Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Modern tech has an unseen dark side to it.

Coders relish the opaqueness surrounding the industry infatuated with developing the next big thing to take Silicon Valley by storm.

There is nothing opaque about the Mad Hedge Technology Letter.

I grind out recommendations and you follow them. Period. End of story.

To put it mildly, the letter has gotten off to a flying start since its inception in February 2018, and there is no looking back, only looking forward.

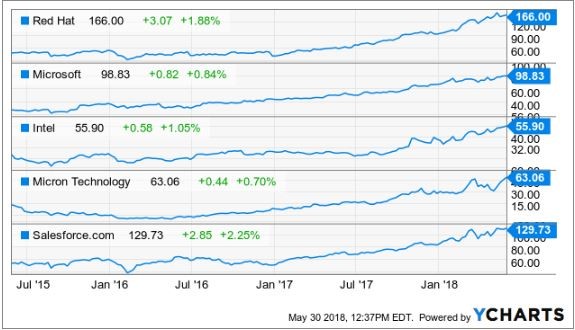

Micron (MU), Red Hat (RHT), Microsoft (MSFT), and Intel (INTC), just to name a few, have been solid recommendations standing up to all the nonsense and mayhem permeating throughout the periodically irrational markets.

Have you noticed lately when you open up the morning paper while sipping on a steaming mug of Blue Bottle Coffee, that almost every story is about technology?

It's not a mistake. I swear.

Technology is permeating into the nooks and crannies of our society and the leaders of this movement are laughing all the way to the bank.

One of those aforementioned pioneers is no other than local lad, Salesforce CEO and perennial Facebook basher Marc Benioff.

I recommended Salesforce at $110 and it was one of the first positions in the Mad Hedge Technology portfolio.

You can't blame me.

I saw this stock pick from a million miles away and I will explain why.

Salesforce set ambitious targets that nobody thought were realistic at the time.

How high in the sky does Benioff want to build his castles?

By 2022, Marc Benioff set out sales targets of a colossal $20 billion per year.

Then Benioff gushed that Salesforce would pass the $40 billion mark, done and dusted by 2028 and $60 billion by 2034.

Remember that tech CEOs are incentivized to forecast ludicrous sales targets because it lures in the unknowledgeable investor.

Unknowledgeable or pure genius, it does not matter, Salesforce is an emphatic buy.

Salesforce is the ultimate growth stock.

In 2016, annual revenue came in at $6.67 billion, which is about the same size as a middle level semiconductor company.

They followed that up with $8.38 billion in 2017, demonstrating the parabolic shaped trajectory of the company.

At the end of fiscal year 2017, Salesforce announced that it expects revenue of around $12.60 billion in 2019.

The latest earnings report, Benioff disclosed full year guidance of $13.13 billion.

This puts Salesforce in the running to achieve its lofty aspirations.

Apparently, the castles Benioff is building aren't in the sky after all.

Theoretically, if Benioff expands the business into a $16 billion to $16.5 billion business by 2019, Salesforce will have a more than likely chance to pass the $20 billion mark by the end of 2020, a full two years than initially thought.

Salesforce will have ample wiggle room on the way to $20 billion if it is 2022 for which it aims.

Why am I rambling on about revenue?

It's the only metric that Salesforce investors value.

The company registered two straight years of less than $200 million in profits then followed it up with a less than stellar 2016 where it lost almost $50 million.

Don't expect any dividends from this neck of the woods anytime soon especially after acquiring MuleSoft, an integration software company, for $6.5 billion last quarter.

This purchase will add another $315 million of annual revenue to Salesforce's quest of eclipsing its future sales targets. This was after MuleSoft made $296.5 million in 2017 before it became a part of Marc Benioff's stable.

Benioff has proved a shrewd dealmaker, taking advantage of cheap capital to add suitable parts to his business.

Since 2016, Benioff has snapped more than 50 niche software companies that he rebrands as Salesforce products and sells them as add-on products.

This is further evidence that any funds available will be allocated toward reinvestment into products and services deeming any future dividend inconceivable, especially with the elevated revenue targets to surpass.

As for the business. Do we still need to talk about it?

Rip-roaring growth was seen across the board with total revenue increasing 25%.

Investors should stay away from any cloud company that is growing less than 20%.

Market intelligence firm International Data Corporation (IDC) voted Salesforce as the No. 1 client relationship management (CRM) platform for the fifth consecutive year.

It is the industry leader in sales, marketing, service, and increased market share in 2017, more than its closest competitors.

Larry Ellison must be tearing his hair out as Oracle's (ORCL) share price has been excommunicated to purgatory indefinitely.

Oracle is a company that I have been pounding on the tables to stay away from.

The Mad Hedge Technology Letter seldom recommends legacy companies that are still legacy companies.

Driving past his former estate, emanating from a sparkling perch in Incline Village overlooking Lake Tahoe, my neighbor gives me the goose bumps.

The property was later sold for $20.35 million. All told, Larry has around $100 million invested in real estate dotted around Incline Village. I sarcastically mentioned to him last time we bumped into each other to call me immediately when his $90 million estate in Kyoto, Japan, hits the market.

Oracle's position in the pecking order is a telltale sign of the inability to land the creme de la creme government contracts that ostensibly fall into Amazon (AMZN), Alphabet (GOOGL), and Microsoft's lap.

And it's not surprising that Larry is spending more time tending to his vast array of glittering luxury properties around the world rather than running Oracle.

Oracle is like a deer caught in the headlights and Marc Benioff is at the wheel.

On the Forbes 500 rankings, Salesforce has moved up almost 200 spots.

This position will rise as Salesforce is under contract booking a further $20.4 billion of commitments driven by its subscription services offering cloud products.

On the domestic contract front, it was much of the same for Salesforce, which inked premium deals with the U.S. Department of Agriculture, Kering, and sports apparel giant Adidas.

International companies such as Philips and Santander UK are expanding their relationships with Salesforce. A firm nod of approval.

Salesforce has been voted in the top three of most innovative companies for the past eight years by reputable Forbes magazine. The list was started in 2011, and it has never dropped out of the top three.

The gobs of innovation are the main logic behind the top five financial institutions expanding their relationship with Salesforce by an extra 70%.

Once companies start using the CRM platform, they become mesmerized with the premium add-ons that help companies run more efficiently.

Benioff has been a huge proponent of artificial intelligence (A.I.) and is an outsized catalyst to product enhancement gains.

Salesforce has taken Einstein, it's A.I. platform, and allowed all the applications to run through it.

The integration of Einstein has resulted in more than 2 billion correct predictions per day paying homage to the quality of A.I. engineering on display.

Instead of hiring a whole team of in-house data scientists, Salesforce is A.I. functionality by the bucket full and it is easy to use on its platform.

In some cases, incorporating Salesforce's A.I. into the business has bolstered other companies' top line by 15%.

Often, Salesforce's A.I. tools are declarative meaning the technology can identify solutions without a fixed formula.

Benioff has choreographed his strategy perfectly.

He is betting the ranch on unlocking data from legacy companies that migrate to his platform.

MuleSoft will help in this process of extracting value, then A.I. will supercharge the data, which is being unlocked.

What does this mean for Salesforce?

Higher revenue and more clients leading to accelerated growth. The share price has powered on north of $130, and after I recommended it at $110, I am convinced this stock will surge higher.

Salesforce is an absolute no-brainer buy on the dip.

Growth Means Shiny New Office Buildings

_________________________________________________________________________________________________

Quote of the Day

"If we become leaders in Artificial Intelligence, we will share this know-how with the entire world, the same way we share our nuclear technologies today." - said current President of Russia, Vladimir Vladimirovich Putin.

Mad Hedge Technology Letter

May 30, 2018

Fiat Lux

Featured Trade:

(WHICH UNICORN WILL EAT YOUR LUNCH?),

(UBER), (AIRBNB)

Hold onto your hats or you might get swept up.

Avoid the projectiles while you're at it.

There are no imminent tsunami warnings. But something else is happening in the world that you might want to know about.

Disruption.

The pace of disruption is accelerating beyond all recognition.

CEOs are here today and gone tomorrow, exiting through the revolving door of companies devoured by disruption.

Are we on the verge of the rise of the robots?

I wouldn't go that far ... yet.

But the truth is that disruption is redefining the world as we know it.

The latest stage of modern disruption came to us by way of smartphone apps.

This application created clear-cut platforms allowing companies to penetrate deep into the smartphone ecosystem where most of the youth are hanging out with consequences galore.

The unfolding of the sharing economy has been nothing short of breathtaking.

Take Uber.

Uber was so disruptive that its former CEO, Travis Kalanick, disrupted himself out of a job at Uber.

That is quite disruptive.

First, look at its business model.

Uber does not actually create intrinsic value.

It does not create something you can eat, sleep on, or imbibe.

Uber is a vanilla app that brings together a marketplace for riders and ride givers effectively becoming a de facto broker.

Brokers have been around since the advent of time.

This type of technology lacks quality, and half the undergraduate computer engineers in university could fabricate something similar with ease.

Disrupters formulate a plan, scavenge for weak points, identify backdoor entrances, then wreak havoc to the guts of the system.

At an auction late last year in 2017, New York City taxi medallions were going for a derisory $186,000, precipitously lower than the $1.3 million in 2014. A spate of taxi driver suicides ensued.

The 86%-plus drop in value is directly correlated to Uber's advancement into the taxi industry.

It's that simple.

Taxi drivers have been left holding the bag and in big-time debt crying their eyeballs out.

Buy low and sell high. I guess taxi drivers didn't get the message.

The initial point of attack was to render the taxi medallion utterly useless.

To find drivers of its own, Uber subcontracted regular people as drivers.

Genius! Another problem solved.

In one fell swoop, the Uber app made every adult with a driver's license a taxi driver anywhere in the world.

Ka-ching!

New York City capped the total amount of medallions in circulation at 13,587.

The flood of new drivers crushed the price of taxi fares around the world bettering the lives of the average Joe.

Uber also figured it would be cheaper to allow drivers to use their own private car, shedding the costs to maintain, finance, and service one of the highest inputs of taxi business models.

Uber and the rest of the tech industry benefit from being the least regulated industry in the world.

The lack of regulation was a golden ticket to test the rules of the road.

That is exactly what unfolded.

Management even approved an app inside the Uber app bent on skirting the challenges of secret strings organized by police enforcement.

The app, called Greyball, reaffirmed the company ethos of pushing regulation to the brink of no return.

Any emerging tech company not pushing the borders of regulation should not be in technology.

Everything reverts back to the fact that emerging tech is held in check by one metric - growth.

Growth solves anything in the eyes of tech investors.

Yes, it's unfair that Walmart and traditional media companies don't get the same free pass, but life is unfair.

Uber had incentive to break all the rules because surpassing growth targets would lure in additional financing.

The outperforming growth is the main logic justifying an investment in a cash-burning enterprise.

People don't like losing money but people with deep pockets will wait it out if they know there is a golden prize at the end of the road.

The administration has grossly failed to regulate technology, even after the Cambridge Analytica scandal came to light.

This all bodes well for technology companies.

Europe is the hotbed for global data regulation. Large tech companies have been astutely planning for the new General Data Protection Regulation (GDPR) rules to take effect.

The companies that do not create anything proprietary are at serious risk of being passed over in the history books.

Therefore, the aggressive tactics "broker apps" adopt are completely justified, and it is paying off in spades as the 2019 IPO approaches.

That upcoming momentous day will enrich many people associated with Uber and in hindsight, management might acknowledge that its initial wild ways were worth the price of the mild rebuke.

The underlying problem is tech disruption, and the success of it has many unintended consequences - particularly social upheaval and job losses.

Myanmar born "Kenny" Chow's body was found floating face down in the river around the Brooklyn Bridge after his family said he disappeared a few days ago.

This was the fifth New York taxi driver suicide in the past five months.

Chow had taken out high-interest loans to pocket his $700,000 New York City medallion and his precarious financial situation, brought upon by the success of Uber, led him to leap to his death.

Sadly, the thirst to grow means taking away other people's livelihood and even their option to live.

We know the pace of change is in full gear. However, the amount of people being economically and socially displaced is a worrying sign that public opinion cannot absorb the accelerating pace of disruption.

More regulation? Probably not.

Chow isn't the first person to lose a job because of technology and won't be the last.

Enter the hotel industry.

Accommodation-sharing app Airbnb was the end for hotels as we knew them.

Airbnb is the Uber of short-term rentals, matching renters with private home owners. They earn revenue by the servicing fee incurred for the brokering.

The harbinger of doom never came to materialize for the hotel industry, which is enjoying record profits - the likes we have never seen before.

The synchronized economic recovery fueled the demand for hotel rooms located in economic hubs close to urban centers.

As we found out, 90% of business travelers have no desire to stay in other people's houses, and the assortment of services hotels offer is critical for the prototypical business traveler.

The hotel industry saved its bacon while Airbnb is thriving. A win-win situation.

You thought wrong.

Airbnb services are a hit with tech-savvy Millennials, which data reveals as upper-middle class, young, and addicted to wanderlust.

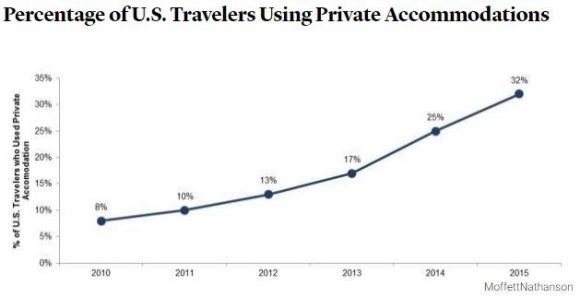

The percentage of American travelers using private housing has more than quadrupled since 2010.

The surge in Airbnb users coincides with an explosion of global tourism led by the bourgeoning Chinese middle-class flooding tourist meccas all over the world.

The app that champions individuals to open up their personal homes is effectively pricing out locals from the dwindling supply of available residential housing.

The problem is most acute in Spain and every other tourist haven.

Madrid currently has 9,000 private units rented out to globe-trotting tourists, a sevenfold rise since 2013.

Of these 9,000 units, 2,000 are illegal and do not possess the necessary permits.

In the port city of Valencia, online-based private housing rose more than 30% since 2016.

To cope with the droves of tourists, the local government is attempting to pass legislation by removing 95% of the housing supply from house-sharing applications, in effect giving local residents back their neighborhoods.

Airbnb is another prime example of the severe lack of regulation that tech revels in, which in turn boosts the pace of technological disruption.

Blame the government. Lawless industries breed marginal behavior. We are all just a function of our environment.

Local neighborhoods are being ravaged by these short-term rentals and entire cities are being turned into massive tourist depots with little afterthought of the local people.

Examples are legion. Venice, Italy; Prague, Czech Republic; Dubrovnik, Croatia; Lisbon, Portugal. And the list goes on and on.

These cities are the victims of their own success and are grappling with hordes of tourists ruining the charm and souls of their beloved cities.

Granted, rapid development of the tourist industry trended toward this result, but the pace of upheaval has accelerated beyond anyone's wildest dreams.

For years, taxi drivers were seen as the first cohort to eventually be swept away with the magic of technology, but it happened too fast for people to accept.

I hope your uncle isn't a taxi driver.

Unfortunately, things are about to get a lot worse as the first stage of disruption transitions to the history books and the next stage is upon us.

The second stage will displace even more people as this unregulated industry sees everything as a zero-sum game.

This stage will incorporate higher grade tech - not just a broker app - that will change the world faster and to a larger degree than anything witnessed today.

And the next stage will incorporate proprietary technology the world has never seen before.

Imminent rollout of self-driving cars hitting the market in 2019 to 2020, will be the first progression for investors to digest.

Followed directly after self-driving will be the broad-based adoption of 5G delivering Internet connection speeds more than 100 times faster than current speeds, stoking a new leg up of commercialization.

As for now, Uber and Airbnb, which both plan to go public in 2019, are eye-opening success stories catapulting them into the top five of global unicorns along with the Uber of China (Didi Chuxing), the Apple of China (Xiaomi), and the Grubhub of China (Meituan-Dianping).

And if you somehow descend on Barcelona during this summer's tourist season, you might want to avoid the tourist protests.

_________________________________________________________________________________________________

Quote of the Day

"They counterfeit our goods, steal our intellectual property rights, and hack the computers of our industries and government. Something must be done about it." - said Director of the United States National Economic Council Larry Kudlow when asked about a specific country.

Mad Hedge Technology Letter

May 29, 2018

Fiat Lux

Featured Trade:

(HERE ARE SOME EARLY 5G WIRELESS PLAYS),

(T), (VZ), (INTC), (MSFT), (QCOM), (MU), (LRCX), (CVX), (AMD), (NVDA), (AMAT)

How would you like to be part of the biggest business development in the history of mankind?

This revolution will increase business functionality up to 10 times while flattening costs by up to 90%.

Still interested?

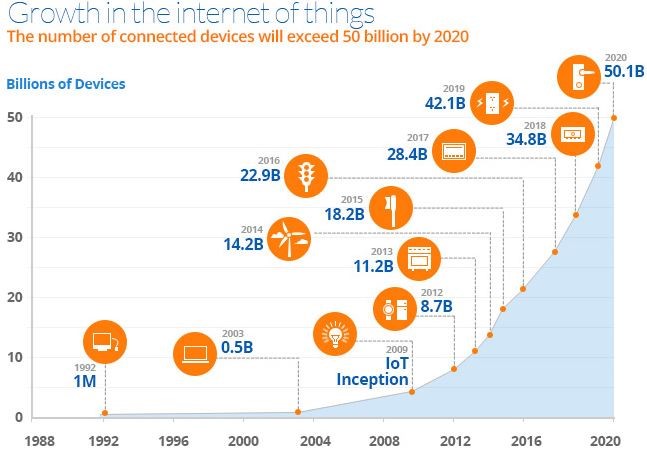

Enter the Internet of Things (IoT).

The Internet of Things (IoT) can be boiled down to Internet connectivity with things.

Your luxury juice maker, hair removal kit, and multi-colored Post-its will soon be online.

No, you won't be able to have Tinder chats with the new connectivity, but embedded sensors, tracking technology, and data mining software will aggregate a digital dossier on how products are performing.

The data will be fed back to the manufacturing company offering a comprehensive and accurate review without ever asking a human.

The magic glue making IoT ubiquitous and stickier than a hornet's nest is the emergence and application of 5G.

4G is simply not fast enough to facilitate the astronomical surge in data these devices must process.

5G is the lubricant that makes IoT products a reality.

Verizon Communications (VZ) and AT&T (T) have been assiduously rolling out tests to select American cities as they lay the groundwork for the 5G revolution.

The aim is for these companies to deliver customers a velocious 1 Gbps (gigabits per second) wireless connection speed.

Delivering more than 10 times the average speed today will be a game changer.

America isn't the only one with skin in the game and some would say we are not even leading the pack.

China Mobile (CHL) is carrying out a bigger test in select Chinese cities, and Chinese telecom company Huawei can lay claim to 10% of the 5G patents.

Americans should start to notice broad-based adoption of 5G networks around 2020.

Once widespread usage materializes, watch out!

It will go down in history books as a transformational headline.

The IoT revolution will follow right after.

Until the 5G rollout is done and dusted, tech companies are licking their chops and preparing for one of the biggest shifts in the tech ecosphere affecting every product, service, and industry.

The worldwide IoT market is poised to mushroom into a $934 billion market by 2025 on the back of cloud computing, big data, autonomous transport technology, and a host of other rapidly emerging technology.

The arrival of 5G will have an astronomical network effect. Companies will be able to enhance product specs faster than before because of the feedback of data accumulated by the tracking technology and sensors.

The appearance of this flashy new technology will spawn yet another immeasurable migration to technological devices by 2020.

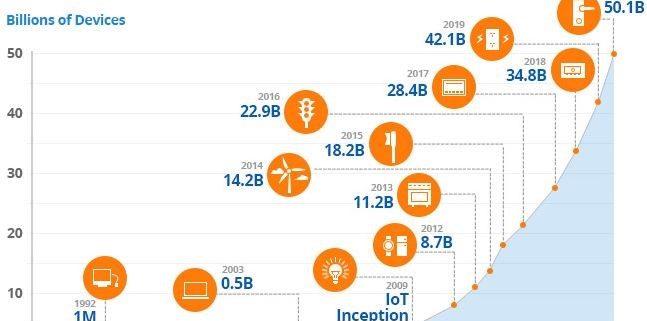

In just two years, the world will play host to more than 50 billion connected devices all pumping out data as well as consuming data.

What a frightful thought!

IoT's synergies with new 5G technology will have an unassailable influence on the business environment.

For instance, industrial products in the form of robots and equipment will be a huge winner with 5G and IoT technology.

The industrial IoT market is expected to sprout to $233 billion by 2023.

Robots will pervade deeply into economic provenance acting as the mule for brute strength heavy labor plus more advanced tasks as they become more sophisticated.

Total global spending related to IoT products will surpass 1.4 trillion dollars by 2021, according to the International Data Corporation (IDC).

IoT growth will become most robust in the thriving Asian markets fueled by a bonus tailwind of the fastest growing region in the world.

The advanced automation abilities of Germany and the U.K. will also give them a seat at the table.

Micron CEO Sanjay Mehrotra gushed about the future at Micron's investor day celebrating IoT and data as the way forward. Mehrotra explained that the explosion of IoT products will create a new tidal wave of "growing demand for storage and memory."

Chips are a great investment to grab exposure to the 5G, IoT, and big data movement.

Up until today, the last generation of technological innovation brought consumers computers and smartphones.

That world has moved on.

Open up your eyes and you will notice that literally everything will become a "data center on wheels or on feet."

To arrive at this stage, products will need chips.

As many high-grade chips as they can find.

Data centers are one segment in dire need of chips. This market will more than double from $29 billion in 2017 to $62 billion in 2021.

The general-purpose chip market for servers is cornered by Intel.

Industry insiders estimate Intel's market share at 98% to 99% of data center chips. Clientele are heavy hitters such as Amazon Web Services, Google, and Microsoft Azure along with other industry peers.

The only other players with data server chips out there are Qualcomm (QCOM) and Advanced Micro Devices Inc. (AMD).

However, there have been whispers of Qualcomm shutting down the 48-core Centriq 2400 chip for data centers that was launched only last November after head of Qualcomm's data center division, Anand Chandrasekher, was demoted via reassignment.

AMD's new data center chip, Epyc, has already claimed a few scalps with Baidu (BIDU) and Microsoft Azure promising to deploy the new design.

IoT integration is the path the world will take to adopting full-scale digitization.

Microsoft just announced at its own Build 2018 conference its plans to invest $5 billion into IoT in the next four years.

The Redmond, Washington-based company noted operational savings and productivity gains as two positive momentum drivers that will benefit IoT production.

Consulting firm A.T. Kearny identified IoT as the catalyst fueling a $1.9 trillion in productivity increases while shaving $177 billion off of expenses by 2020.

These cloud platforms give tech companies the optimal stage to win over the hearts and dollars of non-tech and tech companies that want to digitize services.

Many of these companies will have IoT products percolating in their portfolio.

Examples are rampant.

Schneider Electric in collaboration with Microsoft's IoT Azure platform brought solar energy to Nigeria by the bucket full.

The company successfully installed solar panels harnessing its performance using IoT technology through the Microsoft cloud.

Kohler rolled out a new lineup of smart kitchen appliances and bathroom fixtures coined "Kohler Konnect" with the help of Microsoft's Azure IoT platform.

Consumers will be able to remotely fill up the bathtub to a personalized temperature.

Real-time data analytics will be available to the consumer by using the bathroom mirror as a visual interface with touch screen functionality giving users the option to adjust settings to optimal levels on the fly.

Kohler's tie-up with Microsoft IoT technology has proved fruitful with product development time slashed in half.

To watch a video of Kohler's new budding relationship with Microsoft's Azure IoT platform, please click here.

It is safe to say operations will cut out the wastefulness using these new tools.

Look no further than legacy American stocks such as oil and gas producer Chevron (CVX), which wants a piece of the IoT pie.

Chevron announced a lengthy seven-year partnership with Microsoft's Azure platform.

The fiber optic cables inside oil production facilities generate more than 1 terabyte of data per day.

In the Houston, Texas, offices, sensors installed six miles below the surface shoot back data to engineers who monitor human safety and system operations on four continents from the Lone Star State.

The newest facility in Kazakhstan, using state-of-the-art technology, will produce more data than all the refineries in North America combined.

Using the aid of artificial intelligence (A.I.), computers will analyze seismic surveys. This pre-emptive technology customizes solutions before problems can germinate.

The new smart-work environment will multiply worker productivity that has been at best stagnant for the past generation.

To get in on the IoT action, buy shares of companies with solid IoT cloud platforms such as Microsoft and Amazon.

Buy best-of-breed chip companies such as Nvidia (NVDA), Intel (INTC), Advanced Micro Devices (AMD) and Micron (MU).

And buy tech companies that produce wafer fab equipment such as Applied Materials (AMAT) and Lam Research (LRCX).

_________________________________________________________________________________________________

Quote of the Day

"Don't be afraid to change the model." - said cofounder and CEO of Netflix Reed Hastings.

Mad Hedge Technology Letter

May 25, 2018

Fiat Lux

Featured Trade:

(WHERE 5G CONNECTIVITY WILL TAKE US),

(T), (VZ), (INTC), (TSLA), (AAPL), (GOOGL)

AT&T (T), Verizon (VZ), and the other telecom heavies are in the process of investing $30 billion to make sure that fifth-generation wireless, or 5G, will roll out on time in 2020.

What 5G will do is improve the functionality of IoT (Internet of Things) by 10 times at one-tenth the cost, bringing a 100X increase of functionality over price.

The last time I saw a leap that great was when Intel (INTC) brought out its groundbreaking 8008 8-bit microprocessor chip in 1972. I remember it like it was yesterday.

The news that gravitational waves were discovered, as well as wrinkles in the space-time continuum, was big news in my family. 5G will be of that order.

Of course, we knew it was coming. It was just a matter of when.

I have 11- and 13-year-old girls (I can't help it if the plumbing still works!). Whenever we drive somewhere, we carry out what Einstein called "thought experiments."

They will come up with scientific questions, and I then direct them into finding their own answers through a series of prodding and hopeful questions.

It is much like how the children of royalty were tutored during the Middle Ages.

So they asked, "When will we get driverless cars?" which they had heard about on TV.

I answered in about two years, but that I had friends who run Tesla (TSLA) who already have them now.

And you know the interesting thing they discovered? After two years of beta testing, the cars are starting to develop their own personalities.

Each car has highly advanced learning software. When the mapping software requires one to take a difficult sharp left turn, the vehicle may miss it the first time.

It will then make the next legal U-turn, and then nail that turn every time in the future.

The cars are all programmed to drive like little old ladies. It will never speed, break the law, and always lets other cars cut in front. Over time, some are becoming cautious, while others are getting more aggressive depending on each individual's driving experience.

In other words, experience is turning them into "people."

I asked my daughters, "What would the world be like if everyone had driverless cars?" which will occur in about 30 years, or during their middle age.

They pondered for a moment. Then my older daughter shouted out, "There won't be car accidents anymore!" "Right!" I answered.

"But what will that mean?" I asked.

They puzzled over this.

A few seconds passed. Then it came. "The people who fix cars won't have anything to do!"

"You got it," I replied.

In fact, about 1 million people in the car repair industry will lose their jobs. A small group of vintage car fanatics will survive, much like horse and buggy hobbyists do today.

I pointed out that this is already happening because electric cars don't require any maintenance. You just rotate the tires every 6,000 miles (because electric batteries are so heavy).

I moved on. "Who else will lose their jobs when cars become self-driving?" They hit a brick wall. Then I asked "What else breaks when cars have accidents?"

A few seconds later it came. "People!"

"For sure," I shot back.

Actually, about 35,000 people die in car accidents every year in the United States, and another 500,000 are injured.

This means the demand for doctors, hospitals, and ambulances will go down. Say goodbye to another 1 million jobs.

"So, what else will self-driving cars do?" I was relentless.

My older girl was first: "If cars are driven by computers, it means they can drive closer together." I said, "That was true, but what was the consequence of that?"

The mountain scenery whizzed by. Then they got it.

"There won't be traffic jams anymore."

"Yes!" I blurted out. If a car can drive 70 miles per hour, but only needs to remain one car length behind the one in front of it, that effectively increases the capacity of freeways seven times.

We will never need to build another freeway again. Another 1 million jobs go down the drain.

"What else will self-driving cars do?" I carried on.

They hit a dead end. So, I gave a hint. "What do you see in cities?" After going through buildings, parks, roads, lots of cars, and bridges, I finally got the answer I wanted: "Parking lots."

I then posed the conundrum, "What's the connection between self-driving cars and parking lots?"

Now they were getting into the spirit of the thing. "They won't need them." I replied, "Absolutely."

Self-driving cars won't need to park. They'll just be able to drop you off and drive around the block until you are ready to go home.

This will be economical because after three decades of battery and solar improvements, energy will effectively be free, like air is today.

Oh, and at least 100,000 parking attendants might as well start joining the unemployment lines now.

It gets better.

Entrepreneurs now are developing apps for cars so they never need to park.

In an iteration of the sharing economy, and in a club or membership type format, your car will just drive person to person, selling rides, until you are ready to go home.

Think of it as Uber, without the drivers, that pays you.

Today, parking lots occupy about 15% of the land area of large cities. Self-driving cars will free up a lot of that space for other uses, such as housing and parks.

Then I asked the really big question. "What do all of these changes have in common?"

My 11-year-old picked up on this immediately. "A lot of people are going to lose their jobs!"

"For sure," I bubbled. Notice that every new technology improvement creates a lot of job losses. I went on.

"The trick for you girls is to always stay ahead of the technology curve so your job doesn't get lost, too." This is why I have been sending them to Java development school since they were 8 and 9.

They looked daunted.

And this is what 11- and 13-year-olds were able to figure out. Granted, they were MY kids.

Imagine what Google (GOOGL), Apple (AAPL), and Tesla are doing with this idea. It has become a hot bottom "next big thing." Silicon Valley is now rife with rumors of breakthrough developments and the poaching of staff.

The U.S. military and the Defense Advanced Research Projects Agency (DARPA) are involved in self-driving vehicles in a big way as well, holding regular contests with big prize money and the prospect of mammoth government contracts.

More and more generals and admirals are telling me that the wars of the future will be fought with software.

The bottom line is that things are happening much faster than we imagined possible only a few years ago.

Then my oldest daughter piped up.

"Dad, can I get my driver's license before all the cars are self-driving?" I said, "Sure. What kind of car do you want?"

"A red one."

My first car was a red 1957 Volkswagen Beetle.

On our next trip we will cover gravitational waves, Einstein's Theory of Relativity, and the significance of the clock tower in Bern, Switzerland.

By the way, these girls will be graduating from college in 2026 and 2027 and will be looking for jobs.

Just let me know. :-)

_________________________________________________________________________________________________

Quote of the Day

"Homo sapiens, the first truly free species, is about to decommission the natural selection, the force that made us," said E.O. Wilson, a Harvard University biology professor.

Mad Hedge Technology Letter

May 24, 2018

Fiat Lux

Featured Trade:

(MICRON'S BLOCKBUSTER SHARE BUYBACK)

(MU), (AMZN), (NFLX), (AAPL), (SWKS), (QRVO), (CRUS), (NVDA), (AMD)

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

Growth - Check. Accelerating Revenue - Check. Margins - Check. Earnings beat - Check. Guidance hike - Check.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

Half way into 2018, and there is still a dire shortage of DRAM chips.

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

_________________________________________________________________________________________________

Quote of the Day

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.