Mad Hedge Technology Letter

October 2, 2018

Fiat Lux

Featured Trade:

(TAKE A LOOK AT ENGLAND’S AMAZON),

(LON: OCDO), (KR), (AMZN)

(WE'RE MAKING SOME CHANGES HERE AT THE MAD HEDGE FUND TRADER)

Mad Hedge Technology Letter

October 2, 2018

Fiat Lux

Featured Trade:

(TAKE A LOOK AT ENGLAND’S AMAZON),

(LON: OCDO), (KR), (AMZN)

(WE'RE MAKING SOME CHANGES HERE AT THE MAD HEDGE FUND TRADER)

“Technology's always taken jobs out of the system, and what you hope is that technology's going to put those jobs back in, too. That's what we call productivity.” – Said Salesforce Founder, Chairman and Co-CEO Marc Benioff

Mad Hedge Technology Letter

October 1, 2018

Fiat Lux

Featured Trade:

(ZINC AIR BATTERIES WILL REVOLUTIONIZE ELECTRIC CARS),

(TSLA), (NIO), (FB), (GOOGL), (NFLX)

As Panasonic ramps up its battery production at the Tesla Gigafactory 1 in Sparks, Nevada, the demand and business for renewable energy has never been more robust.

And as the world’s population balloons and man-made pollutants roil the natural ecosphere, business needs an answer to these potential apocalyptic bombshells or there will be nowhere clean enough to live.

Energy security and population growth will have a complicated relationship going forward and cannot be ignored for the sake of mankind.

This isn’t me being a tree-hugging, Birkenstock-trotting, save-the-earth, love and peace-type of guy.

This problem is real and whoever discovers the solution could reap untold profits.

The answer has been found - rechargeable zinc air batteries.

Spearheading this massive initiative is South African-born entrepreneur, sports team owner, Los Angeles Times owner, and more importantly the founder, chairman and CEO of NantEnergy Dr. Patrick Soon-Shiong.

This El Segundo, California-based company presented an utter game changer to the future of the world and the world’s economy.

NantEnergy debuted a rechargeable battery powered by oxidizing zinc with oxygen from the air for commercial use at the One Planet Summit in New York.

It also has the capability to store energy.

Not only is this technology and product cutting edge, but it has the cost basis to support broad-based scalability and adoption.

Ramkumar Krishnan, chief technology officer of NantEnergy claimed this revolutionary battery can “deliver energy for $100 per kilowatt-hour (kWh).”

Lithium-ion batteries have been the mainstay choice for clean energy or clean enough energy since 1992, and its usage varies in cost from $300 to $500 kWh.

Tesla, with its phalanx of superior engineers, has been able to suppress that cost all the way down to a level between $100 to $200 kWh level.

NantEnergy has already registered more than100 related patents in its name and envisions a $50 billion addressable market.

I believe the addressable market is substantially bigger.

For all the hoopla about lithium-ion batteries, there are severe drawbacks in its usage and application.

Let’s concisely run down the pitfalls of batteries of this ilk.

Once out the factory door, the performance starts to go downhill.

Lithium-ion batteries react poorly to high temperatures.

These batteries become inoperable if completely discharged.

There is a slight chance a battery could burst into flames and burn off your face.

Simply put, lithium-ion batteries incorporate cobalt, an extremely toxic material hazardous to human health.

If a Samsung Galaxy smartphone explodes, cover your mouth to avoid inhaling the cobalt-laced fumes.

Dr. Soon-Shiong characterized this new technology as the “holy grail” of renewable energy.

Wide-scale adoption would bring the need for cobalt to its knees.

No longer would tech companies need to scramble to secure a sufficient amount of cobalt supply from the deepest reaches of the Congo jungle.

It would be the end of cobalt as we know it.

At first, lithium would be required for a stopgap measure while engineers refine the battery on its way to a full-fledged zinc alone battery.

The lithium placeholder would only be temporary.

The clean energy movement must be grinning widely as the potential to finally do away with cobalt from renewable energy has pronounced social and economic consequences.

An estimated 1.4 billion people still live in the dark and do not have access to electricity.

This technology is being tested in villages in Africa and desolate communities in Asia as we speak.

The absence of electricity isolates these undeveloped communities in third-world Africa and Asia without access to health care, education, and technology.

It’s hard to kick-start your life as a sprouting little kid when you’re lost in the dark half the time.

Importing fossil fuel to put these communities online is unfeasible and just plain too expensive for communities that have a dire shortage of capital.

Currently, NantEnergy’s rechargeable zinc air batteries are online in 110 villages located in nine Asian and African countries.

The batteries have been combined to establish a microgrid system powering entire areas.

The company will start delivery this product next year widening its type of use to telecommunications towers.

The next step after that would be the home energy storage market targeting California and New York as the first American cities.

Engineers have pointed out that this development could transform the electric grid into a “round-the-clock carbon-free system.”

In addition, with cooperation with Duke Energy, a major utility, NantEnergy’s batteries have been powering communications towers in America for the past six years.

The design is mind-boggling utilitarian - plastic, a circuit board, and zinc oxide wrapped up in a briefcase-size shell.

One charge can offer 72 hours of battery life.

The charging process is easy - electricity from solar installations is stored by converting zinc oxide to zinc and oxygen.

The discharge process is straightforward, too - the system produces energy by oxidizing the zinc with air.

The pursuit of energy reduction is in full throttle, and this is the next leg up for energy aficionados.

Your lithium-ion-run Tesla could become a legacy company in a matter of years if this technology disrupts Elon Musk’s brainchild.

Lately, Musk has been falling behind the eight ball with fresh innovators hot on his heels.

This is the latest company to enter into its market even though still in the incubation stage.

Competitors have popped out of nowhere and are coming for his bacon.

Shanghai headquartered electric car manufacturer Nio (NIO) went public and raised more than $2 billion.

Even though it is not yet a threat to Tesla, it shows that Tesla isn’t the only game in town anymore.

In any case, NantEnergy has the magic to unlock the “holy grail” of renewable energy. And if it can promise on its cost projections, I see no reason why this won’t be furiously adopted by corporations worldwide.

As it is, America has been losing out in the Congo, as China has cornered the cobalt market there.

And, as the evolution of fracking technology quelled the Middle-East situation, it could also have the same effect in the Congo.

More excitingly, it could put online an additional 1.2 billion new customers to devour iPhones and watch Netflix (NFLX).

Companies such as Facebook (FB) and Alphabet (GOOGL) have been developing a way for these remote and poverty-prone places to use Internet from a satellite.

They would need electricity first to power their devices unless Mark Zuckerberg has found a way to use a smartphone without electricity.

NantEnergy’s renewable batteries have already cut the need of 1 million lithium-ion batteries, and warded off the need to release 50,000 metric tons of carbon dioxide since 2012.

California is the flag-bearer in renewable energy policy by forcing its populace to be at 100% carbon-free electricity by 2045.

Musk is on record by saying he expects to break the 100-kWh level, which would contribute to better power storage and expedited electric vehicle (EV) adoption.

In contrast, energy storage analyst Mitalee Gupta at GTM Research has retorted that he’s “unsure $100/kWh is achievable this year.”

Musk, being a naturally optimistic entrepreneur, sets targets then does everything he can to break them.

Either way, two South African born visionaries are doing their part to crater the cost per kWh in the renewable energy market, and Elon Musk might not be the biggest disruptor from South Africa.

Time will tell if this market will become zinc-based or lithium-based – the higher-grade technology eventually wins out spelling doom for Musk.

But it appears that Musk has other things to worry about now.

NantEnergy plans to inaugurate a battery manufacturing facility in California next year.

As for Tesla, buy the car and not the stock.

And for Nio, don’t buy the car or the stock.

“Cleverness is a gift, kindness is a choice,” said founder and CEO of Amazon Jeff Bezos.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

September 27, 2018

Fiat Lux

Featured Trade:

(THE RATS ARE LEAVING THE SINKING SHIP AT FACEBOOK)

(FB)

It could end up all in tears for Facebook (FB).

This was the key takeaway from shocking news that Instagram’s CEO Kevin Systrom and CTO Mike Krieger quit on the spot.

The ideal word to describe this new development is devastation.

Ultimately, this could pave the way for Facebook to screw up Instagram.

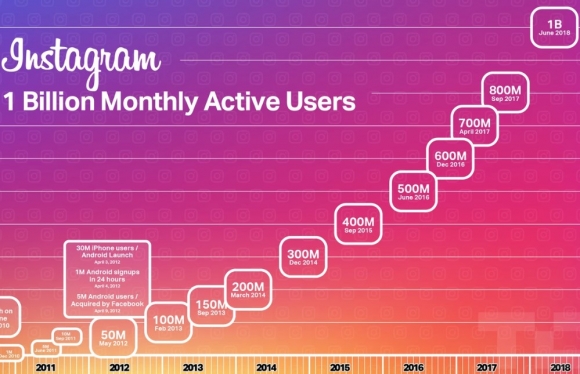

Instagram was the crown jewel in Facebook’s portfolio and recently topped the 1 billion monthly active user (MAU) mark.

Leonardo da Vinci once famously said, "Poor is the pupil who does not surpass his master.”

When founder Systrom sold his company to Facebook for $1 billion in 2012, Instagram had 50 million monthly active users.

Preconditioned in the contract, Systrom was promised a high degree of autonomy that would allow him to grow Instagram as he saw fit.

The relationship was harmonious until 2018 when the pupil surpassed his master in innovation.

Instagram’s growth trajectory has been the envy of Facebook for some time, but that could be explained by the law of numbers and Instagram starting from a small base of users.

Peel back the skin and the situation has been festering for some time.

It came to light that Mark Zuckerberg issued a “throttling back” promotion and marketing for Instagram that peeved Systrom.

This crushed the referral numbers on Instagram, and it almost appeared that Zuckerberg wanted to deliberately bottleneck the growth of Instagram.

On the product engineering side, complication started to mount.

In the past, an Instagram photo uploaded onto Facebook was labeled with an Instagram insignia clearly showing the photo source came from Systrom’s company.

Zuckerberg tweaked this detail and removed the Instagram logo, making it seem that the content originated from Facebook.

Facebook started taking credit for Instagram’s content, and that sent Systrom bouncing off the walls inside his own company that was promised autonomy.

Even though this disagreement seems irrelevant, it showed the intent of Facebook going forward.

This was the beginning of the meddling behind the scenes, and the founder of Instagram aborted ship while he could.

Facebook stealing content and innovation from Instagram damaged Instagram’s team spirit as well.

It came to the point where Systrom saw no way out. After an extended paternity leave that gave him some free time to refresh his vision, he thought the only choice that Zuckerberg left him was to throw in the towel.

I have said numerous times that for Facebook to move on, Zuckerberg must relinquish his role as CEO.

Any CEO in the world operating at the performance level of Zuckerberg would have been sacked long ago.

Zuckerberg is an anomaly because of his stranglehold on voter’s rights excludes him from ever firing himself.

Facebook COO Sheryl Sandberg is quoted as saying “people are fired at Facebook on a regular basis for not doing their jobs.”

People are fired at Facebook but not Zuckerberg.

Anytime the sushi hits the fan at Facebook, Zuckerberg conveniently fires others involved and washes his hands of the mess.

Granted, Instagram’s success was aided by Zuckerberg’s resources and Facebook’s embedded base, but this debacle is laid squarely on the Zuck’s shoulders.

Systrom and Krieger did not give a specific reason for the abrupt departure, which usually means they left unsatisfied.

Since they are the bosses of their own creation, the only factor could be personal or Facebook – easy to guess this one.

Instagram is starting to cannibalize its parent company - a major headwind for this company and stock.

Users are quitting Facebook in droves, and Zuckerberg’s only answer is to become Instagram, which Facebook already owns.

That is why the theft of credit due and engagement began in the first place.

The only bonkers move that could happen next is if Zuckerberg installs himself as the new CEO of Instagram.

Shareholders were biting their nails when they heard this news.

You would think Facebook would do everything they possibly could to entice Systrom and Krieger to stay.

They are the best thing going for Facebook right now.

In allowing this to happen, Facebook creates a massive leadership vacuum at the top of Instagram.

Whispers from Silicon Valley have one of Zuckerberg’s close friends taking over at Instagram, which would be a monumental error.

The outsized risk is if Instagram starts morphing into another Facebook, and engagement sours and usership drops like dead flies.

Facebook has demonstrated its misunderstandings of operating in a climate of big data concerns.

I have also documented how the digital ad industry will have a day of reckoning that is on the horizon, albeit not anytime soon.

Instagram’s CEO certainly closely observed how WhatsApp founders Jan Koum and Brian Acton ditched their brainchild after Zuckerberg rammed down their throats that he would accept the adoption of digital ads.

Former CEO Acton was in the news again, too. He harshly criticized the way Facebook operates, specifically slaughtering Sandberg’s greedy persona and unethical stance toward data privacy models.

In the same interview, he claims he was coached up to mislead European regulators and explain that combining these two data troves, Facebook and WhatsApp, would be near impossible when in reality it was not.

The European Commission fined Facebook $122 million two years later for false information in the original filing, and Facebook maintains these mistakes were unintentional.

If Facebook wants to use its business to practice crony capitalism and push the border of the truth, then it will catch up to them.

Zuckerberg’s imposing his will for the interests of himself and his best friends has been a growing trend at Facebook. As next quarter’s earnings season approaches, Facebook’s stock could get hit hard.

As momentum stagnates, shareholders are concerned that Zuckerberg is forcing out his best and brightest talents.

These decisions smell of desperation to control the company he created. And as fresh leaks about the mismanagement come to light, investors must stay away from Facebook.

Mismanagement at this company did not happen in one day.

Let’s trace back the performance of chief operating officer Sheryl Sandberg a few years ago or her lack of it.

The executive was busy on her book tour around America that took her to many cities promoting her book “Lean In.”

She also wrote another book on top of that.

She even had time to promote her books on daytime talk show Oprah.

At the same time, Zuckerberg was in the middle of completing his personal goal of visiting the 30 states he had never set foot in before.

His “personal challenges” brought him in touch with real Americans, which is almost absurd, since it almost sounds as if he had grown up in Bangladesh, barely spoke a word of English, and is not American, which he is.

Another “personal challenge” of Zuckerberg was learning Mandarin Chinese and running through the smog of Beijing while being pictured in front of the Forbidden City.

When did Zuckerberg and Sandberg have time to run Facebook?

While the executive management was out of the office, the seeds of chaos were sown that all came to light after Sandberg and Zuckerberg were back.

The engineering team had excavated Russian state-sponsored hacking on the platform.

But since the entire 127-member security team worked under the tutelage of Sandberg, the engineering team’s discoveries remained unacted on.

Facebook engineers had also unearthed fake news operations located in Macedonia running riot on its website.

Since most security flaws originate from the engineer side in the form of fake news and manipulation, it’s hard to fathom how there were no channels of communication between the security team and the engineering side.

Sources inside of Facebook note that Sandberg’s business side of Facebook, and Zuckerberg’s engineering side almost mimic “two separate businesses that share the same campus.”

Exposing the manner in which Facebook is run makes it simple to diagnose the extent of major problems cropping up.

Effectively, Facebook grew so fast the past few years that it invited any type of growth – good, bad, and the ugly.

And it did nothing to root out the nefarious actors ruining the platform.

Now comes the hard part of cleaning up the bad and the ugly while segmenting out the good, and persuading the healthy users not to quit.

This will be expensive, time consuming, and awful for the future stock price.

The spillover effects are far from over.

Instagram’s founder and CEO Kevin Systrom quitting isn’t the disease – it’s a side effect.

The disease still hasn’t been cured and remains in the system.

Avoid Facebook shares as the FANGs have decoupled from this digital ad legacy firm.

The days of stellar growth are in the rearview mirror, and the stock won’t experience the parabolic price action it saw in the past.

Facebook needs major internal surgery in its management ranks. Until then, it’s a dysfunctional titanic unsure of when the next iceberg will hit.

Expect surprises, but surprises to the downside.

“Someone once described entrepreneurship to me as a series of happy accidents,” said founder and former CEO of Instagram Kevin Systrom.

Mad Hedge Technology Letter

September 26, 2018

Fiat Lux

Featured Trade:

(DID SIRIUS OPEN UP PANDORA'S BOX?),

(SPOT), (P), (SIRI), (AAPL), (AMZN)