Palantir’s (PLTR) performance in the US is nothing short of extraordinary, and some would even say scintillating.

I’ll tell you why.

The numbers on the screen make you giggle like the 70% year-on-year growth in Q4.

It’s almost inconceivable to do what they did and I am referring to signing that many contracts given the way the product is.

We are witnessing a convergence of Palantir’s software products becoming easier to use which is leading to an augmentation of its capabilities, both driven by developments in AI, and large language models.

The heightened demand and ability to meet that demand is something Palantir’s management calls “with a pilot.”

This new piloting approach is what they call boot camp.

They did over 500 boot camps last year.

Palantir’s management travels around the country now convincing CEOs, CTOs, CFOs, and really, whoever has $1 million to buy the software and transform their enterprise by harnessing everything achieved in AI since inception and putting the best people on it.

Palantir then coaches these best employees on how to run data at a boot camp for 10 hours per day until they know it like the back of their hand.

One unique part of Palantir’s business model is their principle of making it known that they are proud of their work on the war front. They are proud to support the US.

Specifically, they are proud to support the US military.

However, this has rubbed some the wrong way like the Europeans who refuse to do much business with PLTR.

PLTR has been unable to make inroads across the Atlantic.

Yet PLTR is proud to have carved out a pivotally crucial role not only in Ukraine, but management is proud that after October 7, within weeks, Palantir is on the ground, and is involved in operationally crucial roles on the software side in Israel.

I know of no other software company in the world that is at the focal point of Ukraine and Israel and it is important for investors to know this before they decide to invest in the company.

This tech company boards the most talented, interesting, and performance-based people in the world.

Some of the numbers that can’t just be ignored are the 55% growth in customer count year-over-year.

This is the early days of generative AI in software products and for Palantir to describe the rocket fuel growth they are experiencing backs up the AI narrative.

For better or worse, the sector is relying on the AI pixie dust to carry the rest of the tech market.

As soon as the market gets wind that AI-based growth isn’t supercharging balance sheets, the tech sector will pull back.

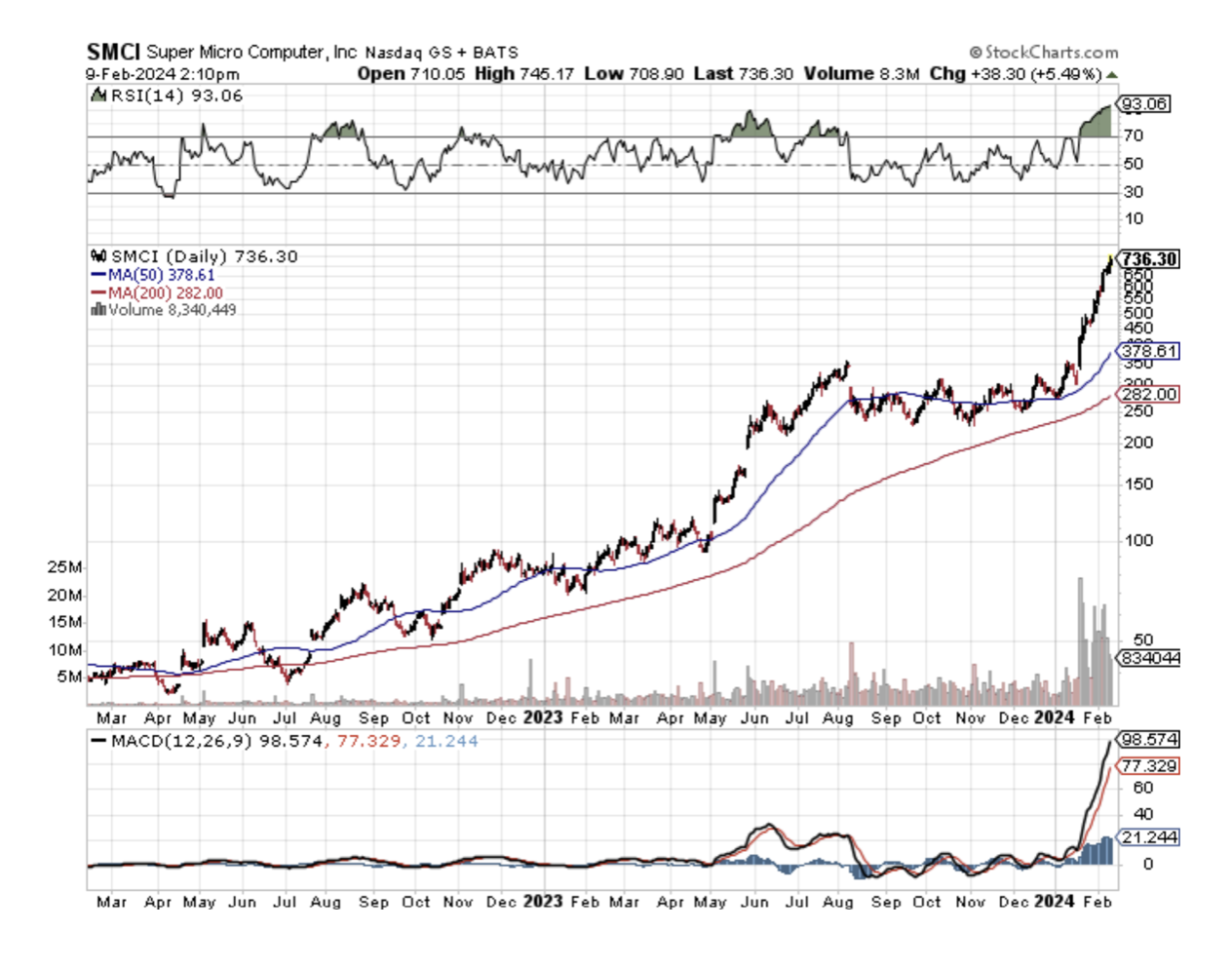

Therefore, it’s highly positive for technology momentum to see stocks like PLTR and chip stocks like Super Micro Computer (SMCI) hit a home run in earnings.

Sadly, Nvidia (NVDA) can’t just carry the load for the entire sector and there needs to be some alternative leadership from other tech stocks connected to the AI story.

PLTR has tripled in the past 365 days and I don’t believe that type of stock performance can continue in the short-term.

The last earnings beat was met with yet another impressive 20% rise in the stock price.

Investors will need to be patient and wait for the stock to pull back otherwise chasing usually ends in tears.

I would advise readers to not chase and wait for big drops in individuals' names to put money to work.