Mad Hedge Technology Letter

July 10, 2024

Fiat Lux

Featured Trade:

(GERMANY BRINGS DOWN BITCOIN)

(BTC), ($COMPQ)

Mad Hedge Technology Letter

July 10, 2024

Fiat Lux

Featured Trade:

(GERMANY BRINGS DOWN BITCOIN)

(BTC), ($COMPQ)

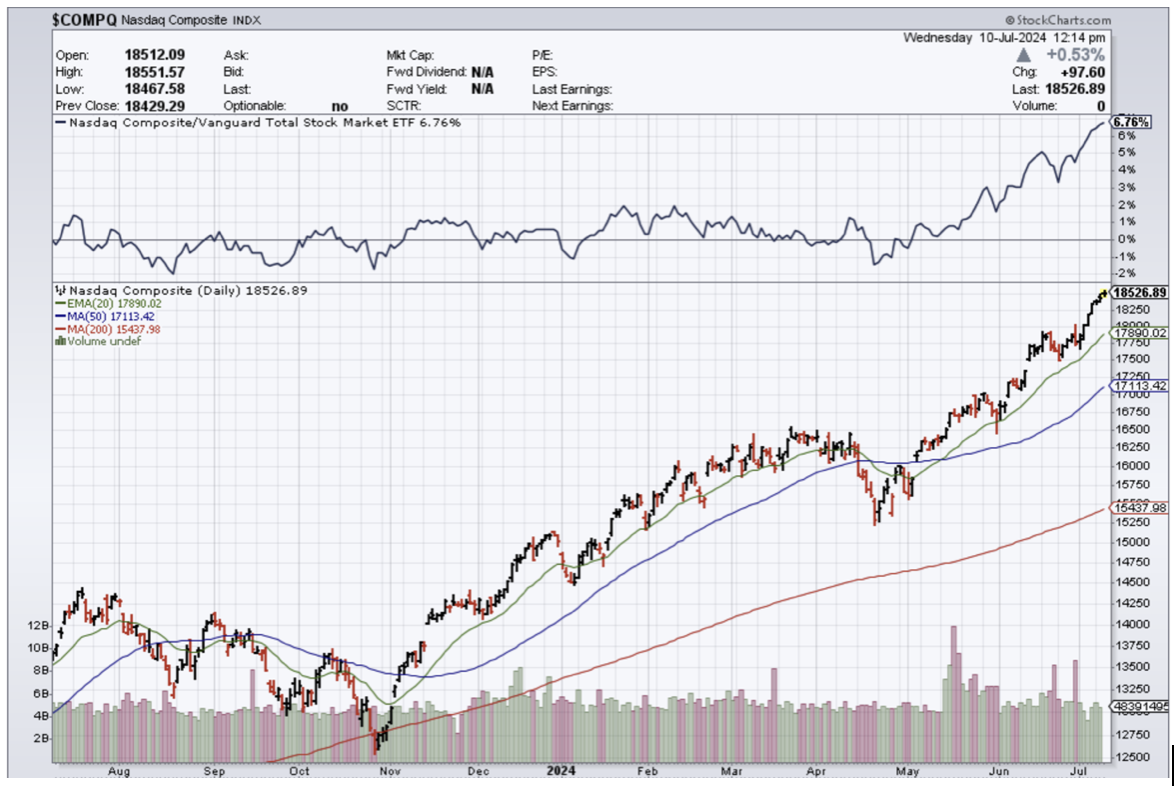

The German government unloading hundreds of Bitcoin (BTC) shows how a random event can reverse positive sentiment.

Technology stocks ($COMPQ) aren’t immune to this type of price action and as we inch closer to the election in November, get prepared for the likelihood of wonkiness to increase.

Luckily enough, the onslaught of regulatory attacks from all sorts of governments has more or less been priced into tech stocks.

A billion fine here or there for many of these tech titans is just a drop in the ocean.

Even political events now do little to sway tech stocks, because many events are just ephemeral in nature and don’t change the trajectory of tech.

Bitcoin isn’t necessarily directly important to tech stocks but operates in parallel.

It is true that there is a lot of crossover between talent pools in the labor forces. Everyone working in Google and Apple knows people working in Bitcoin and vice versa.

More often than not big tech has acted as a feeder source to fill position at Bitcoin and crypto companies.

For weeks now, Germany’s government has been selling hundreds of millions of dollars worth of Bitcoin — and it’s been a key factor behind the cryptocurrency’s intense sell-off.

Last month, the German government began selling Bitcoin from a wallet operated by the country’s Federal Criminal Police Office.

They also sold 900 bitcoins in June.

Last week, the government sold an additional 3,000 bitcoins worth roughly $172 million. Then on Monday, German police sold a further 2,739 bitcoins or $155 million worth of the cryptocurrency.

Bitcoin prices have also been under stress from the payout of billions of dollars worth of digital currency from the collapsed bitcoin exchange Mt. Gox — which went bankrupt in 2014 — to creditors.

A trustee for the Mt. Gox bankruptcy estate has started making repayments in bitcoin and bitcoin cash to some of the creditors through a number of designated crypto exchanges.

Bitcoin’s price is still up a good 89% in the last 12 months.

In January 2024, police in the eastern German state of Saxony announced the seizure of close to 50,000 bitcoins, worth around $2.2 billion at the time.

Today, Germany’s BKA holds roughly 32,488 bitcoins. At current prices, the government’s holdings are worth roughly $1.9 billion.

Although it might feel like a one-off, I do believe governments around the world will be in a position to confiscate more crypto in the future.

This could end up government owning more and more of the finite Bitcoin supply in circulation and could lead to regulation taking a backseat.

The golden goose won’t be killed if the government has skin in the game.

Even though this could become an unusual way for governments to onboard themselves into the crypto ecosystem, killing crypto would have a contagion whiplash that can’t be fully quantified as of now.

Uncertainty always tanks the market.

In fact, I believe the drop in Bitcoin from $73,000 to $53,000 is a positive event for investors because they can load up again at cheaper prices.

I believe we are in a goldilocks phase in technology where Bitcoin and tech stocks grind higher.

Temporary events that drop tech stocks or bitcoin by 20% are few and far between.

Many tech investors would love a better entry point, and it will truly take a real black swan to knock tech stocks or Bitcoin off their high and mighty perch.

As it stands, expect higher prices in both asset classes.

“If you don't understand the details of your business you are going to fail.” – Said Amazon Co-Founder Jeff Bezos

Mad Hedge Technology Letter

July 8, 2024

Fiat Lux

Featured Trade:

(ARM SHINES BRIGHT)

(ARM), (NVDA), (AMD)

With the US Central Bank’s policy being quite accommodative, this advantageous backdrop has really set the platform for certain strategic tech companies to shine on the public markets.

In particular, chip stocks have been the darlings of the AI revolution and will continue to be in the limelight.

Part of this is about investors not knowing in particular what software firms will benefit from AI.

It is really a crapshoot to know how the software will look like in the future, but investors do know that software will be powered by the backend infrastructure which is why AI chips are fetching a premium at market in today’s stock market.

Once the software part of it starts to reveal itself, then it is highly likely the software winners will start to experience the same sort of price appreciation in shares that AI chip companies are experiencing right now.

That trend reversal is still years off so it is better to spend our energy on chip stocks.

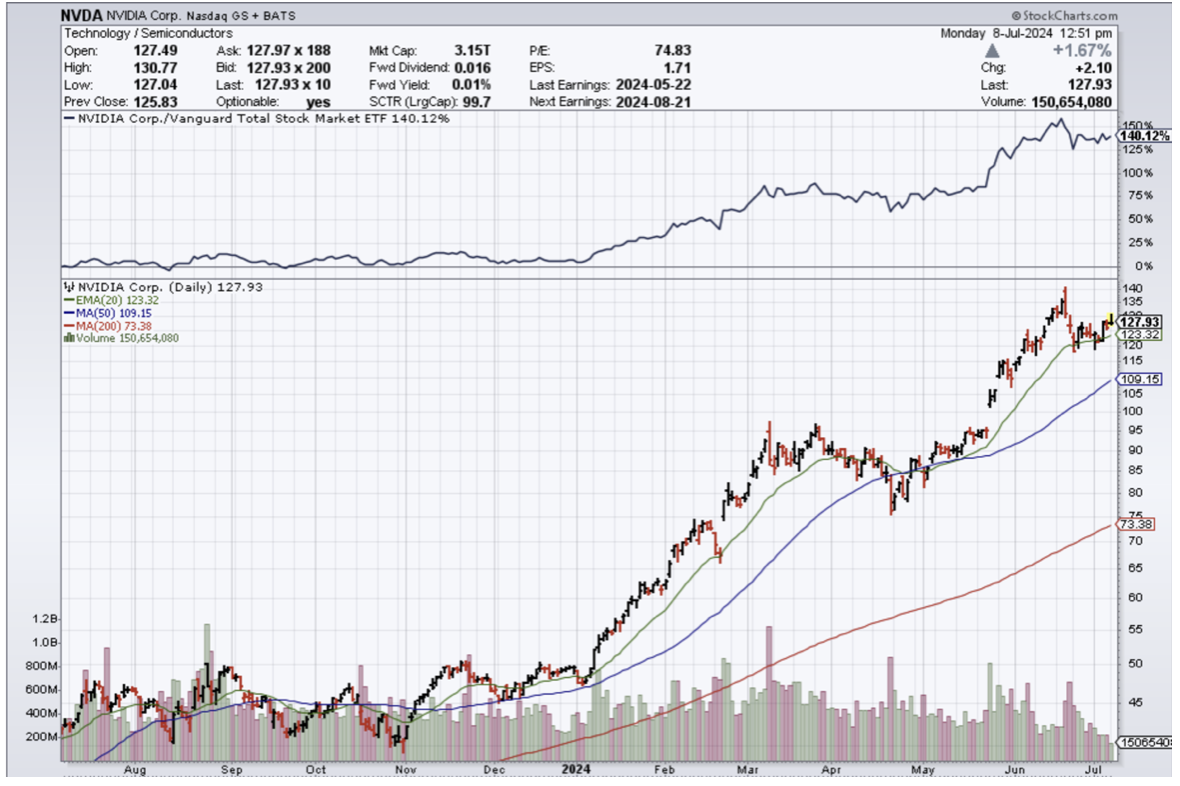

The no-brainers are the likes of Nvidia and AMD, but the lineup is dee.

Look at the 2nd and 3rd tier of chip stocks like British chip company ARM (ARM).

Arm is also right in the mix of the AI boom. The positive market sentiment toward AI advancements continues to propel Arm's stock upwards. Furthermore, the company's former focus on low-power embedded and mobile chips is changing before your eyes. These days, you'll find Arm-based chips all over modern data centers and PC systems.

The broader market dynamics also played a role in Arm's rise. A softer-than-expected jobs report in May fueled hopes for potential interest rate cuts by the Federal Reserve, which would benefit growth stocks. The semiconductor sector is full of growth stories, including Arm.

Industry news also contributed to Arm's strong performance. Reports that Taiwan Semiconductor Manufacturing was investing in extreme ultraviolet lithography suggested a robust demand for next-generation chip technologies. As TSMC is a leading manufacturer of Arm-based chips, this investment indicated a positive outlook for Arm's future growth.

Arm's strategic positioning in the AI ecosystem highlights its potential for sustained growth. The company's advanced v9 architecture and its power-efficient processor platforms are increasingly interesting to major industry players, strengthening Arm's competitive edge in the semiconductor market.

ARM and its ticker symbol were added to the Nasdaq-100 Index on June 24.

This move guarantees more capital flow into ARM as it becomes part of a bigger ETF meaning pension and institutional money will own a piece of ARM and help the stock rise.

Arm's rapid inclusion in the index after an initial public offering last September reminds investors of its growing importance in the global technology ecosystem. As CEO Rene Haas highlighted in that announcement, this achievement validates Arm's business strategy and its critical role in providing foundational compute solutions for AI workloads.

Don’t forget that ARM agreed to be purchased by Nvidia which speaks volumes of what Nvidia believes about ARM.

Unfortunately for both, the deal was shut down due to regulatory issues, and imagines the future trajectory of ARM if that deal went through.

In the past 365 days, the stock is up over 200% and just looking at a 2024 chart, readers can understand how investors have complete belief in the future of ARM.

ARM will continue to maintain an important position in the future of AI and they are a juicy takeover target.

I do believe that AI stocks like ARM will continue to grind up, but we are inching closer to a point where investors will take profits before the next leg up.

Mad Hedge Technology Letter

July 5, 2024

Fiat Lux

Featured Trade:

(EXPENSIVE ENERGY A BIG WORRY FOR THE FUTURE OF AI)

(AI)

One of the forgotten risks of AI is the energy capacity situation in the United States.

Many people forget that AI will require immense energy with a hoard of energy-guzzling data centers to facilitate the next tech revolution.

Many consumers have come to realize how the cost of energy has skyrocketed lately and no doubt the interest rates cut next year might turbocharge commodity prices around the globe.

There is an increasingly real chance that Silicon Valley might not be able to afford AI simply because the costs of energy will deem the AI concept unworthy.

Green energy hasn’t developed as fast as many experts once thought and the United States is still very much dependent on fossil fuels to facilitate tech and business in general.

A pressing question that is popping up is whether the United States can deliver the energy capacity that AI chips demand.

The question is hard to dissect because the situation is always changing.

Numbers need to make sense just like how builders build when they think they can sell their houses and apartment for a profit to the end buyer.

The military conflict in Eastern Europe has forced German manufacturing to deindustrialize because producing without that cheap Russian energy is loss-worthy. AI could follow a similar pattern.

The data grid will become strained but by how much is the next most important matter.

A ChatGPT query, on average, requires almost 10 times as much electricity to process as a Google search does.

The rise of generative AI coincides with a heightening of other factors increasing energy demand, from the electrification of transportation and infrastructure to the on-shoring of US manufacturing. Adding yet another acute demand: AI systems need power all the time.

Critics of AI fanaticism point to potential wastefulness and this could end up morphing into a government regulatory quagmire like so many industries that are overburdened by government agency overreach.

If in the case, the energy demands spiral out of control with everyone going the AI route with every country building AI data centers, the exploding costs will mean that tech won’t be able to profit from AI as quick as it wants.

Many analysts are already raising the flag as to whether all these billions poured into AI investments will really pan out or not. AI isn’t free to produce but shares of it are priced as such.

Much of this hot money is migrating into companies that haven’t proven anything or never even turned a profit, look at OpenAI, it started out as a non-profit.

The issue I have is that generative AI is priced to have zero pushback of its revenue trajectory and I do believe that is wrong.

When there is a pullback, it will be deep and sharp even if not long.

I believe that would be a healthy event for AI because the stock shares of AI have gone parabolic when there isn’t much meaningful follow-through to the underlying business models.

On top of that, generative AI is programmed to be ultra-left-leaning on the social spectrum which could cause conflict down the road.

In short, ride up the momentum until the wave crashes, but watch out for the canary in the coal mine which will bring attention to a deep dip in AI shares.

Mad Hedge Technology Letter

July 3, 2024

Fiat Lux

Featured Trade:

(SHOULD I INVEST IN AI CHIPS OR AI SERVERS?)

(SMCI), (NVDA), (DELL)

The AI server market is booming and so are the AI chip markets.

I’ll talk about 2 prestigious companies right in the mix of things.

For long-term portfolios, it’s essential to not miss out on these supercharge growth companies.

I just don’t think that average investors will be able to make up the performance if they miss the boat of these 2 companies. The law of large numbers will just put you too far behind.

All the hot new money is going into AI which adds to the momentum of the share price trajectories.

Even the old money, after not being convinced by Bitcoin, is starting to come around to AI partly because most of the companies involved in AI are publicly listed companies on the New York Stock Exchange.

It makes it a lot easier when the source of exponential growth isn’t on some alternative exchange in some alternate currency in some backwater jurisdiction.

With a few clicks and moving a few dollars here and there, investors can be part of the AI future whether it be in AI chips or AI servers like the companies I am about to talk about.

What up with Nvidia?

Nvidia (NVDA) dominates an impressive 94% of the AI chip market. It’s basically a monopoly or close to it.

Revenue is rising a stunning 262% year over year.

Even more interesting, emerging growth avenues in the nascent AI market indicate that Nvidia could end up doing even better than that.

For instance, governments are also betting the ranch on AI and this stable source of revenue will highly likely grow substantially for the foreseeable future.

Nvidia's customer base is diversifying beyond the major cloud infrastructure providers that have been deploying its chips in large numbers to train and deploy AI models.

Spending on AI chips is expected to grow more than 10-fold over the next decade, generating $341 billion in revenue in 2033 compared to $23 billion last year.

Nvidia should remain the Tom Brady of AI stocks as the race to develop AI applications by companies and governments alike has created a secular growth opportunity.

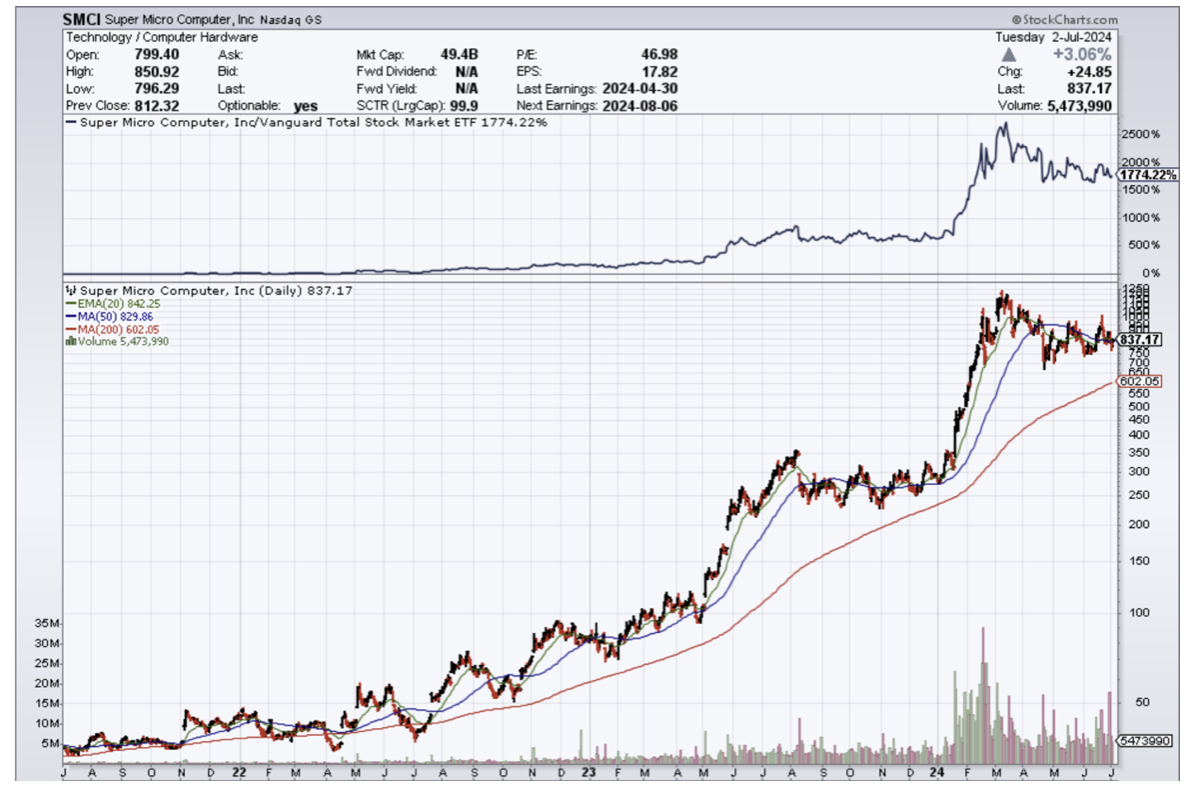

What about Super Micro Computer?

Supermicro's future prospects are attached to some extent with that of Nvidia’s.

Data center operators require server rack solutions of the type that Supermicro sells to mount the processors sold by Nvidia and other chipmakers.

Revenue jumped 200% year over year and Supermicro isn't all that far behind Nvidia when it comes to how AI has supercharged its fortunes.

I expect its top line to nearly double over the next couple of years.

Demand for AI servers is expected to expand at a compound annual rate of 25% through 2029.

Supermicro is growing at a faster pace than the AI server market right now. As it turns out, its growth is faster than that of more established companies such as Dell.

How to invest?

Supermicro is cheaper than Nvidia and Nvidia’s run-up to a more than $3 trillion market valuation has got to scare some people with sticker shock.

People with a time advantage of more than a few years should invest in Super Micro, whereas investors looking for that quick sugar high should buy the dips in Nvidia.

In short, anyone under the age of 40 and many years in front of them should invest long-term in Super Micro at a market cap of $50 billion. With Nvidia, I could easily see its market cap climbing to $4 trillion soon, but a wicked pullback would mean its market cap going from $4 to $3 trillion.

Either way, these are two tech firms with great prospects in the current and future.

“Freedom is never more than one generation away from extinction. We didn't pass it to our children in the bloodstream. It must be fought for, protected, and handed on for them to do the same.” – Said Former US President Ronald Reagan