Mad Hedge Technology Letter

March 20, 2024

Fiat Lux

Featured Trade:

(A NEW SET OF CHIPS ARE COMING)

(NVDA)

Mad Hedge Technology Letter

March 20, 2024

Fiat Lux

Featured Trade:

(A NEW SET OF CHIPS ARE COMING)

(NVDA)

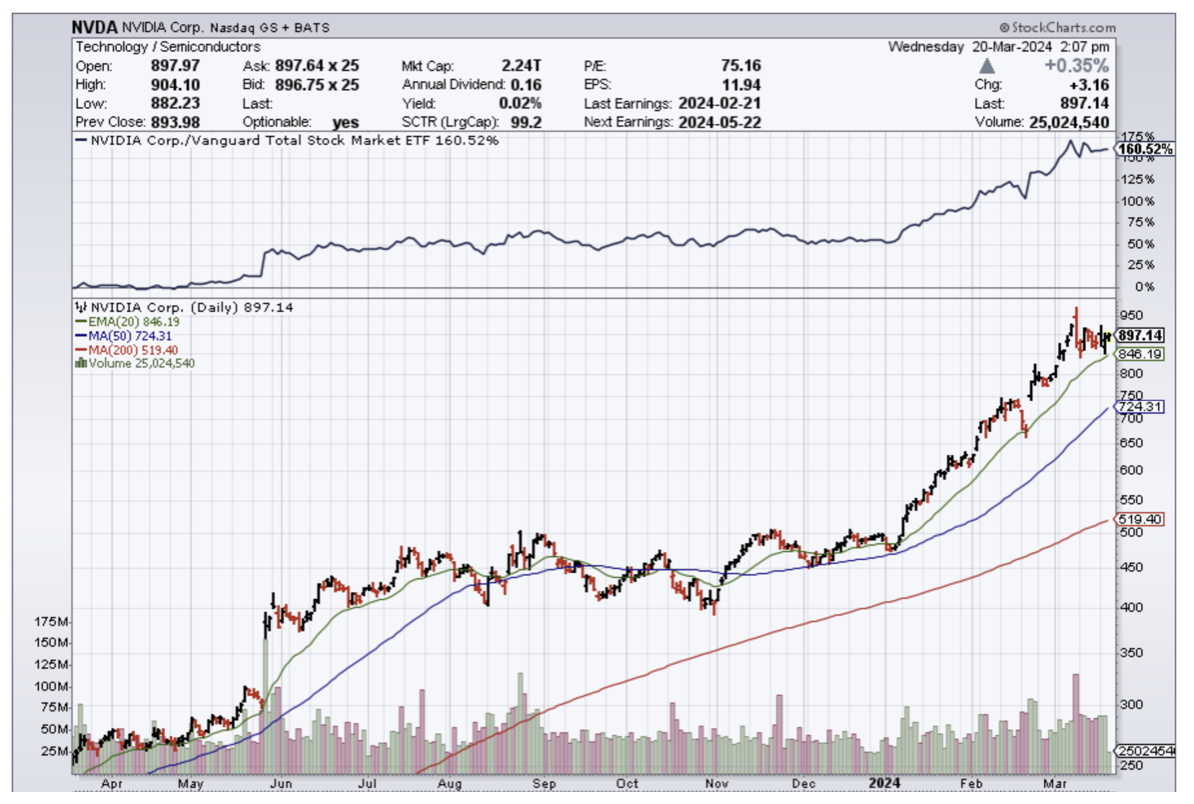

The accolades keep raining down on Nvidia (NVDA) CEO Jensen Huang. I even heard one person say he is the new Steve Jobs.

Those are quite lofty compliments for a guy who has been under the radar for quite a long time. However, he can’t hide anymore as NVDA’s share price has skyrocketed and the valuation today stands at over $2.2 trillion.

NVDA should be at the heart and core of every tech portfolio. They are critical to the facilitation of AI in the present and the future. So when he talks publicly, people listen and that’s what just happened.

Jensen Huang described what he sees ahead for artificial intelligence and Nvidia. He believes it is something so vast and transformative that computing and how we use it will never be the same.

Huang gave the keynote address on Monday to open Nvidia's GTC 2024 conference. Huang focused on what he insisted was the coming transformative influence that his company's Blackwell program of chips and related systems would have on technology and artificial intelligence at the first level and the entire economy beyond.

The audience at the SAP Center in San Jose was waiting for his every word.

Huang focused on Nvidia's new generation of chips and the two factors that make AI work: the training (or programming) that enables the semiconductors to receive data, recognize and organize it, and send it back out to a client in usable form; and the brute computing power to make it all happen.

Nvidia's influence on artificial intelligence is already substantial, thanks to its H100 GPU chips and related products which power most AI applications now.

The Blackwell platform, expected to be available toward the end of 2024, will use a new series of chips, the B200 family, combined with new components and software to get the most out of the chips.

The goal is to let a user pack more training onto chips so these chips and the components built around them can recognize data more quickly.

The chips are supposed to access more inference — the capacity to know how to analyze the data to produce usable conclusions to queries and questions.

Blackwell is supposed to offer 4 times the capacity of Nvidia's wildly popular A100 chip to program the training aspects in the chips themselves and 30 times the inference output.

Add more of these chips into the system, and you can gather more data and translate it into more usable information almost instantaneously.

Nvidia is developing other equally fast components into the platform system so that the information flows in and out swiftly and, as importantly, smoothly, all the while using a lot less power.

Many can see how these cut across a slew of industries by making them more productive and efficient. The head and brains of an operation for most corporations will be an algorithm facilitated by an Nvidia chip.

The demand for these products will be out of the roof coming from industries like logistics, industrial, transport, consumer products, finance, and so on.

Nvidia will supercharge business everywhere.

I will keep tabs on how the Blackwell platform performs, but it is hard to envision it failing because Nvidia’s reputation precedes itself.

This also could trigger another leg to the bull market in tech stocks.

“Economies of scale are a good thing. If we didn't have them, we'd still be living in tents and eating buffalo.” – Said JP Morgan CEO Jamie Dimon

Mad Hedge Technology Letter

March 18, 2024

Fiat Lux

Featured Trade:

(APPLE LOOKS FOR A WAY BACK)

(AAPL), (GOOGL)

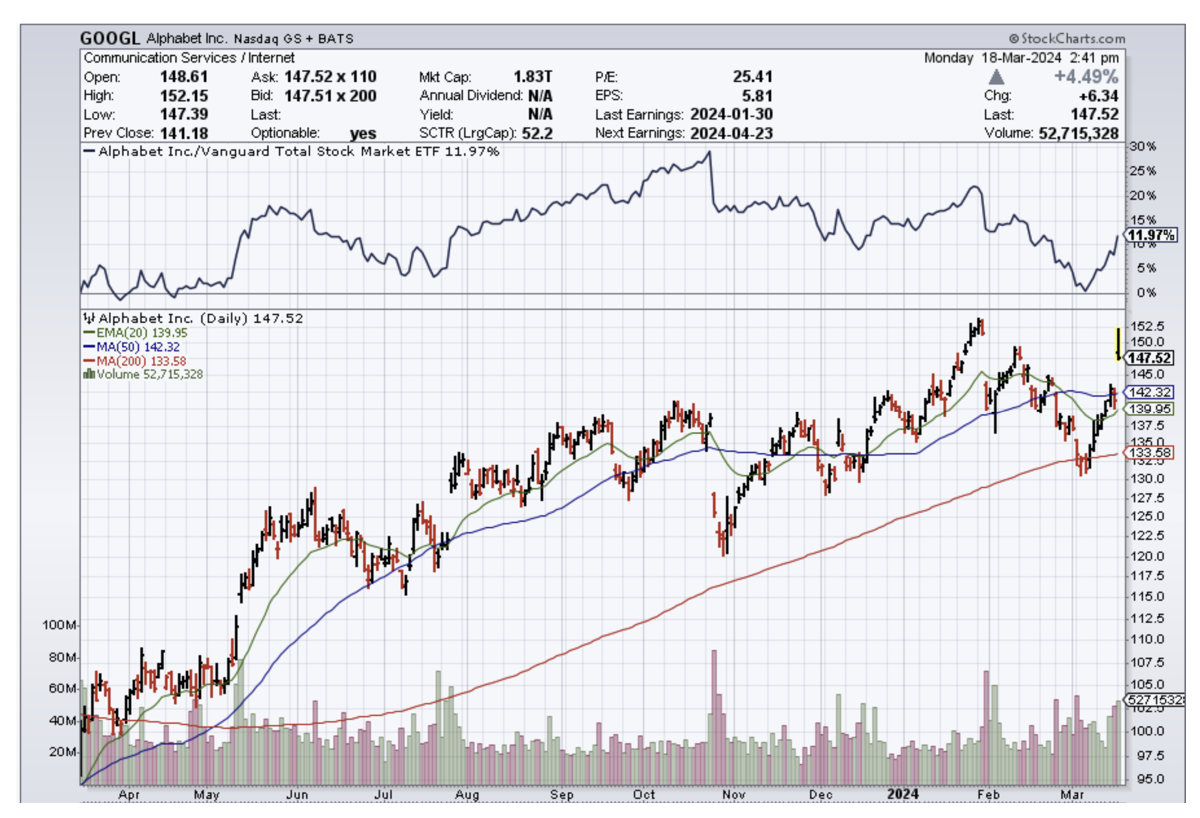

Apple (AAPL) is in active negotiations to support iPhones with Google's (GOOGL) generative artificial intelligence engine and this is big news out of California.

The possible deal signals the sad truth that Apple's AI technology remains inferior to Google's suite of generative AI tools.

The move by Apple is a sign that management is in crisis mode in Cupertino, California.

Management has finally figured out that there is a real threat of getting left behind and steps are being taken to ameliorate this.

To be honest, I have not heard much about Apple’s AI exploits and I boil it down to Apple not having much of anything to show for.

Apple halted its long-rumored “Project Titan” work on developing an electric car.

The company reportedly announced the news internally and said many people in the 2,000-person team behind the car will shift to generative AI efforts instead.

Clearly, there is a strategic shift going on at Apple and management came to a conclusion the only way forward is to collaborate with other tech behemoths.

They are redeploying a 2,000-person team to go into some AI venture and onboarding Google’s AI software will be the next project for this team to work on.

It’s quite disappointing that Apple hasn’t been able to achieve any in-house headway into one of the biggest sub-sectors in technology today.

Apple needs to double down and hire another 2,000-person team of AI specialists to get to the root of the problem.

After the iPhone, many want to know what is next for Apple and CEO Time Cook has had time but an incomplete road map.

The two companies are in active negotiations to let Apple license Gemini, Google's set of generative AI models, to power some new features coming to the iPhone software this year.

Apple also recently held talks with OpenAI revealing their desperation to hang on to any olive branch extended to their future business.

There is even a possibility that an agreement between the two mega-tech giants will not materialize, and/or Apple will seek multiple partners to build a chatbot.

A deal would give Gemini a key edge with billions of potential users.

However, the report said, "the two parties haven't decided the terms or branding of an AI agreement or finalized how it would be implemented."

Google must feel vindicated after their AI tools went awry.

Even with a lot of rust around the edges, Google’s set of AI tools are still highly valued and sought after.

This is a major victory for Google and boosts the profile of their AI team and in-house expertise.

The AI wars will leave many other tech companies behind and Apple is ensuring itself it gets a seat at the table as the smartphone business gradually declines.

Apple has been lean any meaningful AI announcement and although this doesn’t put them back into the driving seat, it really is a breath of fresh air to see Tim Cook finally wake up and realize the company he shepherds is lost.

The iPhone is not the future and this is a painful way of telling shareholders that they have been asleep at the wheel.

In the short term, Google and Apple would be worth a trade.

“The most important investment you can make is in yourself.” – Said American Investor Warren Buffett

Mad Hedge Technology Letter

March 15, 2024

Fiat Lux

Featured Trade:

(POACHING FOREIGN TECH)

(TSLA), (OCDO.L)

Europe is reeling and now it is becoming Silicon Valley’s playground.

The evidence is all over Europe and quite clear-cut at this point.

The royal 7 from the likes of Tesla (TSLA) and Apple (APPL), who have been responsible for most of the stock market gains this year, are leading the charge to cherry-pick the best tech companies in Europe.

Many European companies are now waving the red flag amid commercial electricity costs spiking 100% in many Western European countries.

The unrelenting electricity increase has caused a mad rush to relocate the best European talent to the United States.

Or, if they don’t relocate out of their own will, many are buy-out targets just like the recent news of British online grocer Ocado.

They are on the verge of tasting the sweet hand of acquisitive cash from Amazon (AMZN).

Poached or not poached – Silicon Valley is dominating.

Ocado Group shares jumped the most in more than five years.

Even though the acquisition never came to fruition, this is the type of environment we find ourselves in, as European tech takes the Silicon Valley money before they can go themselves organically without any external help.

Ocado’s stock soared in 2018 on a landmark deal to build warehouses and license software to US supermarket chain Kroger Co., boosting the grocer’s credentials as a technology company. Ocado has partnerships with several grocers, but investor focus has shifted to profitability as demand for automated warehouses slows.

Amazon wasn’t only interested in Ocado, they had to abandon the iRobot deal.

Amazon’s deal to buy Roomba maker iRobot fell apart after iRobot said the deal had “no path to regulatory approval in the European Union.”

iRobot also announced layoffs of around 350 employees, or around 31 percent of its workforce as part of a restructuring.

Ocado has developed, leading automated warehouse technology that could be of great use to Amazon if it tried to take over the European supermarket industry, which it might.

Many American tourists might experience how outdated and obsolete many European supermarkets are these days.

On the corporate side, when I talk to many European workers on the ground in Milan and Brussels, the consensus is that finding a job at an American big tech firm is considered the proverbial golden paycheck.

European counterparts are mired in inefficiency and unproductivity, and the politicians who exist as 27 European Joe Bidens are ruthlessly driving the industry into the ground by taxing and regulating the hell out of them.

European workers also take 2 months of vacation every year along with 15 to 20 federal holidays per year.

When I read the tea leaves, the next expansion of Silicon Valley is to gobble up anything of perceived value in Europe and anything in any European Union country is fair game.

This buying spree could trigger another leg up to big tech and expand margins.

American tech possesses the powerful balance sheets to wield around the world and dominating the European supermarket industry would add to the top line.

Amazon has already forayed into the food industry with Whole Foods in America so this should be viewed as something similar to that.

Look for big tech to enter strategic European industries and eventually buy something like Manchester United or any other high-quality asset.

“Computers are useless. They can only give you answers.” – Said Artist Pablo Picasso

Mad Hedge Technology Letter

March 13, 2024

Fiat Lux

Featured Trade:

(COGNITION AI IS THE TALK OF THE TOWN)

(AI), (NVDA)