ensuring the people making the choices had the best possible information in front of them.

Still, government revenue makes up more than half of Palantir's total and rose at a 23% pace. It was powered by U.S. government revenue, which saw the highest demand since 2022.

No matter how you dice it up, Palantir's Q2 results were phenomenal. However, management thinks its growth may slow in Q3. Third-quarter revenue is expected to be about $699 million, indicating growth of 25%. While that's less than Q2's growth rate, management has consistently beaten its guidance.

My opinion about where the PLTR’s stock is going might surprise some people.

On one hand, the United States has the biggest military in the world and will covet and utilize PLTR’s software to continue to make real-time decisions in a national security sense.

On the other hand, the issue I have with PLTR is not with the quality of the business, but the price of their stock.

The stock has risen too fast too furiously in a short-amount of time.

The move from $5 per share to $32 took place over a 2.5-year time frame obviously boosted by global events in Eastern Europe and the Middle East.

For the rest of the year, I do think PLTR has a chance to blow past $40 per share and at that point, we will most likely reach the short-term high water mark of the stock.

The stock is due for a big sell-off once the AI frenzy cools down a little and that could be later this year.

Remember that the AI narrative has reignited in the short-term so it is smooth saying until the next road bump.

This is a complex company and with many of those, the trajectory of the stock can be many times more complicated.