Mad Hedge Technology Letter

April 25, 2025

Fiat Lux

Featured Trade:

(THIS TECHNOLOGY IS A FLOP)

(META), (AAPL), (MSFT)

Mad Hedge Technology Letter

April 25, 2025

Fiat Lux

Featured Trade:

(THIS TECHNOLOGY IS A FLOP)

(META), (AAPL), (MSFT)

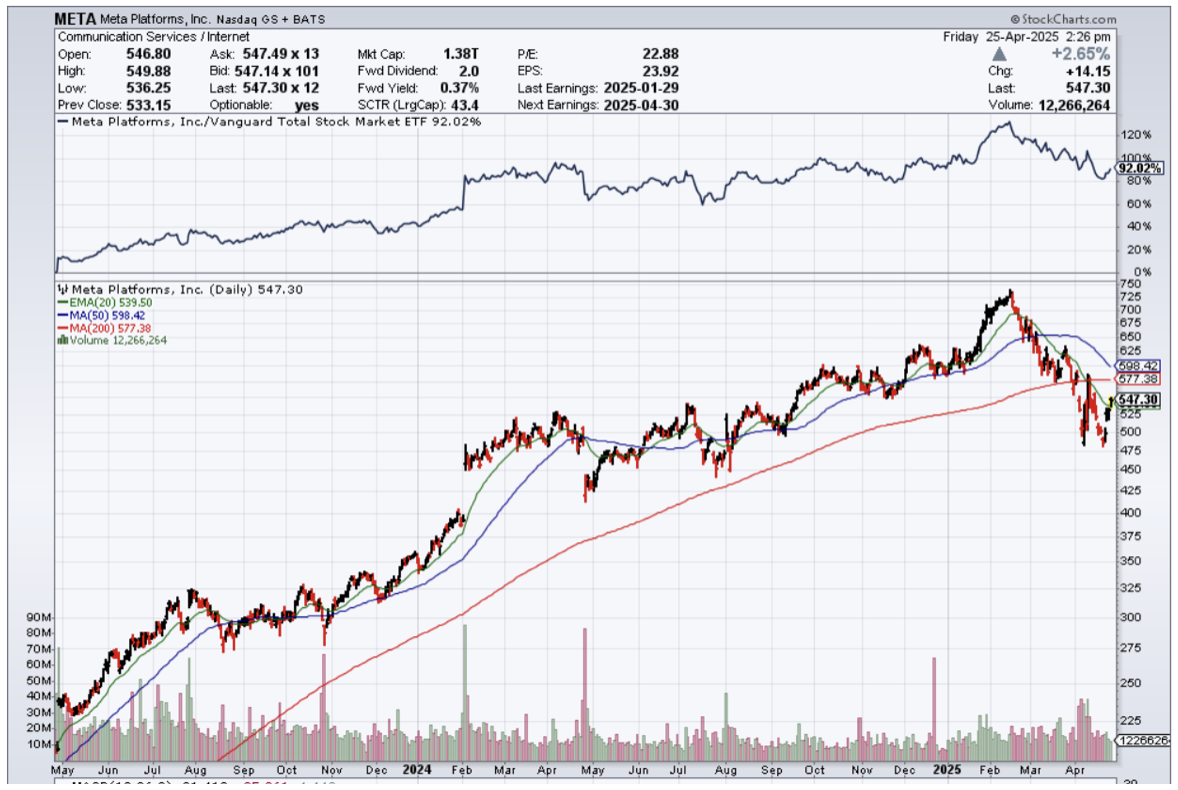

Meta (META) cutting staff in its virtual reality and augmented reality divisions means uncertainty about future products originating from these places.

The juice has not been worth the squeeze.

I think everyone remembers when Founder Mark Zuckerberg had those goofy metaverse commercials depicting him as an avatar when he debuted the company name change from Facebook to Meta.

Well, the metaverse project isn’t working, which is why he’s firing staff from those projects.

The metaverse division has underdelivered and overpromised.

This lethal cocktail of failure is finally forcing management to cut off the fat from its body.

VR and AR are now losing billions of dollars per year, and as the business environment turns more pragmatic, these experimental projects are thrown out for good.

META said its Reality Labs unit recorded an operating loss of $4.97 billion while generating $1.1 billion in sales.

A nice quarterly performance of minus 3 billion dollars has forced management to make some tough decisions.

Now, the AR and VR divisions will be gutted.

Reality Labs is Meta’s unit that makes the Quest family of virtual-reality headsets and Ray-Ban Meta Smart Glasses.

Meta CEO Mark Zuckerberg kick-started his company’s VR endeavors in 2014 when it acquired the startup Oculus for $2 billion. Since then, Zuckerberg has characterized VR and AR as central to his plans to develop the futuristic digital world known as the metaverse, which he has said represents the next major computing platform.

Reality Labs has piled up an operating loss of more than $60 billion since 2020.

The losses cannot just be swept under the carpet.

Meta last week said it would invest between $60 billion and $65 billion in 2025 capital expenditures to expand its computing infrastructure related to artificial intelligence.

Even this AI infrastructure build-out is questionable at this point, as other big tech firms pull back from this type of investment.

Meta released its latest VR headset, the $299 Quest 3S, during its September Connect event and pitched the device as a way for people to watch movies, play games, and work out in VR.

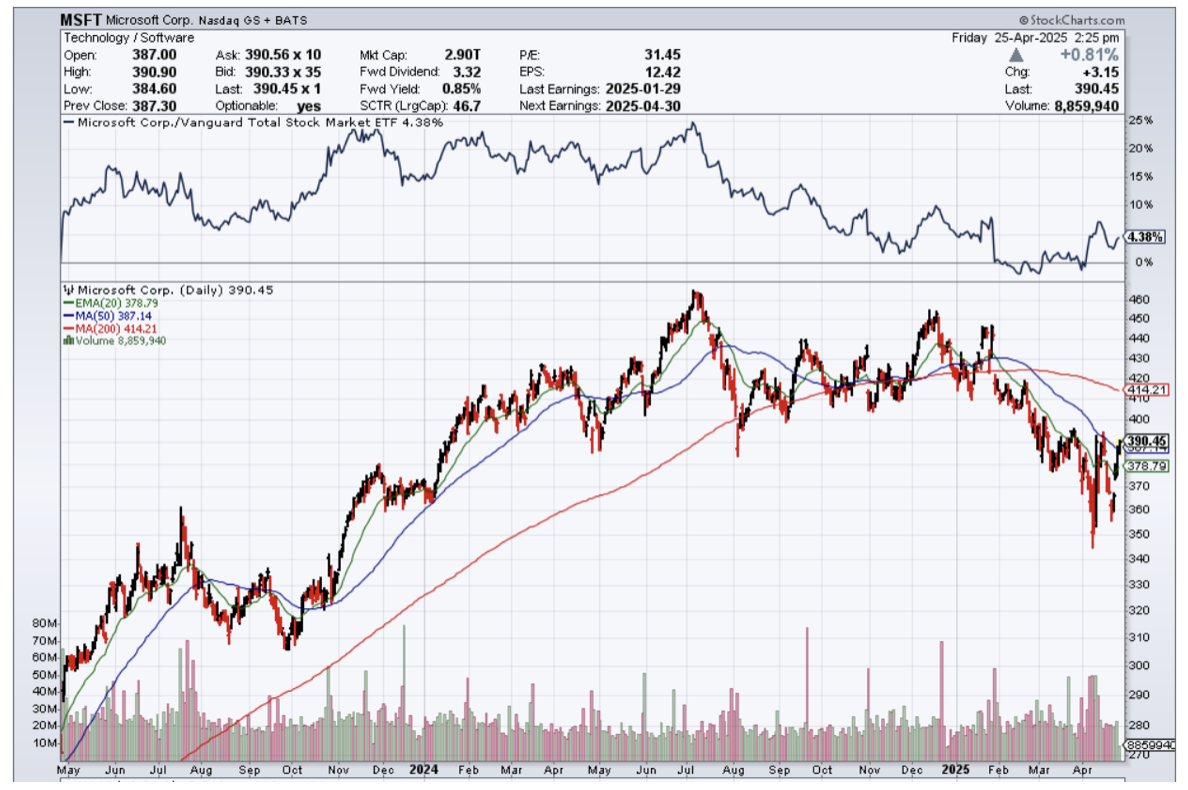

Microsoft (MSFT) has lost at least $5 billion on HoloLens since the launch of the first model in 2016.

The Microsoft HoloLens is a mixed reality headset that allows users to overlay digital information onto the real world, creating a blended experience of physical and digital environments.

Microsoft’s withdrawal from the market for augmented and virtual reality hardware leaves competitors such as Apple and Meta with a less crowded field on which to compete.

Apple (AAPL) is another company that has bet on AR and VR.

In short, VR and AR have been money pits that suck up investment dollars, but deliver nothing in terms of profit.

Whether it is Meta, Apple, or Microsoft, they have all struck out at this technology and will need to embrace the reality that consumers don’t want Google-type technology on their face to interact with a screen.

AR and VR divisions should be buried in the graveyard of attempted technology that people aren’t interested in.

Back to the drawing board…

Mad Hedge Technology Letter

April 23, 2025

Fiat Lux

Featured Trade:

(TESLA HITS AN AIR POCKET)

(TSLA)

Tesla (TSLA) has problems and so do other tech firms at the start of 2025.

Saying that doesn’t give comfort even with a great bull market of 12 years.

The scary thing here is that many tech bulls might believe this is the end of the stock market party.

Moving forward, we will see many tech firms miss gross revenue and profitability.

Then there is the future forecast and I wouldn’t blame management on making excuses using the trade war which they can’t control.

Tesla missed their first quarter revenue target by nearly $2 billion.

Management has literally been in Washington DC getting into politics, and that has hurt Tesla’s stock.

Tesla’s stock almost halved to around $200 before catching a bid.

CEO and Founder Elon Musk said he will step back from his role with DOGE, staying involved part time.

He said he'll continue to spend a day or two a week on government matters, for as long as President Donald Trump wants him to.

Looking forward, a potential key revenue driver is the robo-taxi.

Tesla is set to debut this service in Austin this June, starting with "maybe 10 to 20 vehicles," Musk said.

Tesla also confirmed on the call that the initial launch will include remote human operators who can intervene if a vehicle becomes stuck or encounters an issue.

Musk said the goal is to bring the service to "many other cities in the US by the end of this year," predicting that "there will be millions of Teslas operating fully autonomously in the second half of next year."

Musk said that Tesla would be "the least affected car company" when it comes to tariffs.

"With respect to supply chain risk, something that Tesla has been working on for several years, is to localize supply chains," Musk said. "Tariffs are still tough on a company when margins are still low, but we do have localized supply chains in both America, Europe, and China, so that puts us in a stronger position than any of our competitors."

I do believe the low 200 level for the stock should hold as resistance for TSLA.

Much of the bad news, and there is a lot, is already priced into the stock.

It will be interesting to see if the brand recovers, because the product is deeply unpopular in California and Western Europe.

To be honest, while we wait on the robo-taxi to roll out, Musk saw an air pocket and we are hitting that with full turbulence.

That being said, if there was not a change of administration, there is no way he could make headway with the robo-taxi division.

Musk is waiting on the robo-taxi to save the day and the possibility that happens is better than 50%. In the meantime, I believe he will have a hard time moving sales of his standard EV. He has done a lot of damage by alienating half of his addressable audience.

I believe the stock slowly creeps higher, but in a volatile way.

As for Musk, I think he’ll be spending more time at his day job moving forward and that should help the stock just for that.

“People work better when they know what the goal is and why.” – Said Elon Musk

Mad Hedge Technology Letter

April 21, 2025

Fiat Lux

Featured Trade:

(DIFFICULTY OF DOING BUSINESS FOR CHIP COMPANIES)

(NVDA), (TSM), (HUAWEI)

The U.S. appears to have made a massive blunder in its chip control blocking of China.

The U.S. Commerce Department said last week that Nvidia’s H20 graphics processing units — designed to comply with previous U.S. restrictions — would now require export licenses, as would additional chips from AMD. Nvidia says it has already halted exports of the GPUs, resulting in a quarterly charge of approximately $5.5 billion.

Could this be an example of the government getting in its own way?

Examples of these local AI chipmakers include tech powerhouse Huawei and the partially state-owned and publicly listed Cambricon Technologies, which designs GPUs.

Shares of Cambricon were up over 10% in the past five trading days amid news of the latest Nvidia controls. The stock is up over 400% in the past 12 months.

Can China fill the gap?

Huawei is the clear leader in China’s race to find an Nvidia competitor. The U.S.-blacklisted company has been working on its own improvements to compete with the leading technology.

Huawei remains about a generation behind in chips, but that won’t be the case for long.

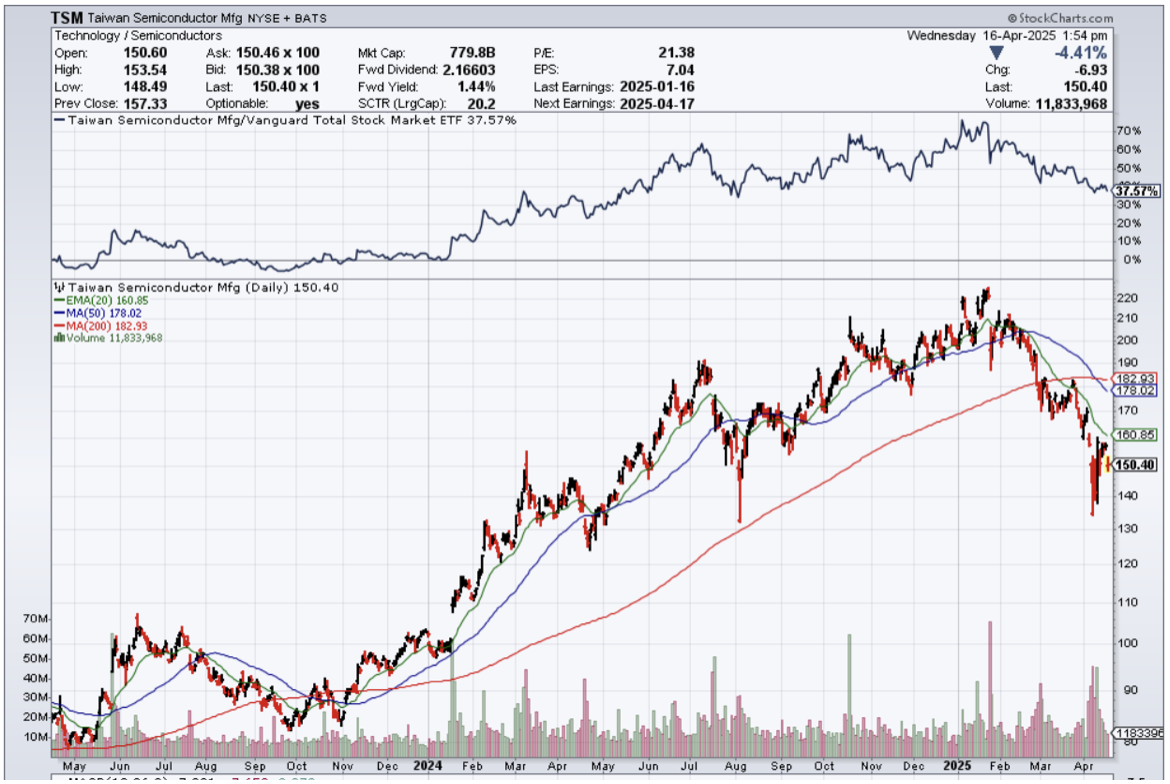

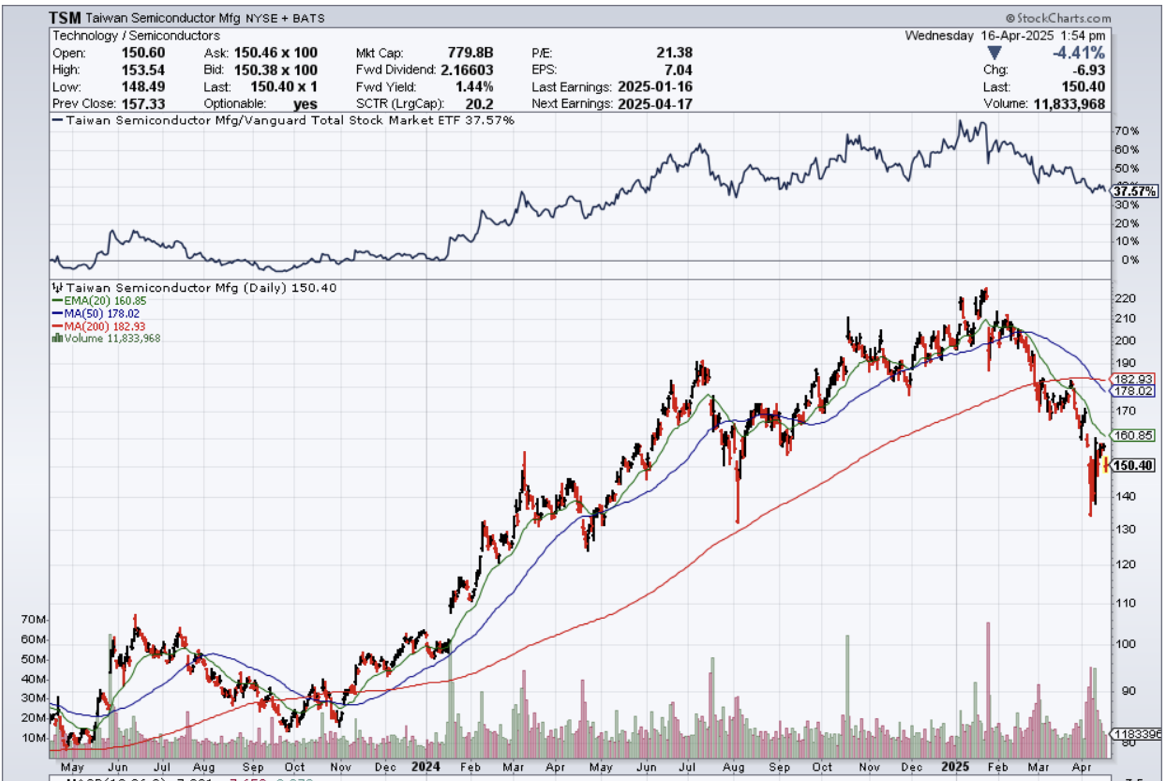

Because TSMC’s chipmaking equipment includes U.S. technology, the company has complied with U.S. trade restrictions on Huawei and the shipment of advanced chips to China. That has left Chinese companies increasingly reliant on domestic foundries like Semiconductor Manufacturing International Corporation.

Nevertheless, SMIC is under its own export controls, which prevent it from accessing some of the world’s most advanced chipmaking equipment.

Are export controls working?

Chinese chip makers won’t need to immediately fill this H20 demand thanks to stockpiles and previous export exemptions and loopholes.

The U.S. government’s aggressive policy against the semiconductor industry is backfiring.

It is interesting that the Federal government never takes into consideration that loopholes and workarounds are possible and what the aftereffects are.

Sanctions can usually be subverted by using a third country to move the goods, and that is what we are seeing.

The end result is higher prices for all.

In general, an increase in the price of semiconductor chips would result in anything tech-related going up in price, and that is after a generation of deflation made devices cheap.

This also raises the price of doing business in AI. The GPUs needed for AI data centers will become more costly.

I could envision the future where harnessing AI software might be reserved for the well-off, because it won’t be cheap to use.

Each pressing day, the cost of business goes up as the globalization trends from post-World War 2 are being ripped to shreds by the existing administration.

Deglobalization is painful for the average person, but when you add on a tech sector in dysfunction, it really turns the screws on the investors.

What’s the end result?

In the short-term, semiconductor stocks will cool off because government obstruction means it is way harder to do business, let alone at profitable prices.

This restriction, this tariff, this rule, this forced export control, and the circus keep going with corporate management wishing one day to operate in a stable business environment.

Nothing is stable about the business environment now, forcing investment dollars to the sidelines.

In the short-term, sell any bear market rally in chip stocks.

Mad Hedge Technology Letter

April 16, 2025

Fiat Lux

Featured Trade:

(AMERICAN TECH ABLE TO OUTFLANK)

(NVDA), (TSM), (AAPL)

I understand that the U.S. administration wants to bring back American manufacturing, but that will not include Silicon Valley manufacturing.

There is a higher likelihood that if China is a no-go zone, American tech companies will venture out to a low-tariff, cheap labor country to continue their path to profits.

If you look through the numbers, it doesn’t make sense for American tech companies to manufacture goods in America.

The costs are too prohibitive.

Silicon Valley tech firms that are public on the New York markets have a fiduciary responsibility to shareholders to sustain short-term profits.

There is no mandate stating that these American tech companies must be manufactured in any specific sovereign country.

Silicon Valley companies are global, and American jobs lose out because of that.

This is a tough nut to crack because wages in rich Western countries dwarf the nominal amount in more affordable places.

U.S. Commerce Secretary Howard Lutnick said during an interview that the (China tariff) move was temporary.

Instead, he explained, tech products will be tariffed as part of the administration's planned duties on semiconductors, which could be announced later this week.

It's not just about timing. Companies would also need the workers to build devices.

While there's a degree of automation possible and while many of the components needed are made in the US, there's still a need for tens of thousands of trained electronics assemblers willing to work long, arduous hours in highly repetitive tasks.

Companies including Nvidia (NVDA), TSMC (TSM), Apple (AAPL), and others have announced increased investments in the US to win over Trump and avoid tariffs.

Nvidia said it will produce $500 billion in AI infrastructure in the US over the next four years through partners including Foxconn (601138.SS), TSMC, and Wistron (3231.TW).

And while that doesn't take away from the fact that the companies are pouring money into the US, it doesn't exactly support the idea that they're moving vast amounts of their manufacturing capabilities to America.

Even if companies brought their manufacturing bases to the US, they'd still have to deal with importing certain parts from abroad.

It's not just Apple that's contending with manufacturing headwinds; everything from laptop makers to display producers would face the same problems if they were to move to the US.

According to some estimates, prices on devices could double, resulting in demand destruction as consumers seek out less expensive options or hold onto their existing smartphones and computers for longer periods.

While it's unlikely manufacturing is coming back to the US, there's still plenty of uncertainty about how tech companies and consumers navigate the next four years of tariff shocks.

The biggest winners appear to be Vietnam or India, and much of the American tech manufacturing has their sights set on these places to reduce costs.

In short, this won’t destroy American tech and their shares will outperform in the long run, but in the short-term, it hurts, because it puts doubt into where they will produce their gizmos and gadgets.

At the very least, this gets American tech out of China, and I believe the federal government would be happy if businesses migrated to a more neutral country, even if they don’t come back home.

Either way, after this all blows over, there will be a great buying opportunity in American tech companies, which will all be trading at a discount.

Mad Hedge Technology Letter

April 14, 2025

Fiat Lux

Featured Trade:

(BIG TECH ANXIOUS FOR CLARITY)

(MSFT), (AAPL), ($COMPQ)