Mad Hedge Technology Letter

May 13, 2024

Fiat Lux

Featured Trade:

(BUY THE TOURIST PLATFORM TECH STOCK)

(ABNB), (EXPE)

Mad Hedge Technology Letter

May 13, 2024

Fiat Lux

Featured Trade:

(BUY THE TOURIST PLATFORM TECH STOCK)

(ABNB), (EXPE)

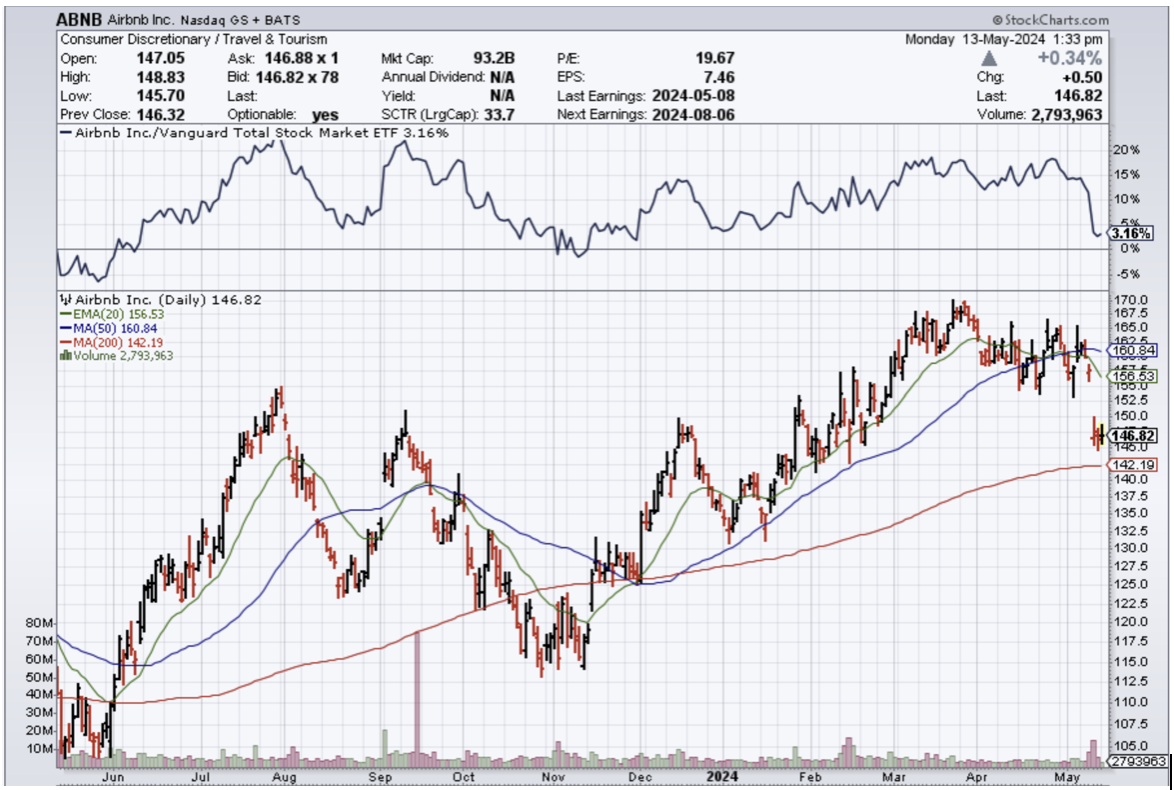

Any type of selloff in Airbnb (ABNB) shares will be short-lived as we approach the summer Olympics and European soccer summer tournament.

Global Events of a month-long will get people out of their homes and spending their cash.

These premium events will move the needle for Airbnb revenue-wise in Europe.

The heart of world travel is Western Europe so it’s convenient that these mega-events are in France and Germany and not in some backwater.

Better luck next time if you haven’t locked up your Airbnb in Germany or France by now.

Travelers even have the option to stay through September and enjoy the annual Oktoberfest in Bavaria.

There isn’t lodging to be found in Western Europe in the summer months and even though the economy is starting to weaken around the edges, we are still in for another summer of travel post-pandemic style.

Tourists are splurging like there is no tomorrow held up by the higher income bracket.

Italy is famous for hosting 8 million Americans per year and is otherwise known as Americans' favorite European destination.

That number is poised to balloon to 12 million by 2030 and that means revenue growth for Airbnb as Italian Airbnb’s are rampant everywhere you go in Italy.

As for the company, the business model has been doing great ever since CEO and Founder Brian Chesky put a tight leash on expenses after being caught wrongfooted during the pandemic.

The stock sold off on the earnings even with the nice beat and the Mad Hedge tech letter executed a call spread on the underlying shares.

Weak guidance has been a hallmark of this past earnings season as the economy softens.

Management needs a lower bar to jump over for later this year.

Revenue increased 18% year over year to $2.14 billion last quarter, ahead of the $2.06 billion consensus.

The surge in profit margins was due in part to a shift in the Easter holiday to the first quarter, strong interest income, and leverage from its revenue growth and cost discipline.

The stock is now down 13% from its year-to-date peak and at its lowest point in close to three months.

Airbnb competes with hotels and other types of overnight accommodations, but its closest competitors are other home-sharing platforms like Expedia's VRBO.

But Airbnb already dominates the home-sharing niche with a leading market share among those platforms, and the company appeared to strengthen its position in the first quarter. Revenue at Expedia (EXPE) increased 8% in the period, while its B2C division which includes VRBO was up just 3%.

Competitors have been unable to overcome the powerful network effect present on Airbnb's platform, allowing it to continue growing its lead.

The shareholder returns program is beefing up.

The company continues to return capital to shareholders, buying back $750 million in stock last quarter. With $2.5 billion in total share repurchases over the past year,

Airbnb has reduced its shares outstanding by nearly 3% over that period. While 3% might not sound like much, this strategy compounds over time, and Airbnb should be able to increase buybacks as profits grow.

Additionally, the company is benefiting from higher interest rates as it's on track to generate close to $1 billion in interest income this year, giving it a significant boost on the bottom line.

I’m betting on an uptick in shareholder interest in the short term at these price levels.

I was a little uncomfortable chasing it higher from $170, but $150 is more reasonable and I do believe the Fed pivot tailwinds could catapult us into profits with this trade.

“He does not possess wealth; it possesses him.” – Said Benjamin Franklin

Mad Hedge Technology Letter

May 10, 2024

Fiat Lux

Featured Trade:

(CHINESE TARIFFS AT THE FOREFRONT)

(EV)

Tariffs on Chinese EVs skyrocketing by 400% are just another example of the federal government getting in the way once again as the current administration limps to the November starting line.

These levies are directed at everything central to producing EVs like the battery and the car itself.

I understand that the point is to protect EV companies at home, but tariffs don’t work and in almost every case, the end price to consumers rises painfully.

It’s not any better over the Atlantic so this frees us China to innovate and get ahead with government support.

The Chinese are playing the long game.

This review of Chinese tariffs was triggered by the administration before it, and it just smacks of inefficiency to me. It only took 4 years to finish the review as infighting took hold and the glacial pace finally ended with a decision.

In fact, Biden's $7.5 billion investment in EV charging has only produced 7 stations in two years, per Washington Post.

Where did the rest of the money go?

My guess is carrying out a raft of economic surveys isn’t cheap when there are no guard rails in price setting.

Maybe the thousands of consultants giving their 2 cents to keep that bureaucratic machine humming in Washington made a dent with another few billion invoices.

I’ll at least give it to the White House that they were able to produce 7 and not 1 or 2.

A billion dollars per EV charger is not good enough in 2024 while the Chinese forge ahead with their technological prowess.

The Chinese tariff rate on electric vehicles is expected to quadruple from roughly 25% to 100% plus an additional 2.5% duty would apply to all automobiles imported into the US.

The EU launched an EV subsidy investigation in October that may lead to additional tariffs by July as well.

The tariffs would likely have little immediate impact on Chinese firms since its world-beating EV manufacturers have steered clear of the US market due to tariffs.

Its solar companies mostly export to the US from third countries to avoid curbs, with US firms seeking higher tariffs on that trade, too.

The move comes after Biden last month proposed new 25% tariffs on Chinese steel and aluminum.

Protecting the American EV sub-sector feels like a situation in which China is outcompeting American EV companies and the government is directly reacting to that in an emotional way.

My guess is that it won’t work.

China will be able to circumnavigate these tariffs easily. It’s impossible to put the genie back in the bottle once it is out.

The only way American EVs will find a solution is to innovate itself away from the competition and that will be tough with the level of interruption by the Federal government.

Sooner or later, these better-made Chinese cars will find themselves in Europe and America on a grand scale.

If the government would get out of the way, tech companies would be forced to innovate or die.

A main strategy of stopping the Chinese from selling to you is a wack-a-mole strategy and the products will eventually arrive,

I am strongly bearish the American EV sub-sector at this point.

This is another tech sub-sector that has turned stale, similar to the streaming sub-sector where I just took profits in a bearish Roku trade.

Why doesn’t the admin go after the Chinese unrealized profits while they’re conjuring up some more tariffs? I wouldn’t put it past them.

Mad Hedge Technology Letter

May 8, 2024

Fiat Lux

Featured Trade:

(THE TECH STOCK HAS MORE ROOM TO RUN)

(ANDREESSEN HOROWITZ)

There is more room for stocks to extend themselves to the upside, which is great news for many who think we might be reaching the last gasp up in tech.

We aren’t there yet and the longest late-cycle bull market continues.

It certainly isn’t over - we received some timely commentary from one of the most prominent venture capital firms in technology, Andreessen Horowitz.

The company isn’t afraid to tell the truth.

Sometimes that means sticking in where it really hurts like a jab to the gut in an industry where most people get their feelings hurt quite easily.

I understand the bravado partly results from the mountains of success that have preceded them, but nonetheless, it is refreshing to hear from successful people who have their pulse on the tech sector.

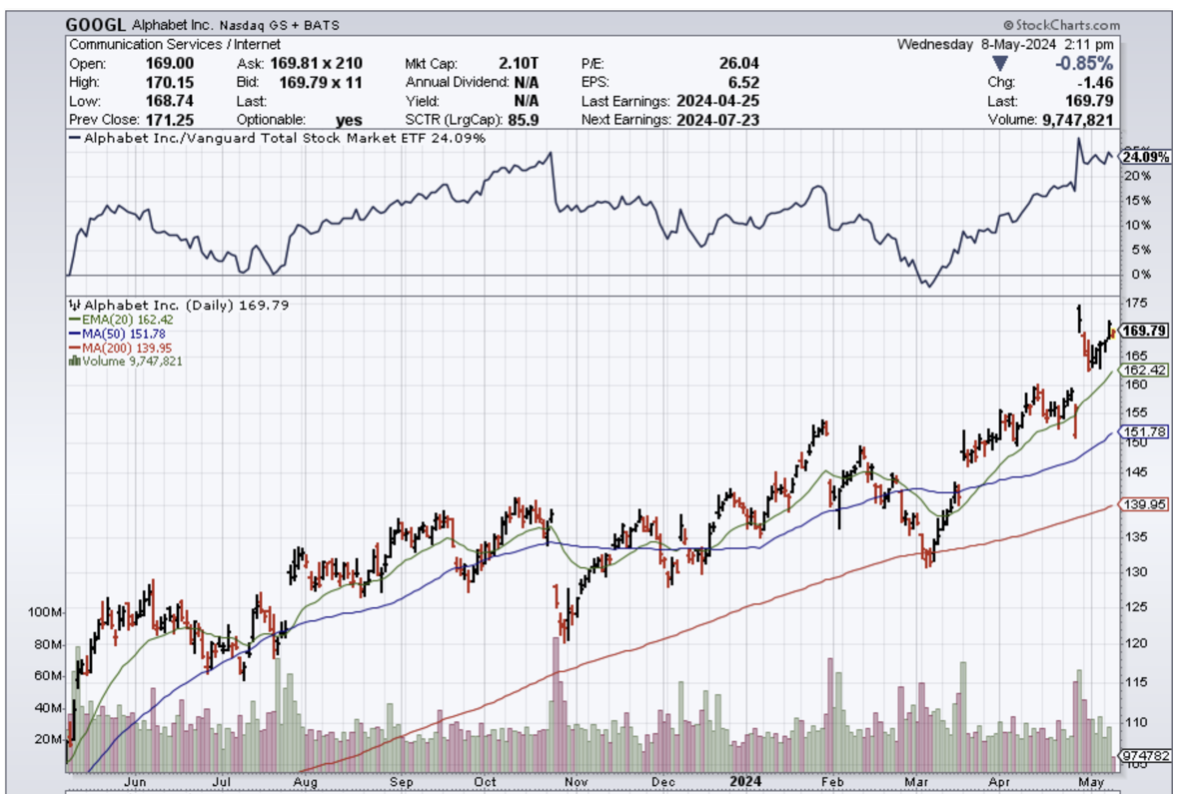

Google might be among corporate America's favorite success stories, but some people aren't convinced Big Tech is operating as efficiently as it could be.

There is still a lot of frittering away in Mountain View, California or that is what Andreessen Horowitz has to say.

The venture capitalist firm said that most Google workers don’t really do anything.

What do I mean by that?

To do nothing “except complete a 10-minute task every now and again” is what they said.

Some workers used their weekdays to learn how to scuba dive or go for a Thai massage because there wasn’t much for them to do in the office.

Companies retaining a bloated headcount with people who don't actually help drive the company forward shows how profitable these companies are.

When push comes to shove and a recession slams us blindly, Google will know what to do with these workers.

The company later said a “bunch of people” in large corporations are working “BS jobs.”

“Anyone who works in a 10,000+ person or larger white-collar job company knows that a bunch of the people can probably be let go tomorrow and the company wouldn’t really feel the difference, maybe it’d even improve with fewer people inserting themselves into things.”

Much of the vendetta against tech workers isn’t all justified, but I do believe it is more about the top 10% carrying the load for the other 90%.

The top end of the talent pool is so brilliant, they are leading $2 trillion companies and that doesn’t happen with a bunch of morons, does it?

However, another trend I have noticed is that America could be running out of talent after exhausting India and China while work visas have never been harder to procure.

After getting rid of the bad workers, will there be those superstars that move the window and that is a big doubt moving forward.

Talking with people in the know, there is great uncertainty with the direction of big tech as nobody understands what will really succeed the smartphone.

The smartphone was that one vehicle of profit that all companies knew they had to make money from and now what is next?

Is it a virtual reality with all those goofy headsets giving people headaches?

Companies are pouring billions into figuring out what the next iPhone is and it’s more like throwing paint on the wall and seeing what sticks.

Luckily, the tech bull market should continue but many companies are facing existential threats due to lack of innovation and lack of top-end employee talent.

If innovation somehow takes a wild turn away from the AI path, many companies could blow up.

Until then, buy the dip in GOOGL until a black swan hits the industry or sub-sector. They have many ways to keep the stock from going down like their newly minted dividend which is a first in the company.

“If you try to do too much, you will not achieve anything.” – Said Confucius

Mad Hedge Technology Letter

May 6, 2024

Fiat Lux

Featured Trade:

(BUFFETT CHIMES IN ON AI)

(BRK/A), (SMCI), (AI), ($UST10Y)

At the once-per-year shareholder meeting for Berkshire Hathaway (BRK/A) in Omaha, Nebraska, the shindig has become a caricature of itself.

A company that does so well, but the leader has self-proclaimed to understand nothing about technology.

It was fascinating to see the Oracle of Omaha Warren Buffett dabble in the cooler talk that is talk about artificial intelligence.

Ironically enough, his pep talk about AI was littered with negatives about the consequences of AI.

Warren Buffett's warning about AI’s potential harm has everything to do with his conservative risk tolerance to not beeline straight to the front of the most modern developments in the tech industry.

He’s late on most stocks but he’s right on them in the end.

It wasn’t too far back when Buffett only would invest in a company as complicated as Coca-Cola, because he famously stated that he doesn’t invest in companies that he doesn’t understand.

Insurance also made Buffett a killing pouring capital into companies like Aflac.

He finally came around to Apple which for better or worse is known as the iPhone company.

His risk tolerance of tech increasing to the almighty smartphone was quite a jump for Buffett that took many years, so don’t expect another leap of faith anytime soon.

In fact, Buffett claiming he doesn’t understand AI too well means there is a lot of capital sitting on the sidelines waiting to enter once they finally do “understand.”

I should also just note the general stockpile of money that has been waiting on the sideline since the Covid-era is enormous.

Any meaningful dip in any meaningful tech company will be met by a torrent of new buying demand.

That’s exactly what happens when the number of great tech companies can be counted on 2 hands.

Almost like what is happening with American restaurants – it’s not that American restaurants are going through a generational renaissance, no, they are packed because so many small restaurants closed after COVID.

Tech is experiencing the same playbook with investor money.

The past 7-12 years have seen the spurring on competition squelched, and the tech industry has never been closer to a full-blown monopoly in some sub-sectors.

Once the bulls get back in control, we are off to the races again, because a few companies move markets now.

That’s what I believe we are seeing in the short-term with the US 10-year inching up only for Central Bank Fed Chair Jerome Powell to deliver us a monumental dovish speech to the sticky inflation we are seeing in numbers now.

Buffett chose to talk about the darker side of AI and the potential for scamming people.

He said that scamming using AI will become a “growth industry of all time.”

Buffett pointed to the technology’s ability to reproduce realistic and misleading content in an effort to send money to bad actors.

Just because we don’t like it, we cannot write it off or afford it as investors.

Readers must deal with AI and the manifestations of it.

One of the big side effects is that it accelerates the winner-takes-all dynamics of tech.

If I were a newbie investor, Super Micro Computers (SMCI) would be on the radar as a powerful growth stock with bountiful potential and exposure to AI.

More tech companies will fail, and they will fail faster, without a trace of even existing sometimes.

It also puts extreme pressure on tech management to implement AI, lose funding, or lose the momentum the business model.

It almost makes tech management over-reliant on AI to fix any and every mess.

The reality is that there will be a lot of losers from AI and punishes companies that never figure out AI.

It is best to identify them before the stock goes to 0.

I don’t necessarily share the same dark outlook as Buffett and I commend him for doing so well on his performance, but when it comes to technology stocks, he shows up late, but it is better than never showing up.